Navigating the Road Ahead: Your Ultimate Guide to the Five-Year Car Loan

Navigating the Road Ahead: Your Ultimate Guide to the Five-Year Car Loan Carloan.Guidemechanic.com

Buying a car is one of the most significant financial decisions many of us make, second only to purchasing a home. In today’s market, the five-year car loan, often referred to as a 60-month auto loan, has become incredibly popular. It strikes a balance for many buyers, offering manageable monthly payments while still allowing them to drive a newer, more reliable vehicle.

But is a five-year car loan the right path for you? While it presents an attractive option, understanding its nuances, benefits, and potential drawbacks is crucial. As an expert blogger and professional SEO content writer, I’ve seen countless individuals navigate this very decision. This comprehensive guide will equip you with all the knowledge you need to make an informed choice, avoid common pitfalls, and secure the best possible deal.

Navigating the Road Ahead: Your Ultimate Guide to the Five-Year Car Loan

What Exactly is a Five-Year Car Loan?

At its core, a five-year car loan is a financing agreement where you borrow money to purchase a vehicle and agree to repay it, plus interest, over a period of 60 months. This extended repayment term distinguishes it from shorter loans, typically 36 or 48 months, and positions it as a middle-ground option compared to longer 72- or even 84-month terms.

The appeal of the 5-year car loan lies primarily in its affordability. By spreading the repayment over a longer duration, the individual monthly payments become significantly lower than those on a shorter-term loan for the same vehicle. This makes newer, more expensive cars accessible to a wider range of budgets. However, this convenience comes with its own set of financial considerations that we’ll explore in depth.

The Allure of the Five-Year Car Loan: Why It’s So Popular

There’s a clear reason why the 60-month car loan has captured the attention of so many car buyers. It addresses several common desires and financial realities, making it a highly attractive option in the competitive automotive market.

Lower Monthly Payments

This is undoubtedly the biggest draw. When you stretch your loan repayment over 60 months instead of, say, 36 or 48 months, your monthly financial obligation drops considerably. This reduction can free up significant cash flow in your personal budget each month.

For many individuals and families, lower monthly payments mean the difference between affording a car that meets their needs – perhaps a safer, more reliable family vehicle or one with better fuel efficiency – and having to settle for an older, less suitable option. It offers immediate budgetary relief, making high-quality transportation more attainable.

Access to Newer, Better Vehicles

With lower monthly payments, buyers often find they can afford a more expensive car than they initially thought. This opens up opportunities to purchase a newer model with advanced safety features, better technology, or enhanced performance. The ability to drive a more modern vehicle is a powerful incentive.

Newer cars typically come with manufacturer warranties, reducing the immediate concern for costly repairs. This peace of mind, combined with the latest amenities, significantly enhances the driving experience. A five-year loan can be the bridge to owning a vehicle that truly aligns with your desires and lifestyle.

Longer Time to Pay Off

The extended repayment period provides a longer runway to pay off your debt. For those who anticipate stable income over the next five years, this can feel less financially constraining than a rapid repayment schedule. It allows for more breathing room, especially if unexpected expenses arise.

This longer term also means that the initial financial shock of a large purchase is mitigated. You have more time for your income to potentially grow or for other financial obligations to decrease, making the loan feel more manageable over its lifespan.

The Flip Side: Potential Downsides to Consider

While the benefits are clear, it’s crucial to look at the other side of the coin. Based on my experience, many buyers get swept up by the low monthly payments and overlook the long-term financial implications. A five-year car loan isn’t without its potential pitfalls.

Higher Total Interest Paid

This is the most significant financial drawback. While your monthly payments are lower, you’re paying interest for a longer period. Even if the interest rate is the same as a shorter loan, the cumulative interest paid over 60 months will be considerably higher. This means the total cost of the car will be more.

Think of it this way: you’re essentially paying for the convenience of lower monthly payments through a higher overall price for the vehicle. Common mistakes to avoid are focusing solely on the monthly payment without calculating the total interest. Always ask for the total cost of the loan before signing.

Increased Risk of Negative Equity (Upside Down)

Negative equity, often called being "upside down" on your loan, occurs when the outstanding balance of your loan is greater than the current market value of your car. Cars depreciate rapidly, especially in the first few years. With a five-year loan, your repayment schedule might not keep pace with this depreciation.

Pro tips from us: This risk is particularly high if you make a small down payment or no down payment at all. Should you need to sell or trade in your car before the loan is paid off, you could find yourself owing money on a car you no longer own. This can trap you in a cycle of debt, as the deficit often gets rolled into your next car loan.

Longer Period of Debt

Committing to a five-year loan means you’ll be in debt for that entire duration. This can impact your ability to take on other financial commitments, such as a mortgage, personal loans, or even save for other goals. It ties up a portion of your income for an extended period.

A longer debt term also means less flexibility in your financial planning. Life happens, and unforeseen circumstances can make a long-term debt burden feel heavy. It’s important to consider your future financial goals and how a five-year commitment fits into that picture.

Depreciation vs. Loan Term

Vehicles generally lose a significant portion of their value in the first few years. After five years, your car will likely have depreciated considerably. If you plan to keep the car for the full loan term and beyond, this might not be a major issue. However, if you typically like to upgrade your vehicle every few years, a five-year loan could leave you in a tricky situation.

The sweet spot for trading in a car, financially speaking, is often before its major depreciation hits hard. A five-year loan might push you past this point, leading to less trade-in value when you’re ready for your next vehicle. Always consider how long you truly intend to own the car.

Is a Five-Year Car Loan Right for You? Key Factors to Evaluate

Deciding on a loan term is a personal financial choice. To determine if a five-year car loan aligns with your needs, consider these crucial factors carefully.

Your Credit Score

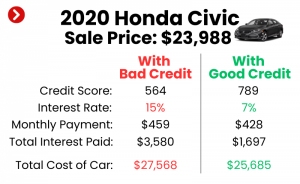

Your credit score is paramount. A strong credit score (typically 700+) will qualify you for the best interest rates, significantly reducing the total cost of your loan. Lenders view borrowers with excellent credit as lower risk, and they reward this with more favorable terms.

Conversely, a lower credit score will result in higher interest rates, making the loan much more expensive over five years. Before applying, it’s always wise to check your credit score and history. Rectifying any errors or making small improvements can save you thousands in interest.

Your Budget and Financial Stability

Can you comfortably afford the monthly payments, along with insurance, fuel, maintenance, and potential repairs, for the next 60 months? A five-year commitment requires stable income and diligent budgeting. Don’t just look at the payment; assess your entire financial picture.

Based on my experience, a common mistake is stretching your budget too thin to afford a car. Always ensure you have an emergency fund and that your car payment doesn’t consume too large a percentage of your disposable income. Financial stability today doesn’t guarantee stability tomorrow, so build in a buffer.

The Vehicle’s Depreciation Rate

Some cars hold their value better than others. Research the specific model you’re interested in to understand its historical depreciation. A car that depreciates slowly will mitigate the risk of negative equity, making a longer loan term less perilous.

SUVs and trucks often have better resale values than sedans, for example. Choosing a vehicle known for its longevity and value retention can make a five-year loan a much safer bet. This foresight can save you from being upside down later.

Your Down Payment Amount

A substantial down payment is one of the most effective ways to offset the risks of a long-term loan. The more you put down, the less you borrow, and the lower your risk of negative equity. A 10-20% down payment is often recommended.

A larger down payment also reduces your monthly payments and the total interest paid over the life of the loan. It shows lenders you are serious and reduces their risk, sometimes leading to slightly better interest rates.

Interest Rates and APR

Always compare the Annual Percentage Rate (APR) from multiple lenders, not just the quoted interest rate. The APR includes the interest rate plus any fees, giving you the true annual cost of borrowing. Even a half-percent difference in APR can add up significantly over five years.

Shop around aggressively for the best rates. Banks, credit unions, and online lenders often offer more competitive rates than dealership financing. Knowing your pre-approved rate gives you leverage at the dealership.

Your Future Plans

How long do you typically keep your cars? If you tend to switch vehicles every 2-3 years, a five-year loan might not be ideal due to the negative equity risk. If you plan to drive the car until its wheels fall off, then a longer term is less problematic.

Consider major life events too. Are you planning to move, start a family, or change careers in the next five years? These events can impact your financial capacity and your need for a specific type of vehicle.

Navigating the Application Process for a 5-Year Car Loan

Once you’ve decided a five-year car loan might be suitable, the next step is to navigate the application process effectively. Being prepared can save you time, money, and stress.

Pre-Approval: The Smart First Step

Pro tips from us: Always get pre-approved for a loan before you step foot in a dealership. This gives you a clear understanding of how much you can borrow, at what interest rate, and for what term. It empowers you to negotiate the car price as a cash buyer, separating the car purchase from the financing.

Pre-approval typically involves a soft credit check, which doesn’t harm your credit score. It provides a concrete offer you can compare against the dealership’s financing options. This competitive edge ensures you get the best deal.

Gathering Necessary Documents

Lenders will require various documents to process your application. Having these ready in advance will streamline the process. Expect to provide proof of income (pay stubs, tax returns), proof of residence (utility bills, lease agreement), identification (driver’s license), and details about the vehicle you intend to purchase.

Some lenders might also ask for bank statements or references. Being organized shows you are a reliable borrower and helps avoid delays.

Comparing Loan Offers

Don’t settle for the first loan offer you receive. Get quotes from at least three different sources: your bank, your credit union, and reputable online lenders. Compare not only the interest rate but also any origination fees, prepayment penalties, and other terms.

Credit unions, in particular, often offer very competitive rates to their members. Online lenders like LightStream or Capital One Auto Finance also provide a convenient way to compare rates from various institutions.

Understanding the Fine Print

Before signing any loan agreement, read every single line of the contract. Look for hidden fees, early repayment penalties, or clauses that allow the lender to repossess the vehicle under specific conditions. If anything is unclear, ask for clarification.

Common mistakes to avoid are rushing through the documents or assuming everything is standard. It’s your money and your commitment, so ensure you understand every aspect of the agreement.

Pro Tips for Securing the Best Five-Year Car Loan Deal

Getting a five-year car loan doesn’t mean you have to settle for average terms. With a strategic approach, you can significantly improve your chances of landing an excellent deal.

Boost Your Credit Score

Even small improvements to your credit score can translate into lower interest rates. Pay off outstanding debts, especially credit card balances, and avoid applying for new credit in the months leading up to your car loan application. A higher score signals less risk to lenders.

Based on my experience, focusing on your payment history and credit utilization (how much credit you’re using vs. available) are the quickest ways to see positive movement. Aim for a credit utilization ratio below 30%.

Make a Substantial Down Payment

As mentioned, a larger down payment is your best friend when taking out a long-term loan. It reduces the amount you borrow, lowers your monthly payments, decreases total interest paid, and builds immediate equity in your vehicle.

Aim for at least 10-20% of the car’s purchase price. If you can afford more, do it. This small sacrifice upfront will pay dividends over the next five years.

Negotiate the Car Price First

When you walk into a dealership with pre-approval, you separate the car price negotiation from the financing. This prevents the dealership from "packing" the deal by offering a seemingly good financing rate but a higher car price, or vice-versa.

Negotiate the best possible cash price for the car first. Once that’s settled, then you can discuss financing, comparing their offer to your pre-approval. This strategy ensures you get the best on both fronts.

Consider a Shorter Term if Possible

While this article focuses on five-year loans, it’s worth asking yourself if you can comfortably afford a 48-month or even 36-month loan. If the difference in monthly payment is manageable, a shorter term will save you a substantial amount in total interest and reduce your time in debt.

Even if you initially apply for a 60-month loan, if your financial situation improves, consider paying extra on your principal each month. This effectively shortens your loan term and reduces total interest without needing to refinance.

Refinancing Options

Life is unpredictable. If your credit score improves significantly after you’ve taken out your loan, or if interest rates drop, you might be able to refinance your five-year car loan. Refinancing can secure you a lower interest rate, reducing both your monthly payment and the total interest paid over the remaining term.

Always investigate refinancing options if you believe you could qualify for better terms. Many online lenders specialize in auto loan refinancing and can make the process straightforward. For more on managing your car expenses, you might find our guide on budgeting for car ownership helpful.

Common Mistakes to Avoid When Getting a Long-Term Car Loan

Even with the best intentions, it’s easy to fall into common traps when financing a vehicle. Being aware of these pitfalls can save you from significant financial headaches down the line.

Focusing Only on Monthly Payments

This is arguably the most common and damaging mistake. While a low monthly payment is appealing, it shouldn’t be your sole focus. A low payment on a long-term loan often means you’re paying significantly more in total interest.

Always ask for the "total cost of the loan" and compare that across different loan terms and offers. Understanding the complete financial picture is crucial for making a smart decision.

Ignoring the Total Cost of the Loan

Beyond interest, the total cost includes the principal amount, any fees, and the impact of depreciation over time. Many buyers overlook how quickly a car loses value, especially when coupled with a long loan term.

Consider how much you’ll have paid for the car by the end of the loan versus what it might be worth. This perspective helps in evaluating the true financial commitment.

Skipping Pre-Approval

As discussed, pre-approval is your superpower in the car buying process. Without it, you’re negotiating blind, giving the dealership a significant advantage. They might manipulate the numbers, offering a low monthly payment but at a higher price or interest rate.

Always secure your financing before you get emotionally attached to a specific vehicle. This puts you in control of the transaction.

Not Factoring in Other Car Expenses

The monthly car payment is just one piece of the puzzle. Remember to budget for insurance, fuel, maintenance, and potential repairs. Newer cars might have lower immediate maintenance costs, but these will increase as the vehicle ages.

Pro tips from us: Neglecting these additional costs can quickly lead to financial strain, even if your car payment seems manageable. Create a comprehensive budget that includes all aspects of car ownership.

Buying More Car Than You Can Afford

It’s tempting to stretch your budget for a fancier model, especially with the allure of lower monthly payments. However, buying a car that pushes your financial limits is a recipe for stress and potential hardship.

Stick to a car that comfortably fits your budget, allowing you to save, invest, and enjoy other aspects of your life. The joy of a new car can quickly fade if it becomes a constant financial burden.

Beyond the Five-Year Mark: What Happens Next?

What happens once those 60 months are up and your five-year car loan is paid off? This milestone opens up new financial possibilities and considerations.

Paying Off the Loan Early

If you’ve been diligent with extra payments or come into some extra cash, paying off your loan early is a fantastic achievement. It frees up your monthly budget, eliminates interest payments, and gives you full ownership of your vehicle.

Just ensure your loan doesn’t have any prepayment penalties before making a large lump sum payment. Most standard auto loans do not, but it’s always worth checking the fine print.

Selling or Trading In

With the loan fully paid, you have clear title to your vehicle. If you choose to sell or trade it in, any money you receive is yours to keep or put towards your next vehicle. This is the ideal scenario, as you’re no longer dealing with negative equity.

However, remember that after five years, your car will have significantly depreciated. Manage your expectations regarding its resale value, and research current market prices.

Maintenance Costs as Car Ages

Once your car is five years old or more, it’s likely out of its original manufacturer’s warranty. This means any repairs will come directly out of your pocket. As cars age, maintenance costs tend to increase.

Factor in potential repair costs into your ongoing budget. Regular maintenance, as outlined in your car’s owner’s manual, can help mitigate larger, unexpected expenses. For more general financial advice, consider resources like the Consumer Financial Protection Bureau (CFPB), which offers excellent guidance on auto loans and other financial products. Visit the CFPB’s website for valuable consumer finance insights.

Conclusion: Driving Smart with a Five-Year Car Loan

The five-year car loan is a popular and viable financing option for many, offering the benefit of lower monthly payments and access to newer vehicles. However, its advantages must be weighed against the potential for higher total interest costs, increased risk of negative equity, and a longer debt commitment.

By understanding the mechanics of a 60-month loan, meticulously evaluating your financial situation, and employing smart strategies like pre-approval and making a substantial down payment, you can navigate the car buying process confidently. Remember, the goal isn’t just to get a car, but to get a car on terms that genuinely serve your long-term financial well-being. Drive smart, plan wisely, and enjoy the journey!