Navigating the Road Ahead: Your Ultimate Guide to Top Car Loan Companies for Bad Credit

Navigating the Road Ahead: Your Ultimate Guide to Top Car Loan Companies for Bad Credit Carloan.Guidemechanic.com

Securing a car loan can feel like an uphill battle when you have bad credit. The conventional wisdom often suggests it’s nearly impossible, or that you’ll be saddled with exorbitant rates. But here’s the truth: getting an auto loan with a less-than-perfect credit score is absolutely achievable. It simply requires a strategic approach, thorough research, and knowing which lenders specialize in helping individuals in your unique situation.

Based on my experience in the automotive finance industry, many people feel overwhelmed and discouraged before they even start. They worry about rejection, hidden fees, and being taken advantage of. This comprehensive guide is designed to empower you. We’ll demystify the process, highlight top car loan companies and types of lenders known for working with bad credit, and provide actionable tips to help you drive away in the car you need, all while building a stronger financial future.

Navigating the Road Ahead: Your Ultimate Guide to Top Car Loan Companies for Bad Credit

Understanding Bad Credit and Its Impact on Car Loans

Before diving into specific lenders, it’s crucial to understand what "bad credit" means in the context of auto financing. Generally, a FICO score below 600-620 is considered subprime, indicating a higher risk to lenders. This can be due to missed payments, defaults, bankruptcies, or a limited credit history.

Lenders view your credit score as a snapshot of your financial reliability. A low score suggests you might struggle to repay a loan, which naturally makes them more cautious. Consequently, if you have bad credit, you’ll likely face higher interest rates and potentially less favorable terms compared to someone with excellent credit. This isn’t to punish you, but to offset the increased risk the lender is taking.

However, having bad credit doesn’t mean you’re without options. A whole segment of the lending industry is dedicated to subprime auto loans. These lenders understand that life happens, and they’re willing to look beyond just your credit score to assess your ability to repay. They often consider other factors like your income stability, employment history, and down payment size.

Key Considerations Before You Apply for a Bad Credit Car Loan

Approaching the car loan process prepared is your strongest asset. Don’t rush into applications without understanding your financial standing and what lenders will be looking for. A little preparation can save you a lot of stress and money in the long run.

1. Know Your Credit Score and Report

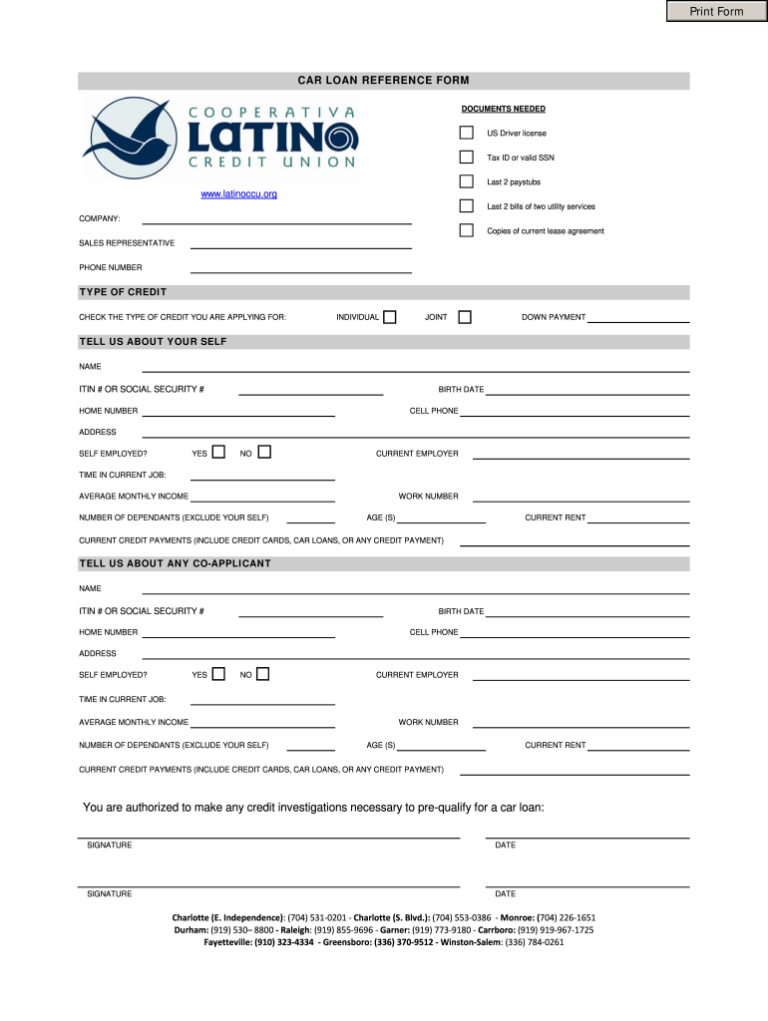

This is your starting point. You can’t improve your situation or explain it to a lender if you don’t know what it looks like. Obtain a copy of your credit report from all three major bureaus (Experian, Equifax, and TransUnion). You are entitled to a free report from each bureau once every 12 months via AnnualCreditReport.com.

Review your reports meticulously for any errors or inaccuracies. Disputing and correcting these can sometimes boost your score surprisingly quickly. Understanding the negative marks on your report will also help you explain your situation to a lender, showing that you are proactive and aware.

2. Create a Realistic Budget

Before you even think about car shopping, determine how much car you can truly afford. This isn’t just about the monthly loan payment. Factor in insurance, fuel, maintenance, and potential repair costs. Lenders will also assess your debt-to-income (DTI) ratio. This compares your total monthly debt payments to your gross monthly income. A high DTI can signal that you’re already overextended, even if you have a stable income.

A good rule of thumb is that your total car expenses (payment, insurance, fuel) shouldn’t exceed 15-20% of your take-home pay. Be honest with yourself about what you can comfortably manage without straining your finances further.

3. Save for a Down Payment

A significant down payment is one of the most powerful tools you have when seeking a bad credit car loan. It directly reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid over the life of the loan. More importantly, it signals to lenders that you are financially committed to the purchase and are less likely to default.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price. If you can contribute more, it will only strengthen your application and potentially unlock better interest rates. Even a few hundred dollars can make a difference.

4. Consider a Co-signer

If your credit is particularly challenged, a co-signer with good credit can significantly improve your chances of approval and secure a better interest rate. A co-signer essentially guarantees the loan. If you fail to make payments, they are legally obligated to step in.

This is a serious commitment for your co-signer, so choose someone you trust implicitly and who understands the responsibility. Ensure they are fully aware of the risks involved. It’s also an excellent opportunity for you to make timely payments and rebuild your credit, benefiting both parties.

5. Understand Your Vehicle Choices

With bad credit, you might not qualify for the brand new luxury SUV you’ve always dreamed of. Be realistic about the type of vehicle you can afford. Opting for a reliable used car that fits within your budget is often the smartest move. This reduces the loan amount and, consequently, your monthly payments and overall interest burden.

Focus on dependable, fuel-efficient models that are known for lower maintenance costs. The goal here is reliable transportation, not a status symbol, at least not yet. Once your credit improves, you can always trade up.

Top Car Loan Companies and Platforms For Bad Credit

Now that you’re armed with preparation, let’s explore the types of lenders and specific companies that are more likely to approve bad credit car loans. It’s not about finding a single "best" company, but rather understanding your options and finding the best fit for your unique situation.

1. Online Lending Networks

Online lending networks act as matchmakers, connecting you with multiple lenders from a single application. These platforms specialize in various credit types, including subprime, and can be incredibly efficient.

How They Work: You fill out one comprehensive application on their website. The network then shares your information (often as a "soft inquiry" initially, which doesn’t harm your credit score) with their vast network of partner lenders. You then receive multiple offers, allowing you to compare terms, rates, and conditions without having to apply to each lender individually.

Pros:

- Convenience: Apply from home, often pre-qualify quickly.

- Multiple Offers: Compare different loan terms to find the best deal.

- Specialization: Many partners specifically cater to bad credit borrowers.

- Time-Saving: Avoid filling out numerous applications.

Cons:

- Information Sharing: Your data is shared with multiple entities.

- Not Direct Lenders: They don’t lend money themselves, they just facilitate connections.

- Potential for Spam: You might receive follow-up calls or emails from various lenders.

Examples:

- Auto Credit Express: Widely recognized for connecting bad credit borrowers with dealers and lenders. They have a strong reputation for helping individuals with challenging credit situations find financing. Their network includes both direct lenders and dealerships with special finance departments.

- MyAutoLoan.com: Another popular platform that provides up to four loan offers in minutes. They work with a broad range of lenders, including those focused on subprime borrowers. They offer resources to help you understand your loan options.

- LendingTree: While known for various types of loans, LendingTree also has an auto loan section. They connect you with multiple lenders, and their service can be useful for comparing offers, even for those with bad credit.

2. Direct Subprime Lenders

These are financial institutions that specialize in lending to individuals with bad credit. They have specific programs and underwriting criteria designed to assess risk differently than traditional banks. They often look beyond just the credit score, considering employment history, income stability, and even the type of vehicle you’re purchasing.

How They Work: You apply directly to these lenders. They have their own underwriting teams that evaluate your application based on their specific risk models. Because they specialize, they are often more flexible than conventional banks.

Pros:

- Specialized Expertise: They understand the nuances of bad credit lending.

- Direct Relationship: You deal directly with the lender.

- Potential for Flexibility: May be more willing to work with unique financial situations.

Cons:

- Higher Rates: Due to the increased risk, interest rates will likely be higher than prime loans.

- Fewer Options: You’re limited to the terms offered by that specific lender.

Examples (Illustrative):

- Capital One Auto Finance: While a major bank, Capital One has a significant presence in the subprime auto loan market. They offer pre-qualification and work with a network of dealerships to provide financing options for various credit tiers.

- Ally Financial: Known for its indirect auto financing, Ally works through dealerships to offer loans to a wide range of credit profiles, including those with less-than-perfect credit. They are a large, established institution.

3. Dealerships with Special Finance Departments ("Buy Here, Pay Here" and Subprime Dealerships)

Many car dealerships have dedicated finance departments that work with a variety of lenders, including those specializing in bad credit. Some dealerships also offer "Buy Here, Pay Here" (BHPH) financing, where the dealership itself is the lender.

How They Work:

- Dealership Finance Departments: These departments act as intermediaries. They submit your application to multiple lenders in their network, seeking approval for you. They often have relationships with subprime lenders that consumers might not easily find on their own.

- "Buy Here, Pay Here" Dealerships: With BHPH, you apply for and receive financing directly from the dealership. Your payments are typically made directly to them, often weekly or bi-weekly. These are usually a last resort due to generally high interest rates and limited vehicle selection.

Pros:

- Convenience: One-stop shop for car and financing.

- Higher Approval Rates (especially BHPH): More lenient credit requirements.

- Immediate Driving: You can often drive off the lot the same day.

Cons:

- Higher Interest Rates: Often the highest rates, especially with BHPH.

- Limited Car Selection: BHPH lots usually have older, higher-mileage vehicles.

- Potential for Predatory Practices: Some BHPH dealers have less-than-transparent terms.

- Less Credit Building (BHPH): Not all BHPH dealerships report payments to credit bureaus, limiting credit-building opportunities. Common mistakes to avoid are not confirming if a BHPH dealer reports to credit bureaus. Always ask this question upfront.

4. Credit Unions

Credit unions are member-owned financial cooperatives that often have more flexible lending criteria than traditional banks. They are known for their customer-centric approach and competitive rates, even for those with challenging credit.

How They Work: You typically need to become a member of a credit union to apply for a loan. Membership requirements are usually easy to meet, such as living in a specific area, working for a certain employer, or joining an affiliated organization. Once a member, you can apply for their auto loans.

Pros:

- Member-Focused: Often more willing to work with members to find solutions.

- Potentially Lower Rates: Can offer more competitive rates than banks, even for bad credit.

- Personalized Service: Often provide more personalized financial advice.

Cons:

- Membership Required: You must meet eligibility criteria to join.

- Slower Process: May not be as fast as online lenders or dealerships.

- Fewer Locations: May have a smaller physical footprint than large banks.

Pro tips from us: If you’re a member of a credit union or know you can easily join one, it’s always worth checking their auto loan options first.

Tips for Improving Your Chances of Approval

Beyond choosing the right lender, there are proactive steps you can take to make your application more appealing. These tips can not only help you get approved but also potentially secure a better deal.

- Boost Your Down Payment: As mentioned, this is huge. The more you put down, the less risk for the lender. It shows your commitment.

- Find a Co-signer: If you have a trusted friend or family member with good credit, their support can be invaluable. This can significantly reduce the perceived risk.

- Choose an Affordable Vehicle: Don’t overreach. A lower-priced car means a smaller loan amount, which is easier for lenders to approve.

- Show Proof of Income Stability: Lenders want to see consistent income. Provide pay stubs, bank statements, or tax returns to demonstrate your ability to make payments.

- Improve Your Credit Score (Even a Little): Even a small improvement can help. Pay off small debts, dispute errors, and make all current payments on time. For more detailed guidance, consider reading our article on Understanding Your Credit Score: A Beginner’s Guide.

- Get Pre-qualified or Pre-approved: This allows you to know what you can afford before you start shopping, putting you in a stronger negotiating position. Pre-qualification usually involves a soft credit check, while pre-approval involves a hard inquiry.

- Shop Rates Within a Short Window: Multiple hard inquiries for the same type of loan (like an auto loan) within a 14-45 day period typically count as a single inquiry on your credit report. This allows you to rate shop without further damaging your score.

Common Mistakes to Avoid When Getting a Bad Credit Car Loan

Navigating the subprime auto loan market can be tricky. Knowing what pitfalls to sidestep is just as important as knowing what steps to take.

- Applying Everywhere: Each hard inquiry can slightly ding your credit score. While rate shopping within a short window is fine, applying to dozens of lenders indiscriminately is not.

- Not Understanding Loan Terms: Don’t just look at the monthly payment. Understand the total loan amount, interest rate (APR), loan term (length), and any fees. A longer loan term means lower monthly payments but significantly more interest paid over time.

- Buying More Car Than You Can Afford: This is a trap many fall into. It leads to payment struggles, potential repossession, and further credit damage. Stick to your budget.

- Ignoring Your Credit Report: As discussed, this is foundational. Errors can unfairly impact your ability to get a loan.

- Falling for "Guaranteed Approval" Traps: Be highly skeptical of any lender promising "guaranteed approval" regardless of your credit score. These often come with extremely high interest rates, unfavorable terms, or hidden fees. True lenders always perform some level of due diligence.

- Skipping the Test Drive and Inspection: Even with bad credit, you have the right to a reliable vehicle. Always test drive and consider getting an independent inspection, especially for used cars.

- Not Considering Refinancing Later: Don’t view your first bad credit car loan as your final one. Once you’ve made 6-12 months of on-time payments and your credit score has improved, you can often refinance for a lower interest rate. This is a powerful strategy for saving money.

Pro Tips for Navigating Bad Credit Car Loans

From our experience, here are some advanced tips to help you succeed:

- Leverage Pre-qualification: Many online lenders and some banks offer pre-qualification, which gives you an estimate of what you might be approved for without a hard credit inquiry. This is a fantastic way to gauge your options without impacting your credit score. It gives you negotiating power at the dealership.

- Negotiate More Than Just the Payment: Don’t let a salesperson anchor you on a monthly payment. Focus on the total price of the car, the interest rate (APR), and the loan term. Negotiating these elements will save you more money in the long run.

- Use the Loan to Rebuild Credit: This loan isn’t just about getting a car; it’s an opportunity. Make every single payment on time, every time. This consistent positive payment history will be reported to credit bureaus and will significantly help improve your credit score over time.

- Understand the "Total Cost of Ownership": Beyond the loan, consider fuel efficiency, insurance costs, and expected maintenance. These factors dramatically affect your long-term budget. For tips on saving for other car-related expenses, check out our guide on How to Save for a Down Payment on a Car.

- Be Transparent and Honest: When speaking with lenders, be open about your financial situation and any past credit issues. Honesty can build trust and help them understand your circumstances better. They are more likely to work with someone who is upfront.

Conclusion: Your Path to a Better Automotive Future

Securing a car loan with bad credit is certainly possible, and it doesn’t have to be a nightmare. By understanding your credit, preparing your finances, knowing which types of lenders to approach, and avoiding common pitfalls, you can navigate this process successfully. Remember, this isn’t just about getting a car; it’s an invaluable opportunity to demonstrate financial responsibility and rebuild your credit for a brighter future.

Take your time, do your homework, and choose a loan that fits your budget and helps you achieve your financial goals. The open road awaits, and with the right strategy, you’ll be driving on it sooner than you think. For further detailed information on managing your credit and finances, we highly recommend visiting the Consumer Financial Protection Bureau (CFPB) website at consumerfinance.gov. They offer a wealth of unbiased resources to empower consumers.