Navigating the Road Ahead: Your Ultimate Guide to Understanding Car Loan Rates in India

Navigating the Road Ahead: Your Ultimate Guide to Understanding Car Loan Rates in India Carloan.Guidemechanic.com

Embarking on the journey to own a car is exciting, but the path to financing it can often seem like a labyrinth of numbers and terms. For many aspiring car owners in India, securing the right car loan is a crucial step. However, the sheer volume of information, coupled with varying interest rates and hidden charges, can make the process daunting.

This comprehensive guide is designed to demystify car loan rates in India, providing you with the expert insights needed to make informed decisions. We’ll delve deep into the factors that influence these rates, reveal common pitfalls, and equip you with strategies to secure the best possible deal. Our goal is to transform you from a confused applicant into a savvy borrower, ready to drive away with confidence.

Navigating the Road Ahead: Your Ultimate Guide to Understanding Car Loan Rates in India

Understanding the Core: What Exactly Are Car Loan Rates?

At its heart, a car loan rate, often referred to as the interest rate, is the cost you pay to borrow money from a lender to purchase a vehicle. It’s expressed as a percentage of the principal loan amount and directly impacts your Equated Monthly Installment (EMI) and the total cost of your car over the loan tenure. Think of it as the rental fee for using someone else’s money.

These rates are not static; they fluctuate based on numerous economic factors, lender policies, and your individual financial profile. A seemingly small difference of even 0.5% in the interest rate can translate into thousands of rupees saved or spent over a typical 5-year loan period. Therefore, understanding this core concept is the first step towards financial prudence.

The Unseen Forces: Key Factors Influencing Car Loan Rates in India

Car loan rates aren’t pulled out of thin air. They are a carefully calculated figure influenced by a multitude of interconnected factors. As an expert in this domain, I’ve seen how these elements collectively determine the final rate offered to an applicant. Let’s break down the most significant ones:

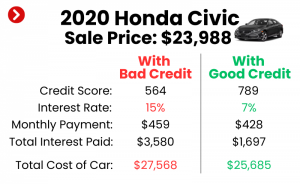

1. Your Credit Score (CIBIL Score)

Without a doubt, your credit score is arguably the most critical determinant of the interest rate you’ll be offered. In India, the CIBIL score is the most widely recognized credit score, ranging from 300 to 900. It’s a three-digit numerical summary of your creditworthiness, reflecting your past repayment behavior and financial discipline.

Lenders use this score as a primary indicator of your ability and willingness to repay a loan. A high CIBIL score (typically 750 and above) signals to lenders that you are a low-risk borrower, making them more inclined to offer you lower interest rates and better terms. Conversely, a low score suggests higher risk, often resulting in higher interest rates or even loan rejection. Based on my experience, a strong credit score is the single most powerful tool you possess in negotiating favorable car loan rates. Building and maintaining a good credit history is paramount.

2. Your Income and Employment Stability

Your current income and the stability of your employment play a significant role in a lender’s risk assessment. Lenders want to ensure you have a consistent and sufficient income stream to comfortably manage your EMI payments. They typically look at your Debt-to-Income (DTI) ratio, which compares your monthly debt payments to your gross monthly income.

Salaried individuals with stable jobs in reputable organizations often receive more competitive rates due to perceived income security. For self-employed individuals or those with variable incomes, lenders might require more extensive documentation or a slightly higher interest rate to offset the perceived risk. The longer your tenure with a current employer, the better it generally looks to a lender.

3. Loan Amount and Tenure

The total amount you wish to borrow and the repayment period (tenure) also influence the interest rate. Generally, for smaller loan amounts, the interest rate might be marginally higher, as the administrative costs for the lender remain somewhat constant regardless of the principal. Conversely, very large loan amounts might also come under scrutiny.

Regarding tenure, longer repayment periods, while reducing your monthly EMI, often result in a higher total interest paid over the life of the loan. Some lenders might offer slightly lower rates for shorter tenures, as the risk exposure for them is reduced. It’s a delicate balance between affordability and the overall cost of borrowing.

4. Type of Vehicle: New vs. Used Car

The type of car you intend to purchase significantly impacts the interest rate. New car loans typically come with lower interest rates compared to used car loans. This is primarily because new cars have a higher resale value and are perceived as lower risk collateral. They also come with warranties, reducing potential maintenance issues.

Used cars, on the other hand, have depreciated in value and carry a higher risk of mechanical issues, making them less secure as collateral. As a result, lenders often charge higher interest rates for used car loans to compensate for this increased risk. The age and condition of the used car further influence this differentiation.

5. Relationship with the Lender

Believe it or not, your existing relationship with a bank or financial institution can sometimes work in your favor. If you have a long-standing relationship with a bank, perhaps through a savings account, salary account, fixed deposits, or previous loans with a good repayment history, you might be eligible for preferential interest rates.

Lenders value loyal customers and often have special schemes or loyalty programs that offer a slight reduction in interest rates or processing fees. Don’t hesitate to inquire about these benefits with your primary bank before exploring other options. This can often be a quick win.

6. Down Payment Amount

The size of your down payment directly impacts the loan amount you need to borrow. A larger down payment reduces the principal loan amount and, consequently, the lender’s risk exposure. When you commit a substantial portion of the car’s value upfront, you demonstrate greater financial commitment and capability.

Lenders view this favorably and may reward you with a lower interest rate. A higher down payment also means a lower EMI, making your loan more manageable and reducing the chances of default. It’s a clear signal of your financial strength.

7. Market Conditions and RBI Policies

Beyond individual factors, broader economic conditions and the Reserve Bank of India’s (RBI) monetary policies play a crucial role in shaping car loan rates. When the RBI adjusts its repo rate (the rate at which it lends to commercial banks), it has a ripple effect across the banking sector, influencing all lending rates, including car loans.

During periods of economic growth and stable inflation, interest rates tend to be more competitive. Conversely, during economic downturns or high inflation, rates might increase. Keeping an eye on these macroeconomic indicators can give you a sense of the general trend in interest rates. For official insights into monetary policy, refer to the .

8. Special Offers and Promotional Schemes

Lenders, especially during festive seasons or at the end of financial quarters, often roll out attractive promotional offers. These can include reduced interest rates, waived processing fees, or extended loan tenures. Car manufacturers also tie up with banks to offer special financing schemes on specific models.

It’s always wise to look out for these limited-time offers, as they can significantly reduce your overall cost of borrowing. However, always read the fine print to ensure there are no hidden conditions or increased charges elsewhere. A good deal should be transparent and genuinely beneficial.

Navigating the Car Loan Landscape: Fixed vs. Floating Rates

When applying for a car loan, you’ll generally encounter two main types of interest rates: fixed and floating. Understanding the difference is crucial for choosing the option that best suits your financial comfort level and market outlook.

1. Fixed Interest Rates

With a fixed interest rate, the interest rate remains constant throughout the entire loan tenure. Your EMI will be the same from the first payment to the last, providing predictability and stability to your monthly budget. This consistency makes financial planning much simpler.

Pros: Predictable EMIs, protection from rising interest rates, easier budgeting.

Cons: You won’t benefit if market interest rates fall, sometimes slightly higher initial rates.

Pro Tips from us: Opt for a fixed rate if you prefer stability and are concerned about potential interest rate hikes in the future. It’s also suitable if you have a tight monthly budget and need certainty.

2. Floating Interest Rates

A floating interest rate, also known as a variable rate, is linked to a benchmark rate (like the MCLR – Marginal Cost of Funds Based Lending Rate in India). This rate can fluctuate during the loan tenure based on market conditions and changes in the benchmark. Your EMI will adjust accordingly.

Pros: You benefit if market interest rates fall, often slightly lower initial rates than fixed.

Cons: EMIs can increase if market rates rise, making budgeting less predictable, potential for higher total cost.

Pro Tips from us: Consider a floating rate if you anticipate interest rates to decline in the future or if you have a buffer in your monthly budget to absorb potential EMI increases. It requires a bit more risk tolerance.

Comparing Car Loan Rates: Don’t Just Look at the Number

When shopping for a car loan, simply comparing the advertised interest rate is a common mistake. A truly informed decision requires a holistic view of the loan offer.

Pro tips from us: When comparing offers, never solely focus on the interest rate. Always ask for the Annual Percentage Rate (APR), which includes other charges, giving you a truer cost. Also, meticulously compare the following:

- Processing Fees: A one-time charge levied by the lender for processing your loan application.

- Pre-closure/Pre-payment Charges: Penalties for paying off your loan earlier than scheduled. These can vary significantly between lenders.

- Late Payment Penalties: Fees incurred if you miss an EMI payment.

- Documentation Charges: Fees for various administrative tasks.

- Stamp Duty: A government tax on loan agreements, which varies by state.

Gather offers from multiple banks and NBFCs (Non-Banking Financial Companies). Utilize online comparison platforms, but always verify the details directly with the lenders. A slightly higher interest rate with no pre-closure charges might be more beneficial than a lower rate with hefty penalties if you plan to pay off your loan early.

The Application Process: Eligibility and Documentation Demystified

Applying for a car loan involves meeting certain eligibility criteria and submitting a set of documents. While specific requirements may vary slightly between lenders, there’s a common framework.

Eligibility Criteria (General)

- Age: Typically between 18/21 years to 60/65 years at loan maturity.

- Residency: Indian resident.

- Income: Minimum net monthly income (varies by lender, usually ₹20,000-₹30,000).

- Employment: Salaried individuals (min. 1 year of employment) or self-employed individuals (min. 2-3 years in business).

- Credit Score: As discussed, a good CIBIL score is crucial.

Required Documents (Common)

- Identity Proof: PAN Card, Aadhaar Card, Passport, Driving License.

- Address Proof: Aadhaar Card, Passport, Utility Bills (electricity, water, gas), Rent Agreement.

- Income Proof:

- Salaried: Latest 3 months’ salary slips, Form 16, 6 months’ bank statements (showing salary credits).

- Self-Employed: Latest 2-3 years’ Income Tax Returns (ITR) with computation of income, latest 6 months’ bank statements (business and personal), Balance Sheet and Profit & Loss Account for the last 2-3 years.

- Vehicle Documents: Proforma invoice/quotation from the car dealer.

- Application Form: Duly filled and signed with passport-sized photographs.

Common mistakes to avoid are submitting incomplete documents or underestimating the importance of a clean credit history. Ensure all your documents are up-to-date and accurately reflect your financial standing. Any discrepancies can lead to delays or rejection.

Calculating Your Car Loan EMI: A Practical Approach

Your Equated Monthly Installment (EMI) is the fixed amount you pay to the lender each month until the loan is fully repaid. It comprises both the principal loan amount and the interest accrued on the outstanding balance. Understanding how EMI is calculated helps you assess affordability.

While the precise formula (P R (1+R)^N / ((1+R)^N-1)) might seem complex, where P is the principal, R is the monthly interest rate, and N is the number of months, you don’t need to be a math wizard. Every bank and financial institution provides online EMI calculators.

Importance of Using an EMI Calculator: These tools allow you to input different loan amounts, interest rates, and tenures to instantly see how your EMI changes. This empowers you to experiment with various scenarios and find an EMI that comfortably fits your budget. A higher interest rate or a shorter tenure will result in a higher EMI, while a longer tenure or a lower interest rate will reduce it.

Strategies to Secure the Best Car Loan Rates in India

Now that you understand the mechanics, let’s talk strategy. As an expert, I’ve seen these approaches consistently help borrowers secure more favorable terms:

- Maintain an Excellent Credit Score: This cannot be stressed enough. Pay all your bills on time, keep your credit utilization low, and regularly check your credit report for errors. A CIBIL score above 750 is your best asset.

- Make a Substantial Down Payment: A larger down payment reduces the loan amount, lowers the lender’s risk, and can open doors to lower interest rates. It also significantly decreases your EMI burden.

- Shop Around and Compare Offers: Don’t settle for the first offer you receive. Approach multiple banks, NBFCs, and even the car dealership’s finance department. Compare not just interest rates but also all associated fees.

- Negotiate with Lenders: Especially if you have a strong credit profile or existing relationship, don’t shy away from negotiating. Lenders often have some flexibility, particularly when they know you have competing offers.

- Improve Your Debt-to-Income Ratio: Before applying, try to pay off any smaller outstanding debts. A lower DTI ratio indicates you have more disposable income to manage new loan payments, making you a more attractive borrower.

- Consider a Shorter Loan Tenure (If Affordable): While it means higher EMIs, a shorter tenure results in less interest paid over time and might qualify you for slightly better rates. Balance this with your monthly budget.

- Get Pre-Approved: Some lenders offer pre-approved car loans based on your financial profile. This gives you a clear budget before you even step into a showroom, strengthening your negotiation position with dealers and lenders alike.

Hidden Charges and Fees: What to Watch Out For

The advertised interest rate is just one piece of the puzzle. Many loans come with additional charges that can significantly increase the overall cost. Being aware of these can save you from unpleasant surprises.

- Processing Fees: A one-time fee for processing your loan application. This can range from 0.5% to 2% of the loan amount, sometimes with a minimum and maximum cap.

- Pre-payment/Foreclosure Charges: If you decide to pay off your loan before the scheduled tenure, lenders might charge a penalty. This typically ranges from 2% to 5% of the outstanding principal. Some lenders offer loans with zero pre-payment charges after a certain period.

- Late Payment Penalties: Missing an EMI due date will incur a penalty, usually a percentage of the overdue amount, plus additional interest.

- Documentation Charges: Fees associated with preparing and verifying loan documents.

- Stamp Duty: A state-level tax on the loan agreement, which varies by location.

- Insurance Charges: While not a loan fee, some lenders might insist on specific insurance policies, which add to your overall car ownership cost.

Always ask for a detailed breakdown of all charges and read the loan agreement thoroughly before signing. Transparency is key.

New Car Loan vs. Used Car Loan: Understanding Rate Differences

As briefly touched upon, the rates for new cars and used cars are distinctly different. This differentiation stems from the inherent risks associated with each.

New Car Loans: These generally offer lower interest rates because new cars are considered less risky collateral. They come with manufacturer warranties, are less prone to immediate mechanical issues, and retain a higher value, especially in the initial years. Lenders have more confidence in recovering their money if a default occurs.

Used Car Loans: Conversely, used car loans typically carry higher interest rates. The reasons are manifold: used cars have depreciated, their mechanical condition can be uncertain, and their resale value is lower. The older the used car, the higher the perceived risk and, consequently, the higher the interest rate. Lenders often have stricter eligibility criteria and shorter loan tenures for older used vehicles.

The Future of Car Loan Rates in India

The landscape of car loan rates in India is dynamic, influenced by global economic trends, domestic inflation, and the RBI’s monetary policy stance. While predicting exact future movements is challenging, current trends suggest a cautious approach from lenders. As the economy evolves, we might see continued competition among lenders, potentially leading to attractive offers, especially for creditworthy borrowers. However, any significant shifts in inflation or global interest rates could lead to adjustments. Staying informed about economic news will always be beneficial.

Conclusion: Drive Away with Confidence

Securing a car loan in India doesn’t have to be a bewildering experience. By understanding the intricate factors that influence interest rates, carefully comparing offers, and proactively managing your financial health, you can navigate the process with ease and confidence. Remember, the goal isn’t just to get a loan, but to secure the best loan that aligns with your financial capabilities and long-term goals.

Armed with the knowledge from this comprehensive guide, you are now well-equipped to make an informed decision and embark on your car ownership journey on the most financially sound footing. Drive smart, borrow wisely, and enjoy the open road ahead!