Navigating the Road Ahead: Your Ultimate Guide to Used Car Loan Term Length

Navigating the Road Ahead: Your Ultimate Guide to Used Car Loan Term Length Carloan.Guidemechanic.com

Buying a used car is a significant financial decision, and one of the most crucial factors often overlooked is the used car loan term length. This single choice can dramatically impact your monthly budget, the total amount you pay for the car, and even your financial flexibility for years to come. It’s more than just picking a number; it’s about strategically aligning your vehicle purchase with your financial health.

As an expert blogger and professional SEO content writer who has navigated the complexities of auto financing for years, I’m here to demystify this critical aspect. This comprehensive guide will equip you with the knowledge to make an informed decision, ensuring your used car purchase is a smart, sustainable investment rather than a financial burden. We’ll dive deep into the pros and cons, hidden costs, and expert strategies for choosing the optimal loan term.

Navigating the Road Ahead: Your Ultimate Guide to Used Car Loan Term Length

What Exactly is a Used Car Loan Term Length?

At its core, the used car loan term length refers to the duration over which you agree to repay the money borrowed to purchase your vehicle. This period is typically expressed in months, commonly ranging from 36 to 72 months, though shorter or longer terms are also available. It’s essentially the timeline you have to make your payments before you officially own the car outright.

This term length directly influences two major components of your loan: your monthly payment amount and the total interest you’ll pay over the life of the loan. Understanding this fundamental relationship is the first step toward making a savvy financing choice. It’s not just a number; it’s a commitment that shapes your financial landscape.

The Interplay: Loan Term, Monthly Payments, and Total Cost

The chosen used car loan term length acts as a seesaw for your finances. Lengthen one side, and the other inevitably changes. This dynamic relationship between the loan term, your monthly payments, and the total cost of the loan is the cornerstone of smart auto financing. Let’s break down how different term lengths play out.

Short-Term Loans: The Fast Track to Ownership

Opting for a shorter loan term, typically 36 or 48 months, means you’re committing to a more aggressive repayment schedule. This approach has several compelling advantages, making it a favorite among financially disciplined buyers.

- Lower Total Interest Paid: This is arguably the most significant benefit. Because you’re paying off the principal balance more quickly, the lender has less time to accrue interest on the outstanding amount. Over the life of the loan, this translates to substantial savings.

- Faster Path to Ownership: With a shorter term, you’ll reach the finish line of car ownership much sooner. This means fewer years with a car payment, freeing up your monthly budget for other financial goals or investments.

- Reduced Risk of Negative Equity: Negative equity, often called being "upside down" on your loan, occurs when you owe more on your car than it’s worth. Used cars depreciate rapidly, and a shorter loan term helps you build equity faster, reducing the chances of falling into this financial trap.

- Less Exposure to Maintenance Costs on an Aging Vehicle: By the time you pay off a short-term loan, your car is still relatively young. This often means you’re less likely to be juggling loan payments with major repair bills that typically arise as cars age.

However, the primary drawback of a shorter loan term is obvious: higher monthly payments. If your budget is tight, these larger installments can be challenging to manage, potentially stretching your finances too thin. It’s a trade-off between immediate cash flow and long-term savings.

Long-Term Loans: Spreading Out the Cost

Conversely, choosing a longer used car loan term length, such as 60 or 72 months, and sometimes even 84 months, extends your repayment period significantly. This option often appeals to buyers looking for lower monthly financial commitments.

- Lower Monthly Payments: This is the immediate and most attractive benefit. By stretching out the repayment over more months, each individual payment becomes smaller, making the car seem more affordable on a month-to-month basis.

- Increased Financial Flexibility: Lower monthly payments can free up cash flow for other expenses, savings, or investments. This can be particularly appealing if you have other financial obligations or prefer to keep more money readily available.

- Opportunity to Afford a Nicer Car: With lower payments, you might be able to afford a slightly more expensive used car that would have been out of reach with a shorter loan term. This allows for an upgrade in features or a newer model year.

However, long-term loans come with their own set of significant disadvantages that demand careful consideration. The most glaring issue is the higher total interest paid. While your monthly payments are lower, you’re paying interest for a much longer period, accumulating a significantly larger sum over the life of the loan. This can add thousands of dollars to the actual cost of your vehicle.

Furthermore, the risk of negative equity escalates dramatically with longer terms. As we’ve discussed, used cars lose value quickly. A long loan term means you’ll be paying off the car slowly while its market value drops faster than you build equity, leaving you owing more than the car is worth for an extended period. This can become a major problem if you need to sell or trade in the car before the loan is paid off.

Factors Influencing Your Ideal Used Car Loan Term Length

Choosing the right used car loan term length isn’t a one-size-fits-all decision. It’s a highly personal choice influenced by a variety of financial and practical factors. Understanding these elements will empower you to tailor a loan that best fits your individual circumstances.

Your Budget & Monthly Cash Flow

This is, without a doubt, the most critical factor. How much can you genuinely afford to pay each month without straining your finances? It’s not just about the car payment; it includes insurance, fuel, maintenance, and potential repair costs.

Based on my experience working with countless car buyers, the biggest pitfall is not truly understanding your monthly cash flow. Many people focus solely on the car payment and forget about the holistic cost of ownership. A lower monthly payment from a longer term might seem appealing, but if it means paying significantly more in interest, it’s a false economy. Be honest with yourself about your budget and avoid overextending.

Interest Rates

The interest rate offered on your loan plays a pivotal role in the total cost. Generally, shorter loan terms often come with slightly lower interest rates because lenders perceive less risk over a shorter period. Conversely, longer terms might carry slightly higher rates to compensate for the extended risk.

Even a small difference in the interest rate can translate to hundreds or thousands of dollars over several years. Always compare the Annual Percentage Rate (APR) across different term lengths and lenders. A low APR on a long term might still cost you more than a slightly higher APR on a short term due to the sheer duration of interest accumulation.

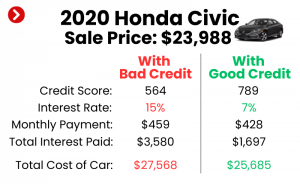

Your Credit Score

Your credit score is a lender’s primary indicator of your creditworthiness. A higher credit score typically qualifies you for lower interest rates and more flexible loan terms. Lenders are more willing to offer competitive rates for shorter durations to borrowers with excellent credit.

If your credit score is less than ideal, you might find yourself limited to higher interest rates or longer loan terms to achieve an affordable monthly payment. This makes improving your credit score before applying for a loan a powerful strategy for securing better financing options. – This internal link offers further value.

Age and Condition of the Used Car

Lenders also consider the vehicle itself. The older a used car is, or the higher its mileage, the more risk lenders associate with it. They might be reluctant to offer very long loan terms (e.g., 72 or 84 months) on an older vehicle because its depreciation accelerates, and its reliability becomes more questionable.

Pro tips from us: If you’re looking at an older used car, aim for the shortest loan term you can comfortably afford. This minimizes the risk of owning a car that becomes a financial liability (high repair costs) while you’re still paying off its loan.

Down Payment

A larger down payment significantly reduces the amount you need to borrow. This not only lowers your monthly payments but also gives you more flexibility in choosing a shorter loan term. By reducing the principal, you can potentially opt for a 36- or 48-month loan without an unmanageably high monthly payment.

A substantial down payment also helps mitigate the risk of negative equity, as you start with more equity in the vehicle from day one. It’s a powerful tool to put you in a stronger negotiating position and secure better loan terms.

Future Financial Goals

Consider your financial roadmap. Are you planning to buy a house, start a family, or make another large purchase in the next few years? A car payment, especially a high one, can impact your debt-to-income ratio and affect your eligibility for other loans.

Common mistakes to avoid are committing to a long-term car payment that clashes with your future aspirations. If you foresee major financial commitments, a shorter car loan term that frees up your budget sooner might be the wisest choice.

Common Loan Term Lengths for Used Cars and Their Implications

While loan terms can vary, certain durations are more common for used car financing. Each has distinct implications for your budget and overall cost.

- 36-Month (3-Year) Term: This is often considered the "gold standard" for used car loans if you can afford the higher monthly payments. It offers the lowest total interest paid and the fastest path to ownership, minimizing depreciation risk. It’s ideal for those prioritizing long-term savings and quick debt elimination.

- 48-Month (4-Year) Term: A popular compromise, the 48-month term balances manageable monthly payments with reasonable total interest costs. It’s a good option for many buyers who want to pay off their car relatively quickly without stretching their budget too thin.

- 60-Month (5-Year) Term: This is one of the most frequently chosen terms for used cars, primarily because it significantly lowers monthly payments compared to shorter options. While more affordable month-to-month, be aware of the increased total interest and the higher likelihood of depreciation outpacing equity building, especially for older models.

- 72-Month (6-Year) Term: Entering the territory of longer terms, 72 months provides even lower monthly payments. This term length should be approached with caution for used cars. The total interest paid becomes substantially higher, and the risk of negative equity is considerable. It’s often reserved for newer, higher-value used vehicles to mitigate some of the depreciation risk.

- 84-Month (7-Year) Term and Beyond: These extended terms are becoming more common, especially for new cars, but are generally ill-advised for most used car purchases. The total interest can be astronomical, and you are almost guaranteed to be upside down on your loan for a significant portion of its duration. Your car might require major repairs or be ready for retirement before you even finish paying it off.

The Hidden Dangers of Long-Term Used Car Loans (72+ Months)

While the appeal of low monthly payments from a long used car loan term length is undeniable, it’s crucial to understand the substantial financial risks involved. For used cars, these dangers are often magnified.

Negative Equity (Upside Down)

This is perhaps the most insidious trap of long-term used car loans. Negative equity means you owe more on your car loan than the car is currently worth. Used cars depreciate rapidly, especially in their first few years. With a long loan term, your payments are spread so thin that you pay off the principal very slowly.

Meanwhile, the car’s value is plummeting. This creates a significant gap where you’re "upside down" for an extended period. If your car is stolen, totaled in an accident, or you need to sell it, you’ll still be responsible for paying the difference between what you owe and what the insurance payout or sale price covers. This can leave you without a car and still owing thousands of dollars. – This internal link adds depth to the depreciation concept.

Higher Overall Interest Paid

This point cannot be stressed enough. A longer loan term, even with a seemingly attractive interest rate, will always result in paying significantly more in total interest. Let’s consider a hypothetical example:

- Car Price: $15,000

- Interest Rate: 6% APR

| Term Length | Monthly Payment | Total Interest Paid | Total Cost of Car |

|---|---|---|---|

| 36 Months | ~$456 | ~$1,416 | ~$16,416 |

| 60 Months | ~$290 | ~$2,400 | ~$17,400 |

| 72 Months | ~$250 | ~$3,000 | ~$18,000 |

As you can see, stretching the loan from 36 to 72 months increases your total interest by over $1,500! That’s $1,500 that could have gone into savings, investments, or towards other financial goals.

Maintenance Costs Overtaking Payments

As a used car ages, its maintenance and repair costs inevitably increase. If you’re still making payments on a 7-year loan for a car that’s now 8 or 9 years old, you might find yourself in a situation where the monthly repair bills start to rival or even exceed your car payment.

This creates immense financial pressure, especially if you haven’t budgeted for these eventualities. It’s a double whammy: a lingering payment for a vehicle that’s constantly demanding more cash to stay on the road.

Limited Resale Value When You Want to Upgrade

When you finally decide to upgrade your vehicle, perhaps after 5 or 6 years, a long-term loan on your used car can severely limit your options. If you’re still significantly upside down, you’ll need to roll that negative equity into your new car loan, making the new loan even larger and more expensive.

Alternatively, you might have to come up with a substantial amount of cash out-of-pocket to cover the difference, which many buyers are unprepared for. This effectively traps you in your current vehicle or forces you into a worse financial position with your next one.

Pro Tips for Choosing the Best Used Car Loan Term Length

Making an informed decision about your used car loan term length requires a strategic approach. Here are some pro tips from us, honed by years of observing smart financial choices in action.

- Prioritize Affordability, Not Just the Lowest Payment: It’s tempting to opt for the longest term to get the lowest monthly payment. However, true affordability considers the total cost of the loan, not just the monthly installment. Can you comfortably afford a higher monthly payment for a shorter term, thereby saving thousands in interest? If so, that’s often the smarter financial move.

- Calculate Total Cost, Not Just Monthly Payments: Use online loan calculators to compare the total amount you’d pay for different loan terms and interest rates. Seeing the full financial picture can be a powerful motivator to choose a shorter, more cost-effective term. Don’t let the illusion of a "low payment" blind you to the real price.

- Consider Pre-Payment Penalties: Before signing any loan agreement, always ask if there are any penalties for paying off your loan early. Most modern auto loans do not have these, but it’s crucial to confirm. Knowing you can pay extra when you have spare cash, or pay it off completely ahead of schedule, offers valuable flexibility.

- Factor in Insurance and Maintenance: Your car payment is only one part of the equation. Get quotes for insurance, and research potential maintenance costs for the specific used car model you’re considering. Add these to your monthly budget before committing to a loan term. A low car payment won’t help if sky-high insurance or repair bills break your budget.

- Shop Around for Lenders and Rates: Don’t just take the first loan offer you receive, especially from the dealership. Apply for pre-approval with several banks, credit unions, and online lenders. Comparing offers can reveal significant differences in interest rates and available term lengths, putting you in a stronger negotiating position. A great resource for understanding consumer finance is the Consumer Financial Protection Bureau, which offers unbiased information on loans: https://www.consumerfinance.gov/ – This external link provides a trusted source.

- Negotiate the Car Price First: Separate the car price negotiation from the financing discussion. Get the best possible price on the vehicle before discussing loan terms. This ensures you’re not distracted by payment figures and can focus on the actual cost of the car itself. Once you have a firm price, then you can apply your chosen loan term strategy.

Real-World Scenarios and Examples

Let’s illustrate how these choices play out in different situations.

Scenario 1: The Financially Savvy Young Professional

Sarah, a 28-year-old marketing professional, has a stable income and a good credit score. She needs a reliable used sedan for her daily commute. She finds a 3-year-old model for $20,000. Sarah has saved a $5,000 down payment.

- Sarah’s Goal: Pay off the car quickly, minimize interest, and maintain a strong debt-to-income ratio for future homeownership plans.

- Her Choice: She opts for a 36-month loan term. With her $5,000 down payment, she finances $15,000. Her monthly payments are higher than a 60-month term, but she can comfortably afford them.

- Outcome: Sarah pays off her car in three years, saving over $2,000 in interest compared to a 60-month loan. She builds equity rapidly and by the time she’s ready to buy a house, she has no car payment, improving her financial standing for a mortgage application.

Scenario 2: The Budget-Conscious Family

David and Maria are a couple with two young children. They need a larger, reliable used SUV but are working with a tighter monthly budget due to other family expenses. They find a 4-year-old SUV for $25,000. They have a $3,000 down payment.

- David and Maria’s Goal: Secure a reliable family vehicle with the lowest possible monthly payment to maintain financial stability.

- Their Choice: After careful budgeting, they realize a 36 or 48-month term would make their monthly payments too high. They reluctantly choose a 60-month loan term, accepting the higher total interest as a necessary compromise for their immediate cash flow needs. They meticulously track their budget to ensure they can manage payments.

- Outcome: They get the SUV they need with manageable monthly payments. However, they commit to paying extra on the principal whenever possible to reduce total interest and build equity faster. They understand the long-term cost but prioritize their current monthly budget.

Conclusion: Drive Smart, Not Just Far

Choosing the optimal used car loan term length is a pivotal decision that extends far beyond your monthly payment. It’s a strategic financial choice that impacts your total cost of ownership, your financial flexibility, and your future financial health. By understanding the intricate relationship between loan terms, interest rates, and depreciation, you empower yourself to make a decision that truly serves your best interests.

Remember to prioritize affordability in its truest sense – the total cost – and always be honest about what your budget can truly bear. Don’t be swayed by the allure of the lowest monthly payment if it means sacrificing thousands in the long run or putting yourself at risk of negative equity. With careful consideration and the expert tips shared here, you can confidently navigate the used car financing landscape and drive away with a deal that makes both financial and practical sense. Make an informed choice today for a smoother financial journey tomorrow.