Navigating the Road: How to Get a Car Loan with Bad Credit and No Down Payment

Navigating the Road: How to Get a Car Loan with Bad Credit and No Down Payment Carloan.Guidemechanic.com

For many, a car isn’t just a luxury; it’s a necessity for work, family, and daily life. But what happens when your credit score has seen better days, and your savings account isn’t quite ready for a substantial down payment? The thought of securing a car loan with bad credit and no down payment can feel like an impossible uphill battle.

However, impossible it is not. While challenging, obtaining a car loan under these circumstances is absolutely achievable with the right strategy, knowledge, and perseverance. This comprehensive guide will equip you with the insights and actionable steps needed to navigate the complexities of auto financing, even when your credit isn’t perfect and your wallet is a bit light. Our goal is to empower you to drive off the lot with confidence, understanding every step of the journey.

Navigating the Road: How to Get a Car Loan with Bad Credit and No Down Payment

Understanding the "Bad Credit No Down Payment" Landscape

Before diving into solutions, it’s crucial to understand why lenders view bad credit and no down payment as a higher risk. A low credit score signals a history of financial difficulties or missed payments, making lenders wary of your ability to repay a new loan. Without a down payment, the lender has more capital at risk, as the car’s value might depreciate faster than you pay off the loan, leaving them exposed if you default.

Based on my experience working with countless individuals in similar situations, the key is to manage your expectations and prepare thoroughly. Lenders aren’t looking to deny you; they’re looking to mitigate their risk. Your job is to present yourself as the least risky borrower possible, despite your credit history. This often means higher interest rates and stricter terms, but it’s a starting point towards rebuilding your credit and securing better deals in the future.

Strategic Pathways to Your No Down Payment Car Loan

Securing a car loan with bad credit and no down payment requires a multi-faceted approach. Here are the most effective strategies you can employ:

1. Focus on Minor Credit Score Improvements

Even a small improvement in your credit score can significantly impact the loan offers you receive. Lenders often have cut-off points for different tiers of interest rates, and bumping your score up by just a few points could move you into a better category. This is often the first and most impactful step to take.

Start by obtaining your free credit reports from all three major bureaus (Equifax, Experian, and TransUnion) at AnnualCreditReport.com. Review them meticulously for any errors or inaccuracies. Disputing and correcting these can sometimes provide an immediate boost to your score.

Furthermore, if you have any outstanding small debts, paying them off or reducing their balances can help. Even paying your current bills on time for a few months leading up to your application can show positive payment behavior, which lenders appreciate. Every little bit helps demonstrate your commitment to financial responsibility.

2. Deep Dive into Your Credit Report and Score

Understanding your credit isn’t just about knowing the number; it’s about understanding the story it tells. Lenders look beyond the FICO or VantageScore number to see the underlying factors. They analyze payment history, amounts owed, length of credit history, new credit, and credit mix.

Knowing the specifics of your report helps you anticipate lender concerns. For instance, if you have a recent bankruptcy, be prepared to explain the circumstances and demonstrate how your financial situation has stabilized since then. This proactive approach shows maturity and transparency, which can work in your favor.

Pro tips from us: Many credit card companies and banks now offer free credit score monitoring and even provide insights into the factors affecting your score. Utilize these tools to stay informed and understand what you can do to improve your standing.

3. Explore Dealerships Specializing in Bad Credit Auto Loans

Not all dealerships are created equal when it comes to bad credit auto loans. Some dealerships, often referred to as "Buy Here, Pay Here" (BHPH) lots, offer in-house financing, meaning they are both the seller and the lender. This can be a viable option for those with severely damaged credit and no down payment, as they focus more on your income stability than your credit history.

However, BHPH dealerships often come with higher interest rates and less flexible terms. While they can provide a solution when other doors close, it’s crucial to understand the total cost of the loan and compare it with other options. Always read the fine print carefully and ensure the payments are genuinely affordable within your budget.

Additionally, many traditional dealerships have "special finance" departments that work with a network of subprime lenders. These lenders specialize in working with borrowers who have less-than-perfect credit. They understand the challenges and are often more willing to approve a car loan bad credit no down payment scenario, albeit with higher rates.

4. The Power of a Co-Signer

If you have a trusted friend or family member with good credit who is willing to co-sign your car loan, this can dramatically increase your chances of approval and potentially secure a better interest rate. A co-signer essentially pledges their own credit and assets as collateral, promising to repay the loan if you default.

Choosing a co-signer is a significant decision for both parties. They are taking on a substantial financial responsibility, and any missed payments will negatively impact their credit score as well as yours. Ensure you both understand the implications fully. This strategy can be a game-changer for getting approved for a no down payment car loan with bad credit.

Common mistakes to avoid are not fully discussing the responsibilities with your co-signer. Be transparent about your financial situation and your plan for repayment. A strong relationship can be strained by financial disagreements, so clear communication is paramount.

5. Present a Robust Application Beyond Your Credit Score

While your credit score is important, it’s not the only factor lenders consider. A strong application highlights your ability to repay the loan through other means. Lenders want to see stability and capacity.

Key elements include:

- Proof of Stable Income: Provide pay stubs, bank statements, or tax returns that clearly show a consistent and sufficient income to cover the loan payments and your other living expenses.

- Proof of Residency: Utility bills or lease agreements can confirm your stable living situation.

- Long-Term Employment: A history of stable employment with the same company for several years demonstrates reliability.

- Low Debt-to-Income (DTI) Ratio: Even with bad credit, if your existing debt obligations are relatively low compared to your income, it shows you have room in your budget for a new car loan.

From my observations, a lender is more likely to take a chance on a borrower with bad credit if they have a long history of stable employment and a clear ability to make payments. These factors can sometimes outweigh a less-than-ideal credit score.

6. Be Realistic About Your Vehicle Choice

When you’re dealing with bad credit and no down payment, your options for vehicles might be more limited. Focus on reliability and affordability rather than luxury. A used car that is a few years old will have a lower purchase price, which translates to a smaller loan amount and more manageable monthly payments.

Avoid the temptation to over-extend yourself financially just to get into a newer, more expensive vehicle. Your primary goal is to secure reliable transportation and use this loan as an opportunity to rebuild your credit. Once your credit improves, you can always trade up in the future.

Consider cars that have a good reputation for durability and lower insurance costs. Researching these aspects before you even step onto a lot can save you money in the long run.

7. Get Pre-Approved, But Proceed with Caution

Seeking pre-approval from multiple lenders can give you a clear idea of what loan terms you qualify for before you even visit a dealership. This empowers you to negotiate confidently, as you’ll know your buying power. However, be mindful of the type of credit inquiry.

A "soft inquiry" does not affect your credit score and is often used for preliminary checks. A "hard inquiry," on the other hand, can slightly lower your score and occurs when a lender is seriously considering your application. When shopping for an auto loan, multiple hard inquiries within a short period (typically 14-45 days, depending on the credit scoring model) are usually treated as a single inquiry, minimizing the impact on your score. So, shop around for pre-approvals within a concentrated timeframe.

Pre-approval can also help you understand the potential interest rates you’ll be facing with a bad credit auto loan, allowing you to budget more accurately.

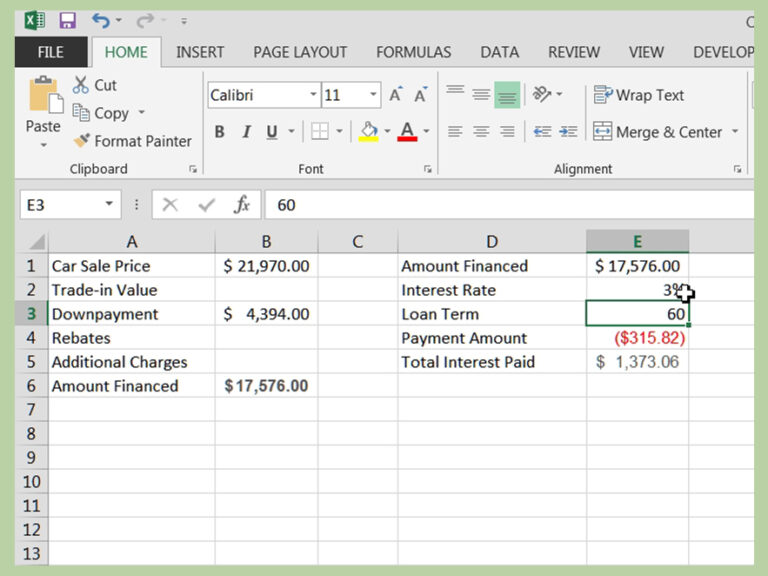

8. Prepare for Higher Interest Rates

It’s a reality that borrowers with bad credit will face higher interest rates compared to those with excellent credit. Lenders compensate for the increased risk by charging more for the loan. Don’t be discouraged by a high Annual Percentage Rate (APR) initially. Your immediate goal is to get approved and establish a positive payment history.

Focus on the total cost of the loan and whether the monthly payments are truly affordable within your budget. Once you’ve consistently made on-time payments for 12-18 months, your credit score will likely improve. At that point, you can explore refinancing your car loan at a lower interest rate, which can save you a significant amount over the remaining life of the loan.

9. Explore Alternative Lenders and Online Platforms

The traditional bank loan isn’t your only option, especially when seeking a car loan bad credit no down payment. The digital age has brought forth numerous online lenders and platforms that specialize in subprime auto loans. These lenders often have more flexible criteria and can process applications quickly.

Many online platforms partner with a network of lenders, allowing you to fill out one application and receive multiple offers. This can save you time and effort while increasing your chances of finding an approval. Just be sure to research the reputation of any online lender before providing your personal information. Look for transparency in their terms and conditions.

For more insights into choosing the right digital lending option, you might find our guide on Tips for Choosing an Online Car Loan Provider particularly helpful. (Simulated internal link)

10. Building Even a Small Down Payment Can Help (If Possible)

While the focus of this article is "no down payment," it’s important to acknowledge that even a small down payment can significantly improve your chances of approval and secure better terms. A down payment reduces the amount you need to borrow, which lowers the lender’s risk.

Pro tips from us: If you can save even 5% of the car’s value, it shows lenders that you have some financial discipline and are invested in the purchase. Consider selling unused items, picking up extra shifts, or temporarily cutting back on non-essential expenses to build up a small reserve. Every dollar you put down reduces the total amount of interest you’ll pay over the life of the loan.

Navigating the Application Process Like a Pro

Once you’ve identified potential lenders and vehicles, the application process itself requires diligence.

- Gather All Necessary Documents: Have your driver’s license, proof of income (pay stubs, tax returns), proof of residency (utility bills), and insurance information ready. Being prepared shows responsibility and streamlines the process.

- Be Honest and Transparent: Don’t try to hide aspects of your financial history. Lenders will uncover it anyway. Being upfront about your bad credit and explaining any extenuating circumstances can actually build trust.

- Understand All Terms: Before signing anything, read the loan agreement thoroughly. Pay close attention to the interest rate, loan term, monthly payment, and any fees. If you don’t understand something, ask for clarification. Common mistakes to avoid are rushing through the paperwork and not fully grasping the commitment you’re making.

- Negotiate (Where Possible): Even with bad credit, there might be some room for negotiation, especially on the vehicle price. If you have a pre-approval in hand, you have more leverage. Don’t be afraid to walk away if the deal doesn’t feel right or if the payments are genuinely unaffordable.

Life After Approval: Managing Your Car Loan and Rebuilding Credit

Congratulations, you’ve secured your car loan bad credit no down payment! This is just the beginning of a new financial chapter. The most critical step now is to manage your loan responsibly.

- Make Payments On Time, Every Time: This is paramount. Consistent on-time payments are the most effective way to rebuild your credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date.

- Budget for All Car Ownership Costs: Beyond the loan payment, remember to factor in car insurance (which can be higher with bad credit), fuel, maintenance, and potential repairs. Having a clear budget prevents surprises and ensures you can comfortably afford your vehicle. For help with budgeting, consider exploring resources like the Consumer Financial Protection Bureau’s financial tools: www.consumerfinance.gov/consumer-tools/ (Simulated external link).

- Consider Refinancing: After 12-18 months of diligent payments, check your credit score again. If it has improved, explore refinancing your car loan. You might qualify for a significantly lower interest rate, reducing your monthly payments and the total amount you pay over the life of the loan.

Final Thoughts: Your Journey to a Car Loan with Bad Credit and No Down Payment

Getting a car loan with bad credit and no down payment is undoubtedly a challenge, but it is far from impossible. It requires patience, thorough research, and a strategic approach. By understanding the lending landscape, preparing a strong application, and being realistic about your options, you can successfully navigate this process.

Remember, this isn’t just about getting a car; it’s an opportunity to demonstrate financial responsibility and actively work towards rebuilding your credit. Each on-time payment is a step closer to a healthier financial future, opening doors to better rates and more favorable terms down the road. Take these steps, stay persistent, and soon you’ll be driving towards your goals, one payment at a time.