Navigating the Road: Securing Car Loans With Bad Credit and No Money Down

Navigating the Road: Securing Car Loans With Bad Credit and No Money Down Carloan.Guidemechanic.com

Dreaming of a new set of wheels but facing the twin challenges of bad credit and no down payment? You’re not alone. For many, the idea of getting a car loan with bad credit and no money down seems like an impossible feat. The good news is, while challenging, it’s not entirely out of reach. This comprehensive guide will demystify the process, equip you with the knowledge you need, and significantly boost your chances of driving off the lot.

Based on my experience working with countless individuals in similar situations, securing this type of financing requires strategy, patience, and a clear understanding of what lenders are looking for. We’ll dive deep into the realities, uncover the best strategies, and help you navigate the subprime auto loan market with confidence.

Navigating the Road: Securing Car Loans With Bad Credit and No Money Down

The Dual Challenge: Bad Credit and No Money Down

Before we explore solutions, let’s first understand the hurdles. Lenders assess risk, and both bad credit and a lack of a down payment signal higher risk.

What Constitutes "Bad Credit" to Lenders?

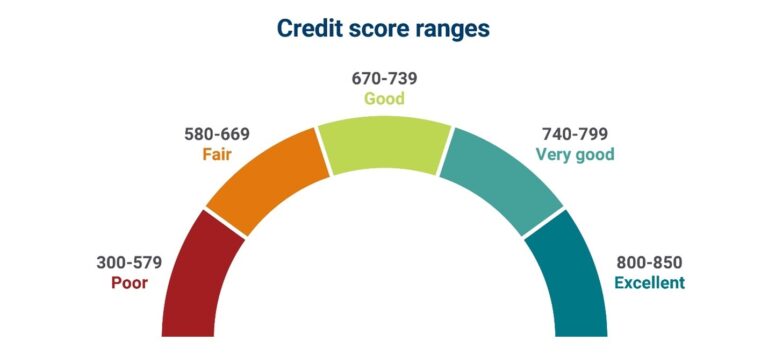

Your credit score is a numerical representation of your creditworthiness. While specific cut-offs vary, generally, a FICO score below 620 is considered "subprime" or "bad credit." This score is influenced by several factors: your payment history, the amount of debt you owe, the length of your credit history, new credit inquiries, and your credit mix.

When you have a low credit score, it suggests to lenders that you’ve had trouble managing debt in the past. This makes them hesitant to lend money, especially for a significant purchase like a car. They worry about the likelihood of default, leading to higher interest rates or outright denial.

Why is "No Money Down" a Red Flag?

A down payment serves several crucial purposes for both the borrower and the lender. For the lender, it immediately reduces their risk. If you default on the loan, they can repossess the vehicle and sell it to recoup their losses. A down payment means they have less money to recover.

For you, a down payment lowers the total amount financed, which translates to smaller monthly payments and less interest paid over the life of the loan. When you put no money down, you’re financing 100% of the vehicle’s value, or even more if you roll taxes and fees into the loan. This increases the principal amount, leading to higher payments and greater overall cost.

Is "No Money Down" Really Possible with Bad Credit? The Reality Check

Let’s be upfront: securing a car loan with bad credit and no money down is more difficult than if you had good credit or a substantial down payment. However, it’s certainly not impossible. Many lenders specialize in what’s known as "subprime auto lending," catering specifically to individuals with less-than-perfect credit histories.

These lenders understand that life happens and that a past financial misstep doesn’t necessarily mean you’re a permanent risk. What they look for instead are indicators of your current ability and willingness to pay. They might focus more heavily on your current income stability, employment history, and debt-to-income ratio rather than solely on your credit score.

The trade-off for this flexibility often comes in the form of higher interest rates and potentially longer loan terms. This is how lenders mitigate the increased risk they’re taking on. Understanding this reality is the first step toward setting realistic expectations and preparing effectively.

Who Are These Lenders? Navigating the Subprime Market

The traditional banks and credit unions that offer prime auto loans might be less willing to approve a car loan with bad credit and no money down. This is where the subprime market comes into play.

Specialized Dealership Financing

Many dealerships have "special finance" departments dedicated to helping customers with bad credit. They often have relationships with a network of subprime lenders who are more flexible with their lending criteria. These departments understand the nuances of bad credit financing and can often match you with a suitable lender.

Another option within dealerships is "buy-here-pay-here" lots. These dealerships act as both the seller and the lender. They often approve loans with very minimal credit checks, focusing almost entirely on your income and ability to make payments. However, pro tips from us suggest exercising caution here: interest rates can be exceptionally high, and vehicle choices might be limited. Always compare offers and understand the total cost before committing.

Online Lenders Specializing in Bad Credit

The digital age has brought forth numerous online lenders who specialize in bad credit auto loans. These platforms often have streamlined application processes and can provide quick pre-approvals. They leverage technology to assess risk differently, sometimes looking at alternative data points beyond just your credit score.

Based on my experience, online lenders can be a great starting point for pre-qualification, as they allow you to compare multiple offers without impacting your credit score significantly (initially, at least). Just ensure any lender you consider is reputable and transparent about their terms and fees.

The Application Process: What to Expect and How to Prepare

Preparation is key to increasing your chances of approval. Lenders will want to verify your identity, your income, and your ability to make regular payments.

Gathering Essential Documents

Before you even start applying, collect the following documents:

- Proof of Income: Recent pay stubs (last 30-60 days), bank statements showing direct deposits, or tax returns if self-employed. Lenders want to see stable, consistent income.

- Proof of Residency: Utility bills, lease agreements, or mortgage statements with your current address. This demonstrates stability.

- Valid Driver’s License: Essential for driving the car and verifying your identity.

- Proof of Insurance: You’ll need this before driving off the lot. Get quotes beforehand.

- References: Some lenders might ask for personal references (not family members).

- Trade-in Information (if applicable): Even if you have "no money down," a small trade-in can sometimes help your case, though it’s separate from a cash down payment.

Pre-qualification vs. Pre-approval

Understanding the difference is crucial. Pre-qualification involves a soft credit pull and gives you an estimate of what you might qualify for without affecting your credit score. It’s a good way to gauge your options.

Pre-approval, on the other hand, typically involves a hard credit inquiry and provides you with a firm offer for a specific loan amount and interest rate. This puts you in a stronger negotiating position at the dealership because you know exactly how much you can spend. Pro tips from us: Always aim for pre-approval from a few different lenders before stepping onto a car lot. This gives you leverage and a clear budget.

The Importance of Honesty

Common mistakes to avoid are trying to inflate your income or hide past financial issues. Lenders will verify the information you provide. Discrepancies can lead to immediate denial. Being honest, even about your bad credit, shows integrity and can sometimes work in your favor if you can explain past issues and demonstrate current stability.

Strategies to Increase Your Approval Chances (Even with Bad Credit and No Down Payment)

While the goal is car loans with bad credit no money down, implementing these strategies can significantly tilt the odds in your favor.

1. Demonstrate Stable and Sufficient Income

This is paramount. Lenders want to see that you have enough disposable income each month to comfortably cover the car payment, insurance, and other car-related expenses, in addition to your existing bills. Aim for an income that’s at least $1,500-$2,000 per month, though this can vary by lender and loan amount. A long, consistent employment history with the same employer is also a huge plus.

2. Manage Your Debt-to-Income Ratio (DTI)

Your DTI is the percentage of your gross monthly income that goes toward debt payments. Lenders prefer a DTI below 40%, and ideally below 36%. To calculate it, add up all your monthly debt payments (credit cards, student loans, mortgage/rent) and divide that by your gross monthly income. Try to pay down some smaller debts before applying to improve this ratio.

3. Consider a Cosigner

A creditworthy cosigner with good credit and stable income can significantly improve your chances of approval and potentially secure a lower interest rate. A cosigner essentially guarantees the loan, promising to make payments if you default. However, this is a serious commitment for the cosigner, as it impacts their credit and financial liability. Ensure they understand the risks involved.

4. Be Realistic About Your Car Choice

Don’t aim for the latest luxury SUV. Lenders are more likely to approve loans for affordable, reliable used cars when you have bad credit and no down payment. Choose a vehicle that is well within your budget and whose value won’t depreciate too rapidly. A lower loan amount is less risky for the lender and easier for you to manage.

5. Show Proof of Residency Stability

Lenders look for stability in all aspects of your life. If you’ve lived at the same address for several years, this indicates reliability. If you’ve moved recently, be prepared to explain why and provide consistent documentation.

6. Demonstrate Financial Responsibility Elsewhere

Even with bad credit, if you’ve consistently paid your rent, utilities, and other non-credit-related bills on time, this shows a commitment to financial obligations. While these don’t always appear on your credit report, some subprime lenders might consider alternative data.

7. Avoid Multiple Hard Inquiries

Common mistakes to avoid are applying to too many lenders at once within a short period. Each "hard inquiry" can slightly ding your credit score. However, most credit scoring models treat multiple inquiries for the same type of loan (like an auto loan) within a specific timeframe (usually 14-45 days) as a single inquiry. So, shop around for rates within that window.

Understanding the Terms: What to Look Out For in Your Loan Agreement

Once you’ve received an offer for a car loan with bad credit no money down, it’s crucial to understand every detail of the agreement. From years of analyzing loan documents, I can tell you that the fine print matters, especially with subprime loans.

Interest Rates (APR)

With bad credit, expect a higher Annual Percentage Rate (APR) than someone with good credit. This is how lenders compensate for the increased risk. A higher APR means you’ll pay significantly more in interest over the life of the loan. Focus on the total cost, not just the monthly payment.

Loan Term

This is the length of time you have to repay the loan. Longer terms (e.g., 72 or 84 months) lead to lower monthly payments, which can be tempting. However, they also mean you pay more in interest over time, and you risk owing more on the car than it’s worth (being "upside down" on the loan) for a longer period.

Total Cost of the Loan

Don’t just look at the monthly payment. Multiply your monthly payment by the number of months in the loan term, then add any upfront fees. This gives you the true cost of the loan. A seemingly affordable monthly payment can hide a very expensive overall loan.

Fees and Charges

Look out for origination fees, processing fees, documentation fees, and any other charges rolled into the loan. These can significantly inflate the amount you’re financing. Always ask for a breakdown of all costs.

Prepayment Penalties

Some loans, especially subprime ones, might include prepayment penalties. This means you’ll be charged a fee if you pay off your loan early. This can be a significant drawback if your credit improves and you want to refinance for a better rate down the line. Always ask if there’s a prepayment penalty.

The "No Money Down" Myth vs. Reality

While we’re discussing car loans with bad credit no money down, it’s important to clarify what "no money down" truly means in practice. Often, it means you’re not paying cash out of pocket at the time of purchase. However, sometimes the down payment amount is simply rolled into the loan, increasing your principal.

The Benefits of Any Down Payment

Even if your goal is zero down, pro tips from us suggest that if you can scrape together even a small amount – say, $500 or $1,000 – it can make a substantial difference. A down payment:

- Reduces Lender Risk: Even a small contribution shows commitment and reduces the loan-to-value (LTV) ratio, making the lender more comfortable.

- Lowers Monthly Payments: A smaller principal means more manageable payments.

- Reduces Total Interest Paid: Less financed means less interest over the loan term.

- Helps Avoid Being Upside Down: With no money down, you’re often immediately upside down on the loan (owing more than the car is worth) due to depreciation and fees. A down payment helps offset this.

If a cash down payment truly isn’t possible, consider if you have an older vehicle, even one with minimal value, that could be used as a trade-in. This acts similarly to a down payment in reducing the amount financed.

The Road Ahead: Building Better Credit and Future Car Purchases

Securing a car loan with bad credit no money down is just the beginning. It’s an opportunity to rebuild your credit and set yourself up for better financial opportunities in the future.

Importance of On-Time Payments

Your new car loan is a powerful tool for credit repair. Make every single payment on time, every month. Payment history is the most significant factor in your credit score. Consistent, timely payments will demonstrate responsibility and gradually improve your score.

Strategies for Improving Your Credit Score

While paying off your loan, continue to work on other aspects of your credit. Keep credit card balances low, avoid opening new lines of credit unnecessarily, and regularly check your credit report for errors. For more tips on improving your credit, check out our article on .

Refinancing Opportunities

Once you’ve made 6-12 months of on-time payments and your credit score has improved, you might be eligible to refinance your car loan at a lower interest rate. This can significantly reduce your monthly payments and the total amount of interest you pay over the remaining loan term.

Actionable Steps: Your Checklist for Success

Ready to pursue your car loan with bad credit no money down? Follow this checklist for the best chance of success:

- Assess Your Financial Situation: Honestly evaluate your income, expenses, and current debt. Determine a realistic car payment you can afford.

- Gather All Necessary Documents: Have pay stubs, bank statements, proof of residency, and your driver’s license ready.

- Check Your Credit Report: Get a free copy of your credit report from AnnualCreditReport.com. Dispute any errors.

- Research Lenders: Explore both online lenders specializing in bad credit and local dealerships with special finance departments.

- Get Pre-qualified/Pre-approved: Apply to a few lenders to compare offers without impacting your credit too much initially.

- Choose an Affordable Car: Select a reliable, used vehicle that fits your budget and meets your needs, not just your wants.

- Negotiate Terms: Use your pre-approval to negotiate the best possible price for the car and the best loan terms.

- Read the Fine Print: Thoroughly understand the APR, loan term, fees, and any prepayment penalties before signing.

- Secure Insurance: Have your car insurance in place before driving off the lot.

Conclusion

Obtaining a car loan with bad credit and no money down is a challenging endeavor, but it is far from impossible. By understanding the landscape of subprime lending, preparing diligently, and employing smart strategies, you can significantly increase your chances of approval. Remember, this isn’t just about getting a car; it’s an opportunity to responsibly manage a major financial commitment and pave the way for a stronger credit future.

Don’t let past financial hurdles define your present. With the right approach, you can navigate the path to car ownership and start rebuilding your credit one on-time payment at a time. Take the first step today – research, prepare, and drive towards a brighter financial future. You might also find our guide on helpful.

For additional resources on understanding and improving your credit score, a trusted external source is MyFICO, which offers detailed information and tools: https://www.myfico.com/.