Navigating the Road to a $30,000 Car Loan: Your Expert Guide to Approval and Smart Financing

Navigating the Road to a $30,000 Car Loan: Your Expert Guide to Approval and Smart Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect, and for many, a $30,000 car loan represents a significant step towards driving their dream car. This amount often aligns with popular sedans, well-equipped SUVs, or even quality pre-owned luxury vehicles, making it a common financing goal. However, securing the best possible terms for a loan of this size requires more than just a quick application; it demands strategic preparation, a deep understanding of the process, and an awareness of the factors that influence approval.

As an expert in auto financing, I’ve seen countless individuals navigate this path. My goal with this comprehensive guide is to equip you with the knowledge and insights needed to confidently secure a $30,000 car loan, ensuring you not only get approved but also land a deal that aligns perfectly with your financial well-being. We’ll delve into everything from credit scores to negotiation tactics, transforming a potentially daunting process into a clear, manageable one.

Navigating the Road to a $30,000 Car Loan: Your Expert Guide to Approval and Smart Financing

Understanding the $30,000 Car Loan Landscape

A $30,000 car loan is a substantial financial commitment, placing you in a segment where lenders scrutinize your financial health carefully. This loan amount typically covers a wide range of vehicles, from brand-new compact SUVs and mid-size sedans to well-maintained, late-model used cars that offer excellent value. The significance of this amount lies in its accessibility to a broad spectrum of consumers, yet it also requires a solid financial standing to secure favorable terms.

The type of vehicle you choose – new or used – will subtly influence the lender’s perception of risk and, consequently, your loan terms. New cars generally come with lower interest rates due due to their higher resale value and lower depreciation risk in the initial years, while used cars might carry slightly higher rates, especially if they are older or have higher mileage. Understanding these nuances is the first step in positioning yourself for success.

The Cornerstone of Approval: Your Financial Health

Securing a $30,000 car loan hinges primarily on your financial health. Lenders assess your ability and willingness to repay the loan through several key indicators. Paying close attention to these aspects before you even start shopping for a car can dramatically improve your chances of approval and help you secure the most competitive interest rates.

Credit Score Explained: Your Financial Report Card

Your credit score is arguably the single most important factor when applying for a car loan. It’s a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repaying debt. For a $30,000 loan, a strong credit score signals to lenders that you are a reliable borrower, translating into lower interest rates and better loan terms.

Different credit score ranges carry varying implications. Generally, a score above 700 is considered good to excellent, qualifying you for the most favorable rates. Scores in the 600s might still get you approved, but often with higher interest rates. Below 600, securing a $30,000 loan can become challenging, possibly requiring a co-signer or a larger down payment. Understanding where you stand is crucial for setting realistic expectations and planning your approach.

Pro tips from us: Before applying for any loan, obtain your credit score and a copy of your credit report. You can get a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once a year through AnnualCreditReport.com. Review it meticulously for any inaccuracies or fraudulent activity, as these could negatively impact your score. Disputing errors can often lead to a quick boost in your score.

Common mistakes to avoid are: Neglecting to check your credit report for errors. Even minor discrepancies can affect your score, and correcting them before you apply can make a significant difference in your loan offer. Don’t assume your score is perfect; always verify.

Income and Employment Stability: Can You Afford It?

Beyond your credit score, lenders want to ensure you have a stable income stream sufficient to cover the monthly payments for a $30,000 car loan. They look for consistent employment history, typically preferring at least two years in the same job or industry. This stability demonstrates a reliable ability to meet your financial obligations.

Your debt-to-income (DTI) ratio is another critical metric. This ratio compares your total monthly debt payments (including the prospective car loan) to your gross monthly income. Lenders generally prefer a DTI ratio below 40%, though some might accept slightly higher depending on other factors. A lower DTI indicates that you have more disposable income available to manage your new car payment, making you a less risky borrower.

Based on my experience: Lenders often request pay stubs, W-2 forms, or tax returns to verify your income. Self-employed individuals may need to provide more extensive documentation, such as bank statements and tax returns from the past two years, to prove consistent earnings. Be prepared with these documents to streamline the application process.

Down Payment Power: Reducing Risk and Costs

Making a down payment is one of the most effective ways to improve your chances of approval for a $30,000 car loan and secure better terms. A down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. It also signals to the lender that you are committed to the purchase and have some financial discipline.

For a $30,000 vehicle, a recommended down payment is typically 10-20% of the car’s purchase price. This means putting down $3,000 to $6,000. While not always mandatory, a substantial down payment mitigates the risk for the lender, especially for used cars where depreciation can be faster. It also helps you avoid being "upside down" on your loan, where you owe more than the car is worth, a common issue with no-money-down loans.

Pro tips from us: The larger your down payment, the better your chances of approval and the more favorable your interest rate will likely be. If you can save up a significant down payment, it will pay dividends in the long run by reducing your overall cost of borrowing and giving you more equity in your vehicle from day one.

Navigating the Loan Application Process

Once you’ve shored up your financial health, the next step is to navigate the actual loan application process. This involves several stages, from getting pre-approved to choosing the right lender, all of which are crucial for securing the best possible $30,000 car loan.

Pre-Approval: Your Secret Weapon

Getting pre-approved for a car loan before you step foot in a dealership is a powerful strategy. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount (like $30,000) at a certain interest rate, pending a final review of the vehicle and your documentation. This process usually involves a "soft" credit inquiry, which doesn’t impact your credit score.

The benefits of pre-approval are immense:

- Knowing Your Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Negotiating Power: You become a cash buyer in the eyes of the dealership, allowing you to focus solely on negotiating the car’s price without the added pressure of financing.

- Comparing Offers: You can compare the pre-approved offer with any financing options the dealership presents, ensuring you get the most competitive rate.

How to get pre-approved: You can seek pre-approval from various financial institutions, including your local bank, credit unions, and reputable online lenders. Many provide an easy online application process that can give you a decision within minutes or a few hours.

Common mistakes to avoid are: Skipping pre-approval and going straight to the dealership. Dealerships often prioritize their own financing options, which may not always be the most competitive for you. Having a pre-approval in hand gives you leverage and a benchmark to compare against.

Choosing the Right Lender: Options Galore

For a $30,000 car loan, you have several avenues for financing, each with its own advantages and disadvantages.

- Banks: Traditional banks offer competitive rates, especially if you have a strong relationship with them. They are reliable and often provide a personalized experience.

- Credit Unions: Known for their member-focused approach, credit unions often offer some of the lowest interest rates due to their non-profit status. It’s worth exploring if you’re eligible for membership.

- Online Lenders: Companies like Capital One Auto Finance, LightStream, and Carvana Financing offer quick, convenient online applications and competitive rates. They are excellent for comparing offers from multiple lenders quickly.

- Dealership Financing: While convenient, dealership financing involves the dealer acting as an intermediary, working with various lenders. While they can sometimes match or beat outside offers, it’s crucial to have your own pre-approval to ensure you’re getting a fair deal.

Pro tips from us: Don’t settle for the first offer you receive. Shop around and compare interest rates, loan terms, and any associated fees from at least three different lenders. This competition will help you secure the best possible deal for your $30,000 car loan. Remember, a few percentage points difference in interest can save you hundreds, if not thousands, over the life of the loan.

Required Documentation: Be Prepared

When it’s time to finalize your $30,000 car loan, lenders will require specific documentation to verify your identity, income, and residence. Having these documents ready can significantly speed up the approval process.

Typical documents include:

- Government-issued ID (driver’s license or passport)

- Proof of income (recent pay stubs, W-2 forms, or tax returns)

- Proof of residence (utility bill or lease agreement)

- Proof of auto insurance (once the car is purchased)

- Social Security Number

Based on my experience: Having all your documents organized and easily accessible before you start the application process can prevent delays and frustration. A well-prepared applicant gives lenders confidence in your readiness and responsibility.

Understanding Loan Terms and Costs

Beyond the approval itself, understanding the specifics of your loan terms is critical. The interest rate, loan term, and any additional fees will collectively determine the total cost of your $30,000 car loan.

Interest Rates: The Cost of Borrowing

The interest rate is the percentage charged by the lender for the money you borrow. It’s a key factor in determining your monthly payment and the total amount you’ll repay over the loan’s life. For a $30,000 car loan, even a small difference in interest rate can result in significant savings.

Interest rates are primarily determined by your credit score, the loan term, the current market rates, and the lender’s risk assessment. Auto loans are almost exclusively fixed-rate loans, meaning your interest rate and monthly payment remain constant throughout the loan term, providing predictability in your budget.

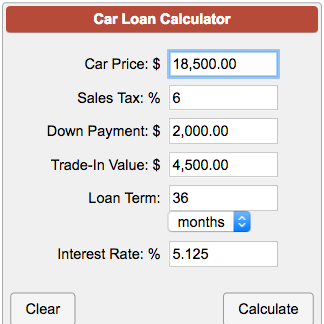

Example: On a $30,000 loan over 60 months, a 5% interest rate results in a monthly payment of approximately $566, with total interest paid around $3,960. If that rate jumps to 8%, your monthly payment increases to about $608, and total interest paid reaches approximately $6,480. That’s a difference of over $2,500 just from a 3% rate change.

Loan Term (Length of the Loan): Balance Between Payments and Total Cost

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, 84 months). While a longer loan term will result in lower monthly payments, it also means you’ll pay more in total interest over the life of the loan. Conversely, a shorter term leads to higher monthly payments but less interest paid overall.

For a $30,000 car loan, common terms range from 60 to 72 months. While 84-month terms are available, they are generally not recommended for most borrowers. They significantly increase the total interest paid and keep you in debt for a longer period, often leading to negative equity where the car’s value depreciates faster than you pay off the loan.

Common mistakes to avoid are: Automatically choosing the longest loan term to achieve the lowest monthly payment. While it makes the car more "affordable" in the short term, you end up paying substantially more for the vehicle and risk being upside down on your loan for a prolonged period. Always aim for the shortest term you can comfortably afford.

Additional Costs: Beyond the Sticker Price

When budgeting for your $30,000 car, remember that the purchase price is just one component of the total cost. Several other expenses need to be factored in:

- Sales Tax: Varies by state, but can add hundreds or even thousands to your total.

- Registration and Licensing Fees: Required by your state’s DMV.

- Documentation Fees: Charged by dealerships for processing paperwork (often negotiable).

- GAP Insurance: Covers the difference between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. Highly recommended, especially with a small down payment.

- Extended Warranties/Service Contracts: These are optional but can be costly. Evaluate if they offer real value or if your vehicle is likely to have issues that exceed the cost of the warranty.

Pro tips from us: Always get a detailed breakdown of all fees and charges before signing any paperwork. Question anything you don’t understand and negotiate where possible, especially on documentation fees and extended warranties. Factoring these into your overall budget from the outset prevents unwelcome surprises.

Strategies for Maximizing Your Approval Chances and Getting the Best Deal

Getting approved for a $30,000 car loan at a great rate isn’t just about meeting the minimum requirements; it’s about optimizing your financial profile and employing smart strategies.

Improving Your Credit Score

If your credit score isn’t where you want it to be, take steps to improve it before applying. Pay all your bills on time, keep credit card balances low (below 30% utilization), and avoid opening new lines of credit.

Paying Down Debt

Lowering your existing debt, especially credit card balances, can significantly improve your debt-to-income ratio, making you a more attractive borrower. Focus on high-interest debts first.

Saving for a Larger Down Payment

As discussed, a larger down payment reduces the loan amount and signals financial responsibility. If you can wait a few extra months to save more, it will likely pay off in better loan terms.

Considering a Co-signer

If your credit score or income is borderline, a co-signer with excellent credit and a stable income can significantly improve your approval chances and secure a lower interest rate. However, understand that the co-signer is equally responsible for the loan, and any missed payments will affect their credit too.

Negotiating the Car Price

Remember, the loan is for the car’s price. Negotiating a lower purchase price for the vehicle directly reduces the amount you need to borrow, which in turn lowers your monthly payments and total interest. Separate the car negotiation from the loan negotiation to avoid confusion.

Pro tips from us: Don’t be afraid to walk away from a deal if it doesn’t feel right or if the numbers don’t align with your budget. There are always other cars and other dealerships. Patience and persistence are your allies in securing the best possible deal.

After Approval: Smart Car Ownership

Congratulations, you’ve secured your $30,000 car loan! But the financial journey doesn’t end there. Responsible car ownership involves budgeting for ongoing costs and making smart financial decisions throughout the life of your loan.

Budgeting for Monthly Payments

Integrate your new car payment seamlessly into your monthly budget. Ensure you have enough buffer to cover it comfortably, even if unexpected expenses arise. Setting up automatic payments can help you avoid missed payments and protect your credit score.

Insurance Costs

A $30,000 vehicle will likely incur higher insurance premiums compared to a less expensive car. Get insurance quotes before finalizing your purchase to understand the full cost of ownership. Most lenders will require comprehensive and collision coverage for the duration of the loan.

Maintenance and Fuel

Factor in regular maintenance (oil changes, tire rotations, etc.) and fuel costs. A new car often comes with a warranty, but routine maintenance is still essential. Fuel efficiency can vary widely, so consider this when choosing your vehicle.

Understanding Depreciation

Vehicles, especially new ones, begin to depreciate the moment you drive them off the lot. A $30,000 car will likely lose a significant portion of its value in the first few years. Be aware of this when considering trade-ins or future sales, particularly if you have a longer loan term.

Common mistakes to avoid are: Forgetting about these ongoing ownership costs. Many buyers focus solely on the monthly payment and sticker price, only to be surprised by the true cost of owning a $30,000 vehicle. A holistic budget is key.

Conclusion: Your Path to a Confident Car Loan

Securing a $30,000 car loan doesn’t have to be an intimidating process. By understanding the critical role of your credit score and financial stability, diligently preparing your documentation, getting pre-approved, and strategically shopping for the best loan terms, you empower yourself to make informed decisions. This proactive approach not only increases your chances of approval but also ensures you secure a loan that aligns with your financial goals, saving you money in the long run.

Remember, a car loan is a significant financial commitment. Arm yourself with knowledge, be thorough in your preparation, and don’t hesitate to negotiate. Your ideal $30,000 car loan is within reach when you approach the process with confidence and clarity. Drive off the lot not just with a new car, but with the satisfaction of a smart financial decision.

What was your experience getting a car loan? Share your tips and insights in the comments below!