Navigating the Road to a Car Loan with a 430 Credit Score: Your Ultimate Guide

Navigating the Road to a Car Loan with a 430 Credit Score: Your Ultimate Guide Carloan.Guidemechanic.com

Securing a car loan can feel like an uphill battle when your credit score is in the "very poor" range, such as a 430. Many people believe it’s impossible, leading to frustration and the misconception that their only option is to save up cash. While it’s undeniably challenging, getting a car loan with a 430 credit score is not entirely out of reach. It requires a strategic approach, a clear understanding of the market, and a commitment to demonstrating your financial reliability.

This comprehensive guide is designed to empower you with the knowledge and actionable strategies needed to navigate the complexities of securing an auto loan when your credit is at its lowest point. We’ll delve deep into what lenders look for, where to find specialized financing, and how to improve your chances of approval, even with a 430 credit score. Our goal is to provide real value, offering insights and pro tips from years of experience in the automotive finance landscape.

Navigating the Road to a Car Loan with a 430 Credit Score: Your Ultimate Guide

Understanding Your 430 Credit Score: The Starting Point

Before we explore solutions, it’s crucial to understand what a 430 credit score signifies. Credit scores, like FICO and VantageScore, typically range from 300 to 850. A score of 430 places you firmly in the "Very Poor" category. This indicates to lenders that you pose a high risk of defaulting on a loan, often due to past missed payments, high credit utilization, or even bankruptcies.

This low score means traditional lenders, such as major banks and credit unions, are highly unlikely to approve your application. They prioritize borrowers with strong credit histories to minimize their risk exposure. However, this doesn’t mean all doors are closed. The automotive finance industry has a segment dedicated to subprime lending, specifically designed for individuals with challenging credit.

The Reality of Seeking a Car Loan with a 430 Credit Score

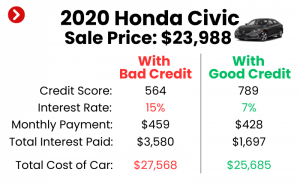

Let’s set realistic expectations upfront. Obtaining a car loan with a 430 credit score will differ significantly from someone with excellent credit. You will likely face higher interest rates, stricter terms, and potentially a more limited selection of vehicles. This is simply how lenders mitigate the increased risk associated with your credit profile.

Based on my experience working with countless individuals navigating challenging credit situations, the key is not to get discouraged but to be prepared. Understanding these realities allows you to approach the process with a clear mind, empowering you to make informed decisions and avoid predatory practices. Your goal isn’t just to get approved, but to secure a loan that you can realistically afford and that helps you rebuild your credit.

Strategies to Significantly Improve Your Chances of Approval (Pre-Application)

Even with a 430 credit score, there are proactive steps you can take before applying that can dramatically improve your approval odds and potentially secure better loan terms. These strategies focus on presenting yourself as the most reliable borrower possible, despite your credit history.

1. Focus on Credit Repair (Even Short-Term Improvements Matter)

While rebuilding a 430 credit score takes time, even minor improvements can make a difference. Lenders often see an applicant as more favorable if they show recent positive financial behavior.

- Address Past-Due Accounts: If you have any accounts that are currently past due, prioritize bringing them current immediately. Lenders view recent delinquencies very negatively. Showing you’ve resolved these can be a powerful signal.

- Reduce Credit Utilization: High credit card balances relative to your credit limits (credit utilization) significantly drag down your score. Try to pay down as much credit card debt as possible. Aim for utilization below 30% on all cards, but even getting it under 50% can help.

- Check Your Credit Report for Errors: Pro tips from us: Always pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) at AnnualCreditReport.com. Dispute any inaccuracies you find, as these could be unfairly lowering your score. Correcting even one error could nudge your score up.

- Consider a Secured Credit Card: If you don’t have active credit, a secured credit card can be a great way to start building positive payment history. You deposit money as collateral, and that becomes your credit limit. Use it responsibly and pay it off in full each month.

Even if you can only improve your score by 20-30 points before applying, it demonstrates a commitment to financial responsibility, which lenders appreciate.

2. Save for a Substantial Down Payment

A significant down payment is perhaps the single most impactful strategy for securing a car loan with a 430 credit score. It directly addresses the lender’s primary concern: risk.

- Reduces Lender Risk: When you put down a large sum, you reduce the amount the lender has to finance. This lowers their potential loss if you default.

- Shows Commitment: A substantial down payment demonstrates your financial commitment to the purchase and your ability to save money. This signals stability to lenders.

- Potential for Better Terms: With less money to finance, lenders may be more willing to offer slightly lower interest rates or more favorable terms, even with a low credit score. Aim for at least 10-20% of the car’s purchase price, if not more.

Based on my experience, a strong down payment can often be the deciding factor between approval and rejection for bad credit borrowers. It acts as a powerful counterbalance to your low credit score.

3. Consider a Co-signer with Excellent Credit

If you have a trusted friend or family member with excellent credit and a stable income, asking them to co-sign your loan can significantly boost your approval chances.

- Leveraging Strong Credit: A co-signer essentially guarantees the loan. If you fail to make payments, they are legally obligated to do so. This drastically reduces the lender’s risk.

- Who Makes a Good Co-signer: Ideal co-signers have a high credit score (700+), stable employment, and a low debt-to-income ratio.

- Risks Involved: Common mistakes to avoid include not fully discussing the responsibilities and risks with your co-signer. Both your credit reports will be affected by the loan, so timely payments are crucial for both parties. Ensure your co-signer understands the full implications before agreeing.

While a co-signer can be a game-changer, it’s a serious commitment for both parties and should only be pursued if you are absolutely confident in your ability to make every payment on time.

4. Know Your Budget and What You Can Truly Afford

Before you even start car shopping, sit down and honestly assess your finances. This involves more than just the monthly car payment.

- Total Monthly Expenses: Factor in fuel costs, insurance (which will be higher with a low credit score), maintenance, and potential repair costs.

- Debt-to-Income Ratio: Lenders will look at your debt-to-income (DTI) ratio, which is your total monthly debt payments divided by your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments.

- Avoid Overextending Yourself: Pro tips from us: It’s tempting to get the nicest car possible, but with a 430 credit score, financial stability should be your priority. Choose a reliable, affordable vehicle that fits well within your budget. Getting a loan you can’t afford is a fast track to further credit damage.

5. Gather Proof of Income and Stability

Lenders want to see that you have a consistent and reliable income stream to make your payments. A low credit score makes this proof even more critical.

- Documents to Prepare: Collect recent pay stubs (at least 2-3 months), bank statements, and tax returns if you’re self-employed.

- Employment History: Be ready to demonstrate stable employment history. Lenders prefer to see at least 6 months to a year at your current job, or a consistent work history if you’ve recently changed roles within the same industry.

- Proof of Residence: Utility bills or lease agreements can confirm your residential stability, which also signals reliability.

The more comprehensive and organized your financial documentation, the more positively lenders will view your application.

Where to Look for a Car Loan with a 430 Credit Score

Traditional banks might turn you away, but specific lenders specialize in helping individuals with challenging credit. Knowing where to look is half the battle.

1. Subprime Lenders and Dealerships Specializing in Bad Credit

These are your primary avenues when your credit score is 430. Subprime lenders are financial institutions that specialize in providing loans to borrowers with low credit scores.

- Buy Here, Pay Here (BHPH) Dealerships: These dealerships act as both the seller and the lender. They often have more lenient approval standards and focus heavily on your income and down payment. However, common mistakes to avoid include high interest rates, limited vehicle selection, and potentially less transparent loan terms. Always read the fine print.

- Online Bad Credit Auto Lenders: Many online platforms specialize in connecting borrowers with subprime lenders. These can be aggregators that match you with multiple lenders or direct lenders themselves. They often have quick pre-approval processes and can be a good starting point to gauge your options.

- Credit Unions: While some credit unions are conservative, others are more community-focused and may be willing to work with members who have lower credit scores, especially if you have an existing relationship with them. They might offer slightly better rates than traditional subprime lenders.

2. Dealership Finance Departments

Most car dealerships have finance departments that work with a network of lenders, including subprime ones.

- Multiple Lender Options: They can submit your application to various lenders, increasing your chances of finding an approval.

- Convenience: It can be convenient to handle the car purchase and financing in one place.

- Be Cautious: In my years covering financial topics, I’ve seen that some dealerships might try to push you into loans with unfavorable terms or add-ons. Do your research, understand the deal, and don’t feel pressured.

3. Avoid "No Credit Check" Scams

Be extremely wary of any lender promising "guaranteed approval" or "no credit check" loans, especially if they demand upfront fees. While some legitimate lenders might offer options that weigh credit less heavily, outright "no credit check" loans are often predatory. They typically come with exorbitant interest rates, hidden fees, and unfavorable terms designed to trap borrowers in a cycle of debt. Always verify a lender’s legitimacy and read reviews.

The Application Process for Bad Credit Loans

When you have a 430 credit score, the application process will be more scrutinized than for someone with excellent credit. Lenders need to be convinced you’re a worthy risk.

What Lenders Look For Beyond Your Score

Since your credit score is a major red flag, lenders will place extra emphasis on other aspects of your financial profile:

- Income Stability: As mentioned, consistent income is paramount.

- Debt-to-Income Ratio (DTI): A lower DTI shows you have room in your budget for new payments.

- Employment History: Long-term employment at the same company is a big plus.

- Down Payment Amount: The more you put down, the better your chances.

- Residence Stability: Showing you’ve lived at the same address for a while suggests stability.

- Banking History: Lenders may review your bank statements to look for bounced checks or consistent overdrafts, which signal financial instability.

Required Documents

Be prepared to provide a comprehensive set of documents:

- Government-issued ID (Driver’s License)

- Proof of residence (utility bill, lease agreement)

- Proof of income (recent pay stubs, bank statements, tax returns for self-employed)

- List of references (sometimes required by subprime lenders)

- Proof of auto insurance (often required before driving off the lot)

Having these ready and organized will streamline the application process and show your seriousness.

Negotiating Your Bad Credit Car Loan

Even with a low credit score, you still have some power in the negotiation process. Don’t assume you have to accept the first offer.

1. Negotiate the Car Price, Not Just the Loan

This is a critical distinction. A lower purchase price means you’re financing less money, which directly impacts your total loan amount and interest paid.

- Research Car Values: Use resources like Kelley Blue Book (KBB) or Edmunds to determine the fair market value of the car you’re interested in. Don’t overpay.

- Separate Negotiations: Try to negotiate the car price first, before discussing financing terms. Once you agree on a price, then move to the loan.

2. Understand the Loan Terms Fully

Bad credit loans often come with less favorable terms, so scrutinize every detail.

- Annual Percentage Rate (APR): This is the true cost of borrowing, including the interest rate and any fees. With a 430 credit score, expect a high APR, potentially in the double digits.

- Loan Term Length: While a longer term (e.g., 72 months) might offer lower monthly payments, you’ll pay significantly more in interest over the life of the loan. Aim for the shortest term you can comfortably afford.

- Prepayment Penalties: Check if there are any penalties for paying off your loan early. Ideally, you want a loan that allows you to pay it down faster without extra fees, especially as you rebuild your credit.

3. Walk Away if It Doesn’t Feel Right

Never feel pressured to sign a deal that makes you uncomfortable or that you don’t fully understand. If the terms are too high, the car is overpriced, or you feel rushed, it’s perfectly acceptable to walk away. There will always be other options, and protecting your financial well-being is paramount.

Post-Loan Approval: Rebuilding Your Credit for a Brighter Future

Getting a car loan with a 430 credit score is not just about getting a vehicle; it’s a golden opportunity to start rebuilding your credit. This loan can be a powerful tool if managed correctly.

1. Make Payments On Time, Every Time

This is the most crucial step. Your payment history is the single largest factor in your credit score.

- Set Up Reminders: Use calendar alerts, automatic payments, or budgeting apps to ensure you never miss a payment.

- Pay More Than the Minimum: If possible, pay a little extra each month. This reduces the principal faster, saving you interest and helping you pay off the loan sooner.

Consistent, on-time payments will gradually and positively impact your credit score, opening doors to better financial opportunities in the future.

2. Don’t Take on More Debt Immediately

Resist the urge to open new credit cards or take out other loans shortly after securing your car loan. Focus solely on making your car payments and responsibly managing any existing credit. Lenders want to see a period of successful repayment before you take on additional obligations.

3. Explore Refinancing Opportunities

Once you’ve made 6-12 months of consistent, on-time payments, and your credit score has shown improvement, you may be able to refinance your car loan.

- Lower Interest Rates: Refinancing allows you to replace your high-interest bad credit loan with a new loan that has a lower interest rate. This can save you thousands of dollars over the life of the loan.

- Better Terms: You might also be able to secure a shorter loan term or more favorable conditions.

- Internal Link: For a detailed walkthrough on how to approach this, you might find our article, "Navigating Car Loan Refinancing: A Guide for Improving Your Terms" particularly helpful. It explains the process step-by-step.

Refinancing is a smart financial move that leverages your improved credit to reduce your overall cost of ownership.

Common Mistakes to Avoid When Getting a Car Loan with Bad Credit

Navigating subprime lending can be tricky. Based on our collective experience, certain pitfalls are common for borrowers with low credit scores. Avoiding these can save you money and stress.

- Not Checking Your Credit Report: As mentioned, this is fundamental. You can’t fix what you don’t know, and errors can severely impact your chances.

- Not Saving for a Down Payment: Underestimating the power of a down payment is a major oversight. It’s your strongest asset when your credit is weak.

- Accepting the First Offer: Don’t feel like you’re out of options. Always compare offers from multiple lenders if possible, even if they are all subprime.

- Ignoring the Total Cost of the Loan: Focus on the total amount you will pay over the life of the loan, not just the monthly payment. High interest rates can double the cost of a vehicle.

- Falling for "Guaranteed Approval" Scams: If it sounds too good to be true, it almost certainly is. Legitimate lenders will always perform some form of assessment.

- Buying a Car You Can’t Afford: The biggest mistake of all. An unaffordable loan will lead to missed payments, further damaging your credit, and potentially vehicle repossession. Always prioritize practicality over luxury.

- Not Getting Independent Vehicle Inspections: Common mistakes we frequently observe include not having a pre-owned vehicle inspected by a trusted mechanic. This is especially crucial at BHPH lots, where vehicles might be older or have hidden issues.

Real-Life Scenarios and the Power of Persistence

While a 430 credit score presents significant hurdles, countless individuals have successfully navigated this challenge. For instance, consider Sarah, who needed a car for her new job but had a score of 450 due to medical debt. She saved diligently for six months, accumulating a 25% down payment. With a stable income and a co-signer, she secured a subprime loan. By making every payment on time, she improved her score by over 100 points in a year, eventually refinancing into a much better loan.

Her story, and many others like it, underscores the power of preparation, persistence, and responsible financial behavior. It’s not about instant gratification, but about strategically using this opportunity to rebuild.

Conclusion: Your Path Forward to a Car Loan with a 430 Credit Score

Securing a car loan with a 430 credit score is undeniably one of the toughest financial challenges many people face. However, as we’ve explored, it is far from impossible. It demands realistic expectations, thorough preparation, and a strategic approach to finding the right lender and the right deal.

Remember, your low credit score is a snapshot of your past, not a permanent sentence. By focusing on a substantial down payment, exploring subprime lenders or co-signers, understanding all loan terms, and committing to timely payments, you can not only get the car you need but also transform this loan into a powerful tool for credit repair. Take control of your financial future, make informed decisions, and use this opportunity to pave the way for better credit and more favorable financial opportunities down the road.

Your journey starts with knowledge and proactive steps. Be patient, be diligent, and stay focused on your long-term financial health. For more detailed information on managing and improving your credit, we recommend visiting Experian’s comprehensive credit education hub at Experian.com/credit-education.