Navigating the Road to a Car Loan with a 534 Credit Score: Your Ultimate Guide

Navigating the Road to a Car Loan with a 534 Credit Score: Your Ultimate Guide Carloan.Guidemechanic.com

Securing a car loan can feel like a daunting journey, especially when your credit score hovers around the 534 mark. Many people believe that a low credit score automatically slams the brakes on their dreams of car ownership. While it’s true that a 534 credit score presents significant challenges, it certainly doesn’t make getting a car loan impossible.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals navigate these waters successfully. This comprehensive guide is designed to be your definitive resource, offering actionable strategies, expert insights, and a clear roadmap to help you finance a vehicle, even with a subprime credit score. We’ll explore everything from understanding your credit standing to finding the right lenders and rebuilding your financial future.

Navigating the Road to a Car Loan with a 534 Credit Score: Your Ultimate Guide

Understanding Your 534 Credit Score: What It Really Means

Before we dive into the "how-to," let’s clarify what a 534 credit score signifies in the world of lending. Credit scores, primarily FICO and VantageScore, are three-digit numbers that lenders use to assess your creditworthiness. They reflect your past financial behavior and predict your likelihood of repaying debt.

A score of 534 falls squarely into the "Poor" or "Very Poor" category, often referred to as subprime. To put it in perspective, FICO scores typically range from 300 to 850. Scores below 580 are generally considered poor, indicating a high risk for lenders. This classification is crucial because it directly impacts the interest rates and terms you’ll be offered.

Based on my experience, lenders view a 534 score as a red flag, suggesting a history of missed payments, high debt, or limited credit history. This doesn’t mean you’re a bad person; it simply means lenders perceive you as a higher risk. Consequently, they will seek to mitigate that risk through various means, which we will explore in detail.

The Reality of Getting a Car Loan with a 534 Credit Score

So, can you actually get a car loan with a 534 credit score? The short answer is yes, but it comes with a few caveats. It’s important to manage your expectations and prepare for a different lending landscape than someone with excellent credit.

What to Expect in the Subprime Market

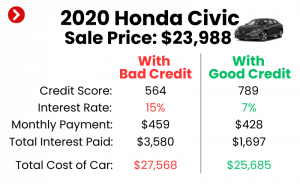

When applying for a 534 credit score car loan, you should anticipate higher interest rates (Annual Percentage Rates, or APRs) compared to national averages. Lenders charge more interest to compensate for the increased risk they’re taking on. This means your monthly payments will be higher, and the total cost of the car will be significantly greater over the loan’s lifetime.

Furthermore, lenders may require a larger down payment, a shorter loan term, or even a co-signer to approve your application. They are looking for any factor that can reduce their exposure to risk. Common mistakes to avoid here include expecting prime rates or getting discouraged by initial rejections. Persistence and preparation are key.

Dispelling Common Misconceptions

One prevalent myth is that "no credit check" car loans are a viable option for those with bad credit. While some dealerships advertise this, it’s often misleading. They might perform a "soft" inquiry that doesn’t affect your score initially, but a "hard" inquiry is almost always required for final approval. Additionally, these loans often come with exorbitant interest rates and unfavorable terms. Our pro tip from us: Always be wary of offers that seem too good to be true, especially when dealing with a low credit score.

Key Strategies for Securing a Car Loan with Bad Credit

Navigating the subprime auto loan market requires a strategic approach. Here are the most effective strategies to improve your chances of approval and secure a manageable loan.

Strategy 1: Saving for a Significant Down Payment

This is arguably one of the most powerful tools in your arsenal when seeking a 534 credit score car loan. A substantial down payment directly reduces the amount you need to borrow, which in turn lowers the lender’s risk.

Why is a down payment so crucial? It shows lenders that you have "skin in the game" and are financially committed to the purchase. It also immediately gives you equity in the vehicle, making it less likely you’ll be "upside down" on your loan (owing more than the car is worth). Based on my experience, even 10-20% down can significantly sway a lender’s decision, making your application much more appealing.

Pro tips for saving: Start a dedicated savings fund, cut unnecessary expenses, or even consider a temporary side hustle. Every dollar you put down upfront will save you money in interest over the life of the loan.

Strategy 2: Finding a Co-signer with Good Credit

Enlisting a co-signer with excellent credit can dramatically improve your chances of loan approval and help you secure better terms. A co-signer essentially promises to take over payments if you default, providing an extra layer of security for the lender.

Who makes a good co-signer? Ideally, someone with a strong credit history, stable income, and low debt-to-income ratio. This is often a trusted family member or close friend. However, it’s vital to understand the implications for both parties. Your co-signer’s credit is on the line, and any missed payments will negatively impact both your credit scores.

From a professional standpoint, ensure both you and your co-signer fully understand the legal agreement. It’s a significant responsibility for them, and clear communication can prevent future financial strain or damaged relationships.

Strategy 3: Exploring Specialized Lenders and Dealerships

Traditional banks might be hesitant to approve a 534 credit score car loan, but there’s an entire segment of the lending industry that specializes in subprime auto financing. These include specific subprime lenders and many dealership finance departments.

Subprime lenders are more accustomed to working with individuals who have lower credit scores. They often have more flexible underwriting criteria, focusing on other factors like income stability and down payment size. While their interest rates will be higher, they are designed to offer solutions where traditional lenders might not.

When dealing with dealerships, be transparent about your credit situation. Many dealerships have relationships with multiple lenders, including those specializing in bad credit car loans. They can often "shop" your application to several institutions, potentially finding you the best available terms. Be cautious, though; always compare offers and read the fine print carefully.

Strategy 4: Improving Your Credit Score (Short-Term & Long-Term)

While you might need a car now, taking steps to improve your credit score can significantly benefit you in the long run. Even small improvements can make a difference in your loan terms.

For short-term gains, focus on quickly disputing any errors on your credit report. You can also try to pay down small, high-interest debts to reduce your credit utilization ratio. This shows immediate positive movement.

For long-term improvement, consistent on-time payments are paramount. Your payment history accounts for 35% of your FICO score. Keep your credit utilization low (ideally below 30% of your available credit) and avoid opening too many new credit accounts at once. Building a positive payment history, even with a subprime car loan, is an excellent way to rebuild your credit. For more in-depth strategies on improving your credit, consider reading our article on How to Quickly Boost Your Credit Score for Big Purchases.

Strategy 5: Choosing the Right Vehicle

The type of vehicle you choose plays a significant role in loan approval, especially with a 534 credit score. Lenders are more likely to approve a loan for a reliable, affordable car rather than a luxury model.

Focus on a car that fits your budget, considering not just the monthly payment but also insurance, maintenance, and fuel costs. A less expensive, used car often makes more sense for a subprime loan applicant. It reduces the total loan amount, making payments more manageable and lowering the risk for the lender. Pro tips from us: Look for reliable, fuel-efficient models that hold their value well. This minimizes depreciation and potential negative equity.

What Lenders Look For Beyond Just Your Score

While your 534 credit score is a major factor, it’s not the only one. Lenders conduct a holistic review of your financial situation. Understanding these additional factors can help you present a stronger case.

Income Stability and Debt-to-Income Ratio

Lenders want to see consistent income that can comfortably cover your car payments and existing debts. They will scrutinize your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to allocate to a new car loan.

Based on my experience, demonstrating a stable employment history (at least 6-12 months at your current job) significantly strengthens your application. Prepare to provide pay stubs, bank statements, or tax returns as proof of income.

Employment and Residence History

A steady employment history signals reliability. Lenders prefer applicants who have held the same job for a reasonable period, as it suggests consistent income. Similarly, a stable residence history (living at the same address for several years) can also be viewed favorably, indicating stability. Frequent job or address changes can be perceived as instability, increasing the lender’s risk assessment.

Down Payment Size and Vehicle Choice

As discussed, a larger down payment reduces the loan amount and the lender’s risk. The vehicle itself also matters. Lenders might be more willing to finance a well-maintained, reasonably priced used car than a brand-new, high-value luxury vehicle, especially for applicants with lower credit scores. The car’s age, mileage, and condition all factor into its perceived value and the lender’s comfort level.

Types of Car Loans Available for Bad Credit

Not all car loans are created equal, especially for individuals with a 534 credit score. Knowing your options can help you target the right lenders.

Traditional Bank Loans and Credit Unions

While less likely to approve a 534 credit score car loan without significant compensating factors (like a large down payment or a co-signer), it’s still worth exploring. Credit unions, in particular, are often more community-focused and may be more flexible with their lending criteria than large banks. They might offer slightly better rates or terms if you’re an existing member or have a strong relationship with them.

Dealership Financing (Subprime Specialists)

Many dealerships have dedicated finance departments that work with a network of lenders, including those specializing in subprime loans. These lenders are designed to serve individuals with lower credit scores. The convenience of one-stop shopping at a dealership can be appealing, but always compare their offers with those from other sources.

Buy-Here-Pay-Here (BHPH) Lots

Buy-Here-Pay-Here dealerships are often considered a last resort. They directly finance the vehicles they sell, meaning you make your payments directly to the dealership rather than a third-party lender. While they often advertise "guaranteed approval," the terms are typically very unfavorable.

BHPH loans usually come with extremely high interest rates, short repayment periods, and sometimes even tracking devices on the vehicle. Common mistakes to avoid include jumping into a BHPH loan without fully understanding the total cost and all the associated risks. Pro tips from us: Only consider BHPH if all other avenues have been exhausted, and even then, exercise extreme caution and read every single word of the contract.

The Application Process with a 534 Credit Score

Approaching the application process strategically can make a significant difference in your outcome.

Gathering Your Documents

Before you even step foot in a dealership or contact a lender, have all your necessary documents ready. This includes:

- Proof of income (recent pay stubs, tax returns, bank statements)

- Proof of residence (utility bills, lease agreement)

- Driver’s license

- Proof of insurance (or be prepared to get it)

- Trade-in title (if applicable)

Having these ready demonstrates your seriousness and preparedness, streamlining the application process.

Pre-qualification vs. Full Application

Many lenders offer a pre-qualification option. This involves a "soft" credit inquiry, which doesn’t harm your credit score, and gives you an idea of the loan terms you might qualify for. This is a great way to shop around without damaging your credit.

Once you find a promising offer, you’ll proceed with a full application, which involves a "hard" credit inquiry. This will temporarily ding your credit score by a few points, but the impact is usually minimal and short-lived. Pro tips from us: Complete all your loan shopping within a 14-45 day window (depending on the credit scoring model) to have multiple hard inquiries count as a single inquiry for scoring purposes.

Shopping Around for Rates

Never accept the first offer you receive, especially with a 534 credit score. Rates can vary significantly between lenders. Apply with several different lenders – credit unions, online subprime lenders, and dealership finance departments – and compare their offers. Look beyond just the monthly payment; focus on the APR, total loan cost, and any hidden fees.

Common Mistakes to Avoid When Seeking a 534 Credit Score Car Loan

Making informed decisions is crucial when your credit score is challenging. Here are some pitfalls to steer clear of.

Applying Everywhere indiscriminately

While shopping around is good, applying for dozens of loans can backfire. Each "hard" inquiry can slightly lower your credit score. As mentioned, group your applications within a short timeframe to minimize the impact. Applying for too many credit lines in a short period signals desperation to lenders.

Not Having a Realistic Budget

Before you even look at cars, establish a clear budget. Factor in not just the monthly car payment, but also insurance, fuel, maintenance, and potential repair costs. Based on my experience, many people get approved for a loan but then struggle to afford the car’s overall expenses. A car loan with a 534 credit score will likely have higher payments, so an accurate budget is non-negotiable.

Ignoring the Total Cost of the Loan

Focusing solely on the monthly payment is a common and costly mistake. A longer loan term might offer lower monthly payments, but it significantly increases the total amount of interest you’ll pay over time. Always ask for the total cost of the loan, including all interest and fees, before signing any agreement.

Buying More Car Than You Can Afford

It’s tempting to want the latest model with all the bells and whistles, but this is a dangerous path with bad credit. Overextending yourself financially can lead to missed payments, repossession, and further damage to your credit score. Stick to a reliable, affordable vehicle that meets your needs without straining your budget.

Falling for Predatory Lenders

Be vigilant against lenders who pressure you into signing immediately, refuse to provide clear terms, or charge exorbitant fees without explanation. If something feels off, it probably is. Always read the fine print, ask questions, and don’t hesitate to walk away if you’re uncomfortable. Our pro tip from us: Reputable lenders will be transparent and allow you time to review documents.

After You Get the Loan: Rebuilding Your Credit

Securing a 534 credit score car loan isn’t just about getting a car; it’s also a powerful opportunity to rebuild your credit.

Making Timely Payments

This is the most critical step. Every single on-time payment you make will be reported to the credit bureaus and will positively impact your payment history – the largest factor in your credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date.

The Benefits of a Successfully Paid-Off Loan

A successfully paid-off car loan, especially one started with a lower credit score, demonstrates your ability to manage debt responsibly. This positive entry on your credit report can significantly boost your score, opening doors to better rates on future loans (like mortgages or personal loans) and credit cards.

Using This Loan as a Stepping Stone

View this car loan as a strategic stepping stone. As your credit score improves, you might even be able to refinance your car loan for a lower interest rate, saving you money. Continue practicing good financial habits: keep credit utilization low, pay bills on time, and regularly monitor your credit report for errors. For further guidance on repairing your financial standing, explore our article on Your Guide to Rebuilding Credit After a Car Loan.

Alternative Transportation Options (If a Loan Isn’t Feasible Right Now)

Sometimes, despite your best efforts, a car loan might not be the right move at this moment, or you might not qualify for favorable terms. It’s important to consider all options.

If a car loan with a 534 credit score proves too expensive or unattainable, explore alternatives. Public transportation, ride-sharing services, or even carpooling can be viable options. Saving up cash to buy a cheap, reliable used car outright could be a smarter financial move in the short term, allowing you to avoid high interest rates and simultaneously build up your credit through other means. This approach provides financial breathing room and allows you to improve your credit score before taking on significant debt.

Conclusion: Your Journey to Car Ownership and Beyond

Obtaining a 534 credit score car loan is undoubtedly challenging, but with the right knowledge, strategies, and perseverance, it is entirely achievable. This journey is not just about getting a new set of wheels; it’s also a significant opportunity to demonstrate financial responsibility and actively rebuild your credit for a stronger financial future.

Remember to prioritize a significant down payment, explore specialized lenders, consider a co-signer, and choose an affordable vehicle. Most importantly, commit to making every payment on time. By following these expert strategies and avoiding common pitfalls, you can successfully navigate the subprime auto loan market and transform your car loan into a powerful tool for credit improvement. Start planning today, take control of your financial narrative, and hit the road with confidence.