Navigating the Road to a Car Loan with a 560 Credit Score: Your Comprehensive Guide

Navigating the Road to a Car Loan with a 560 Credit Score: Your Comprehensive Guide Carloan.Guidemechanic.com

Getting approved for a car loan can feel like a daunting task, especially when your credit score isn’t in the "excellent" or "good" range. If you’re looking for a 560 credit score car loan, you’re likely facing the challenge of what’s considered a "poor" or "subprime" credit rating. But here’s the crucial truth: while it presents hurdles, securing an auto loan with a 560 credit score is absolutely possible. It simply requires a strategic approach, thorough preparation, and a clear understanding of the lending landscape.

This comprehensive guide is designed to empower you with the knowledge and actionable strategies needed to drive away in the car you need, even with a challenging credit history. We’ll delve deep into understanding your score, exploring your options, and outlining the steps to secure a loan that works for you.

Navigating the Road to a Car Loan with a 560 Credit Score: Your Comprehensive Guide

Understanding Your 560 Credit Score

Before we dive into loan strategies, let’s clarify what a 560 credit score actually means in the eyes of lenders. Credit scores typically range from 300 to 850. A score of 560 falls squarely into the "Poor" category, according to most major credit scoring models like FICO and VantageScore.

This designation indicates to lenders that you may represent a higher risk. Historically, individuals with scores in this range have a higher likelihood of defaulting on loans. Consequently, lenders will either be more hesitant to approve your application or will offer less favorable terms to offset their perceived risk.

What Contributes to a 560 Score?

Several factors can lead to a 560 credit score. Based on my experience in financial advising, common culprits include:

- Payment History Issues: Missed or late payments on credit cards, previous loans, or even utility bills are significant detractors.

- High Credit Utilization: Maxing out credit cards or using a large percentage of your available credit signals financial strain.

- Limited Credit History: If you’re new to credit, a lack of established history can keep your score low.

- Public Records: Bankruptcies, foreclosures, or collections accounts will severely impact your score.

- Too Many Hard Inquiries: Applying for multiple lines of credit in a short period can temporarily ding your score.

Understanding why your score is 560 is the first step toward improving it and effectively communicating your financial situation to potential lenders.

The Reality of Getting a Car Loan with a 560 Credit Score

Let’s be upfront: securing a car loan with a 560 credit score won’t be as straightforward as it is for someone with excellent credit. You should temper your expectations regarding interest rates and loan terms.

Higher Interest Rates Are Expected

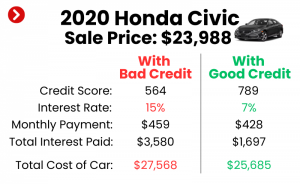

Lenders categorize a 560 score as "subprime." To compensate for the increased risk they take on, they will almost certainly charge a higher Annual Percentage Rate (APR) compared to borrowers with better credit. This means the total cost of your loan over its lifetime will be significantly higher. For example, while someone with a 700+ score might get an APR of 5-7%, you might see offers in the 15-25% range, or even higher.

Stricter Loan Terms

Beyond higher interest, you might also encounter stricter loan terms. This could include:

- Larger Down Payment Requirements: Lenders often ask for a more substantial down payment to reduce their loan exposure.

- Shorter Loan Terms: While a shorter term means higher monthly payments, it also means less interest paid overall and less risk for the lender.

- Limited Vehicle Options: You might find yourself approved for a lower loan amount, restricting your choice of vehicle to older, less expensive models.

Despite these challenges, it’s crucial to remember that approval is achievable. Many lenders specialize in subprime auto loans, understanding that people need reliable transportation regardless of their credit history.

Strategies to Increase Your Chances of Approval

Now, let’s focus on the actionable strategies that can significantly improve your odds of securing a 560 credit score car loan. These tips come from years of observing successful and unsuccessful loan applications.

1. Save for a Significant Down Payment

This is, perhaps, the single most impactful strategy for a borrower with a 560 credit score. A substantial down payment directly addresses the lender’s primary concern: risk.

- How it Helps: When you put down a larger sum of money, you reduce the amount you need to borrow. This lowers the lender’s financial exposure, making you a less risky proposition. It also shows the lender that you have some financial discipline and are invested in the purchase.

- Pro Tips from Us: Aim for at least 10-20% of the car’s purchase price, if not more. If you’re buying a $15,000 car, a $1,500 – $3,000 down payment can make a huge difference in approval and interest rates. Even a small down payment is better than none, but the more you can offer, the better your chances.

2. Consider a Co-Signer with Good Credit

Enlisting a co-signer can dramatically improve your loan application’s strength. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you fail to make payments.

- How a Co-Signer Helps: Lenders will factor in the co-signer’s strong credit history, making the loan appear less risky. This can lead to approval, and potentially even better interest rates than you’d get on your own.

- Common Mistakes to Avoid: Ensure both you and your co-signer fully understand the implications. If you miss payments, your co-signer’s credit will also be negatively affected, and they will be legally obligated to pay. This can strain relationships, so open communication is vital. Only ask someone you trust deeply, and who trusts you, to take on this responsibility.

3. Explore "Buy Here, Pay Here" Dealerships (with caution)

"Buy Here, Pay Here" (BHPH) dealerships are an option, but they come with significant caveats. These dealerships offer in-house financing, meaning they are both the seller and the lender.

- Pros: They often have very lenient approval standards, making it easier to get a loan with a 560 credit score. Your credit history is less of a barrier.

- Cons: The interest rates are typically much higher – sometimes reaching the maximum legal limit. The vehicle selection might be limited, and the cars may be older or have higher mileage. Crucially, many BHPH dealerships do not report your payments to credit bureaus, meaning on-time payments won’t help rebuild your credit score.

- Based on My Experience: While they offer a solution for immediate transportation needs, BHPH loans should generally be a last resort. Always compare their terms with other lenders first. If you go this route, ensure they report to credit bureaus to help your credit rebuilding journey.

4. Focus on Affordable and Reliable Vehicles

When your credit score is 560, it’s not the time to aim for a luxury car. Lenders are more comfortable financing a lower-risk asset.

- Lower Loan Amount, Lower Risk: Seeking a less expensive vehicle means you need to borrow less money. This inherently reduces the lender’s risk and makes approval more likely.

- Prioritize Reliability: Focus on a used car that has a strong reputation for reliability and low maintenance costs. You don’t want to be saddled with high loan payments and expensive repair bills.

- Pro Tip: Research vehicles known for holding their value and having reasonable insurance costs. This will make your overall cost of ownership more manageable.

5. Improve Your Credit Score First (If Time Allows)

If your need for a car isn’t immediate, taking some time to improve your credit score can save you thousands of dollars in interest. Even a 30-50 point increase can make a difference.

- Quick Wins:

- Pay Off Small Debts: Tackle any small outstanding balances on credit cards or collections.

- Dispute Errors: Obtain copies of your credit reports from all three major bureaus (Experian, Equifax, TransUnion) and dispute any inaccuracies.

- Reduce Credit Utilization: Try to pay down credit card balances to below 30% of your credit limit.

- Longer-Term Strategies:

- Consistent On-Time Payments: The most powerful way to build credit is to consistently pay all your bills on time, every time.

- Keep Old Accounts Open: The length of your credit history matters, so avoid closing old, established accounts.

(For a more detailed guide on boosting your credit, check out our article: )

6. Get Pre-Approved Before Visiting Dealerships

Getting pre-approved for a loan is a powerful tool for any car buyer, especially those with a 560 credit score.

- Benefits: Pre-approval gives you a clear idea of how much you can afford and the interest rate you qualify for before you step onto a car lot. This knowledge transforms you into a cash buyer in the eyes of the dealership, giving you significant leverage in negotiations.

- Where to Get Pre-Approved: Start with your local bank or credit union. They often have more flexible lending criteria for their members. Online lenders specializing in subprime auto loans are another excellent option.

Where to Apply for a 560 Credit Score Car Loan

Knowing where to direct your efforts can save you time and frustration. Not all lenders are equally willing or equipped to work with borrowers with a 560 credit score.

Specialized Subprime Lenders

A growing number of online lenders and financial institutions specialize in auto loans for individuals with poor credit. These lenders have different risk assessment models and are more accustomed to approving loans for scores like 560.

- Benefits: Higher approval rates for challenging credit. Streamlined online application processes.

- Drawbacks: May have higher interest rates than traditional banks or credit unions, even among subprime options.

- Examples: Companies like Capital One Auto Finance, Ally Financial, or dedicated subprime auto loan platforms.

Credit Unions

Don’t overlook your local credit union. Credit unions are member-owned and often have a more community-focused approach to lending.

- Benefits: They may be more flexible with their lending criteria, especially for existing members. You might find slightly better rates than specialized subprime lenders. They prioritize member relationships.

- Drawbacks: You typically need to be a member to apply, which might require opening an account.

Dealership Financing

Most dealerships offer financing options, either through their own captive finance companies (e.g., Ford Credit, Toyota Financial Services) or by partnering with a network of banks and lenders.

- Benefits: Convenience of one-stop shopping. Dealerships often have relationships with subprime lenders and can sometimes find an approval even if you’ve been turned down elsewhere.

- Negotiating Tips: Be wary of high-pressure sales tactics. Always compare the dealership’s financing offer with any pre-approvals you’ve secured elsewhere. Don’t let them push you into a deal that feels uncomfortable. Remember, their financing department might add their own mark-up to the interest rate they get from the lender.

The Application Process: What to Expect

When applying for a 560 credit score car loan, be prepared for a thorough review of your financial situation. Lenders will be looking for stability and your ability to repay the loan.

Required Documents

You’ll typically need to provide:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), tax returns if self-employed, or bank statements. Lenders want to see consistent income that can cover the monthly payment.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Proof of Insurance: You’ll need to secure full coverage insurance before driving off the lot.

- References: Sometimes, lenders may ask for personal references.

The Importance of Honesty

Always be honest and transparent on your application. Providing false information can lead to loan denial or even legal repercussions. Lenders will verify your income and other details.

Understanding the Loan Offer

Once approved, carefully review the loan offer. Pay close attention to:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and some fees.

- Loan Term: The length of time you have to repay the loan (e.g., 36, 48, 60 months).

- Monthly Payment: Ensure it fits comfortably within your budget.

- Total Cost of Loan: Calculate the total amount you’ll pay over the life of the loan, including interest.

Understanding Loan Terms and Avoiding Pitfalls

Securing a loan is just the first step. Understanding the terms and being aware of potential pitfalls is crucial, especially with a 560 credit score.

APR vs. Interest Rate

While often used interchangeably, the APR is the more comprehensive measure.

- Interest Rate: This is the percentage charged by the lender for borrowing the principal amount.

- APR (Annual Percentage Rate): This includes the interest rate plus any additional fees associated with the loan, such as origination fees. It provides a more accurate picture of the total annual cost of your loan. Always compare APRs when shopping for a loan.

Loan Term: Shorter vs. Longer

The loan term significantly impacts both your monthly payment and the total interest you pay.

- Shorter Term (e.g., 36-48 months): Higher monthly payments, but you pay less interest over the life of the loan. This is generally preferred if you can afford it.

- Longer Term (e.g., 60-72 months): Lower monthly payments, making the car seem more affordable. However, you’ll pay significantly more in total interest. With a 560 credit score, high interest rates compounded over a long term can be very costly.

Hidden Fees and Predatory Lending

- Common Fees: Watch out for documentation fees, loan origination fees, and extended warranty sales. Always ask for a full breakdown of all costs.

- Predatory Lending Warning Signs: Be cautious of lenders who pressure you into signing quickly, don’t provide clear terms, or offer "guaranteed approval" without any credit check. If a deal sounds too good to be true, it probably is.

- Pro Tips from Us: Always read the fine print of all documents before signing. Don’t be afraid to ask questions or walk away if something doesn’t feel right.

(For more information on consumer rights and financial protection, you can visit the Consumer Financial Protection Bureau’s website: ).

After You Get the Loan: Building a Better Financial Future

Getting a car loan with a 560 credit score is a big step. Now, it’s about leveraging this opportunity to rebuild your credit and improve your financial standing.

Make Payments On Time, Every Time

This is the golden rule. Consistent, on-time payments are the most effective way to improve your credit score. Every timely payment reported to the credit bureaus demonstrates your reliability as a borrower.

- Set Reminders: Use calendar alerts, automatic payments, or financial apps to ensure you never miss a due date.

- Pay More Than the Minimum (If Possible): Even a small extra payment each month can help reduce the principal faster and save you interest in the long run.

Refinancing Opportunities

Once you’ve made 6-12 months of on-time payments, and your credit score has shown improvement, you might be eligible to refinance your car loan.

- How it Works: Refinancing means taking out a new loan to pay off your old one, ideally at a lower interest rate.

- Benefits: A lower interest rate means lower monthly payments and/or less total interest paid over the life of the loan.

- When to Consider: If your credit score has improved significantly, or if interest rates have dropped since you took out your initial loan, explore refinancing options.

Monitor Your Credit Score

Regularly checking your credit score and report allows you to track your progress and catch any errors.

- Free Credit Reports: You’re entitled to a free credit report from each of the three major bureaus once a year via AnnualCreditReport.com.

- Credit Monitoring Services: Many banks and credit card companies now offer free credit score monitoring, or you can use services like Credit Karma or Experian.

- Track Your Progress: Seeing your score increase due to responsible payments is incredibly motivating.

Common Mistakes to Avoid When Seeking a 560 Credit Score Car Loan

Knowing what not to do is just as important as knowing what to do. Avoid these common missteps:

- Applying Everywhere: Each loan application results in a "hard inquiry" on your credit report, which can temporarily lower your score. Limit your applications to a few trusted lenders within a short window (typically 14-45 days, depending on the scoring model, to count as a single inquiry for rate shopping).

- Not Budgeting for Total Cost of Ownership: A car loan is just one part of car ownership. Don’t forget to budget for insurance, fuel, maintenance, repairs, and registration fees. These costs can quickly add up and strain your budget.

- Settling for the First Offer: Always shop around and compare offers from multiple lenders (banks, credit unions, online lenders, and dealerships). Even a slight difference in APR can save you hundreds or thousands of dollars over the loan term.

- Buying More Car Than You Can Afford: It’s tempting to stretch your budget for a nicer vehicle, but with a 560 credit score, it’s crucial to be conservative. A manageable monthly payment is key to avoiding default and rebuilding your credit.

- Ignoring the Fine Print: As mentioned, always read every line of your loan agreement. Understand all fees, terms, and conditions before you sign on the dotted line.

Conclusion: Your Journey to a Car Loan with a 560 Credit Score

Securing a 560 credit score car loan is not a pipe dream; it’s a tangible goal that many achieve every day. It requires patience, strategic planning, and a commitment to understanding the process. While you might face higher interest rates initially, view this as an opportunity. By diligently making your payments on time, you’re not just paying for a car; you’re actively rebuilding your credit and opening doors to better financial opportunities in the future.

Take control of your financial journey. Arm yourself with information, prepare your finances, and approach the lending process with confidence. With the right strategy, you can navigate the road to a car loan and drive towards a stronger financial future.