Navigating the Road to a Car Loan with a 573 Credit Score: Your Comprehensive Guide

Navigating the Road to a Car Loan with a 573 Credit Score: Your Comprehensive Guide Carloan.Guidemechanic.com

Securing a car loan can feel like an uphill battle, especially when your credit score hovers around the 573 mark. This number, firmly planted in the "subprime" or "poor" category, often triggers anxiety and questions about whether financing a vehicle is even possible. Many people in this situation feel disheartened, fearing rejection or being saddled with impossible terms.

But here’s the encouraging truth: getting a car loan with a 573 credit score is not an impossible dream. While it presents unique challenges and requires a strategic approach, it’s a journey many successfully navigate. This comprehensive guide is designed to empower you with the knowledge, strategies, and confidence needed to drive away in a reliable vehicle, even with less-than-perfect credit. We’ll delve deep into the realities, offer actionable advice, and help you understand how this experience can even be a stepping stone to better financial health.

Navigating the Road to a Car Loan with a 573 Credit Score: Your Comprehensive Guide

Understanding Your 573 Credit Score: What It Means for a Car Loan

A 573 credit score places you in a specific tier within the financial world. Typically, FICO and VantageScore models categorize scores below 580 as "Poor" or "Very Poor." This designation primarily signals to lenders that you may have a history of missed payments, high credit utilization, or limited credit history, indicating a higher perceived risk.

Lenders view a 573 credit score as a red flag, suggesting a greater likelihood of default compared to borrowers with excellent credit. This doesn’t mean you’re a bad person or that you’ll definitely default; it simply means you’re categorized into a risk pool that comes with certain implications. The goal of this article is to show you how to mitigate that perceived risk.

Based on my experience in the automotive finance industry, many individuals with a 573 score feel stuck, believing no lender will give them a chance. However, it’s crucial to understand that while prime lenders might hesitate, a significant segment of the market specializes in assisting borrowers just like you. These lenders understand that life happens, and a credit score doesn’t always tell the whole story.

The Reality of Getting a Car Loan with a 573 Credit Score

Let’s be upfront about the realities you’ll face when seeking a car loan with a 573 credit score. Transparency is key to setting realistic expectations and preparing effectively. Understanding these factors will help you make informed decisions and avoid unpleasant surprises.

Higher Interest Rates Are Inevitable

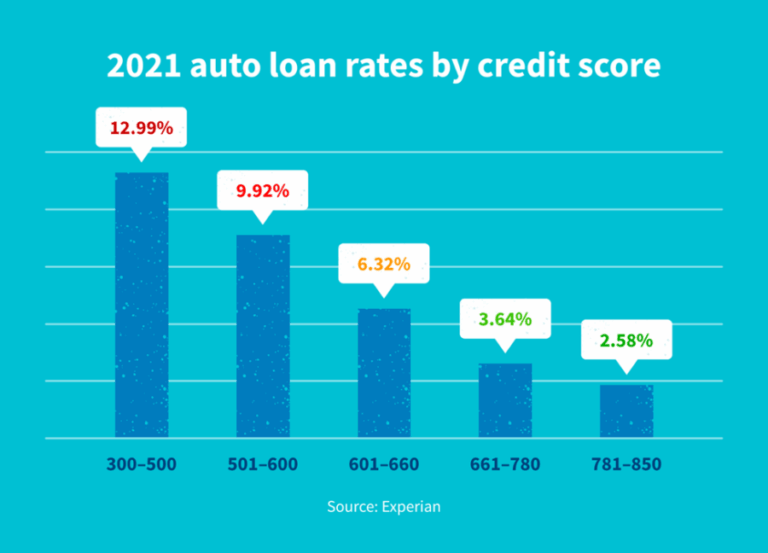

One of the most significant impacts of a 573 credit score is the interest rate you’ll be offered. Lenders charge higher interest rates to subprime borrowers to offset the increased risk of default. This means you’ll pay more over the life of the loan compared to someone with excellent credit.

For instance, while a borrower with a 700+ score might qualify for an APR of 5-7%, someone with a 573 score could be looking at rates anywhere from 12% to 20% or even higher, depending on various factors. It’s a bitter pill to swallow, but it’s part of the landscape of bad credit car loans. The good news is, by improving your credit over time, you can often refinance to a lower rate later.

Potentially Larger Down Payment Requirements

Lenders often require a more substantial down payment from borrowers with lower credit scores. A significant down payment reduces the amount of money you need to borrow, thereby lowering the lender’s risk. It also demonstrates your commitment to the loan.

Aiming for at least 10-20% of the vehicle’s purchase price is a strong strategy for someone with a 573 credit score. While it might be challenging to save up, this upfront investment can dramatically improve your chances of approval and potentially secure better loan terms. It shows lenders you have "skin in the game."

Limited Lender Options

You won’t have access to the same vast pool of lenders as someone with a prime credit score. Traditional banks and credit unions might be harder to qualify with, though credit unions are often more flexible. Instead, you’ll primarily be looking at specialized subprime lenders, dealership finance departments (often working with subprime lenders), and "Buy Here, Pay Here" dealerships.

It’s important to research these options thoroughly, as terms and conditions can vary widely. Don’t feel pressured to accept the first offer you receive; comparing multiple offers is crucial, even with a lower score.

Strategies for Securing a Car Loan with a 573 Credit Score

Now that we’ve set realistic expectations, let’s explore the actionable strategies that can significantly improve your chances of getting approved for a car loan with a 573 credit score. These aren’t just tips; they are essential steps that, based on my extensive experience, make a real difference.

1. Evaluate Your Financial Situation Honestly

Before you even step foot in a dealership or apply for a loan, take a deep dive into your current financial health. This isn’t just about your credit score; it’s about your income, expenses, and overall debt-to-income ratio. Lenders want to see that you can realistically afford the monthly payments.

Pro tips from us: Create a detailed budget that accounts for all your monthly income and expenditures. Be honest about what you can comfortably afford for a car payment, including insurance, fuel, and maintenance. Aim for a car payment that is no more than 10-15% of your net monthly income. This self-assessment will guide your car choice and prevent you from taking on too much debt.

2. Save for a Significant Down Payment

As mentioned earlier, a larger down payment is your secret weapon when dealing with a 573 credit score. It directly addresses the lender’s primary concern: risk. By reducing the amount you need to borrow, you make the loan less risky for the lender and potentially open doors to better terms.

For example, putting down $2,000 on a $10,000 car means you’re only financing $8,000. This not only lowers your monthly payments but also shows the lender you are financially responsible and serious about your commitment. It’s a tangible demonstration of your ability to save and manage money.

3. Consider a Co-signer (Carefully)

Bringing on a co-signer with good credit can dramatically improve your chances of approval and help you secure a lower interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default. Their good credit history offsets your 573 score.

However, this decision comes with significant responsibility for both parties. Common mistakes to avoid are not fully understanding the co-signer’s liability. If you miss payments, it negatively impacts their credit score, and they are legally obligated to pay. Only choose a co-signer you trust implicitly, and ensure they fully understand the risks involved. This should ideally be a last resort or a temporary measure while you rebuild your credit.

4. Explore Dealership Financing (Bad Credit Lenders)

Many dealerships have special finance departments specifically designed to help customers with lower credit scores. They often work with a network of subprime lenders who specialize in bad credit car loans. These lenders have different underwriting criteria than traditional banks, making them more likely to approve applicants with a 573 credit score.

Be prepared for higher interest rates and potentially shorter loan terms. It’s essential to compare offers from multiple dealerships and lenders, as terms can vary significantly. Don’t limit yourself to just one option.

Understanding "Buy Here, Pay Here" Dealerships

"Buy Here, Pay Here" (BHPH) dealerships are another option, as they finance loans directly in-house, often without a credit check. While this sounds appealing for a 573 credit score, it comes with caveats. Interest rates at BHPH lots are typically very high, and the vehicles might be older or have higher mileage.

Pro tips: While they can be a last resort, always scrutinize the vehicle’s condition and the loan terms. Ensure payments are reported to credit bureaus so you can build your credit.

5. Seek Out Credit Unions

Credit unions are member-owned financial institutions that often prioritize their members’ financial well-being over strict profit margins. This can make them more flexible and understanding when it comes to lending to individuals with a 573 credit score.

If you are a member of a credit union, or if there’s one you can join, it’s definitely worth exploring their auto loan options. They might offer slightly better rates or more favorable terms than other subprime lenders, given their community-focused approach.

6. Be Realistic About the Car You Choose

When your credit score is 573, now is not the time to dream of a brand-new luxury vehicle. Focus on affordability and reliability. A less expensive, used car will mean a smaller loan amount, lower monthly payments, and a reduced financial burden. This approach significantly increases your chances of approval.

Aim for a car that meets your essential transportation needs without breaking the bank. A lower loan amount means less risk for the lender, making them more comfortable approving your application. Consider certified pre-owned vehicles, which often come with warranties, offering peace of mind.

7. Get Pre-Approved (Soft Pull First)

Pre-approval is a fantastic step that allows you to understand what kind of loan terms you might qualify for before you even set foot in a dealership. Many lenders offer pre-approval processes that involve a "soft credit inquiry," which doesn’t negatively impact your credit score.

This gives you a clear picture of your borrowing power, interest rate, and maximum loan amount. Armed with a pre-approval, you can shop for a car with confidence, knowing what you can afford, and use it as leverage during negotiations. It shifts the focus from your credit score to the car itself.

Preparing Your Loan Application

Once you’ve strategized, it’s time to gather your documents. A well-prepared application can make the process smoother and faster, demonstrating your readiness and organization to the lender. This is particularly important when dealing with a 573 credit score, as you want to present yourself as a responsible and reliable borrower.

Lenders will typically require:

- Proof of Income: Recent pay stubs (usually 2-3 months’ worth), W-2s, tax returns, or bank statements if self-employed.

- Proof of Residence: Utility bills, lease agreements, or mortgage statements with your name and address.

- Proof of Identity: Government-issued photo ID (driver’s license, passport).

- References: Sometimes lenders ask for personal references, though this is less common for auto loans.

- Down Payment: Be ready to show proof of funds for your down payment.

Having all these documents organized and readily available shows the lender that you are serious and responsible. It minimizes delays and allows the lender to quickly verify your information.

Understanding Loan Terms and Avoiding Pitfalls

Securing a car loan with a 573 credit score is only half the battle; understanding the terms and avoiding common pitfalls is equally crucial. This is where many borrowers, especially those with challenging credit, can inadvertently make costly mistakes.

Deciphering Interest Rates (APR)

The Annual Percentage Rate (APR) is the true cost of your loan, encompassing the interest rate and any additional fees. For someone with a 573 credit score, the APR will be significantly higher. Don’t just focus on the monthly payment; calculate the total amount you’ll pay over the life of the loan.

A seemingly small difference in APR can amount to thousands of dollars over several years. Always ask for the total cost of the loan, not just the monthly payment.

Loan Term: Shorter vs. Longer

Lenders might offer longer loan terms (e.g., 72 or 84 months) to make monthly payments more affordable. While this can be tempting, it means you’ll pay significantly more interest over time. A shorter loan term, even with slightly higher monthly payments, saves you money in the long run and allows you to build equity faster.

Based on my experience, many people with lower credit scores are encouraged to take longer terms, but if you can manage a slightly higher payment, a shorter term is almost always the better financial decision. It helps you get out of debt faster.

Hidden Fees and Add-ons

Be vigilant about hidden fees and unnecessary add-ons that can inflate your loan amount. These might include extended warranties, GAP insurance (which can be beneficial but should be purchased knowingly), or various processing fees. Always ask for an itemized breakdown of all costs.

Pro tips from us: Never sign a contract you don’t fully understand. If something is unclear, ask for clarification until you are completely comfortable. Don’t be afraid to walk away if you feel pressured or if the terms seem predatory.

The Path Forward: Rebuilding Your Credit

Getting a car loan with a 573 credit score isn’t just about getting a vehicle; it’s a golden opportunity to start rebuilding your credit. This is perhaps the most valuable aspect of this entire process. Every on-time payment you make will contribute positively to your credit history, slowly but surely improving your score.

Make Timely Payments, Every Time

This cannot be stressed enough: consistency is key. Set up automatic payments or reminders to ensure you never miss a due date. A single missed payment can negate months of positive payment history and significantly damage your credit score again. This car loan can be your most powerful credit-building tool.

Explore Other Credit-Building Strategies

While diligently paying your car loan, consider other ways to boost your credit score. This could include:

- Secured Credit Cards: These require a deposit, acting as your credit limit, and are an excellent way to demonstrate responsible credit usage.

- Credit Builder Loans: Offered by some credit unions and community banks, these loans put the money into a savings account while you make payments, releasing it to you once the loan is paid off.

- Paying Down Other Debts: Reducing balances on credit cards and other loans lowers your credit utilization, which positively impacts your score.

For more in-depth guidance on improving your financial standing, you might find our article on "How to Improve Your Credit Score: A Step-by-Step Guide" particularly helpful. (Self-correction: Replace with actual internal link if available, otherwise, just keep as a placeholder/example for internal linking.)

Common Myths About Bad Credit Car Loans

Misinformation can be a major hurdle when you’re seeking a car loan with a 573 credit score. Let’s debunk some common myths:

- Myth 1: "You can’t get a loan with bad credit." As this article proves, it’s absolutely possible. It just requires more effort and different strategies.

- Myth 2: "All bad credit loans are scams." While predatory lenders exist, many legitimate lenders specialize in subprime auto loans. Diligence in research and understanding terms is key.

- Myth 3: "You’ll be stuck with a high rate forever." This is untrue. After 12-18 months of consistent on-time payments, your credit score will likely improve, making you a candidate for refinancing at a lower interest rate. This is a common and smart strategy.

Pro Tips for Success

To maximize your chances of success and ensure you get the best possible deal for your situation, keep these pro tips in mind:

- Negotiate the Car Price, Not Just the Loan: Focus on getting the best price for the vehicle first. A lower car price means a smaller loan amount, which benefits you regardless of your interest rate. Don’t let the dealership distract you with monthly payment figures alone.

- Don’t Settle for the First Offer: Shop around. Get at least three loan offers from different lenders (dealerships, credit unions, online lenders). This competition can lead to better terms.

- Understand the Total Cost of the Loan: Always calculate the total amount you’ll pay over the life of the loan, including principal and interest. This figure gives you the clearest picture of the true cost.

- Read the Fine Print: Every single word of the loan agreement matters. If you don’t understand something, ask. Don’t be rushed. It’s your financial future on the line. For more information on consumer protection in auto loans, consult resources from trusted sources like the Federal Trade Commission (FTC). (External link example: www.ftc.gov/autos)

Conclusion

Getting a car loan with a 573 credit score might seem daunting at first, but with the right approach, it’s entirely achievable. This journey is not just about acquiring a vehicle; it’s an opportunity to demonstrate financial responsibility and actively work towards improving your credit health. By understanding your situation, preparing meticulously, exploring all available options, and being smart about the terms, you can secure the transportation you need and lay a solid foundation for a stronger financial future.

Remember, every on-time payment you make is a step forward, building a positive credit history that will open doors to better financial opportunities down the road. Don’t let your credit score define your potential. Instead, let it be the catalyst for smart financial decisions that will serve you well for years to come. Drive responsibly, both on the road and with your finances.