Navigating the Road to a Car Loan with a 597 Credit Score: Your Comprehensive Guide

Navigating the Road to a Car Loan with a 597 Credit Score: Your Comprehensive Guide Carloan.Guidemechanic.com

For many, owning a car is more than a convenience; it’s a necessity, a symbol of independence, and a gateway to opportunities. However, the path to vehicle ownership can seem daunting, especially when your credit score isn’t in the prime range. If you’re looking to secure a car loan with a 597 credit score, you’re likely facing some unique challenges.

But here’s the good news: getting a car loan with a 597 credit score is absolutely possible. It simply requires a strategic approach, a clear understanding of the landscape, and a commitment to smart financial decisions. This comprehensive guide is designed to empower you with the knowledge and actionable steps needed to drive away in your next vehicle, even with a less-than-perfect credit history. We’ll delve deep into what a 597 score means, what to expect, and how to maximize your chances of approval, all while focusing on building a stronger financial future.

Navigating the Road to a Car Loan with a 597 Credit Score: Your Comprehensive Guide

Understanding Your 597 Credit Score: What It Means for Auto Financing

A credit score is a three-digit number that lenders use to assess your creditworthiness. It’s a snapshot of your financial reliability, based on your borrowing and repayment history. Your 597 credit score falls into what’s typically considered the "poor" or "subprime" category, according to common scoring models like FICO and VantageScore.

This designation doesn’t mean you’re a bad person or inherently irresponsible. Often, a 597 score can be the result of past financial challenges, such as late payments, high credit card utilization, a limited credit history, or even bankruptcy. Understanding why your score is 597 is the first step toward improving it and making informed decisions about your car loan.

Based on my experience as a financial content writer, a credit score in the 500s signals to lenders that there’s a higher risk associated with lending you money. They might perceive a greater chance of default compared to borrowers with excellent credit. This perception directly impacts the terms you’ll be offered, from interest rates to down payment requirements. Don’t despair, though; many lenders specialize in working with individuals in your exact situation.

The Reality of Getting a Car Loan with a 597 Credit Score

Let’s be upfront: securing a car loan with a 597 credit score presents certain hurdles. It’s not as straightforward as it would be with a prime score, but it is far from impossible. The key is to manage your expectations and prepare thoroughly.

The primary challenge you’ll face is higher interest rates. Lenders mitigate the increased risk associated with subprime borrowers by charging more for the loan. This means your monthly payments will be higher, and the total cost of the car over the loan term will be significantly greater than for someone with good credit. Additionally, you might encounter stricter loan terms, such as shorter repayment periods or requirements for a larger down payment.

Common mistakes to avoid are expecting the same rates and terms as someone with a 700+ credit score, or giving up before you even try. Many dealerships and specialized lenders are specifically set up to help individuals with lower credit scores. Your success hinges on smart preparation and knowing where to look.

Strategies to Dramatically Improve Your Chances (Before You Apply)

Before you even step foot into a dealership or submit an online application, there are several proactive steps you can take to strengthen your position. These strategies won’t just help you get approved; they’ll help you secure better terms.

1. Know Your Credit Report Inside Out

Your credit score is derived from your credit report. It’s absolutely crucial to obtain copies of your credit reports from all three major bureaus (Experian, Equifax, and TransUnion) and review them meticulously. You can do this for free once a year at AnnualCreditReport.com.

Look for any inaccuracies, such as accounts that aren’t yours, incorrect payment statuses, or outdated information. Even a small error could be dragging your score down. If you find discrepancies, dispute them immediately with the credit bureau. Correcting errors can sometimes boost your score surprisingly quickly.

2. Save for a Substantial Down Payment

This is perhaps the single most impactful step you can take with a 597 credit score. A significant down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. It shows the lender that you have "skin in the game" and are committed to the purchase.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price, if possible. The more you put down, the lower your monthly payments will be, and the less interest you’ll pay over the life of the loan. A larger down payment can also make a hesitant lender more likely to approve your loan.

3. Reduce Your Existing Debt

Your debt-to-income (DTI) ratio is another critical factor lenders consider. This ratio compares your total monthly debt payments to your gross monthly income. A high DTI can signal that you’re overextended and might struggle with new debt.

Focus on paying down high-interest debts, especially credit card balances, before applying for a car loan. Even a small reduction in your overall debt can improve your DTI and make you a more attractive borrower. This also frees up more of your income for a car payment.

4. Stabilize Your Employment and Income

Lenders want to see stability. If you’ve been at your current job for a reasonable period (typically six months to a year or more) and have a consistent income, it demonstrates reliability. Gather pay stubs, bank statements, and any other documentation that proves your steady employment and income.

If you’ve recently changed jobs, be prepared to explain the circumstances. A promotion or a move to a higher-paying position can be viewed positively, but frequent job hopping might raise red flags.

5. Consider a Co-signer (If Available)

A co-signer is someone with good credit who agrees to take on the responsibility of the loan if you fail to make payments. This can significantly improve your chances of approval and potentially secure better loan terms, as the lender has an additional guarantee.

Choose your co-signer wisely. This should be someone you trust implicitly, and who trusts you. Remember, if you miss payments, it will negatively affect both your credit scores. Ensure both parties understand the full implications before proceeding.

Where to Look: Types of Lenders for Subprime Car Loans

Not all lenders are created equal, especially when it comes to borrowers with lower credit scores. Knowing where to focus your efforts can save you time and frustration.

1. Dealership Financing

Many dealerships offer in-house financing or work with a network of lenders, including those who specialize in subprime auto loans.

- Captive Finance Companies: These are financing arms of car manufacturers (e.g., Ford Credit, Toyota Financial Services). While they often target prime borrowers, some have programs for those with lower scores, especially for their own brand’s vehicles.

- Buy Here, Pay Here (BHPH) Dealerships: These dealerships act as both the seller and the lender. They are often very willing to work with individuals with bad credit because they finance the loans themselves. However, be very cautious with BHPH lots. They often come with extremely high interest rates, older vehicles, and strict repayment terms. While they offer high approval rates, the overall cost can be exorbitant.

2. Credit Unions

Credit unions are often a fantastic option for borrowers with less-than-perfect credit. As member-owned institutions, they tend to be more flexible and empathetic than traditional banks. They may be more willing to look beyond just your credit score and consider your overall financial situation, including your relationship with the credit union.

Their interest rates are also often more competitive than those offered by traditional banks or subprime lenders. It’s worth exploring local credit unions and their auto loan offerings.

3. Online Lenders Specializing in Bad Credit

The digital age has brought forth a number of online lenders who specialize in subprime auto loans. These lenders often have streamlined application processes and can provide pre-approvals quickly. They are specifically designed to cater to borrowers with credit scores like 597.

Many of these platforms allow you to get pre-qualified without a hard credit inquiry, which is excellent for shopping around and comparing offers without impacting your score. Examples include Carvana, Capital One Auto Finance, and specialized bad credit auto loan providers.

4. Traditional Banks

While traditional banks (like Chase, Wells Fargo, Bank of America) generally prefer borrowers with good to excellent credit, it’s still worth checking with your current bank. They might be more lenient with existing customers, especially if you have a long-standing relationship and a positive banking history with them. However, their approval standards for a 597 score will likely be higher than specialized subprime lenders.

What to Expect When Applying for a Car Loan with a 597 Credit Score

Setting realistic expectations is crucial to a successful car loan experience when you have a 597 credit score.

1. Higher Interest Rates Are Inevitable

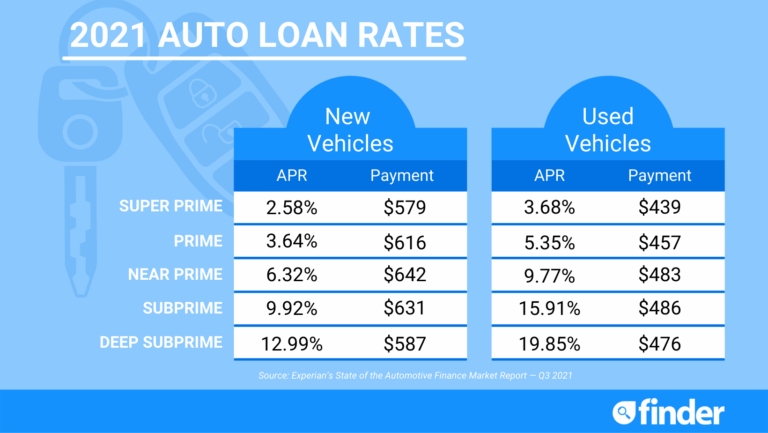

As mentioned, lenders offset the risk of a lower credit score with higher interest rates. While a borrower with excellent credit might get an APR (Annual Percentage Rate) in the low single digits, you should expect rates ranging from 10% to 25% or even higher, depending on the lender, loan term, and vehicle.

This higher interest significantly increases the total cost of the loan over time. Focus on making timely payments to eventually qualify for refinancing at a lower rate.

2. Down Payment Expectations

A substantial down payment will almost certainly be expected. While 10-20% is a good target, some lenders might require even more, or suggest it strongly, to approve your loan. This shows your commitment and reduces their financial exposure.

3. Loan Terms and Vehicle Restrictions

Lenders might offer different loan terms. Shorter terms mean higher monthly payments but less interest paid overall. Longer terms reduce monthly payments but dramatically increase the total interest paid and the risk of being "upside down" (owing more than the car is worth).

You might also find some restrictions on the type of vehicle you can finance. Lenders often prefer newer, more reliable used cars (typically less than 7-8 years old and under 100,000 miles) because they hold their value better, reducing the lender’s risk if they need to repossess it.

4. Required Documentation

Be prepared to provide a range of documents to verify your identity, income, and residence. This typically includes:

- Government-issued ID (driver’s license)

- Proof of residence (utility bill, lease agreement)

- Proof of income (recent pay stubs, bank statements, tax returns for self-employed)

- Proof of insurance (before driving off the lot)

- References (sometimes required by subprime lenders)

The Application Process: Step-by-Step for a 597 Credit Score

Navigating the application process strategically can make a significant difference in your outcome.

Step 1: Get Pre-Approved (Soft Inquiry First)

Start by getting pre-approved through multiple lenders, especially online lenders and credit unions. Many offer pre-qualification that uses a "soft inquiry," which doesn’t affect your credit score. This gives you an idea of what loan amount and interest rate you might qualify for before you commit to a specific vehicle or a hard credit check.

Having a pre-approval in hand gives you leverage at the dealership and helps you set a realistic budget.

Step 2: Shop Around and Compare Offers

Once you have a few pre-approvals, compare them carefully. Don’t just look at the monthly payment. Pay close attention to:

- APR: This is the true cost of borrowing.

- Loan Term: How many months will you be paying?

- Total Cost of the Loan: Multiply your monthly payment by the number of months, then add your down payment.

- Any Fees: Origination fees, processing fees, etc.

Remember, even a slight difference in APR can save you hundreds or thousands of dollars over the life of the loan.

Step 3: Negotiate Smartly (Beyond Just the Price)

Armed with your pre-approval, you can negotiate with the dealership. You’re not just negotiating the car’s price; you’re also negotiating the financing terms. If the dealership can beat your pre-approved rate, great! If not, you have a solid offer to fall back on.

Based on my experience, it’s always best to separate the car price negotiation from the financing negotiation. Get the best price on the car first, then discuss financing. This prevents the dealer from hiding a higher interest rate behind a seemingly good car price.

Step 4: Read the Fine Print

Before signing any documents, read everything thoroughly. Understand all the terms and conditions, including any prepayment penalties, late fees, and what happens if you miss a payment. Don’t hesitate to ask questions if anything is unclear.

Beyond the Loan: Building Credit for the Future

Getting a car loan with a 597 credit score isn’t just about driving a new vehicle; it’s also a powerful opportunity to rebuild and improve your credit.

Make All Payments On Time, Every Time

This is the single most important action you can take. Your payment history accounts for 35% of your FICO score. Consistently making your car loan payments on time will show lenders that you are a responsible borrower, and your credit score will steadily improve. Set up automatic payments to avoid missing due dates.

Consider Refinancing Later

Once you’ve made 6-12 months of on-time payments, your credit score will likely have improved. At that point, you can explore refinancing your car loan. Refinancing allows you to replace your current high-interest loan with a new one at a lower interest rate, saving you money and potentially reducing your monthly payments. You can learn more about understanding car loan interest rates and how they affect your overall costs in our detailed guide.

The Car Loan as a Credit-Building Tool

View this car loan as a stepping stone. It’s a significant installment loan that, when managed properly, can significantly boost your credit profile. As your score rises, you’ll gain access to better financial products, from credit cards to mortgages, at more favorable terms. For more strategies on rapid credit score improvement, check out our dedicated article.

Alternatives to a Traditional Car Loan with a 597 Credit Score

If the terms for a traditional car loan seem too steep, or you’re not comfortable with the risk, consider these alternatives:

1. Save Up and Buy Used with Cash

The most financially sound option, if feasible, is to save up enough money to buy a reliable used car outright with cash. This eliminates interest payments entirely and ensures you won’t be saddled with debt. It might mean delaying your purchase, but it’s a debt-free path to ownership.

2. Ridesharing or Public Transportation

If a car isn’t an immediate necessity, consider using ridesharing services, public transportation, or even carpooling for a while. This temporary solution allows you to save money, improve your credit, and then pursue a car loan on better terms in the future.

3. Leasing (with Caution)

While leasing is typically geared towards those with good credit, some dealerships might offer leases to subprime borrowers, often requiring a larger down payment and higher monthly payments. However, leasing can be complex, and you don’t build equity. It’s generally not recommended for those looking to build credit or save money with a 597 score, but it’s an option to be aware of.

Conclusion: Your Journey to Car Ownership and Beyond

Securing a car loan with a 597 credit score is a journey that requires patience, research, and strategic action. While the road may have more bumps than for those with higher scores, it is certainly navigable. By understanding what your score means, preparing thoroughly, knowing where to seek financing, and managing your expectations, you can successfully obtain the vehicle you need.

More importantly, view this as an opportunity. This car loan can be a powerful tool for rebuilding your credit and paving the way for a more financially secure future. By making consistent, on-time payments, you’ll not only enjoy the freedom of car ownership but also steadily improve your credit score, opening doors to better financial opportunities down the line.

Don’t let a past financial misstep define your future. Take control, apply the strategies outlined in this guide, and start your journey towards car ownership and improved financial health today! Remember, the goal isn’t just to get the loan, but to use it wisely and build a stronger credit profile for tomorrow.

External Link: For more information on understanding your credit report and disputing errors, visit the official Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/