Navigating the Road to a Car Loan with a 625 Credit Score: Your Comprehensive Guide

Navigating the Road to a Car Loan with a 625 Credit Score: Your Comprehensive Guide Carloan.Guidemechanic.com

Getting a car loan can feel like a daunting journey, especially when you’re uncertain about how your credit score will impact the process. If you find yourself with a 625 credit score, you’re in a common position: you’re not in the "prime" tier, but you’re also far from being considered "bad credit." This "fair" credit standing opens up many opportunities, but it also requires a strategic approach.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to secure a 625 credit score car loan. We’ll delve deep into what lenders look for, how to optimize your application, and what to expect regarding interest rates and terms. Our ultimate goal is to make your car financing experience smooth, informed, and successful, ensuring you drive away with a deal that truly works for you.

Navigating the Road to a Car Loan with a 625 Credit Score: Your Comprehensive Guide

Understanding Your 625 Credit Score in the Auto Loan Landscape

A 625 credit score typically falls within the "Fair" range on the FICO scale, which generally spans from 300 to 850. While it’s above the poor credit threshold, it indicates that you may have some areas for improvement in your credit history. Lenders perceive this score as carrying a moderate level of risk.

Based on my experience, lenders categorize credit scores to gauge a borrower’s reliability. A 625 score means you’ve likely had some late payments in the past, a higher credit utilization ratio, or perhaps a shorter credit history. These factors collectively tell a story about your financial habits.

However, it’s crucial to understand that a 625 score doesn’t close the door to car ownership. Many lenders specialize in working with individuals in this credit tier. They understand that life happens, and a credit score is just one piece of the puzzle when assessing your ability to repay a loan.

What Does a 625 Score Signal to Lenders?

When a lender sees a 625 credit score, they interpret it as a sign of potential risk. It suggests that while you generally make payments, there might have been occasional missed due dates or high balances on your credit cards. These habits can sometimes lead to a slightly higher interest rate compared to someone with excellent credit.

From an expert’s perspective, a 625 score doesn’t automatically disqualify you; it simply means lenders will conduct a more thorough review of your overall financial situation. They’ll look at your income, employment stability, debt-to-income ratio, and down payment amount. These additional factors become even more critical for a 625 credit score car loan.

Is a 625 Credit Score Good Enough for a Car Loan? Absolutely!

The short answer is a resounding yes, a 625 credit score is absolutely good enough to secure a car loan. While you might not qualify for the absolute lowest advertised interest rates, you are firmly in a position where numerous lenders will consider your application. Don’t let initial hesitation or outdated information deter you.

Many financial institutions, including banks, credit unions, and specialized auto lenders, actively cater to borrowers with fair credit. They recognize the vast market segment that falls into this credit range and have tailored products to meet their needs. Your focus should be on finding the right lender and presenting the strongest possible application.

Pro tips from us: The key isn’t just getting approved, but getting approved on favorable terms. With a 625 credit score, you have leverage if you approach the process strategically. Preparing thoroughly can significantly impact the interest rate and overall cost of your loan.

Preparing for Your Car Loan Application: Laying the Groundwork

Preparation is paramount when seeking a 625 credit score car loan. A well-prepared applicant signals responsibility and reliability to lenders, potentially leading to better terms. This proactive approach can make a significant difference in your approval odds and the final cost of your vehicle.

1. Know Your Credit Score and Report Inside Out

Before you even think about visiting a dealership, pull your credit reports from all three major bureaus (Experian, Equifax, and TransUnion). You can do this for free once a year at AnnualCreditReport.com. This trusted external source provides a comprehensive view of your credit history.

Carefully review each report for inaccuracies or errors. Common mistakes to avoid are not checking for old accounts that should be closed, incorrect payment statuses, or identity theft. Disputing and correcting errors can potentially boost your score before you apply, improving your chances for a better 625 credit score car loan.

2. Craft a Realistic Budget

Understanding what you can truly afford each month is non-negotiable. Your budget should encompass not only the car loan payment but also insurance, fuel, maintenance, and potential parking fees. Overextending yourself is a common mistake that can lead to financial strain down the road.

Use an online car loan calculator to estimate monthly payments based on different interest rates and loan terms. This will give you a clear picture of what fits comfortably within your existing financial commitments. Remember, a car is a necessity, but it shouldn’t become a financial burden.

3. Maximize Your Down Payment

A substantial down payment is one of your most powerful tools when applying for a 625 credit score car loan. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. Lenders also view a larger down payment as a sign of commitment and reduced risk.

Based on my experience, a down payment of 10% to 20% of the vehicle’s price is often recommended. If you can manage more, it will only strengthen your application. Consider saving aggressively for a few months or selling an old vehicle to boost your down payment fund.

4. Consider Your Trade-In

If you have an existing vehicle, using it as a trade-in can function much like a down payment. The value of your trade-in will be subtracted from the new car’s price, reducing the amount you need to finance. This can significantly improve your loan-to-value (LTV) ratio, which lenders favor.

Get an estimate of your car’s trade-in value from multiple sources, such as Kelley Blue Book or Edmunds, before heading to the dealership. This ensures you have an informed starting point for negotiation. Don’t just accept the first offer; know your car’s worth.

5. Gather All Necessary Documents

Streamlining your application process involves having all your documents ready. This typically includes:

- Proof of identity (driver’s license, passport)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of insurance (you’ll need this before driving off the lot)

- References (sometimes required, but less common for auto loans)

Having these readily available demonstrates your preparedness and can expedite the approval process for your 625 credit score car loan.

Where to Get a Car Loan with a 625 Credit Score

With a 625 credit score, you have several avenues to explore for financing. Each option has its own advantages, and shopping around is critical to finding the best deal. Common mistakes to avoid are simply accepting the first offer presented to you without comparison.

Dealership Financing

Most dealerships offer in-house financing options, working with a network of banks and credit unions. This can be convenient, as you can handle the entire car-buying and financing process in one place. Dealerships often have relationships with lenders who specialize in various credit tiers, including fair credit.

However, while convenient, dealership financing might not always yield the absolute lowest interest rate. It’s a good starting point, but it should be compared with other offers. Be prepared to negotiate not just the car price but also the financing terms.

Banks and Credit Unions

Traditional banks and credit unions are excellent sources for auto loans. Credit unions, in particular, are known for offering competitive rates and more personalized service to their members, even for those with fair credit scores. They often prioritize member relationships over strict credit score cutoffs.

Applying for pre-approval from a bank or credit union before visiting a dealership is a smart move. A pre-approval letter gives you concrete financing terms, empowering you to negotiate the car’s price as a cash buyer. This significantly strengthens your position when seeking a 625 credit score car loan.

Online Lenders

The digital age has brought a surge of online lenders specializing in auto loans for a wide range of credit scores. Many of these platforms offer quick applications and rapid approval decisions. They can be particularly useful for comparing multiple offers from different lenders without impacting your credit score significantly (if done within a short shopping window).

Online lenders often have proprietary algorithms that allow them to assess risk differently, sometimes making them more flexible for fair credit borrowers. This can lead to competitive rates for a 625 credit score car loan that you might not find elsewhere. Just ensure you’re working with reputable and secure platforms.

Strategies to Improve Your Chances of Approval and Get Better Terms

Even with a 625 credit score, there are proactive steps you can take to enhance your loan application and secure more favorable terms. These strategies demonstrate your commitment and financial prudence to lenders.

1. Increase Your Down Payment

As mentioned earlier, a larger down payment is arguably the most impactful immediate action you can take. It directly reduces the lender’s risk and shows your financial commitment. For a 625 credit score car loan, this could mean the difference between approval and rejection, or between a high and a more manageable interest rate.

2. Consider a Co-signer

If you have a trusted friend or family member with excellent credit who is willing to co-sign your loan, this can significantly improve your chances of approval and secure a lower interest rate. A co-signer essentially guarantees the loan, taking on the responsibility if you default.

However, this decision should not be taken lightly. A co-signer’s credit will be affected by the loan, and any missed payments will harm both your credit scores. Ensure both parties fully understand the responsibilities involved before proceeding.

3. Shop Around for Multiple Pre-approvals

Don’t settle for the first loan offer you receive. Apply for pre-approval from at least three to four different lenders (banks, credit unions, and online lenders). When done within a focused 14-45 day window, multiple inquiries for the same type of loan are typically treated as a single hard inquiry by credit bureaus, minimizing the impact on your score.

This process allows you to compare interest rates, loan terms, and fees directly. Having multiple offers in hand gives you powerful negotiation leverage, especially when dealing with dealership financing for your 625 credit score car loan.

4. Choose the Right Car

The type of car you choose can also influence your loan terms. Lenders consider the vehicle’s value and marketability as collateral. Newer, more reliable cars with a strong resale value often qualify for better rates than very old or high-mileage vehicles.

Additionally, avoid overspending. Stick to your budget and opt for a car that is practical and affordable. Trying to finance a luxury vehicle with a fair credit score will likely result in higher rates or even rejection.

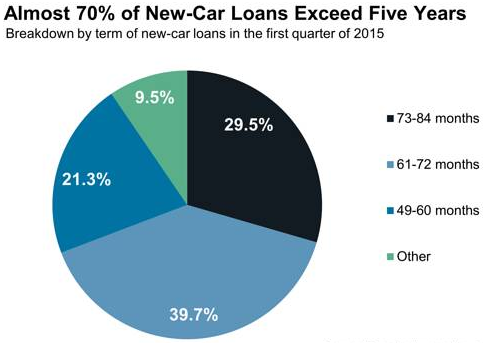

5. Shorten the Loan Term (If Affordable)

While a longer loan term means lower monthly payments, it also means you’ll pay significantly more in interest over the life of the loan. If your budget allows, opting for a shorter loan term (e.g., 48 or 60 months instead of 72 or 84 months) can drastically reduce the total interest paid.

For a 625 credit score car loan, a shorter term demonstrates your ability to manage higher payments and reduces the lender’s exposure to risk over time. Always balance affordability with the total cost of the loan.

6. Boost Your Credit Score (Pre-Application)

If you have some time before you need a car, focus on improving your credit score. Even a small increase can open up better loan options.

- Pay all your bills on time: Payment history is the most significant factor in your credit score.

- Reduce credit card balances: Lowering your credit utilization ratio (amount of credit used vs. available) can quickly boost your score. Aim for under 30%.

- Avoid new credit applications: Each new application can cause a small dip in your score.

- Monitor your credit report: Dispute any errors promptly.

For a deeper dive into improving your credit score, check out our comprehensive guide: .

Understanding Interest Rates and Terms for a 625 Credit Score

When you’re looking for a 625 credit score car loan, it’s essential to have realistic expectations regarding interest rates and terms. While you won’t get prime rates, you also shouldn’t accept rates typically offered to those with very poor credit.

What to Expect

For borrowers with a 625 credit score, interest rates will generally be higher than those offered to individuals with excellent credit (700+). However, they will be considerably lower than rates for subprime borrowers (below 580). Based on my experience, you might see rates in the range of 7% to 15%, depending on various factors.

It’s important to remember that these are general ranges. Your specific rate will be influenced by the current market, the lender’s risk assessment, your income, debt-to-income ratio, and the specific vehicle you choose. Don’t be surprised if offers vary significantly.

Factors Influencing Your Specific Rate

- Loan Term: Longer terms usually come with higher interest rates.

- Down Payment: A larger down payment can lead to a lower rate.

- Vehicle Age and Mileage: Newer cars often secure better rates due to their higher collateral value.

- Income Stability and Debt-to-Income Ratio: Lenders want to see that you have a stable income and can comfortably afford the monthly payments.

- Current Market Conditions: Interest rates fluctuate based on the broader economic environment.

Always focus on the Annual Percentage Rate (APR), which includes not only the interest rate but also any additional fees associated with the loan. This gives you the true cost of borrowing.

The Car Loan Application Process Step-by-Step

Navigating the application process for your 625 credit score car loan can be straightforward if you follow these steps. Being organized and informed will make the experience much smoother.

1. Get Pre-approved

As discussed, obtaining pre-approvals from multiple lenders is your first strategic move. This provides you with concrete loan offers, allowing you to shop for a car with confidence, knowing exactly what you can afford and what your financing terms will be. It gives you significant negotiating power.

2. Select Your Vehicle

Once you have your pre-approval in hand, you can confidently shop for a car that fits your budget and needs. Remember to consider not just the purchase price but also the total cost of ownership, including insurance, fuel, and maintenance.

3. Final Application and Negotiation

When you’ve chosen your vehicle, the final loan application will be completed. If you have a pre-approval, you can present it to the dealership. They may try to beat your pre-approved rate, but you now have a strong benchmark. Negotiate both the car’s price and the financing terms. Don’t be afraid to walk away if the deal isn’t right.

4. Review and Sign the Contract

Before signing anything, meticulously review the entire loan contract. Ensure that all terms, including the interest rate (APR), monthly payment, loan term, and any fees, match what you agreed upon. This is where common mistakes to avoid are rushing through the paperwork and not understanding every clause. If anything is unclear, ask for clarification.

Post-Approval: Managing Your Car Loan and Improving Your Credit

Securing a 625 credit score car loan is a significant achievement, but your journey doesn’t end there. Responsible management of your new loan can further boost your credit score and open doors to even better financial opportunities in the future.

Making Timely Payments

This is the single most important action you can take. Consistent, on-time payments are reported to credit bureaus and will positively impact your payment history, the largest factor in your credit score. Consider setting up automatic payments to avoid any accidental late fees.

Every on-time payment reinforces your creditworthiness, steadily improving your score over the loan’s duration. This responsible behavior is what transforms a "fair" credit score into a "good" or even "excellent" one.

Avoiding Late Fees and Penalties

Beyond credit score damage, late payments incur fees that add to the cost of your loan. Understand your payment due dates and grace periods. If you anticipate difficulty making a payment, contact your lender immediately. They may be able to offer solutions, such as deferment, to prevent a negative mark on your credit report.

Refinancing Opportunities

As you make consistent payments and your credit score improves, you may become eligible for refinancing your car loan at a lower interest rate. This can save you a significant amount of money over the remaining term of the loan. Many people with a 625 credit score car loan find refinancing to be a powerful tool for reducing their monthly payments or total interest paid.

Considering refinancing down the line? Our comprehensive guide on can help you understand when and how to pursue this option.

Common Pitfalls and How to Avoid Them

Even with a fair credit score, the car loan process can have its traps. Being aware of these common pitfalls will help you make smarter decisions.

- Not Budgeting Properly: Buying more car than you can truly afford is a recipe for financial stress. Always factor in all associated costs, not just the monthly payment.

- Accepting the First Offer: This is a major mistake. Always shop around for multiple loan offers to ensure you’re getting the most competitive rate. Pro tips from us: Negotiation is your friend.

- Falling for "Zero Down" Traps: While tempting, "zero down" offers often come with higher interest rates or result in you owing more than the car is worth (being "upside down" on your loan). A down payment is almost always beneficial, especially with a 625 credit score.

- Ignoring the Fine Print: Always read your loan contract thoroughly. Understand every fee, clause, and penalty. Don’t sign anything you don’t fully comprehend.

- Extended Loan Terms: While a 72 or 84-month loan may offer lower monthly payments, it dramatically increases the total interest you’ll pay and the risk of owing more than the car is worth as it depreciates. Aim for the shortest term you can comfortably afford.

Conclusion: Your Path to a Successful 625 Credit Score Car Loan

Securing a 625 credit score car loan is not only possible but entirely achievable with the right strategy and preparation. While your credit score places you in the fair credit category, it signals to lenders that you are a viable borrower, albeit one they might assess with a bit more scrutiny. By understanding your credit, budgeting wisely, making a solid down payment, and shopping around for the best terms, you can significantly improve your chances of approval and secure a favorable deal.

Remember, every on-time payment on your new car loan is an investment in your financial future, steadily building a stronger credit profile. Don’t let your current credit score deter you from finding reliable transportation. Take proactive steps, be an informed consumer, and drive away with confidence, knowing you’ve made a smart financial decision. Start your journey today!