Navigating the Road to a Car Loan with a 635 Credit Score: Your Ultimate Guide

Navigating the Road to a Car Loan with a 635 Credit Score: Your Ultimate Guide Carloan.Guidemechanic.com

Securing a car loan can feel like a daunting journey, especially when your credit score isn’t in the "excellent" range. If you’re looking to finance a vehicle and your credit score hovers around 635, you’re in a common position. Many people wonder if a 635 credit score is good enough to get approved for an auto loan, and more importantly, what kind of terms they can expect.

Based on my extensive experience in the financial and automotive sectors, I can tell you unequivocally: yes, getting a car loan with a 635 credit score is absolutely possible. However, it requires a strategic approach, a clear understanding of the lending landscape, and a commitment to preparing yourself for the best possible outcome. This comprehensive guide will equip you with all the knowledge and strategies you need to drive away in your new (or new-to-you) car.

Navigating the Road to a Car Loan with a 635 Credit Score: Your Ultimate Guide

Understanding Your 635 Credit Score in the Auto Loan World

Before we dive into the "how-to," let’s clarify what a 635 credit score signifies to a lender. Credit scores typically range from 300 to 850. A score of 635 falls within the "Fair" category, often considered "subprime" by many auto lenders.

This means you’re generally viewed as a moderate risk borrower. You’re not in the "poor" category, but you also don’t have the stellar payment history or low debt levels that would place you in the "good" or "excellent" tiers. Lenders will be willing to work with you, but they’ll likely mitigate their risk by offering different terms.

How Lenders Interpret a 635 Score

When a lender sees a 635 credit score, they interpret it as a signal. It tells them you might have had some financial hiccups in the past, such as late payments, a high credit utilization ratio, or perhaps a limited credit history. They understand that life happens, and a 635 score doesn’t automatically disqualify you.

However, it does mean they’ll scrutinize other aspects of your financial profile more closely. Your income stability, employment history, and existing debt obligations will play a crucial role in their decision-making process. They want to ensure you have the capacity to comfortably make your monthly car payments.

The Reality: Higher Interest Rates and Potential Hurdles

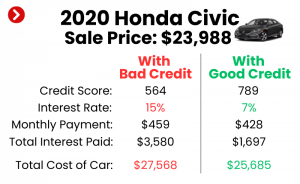

It’s important to set realistic expectations. While approval for a 635 credit score car loan is probable, it won’t be on the same terms as someone with an excellent score. The primary difference you’ll encounter is a higher interest rate.

Lenders use interest rates to compensate for the perceived risk. A 635 score suggests a higher risk of default compared to, say, a 750 score. Consequently, they’ll charge more for borrowing money. This translates to higher monthly payments and a greater total cost over the life of the loan.

Navigating Higher Interest Rates

Don’t let higher interest rates discourage you entirely. The goal is to secure the most favorable rate possible for your credit tier. By understanding why rates are higher, you can implement strategies to mitigate their impact. Our pro tip from years of observing the market is to focus on the total cost of the loan, not just the monthly payment, especially when comparing offers.

Sometimes, a slightly higher monthly payment for a shorter loan term can save you thousands in interest over time. It’s a balance between affordability now and total cost later.

Beyond the Score: Other Factors Influencing Your Approval

Your 635 credit score is a significant piece of the puzzle, but it’s not the only one. Lenders look at your overall financial picture to assess your ability to repay the loan. Understanding these additional factors can help you strengthen your application.

Income and Employment Stability

Lenders want to see a consistent and reliable source of income. A steady job for at least one to two years with a verifiable income stream makes you a much more attractive borrower. They want assurance that you can consistently meet your financial obligations.

If you’ve recently changed jobs, or have a less traditional income source, be prepared to provide extensive documentation. The more stable your income appears, the more confident lenders will be in your ability to repay.

Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another critical metric. This ratio compares your total monthly debt payments (including the prospective car loan) to your gross monthly income. A lower DTI indicates you have more disposable income to cover new debt.

Generally, lenders prefer a DTI ratio below 43%, though some subprime lenders might approve slightly higher. A high DTI suggests you’re already stretched thin financially, making a new car payment a riskier proposition. Proactively reducing other debts before applying can significantly improve this ratio.

Down Payment Amount

A substantial down payment is one of the most powerful tools you have when financing a car with a 635 credit score. It immediately reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid.

More importantly, a significant down payment signals to lenders that you’re serious about the purchase and have some skin in the game. It reduces their risk, as they have less capital at stake if you were to default. We often advise clients with fair credit to aim for at least 10-20% down.

Vehicle Choice

The type of vehicle you choose also plays a role. Lenders are often more comfortable financing newer, more reliable cars. Older vehicles or those with high mileage can be riskier because their value depreciates faster, and they may require costly repairs.

This doesn’t mean you can’t get a loan for an older car, but it might be harder or come with less favorable terms. Choosing a moderately priced, reliable vehicle that fits within your budget can significantly improve your chances of approval.

The Power of a Co-signer

Bringing a co-signer with excellent credit to the table can dramatically improve your approval odds and potentially secure a lower interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

This reduces the lender’s risk considerably. However, it’s a significant responsibility for the co-signer, as their credit will also be impacted if payments are missed. Only consider this option with someone you trust implicitly and who fully understands the commitment.

Strategies to Supercharge Your Car Loan Approval Chances

Now that you understand the landscape, let’s talk about actionable strategies. These pro tips are designed to maximize your approval odds and help you secure the best possible terms for your 635 credit score car loan.

1. Build a Strong Down Payment

As mentioned, this is paramount. Start saving as much as you can before you even step foot in a dealership or apply online. The more you put down, the less you borrow, and the more attractive you appear to lenders.

A larger down payment also reduces your loan-to-value (LTV) ratio, which is another metric lenders use. A lower LTV means you owe less than the car is worth, providing a cushion against depreciation. This is a common mistake people make – underestimating the power of a solid down payment.

2. Find a Reliable Co-signer

If saving a large down payment isn’t feasible, or you want to aim for even better terms, consider asking a trusted individual to co-sign. This could be a parent, spouse, or close family member with a strong credit history and stable income.

Ensure your co-signer understands the full implications. Their credit score will be on the line, and they will be legally responsible for the debt if you cannot pay. Open and honest communication is key here to avoid future financial strain or relationship issues.

3. Choose the Right Vehicle for Your Budget

Resist the temptation to overspend on a car. With a 635 credit score, aiming for a vehicle that is well within your means is crucial. Focus on reliability and affordability over luxury.

A more affordable car means a smaller loan amount, which translates to lower monthly payments. This helps keep your DTI ratio in check and makes the loan more manageable, increasing the likelihood of approval.

4. Gather All Your Documents in Advance

Being prepared can streamline the application process and show lenders you are serious and organized. Before you apply, have the following documents ready:

- Proof of Income: Pay stubs (last 2-3 months), W-2s, tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement.

- Identification: Driver’s license, passport.

- Bank Statements: To verify funds for a down payment.

- Trade-in Information: If applicable, title and registration.

Having these documents readily available can prevent delays and make a positive impression on potential lenders.

5. Shop Around for Lenders (Don’t Settle!)

This is perhaps the most critical advice we can offer. Do not simply walk into a dealership and accept their first financing offer. Different lenders have different criteria and risk appetites, especially for subprime loans.

Pro tip from us: Apply for pre-approval with several types of lenders within a short window (typically 14-45 days, depending on the credit scoring model). This allows multiple inquiries to be treated as a single hard inquiry on your credit report, minimizing the impact. Compare interest rates, loan terms, and fees from each offer.

Types of Lenders to Consider for Your 635 Credit Score Car Loan

Knowing where to look is half the battle. Here are the primary types of lenders you should explore:

Dealership Financing

Many dealerships offer in-house financing or work with a network of lenders. This can be convenient, as it’s a one-stop shop for buying and financing. They often have relationships with subprime lenders who specialize in working with fair credit scores.

However, dealership financing might not always offer the best rates, as they sometimes add a markup to the interest rate. Always come to the dealership with pre-approved offers from other sources to use as leverage in negotiations.

Traditional Banks

Your personal bank or other large national banks can be a good starting point, especially if you have an existing relationship with them. They might be more willing to work with you due to your established history.

While banks typically prefer higher credit scores, some have programs for borrowers with fair credit. It’s worth checking their rates and terms, as they can sometimes offer competitive options.

Credit Unions

Credit unions are often a fantastic option for borrowers with fair credit. As member-owned institutions, they are known for their personalized service and generally offer lower interest rates and more flexible terms compared to traditional banks.

They tend to be more forgiving of credit score imperfections if you have a strong overall financial profile and a history of membership. Joining a credit union is usually straightforward and often requires only a small deposit.

Online Lenders Specializing in Subprime Auto Loans

The digital landscape has brought forth many online lenders who specialize in working with individuals who have fair or even poor credit. These lenders often have streamlined application processes and can provide quick pre-approvals.

They understand the nuances of subprime lending and are often more flexible than traditional institutions. However, always research their reputation and read reviews before committing, as terms can vary widely.

Navigating the Application Process and What to Expect

Once you’ve done your research and gathered your documents, it’s time to apply. Understanding the process will help you feel more confident.

Pre-approval vs. Full Application

Start with pre-approval. This involves a soft credit pull (which doesn’t harm your score) and gives you an idea of the loan amount and interest rate you might qualify for. Pre-approval letters are powerful negotiation tools.

A full application will involve a hard credit pull and requires all your documentation. Only proceed with a full application once you’re serious about a specific vehicle and have compared multiple pre-approval offers.

Understanding the Terms: APR, Loan Term, Monthly Payments

- APR (Annual Percentage Rate): This is the true cost of borrowing, including interest and certain fees. Focus on comparing APRs across different loan offers.

- Loan Term: This is the length of time you have to repay the loan (e.g., 36, 48, 60, 72 months). A longer term means lower monthly payments but more interest paid over time.

- Monthly Payments: Ensure the monthly payment is comfortable and fits easily within your budget. Don’t stretch yourself too thin, even if approved for a larger amount.

Common Mistakes to Avoid

Based on my experience, common mistakes people make when getting a car loan with a 635 credit score include:

- Not shopping around: Accepting the first offer without comparing.

- Focusing only on monthly payment: Neglecting the total cost and APR.

- Underestimating the down payment’s power: Not saving enough upfront.

- Not checking their credit report: Being unaware of errors or actual score. ]

Pro Tips for Success: Beyond the Application

Getting approved is just the first step. Here are some seasoned tips to ensure a successful car buying and loan experience.

Negotiate Everything

Don’t just negotiate the car’s price. Negotiate the trade-in value (if applicable), the interest rate, and any additional fees. Everything is negotiable, especially if you have pre-approval offers from other lenders.

Be firm but polite. If you feel pressured or uncomfortable, don’t be afraid to walk away. There are always other dealerships and other cars. ]

Read the Fine Print

Before you sign any documents, read every line of the loan agreement. Understand the interest rate, the full loan term, any prepayment penalties, and all associated fees. Ask questions if anything is unclear.

It’s your financial commitment, so ensure you understand precisely what you’re agreeing to. A common mistake is rushing through the paperwork because of excitement.

Consider Refinancing Later

If you secure a car loan with a higher interest rate due to your 635 credit score, remember that it’s not necessarily forever. As you make on-time payments, your credit score will likely improve.

After 6-12 months of consistent, on-time payments, you might be in a much better position to refinance your car loan at a lower interest rate. This can save you a significant amount of money over the remaining life of the loan.

Improving Your Credit Score for Future Loans

Your 635 credit score is a stepping stone. While you can get a car loan now, proactively working to improve your score will unlock better financial opportunities in the future.

1. Pay All Bills on Time, Every Time

Payment history is the most significant factor in your credit score. Make sure all your credit card payments, utility bills, and any existing loan payments are made on or before their due dates. Consider setting up automatic payments to avoid missing deadlines.

2. Reduce Your Existing Debt

Focus on paying down high-interest credit card debt. A lower credit utilization ratio (the amount of credit you’re using compared to your available credit) can significantly boost your score. Aim to keep your credit utilization below 30%.

3. Check Your Credit Report for Errors

You’re entitled to a free credit report from each of the three major bureaus (Equifax, Experian, TransUnion) once a year. Review them carefully for any inaccuracies or fraudulent activity. Dispute any errors immediately, as they can negatively impact your score. You can obtain your free report from AnnualCreditReport.com. ]

4. Maintain a Good Credit Mix

Having a mix of credit types (e.g., credit cards, installment loans) can positively influence your score, showing lenders you can manage different forms of credit responsibly. However, only open new accounts if you genuinely need them and can manage the payments.

Conclusion: Drive Away with Confidence

Getting a car loan with a 635 credit score is a realistic and achievable goal. It requires diligence, preparation, and a strategic approach, but it is certainly within reach. By understanding how lenders view your score, preparing a strong application, shopping around for the best terms, and being ready to negotiate, you can secure the financing you need.

Remember, this car loan isn’t just about getting a vehicle; it’s also an opportunity to rebuild and strengthen your credit. Consistent, on-time payments will slowly but surely elevate your score, paving the way for even better financial opportunities in the future. So, take a deep breath, follow these steps, and get ready to drive away in your next car with confidence!