Navigating the Road to a Car Loan with a 650 Credit Score: Your Ultimate Guide

Navigating the Road to a Car Loan with a 650 Credit Score: Your Ultimate Guide Carloan.Guidemechanic.com

Securing a car loan is a significant financial step, and your credit score plays a pivotal role in the process. If you’re looking to finance a vehicle and find yourself with a 650 credit score, you might be wondering what your options are. The good news is that a 650 credit score for a car loan is absolutely manageable. It sits squarely in the "fair" or "average" credit range, meaning while it’s not considered prime, it’s far from the subprime category.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to successfully navigate the auto loan landscape with a 650 credit score. We’ll delve into what lenders look for, how to improve your chances of approval, and essential tips for securing the best possible terms. Our ultimate goal is to provide real value, making your journey to a new car as smooth and affordable as possible.

Navigating the Road to a Car Loan with a 650 Credit Score: Your Ultimate Guide

Understanding Your 650 Credit Score: What It Means for Auto Loans

Before diving into the specifics of car loans, let’s clarify what a 650 credit score represents. Credit scores typically range from 300 to 850, and a 650 score falls into the "fair" category according to most major credit bureaus. This means you’ve demonstrated some responsible credit behavior, but there might also be areas for improvement, or perhaps a shorter credit history.

Lenders view a 650 score with a degree of caution. You’re generally seen as a moderate risk, which will influence the interest rates and loan terms you’re offered. While borrowers with excellent credit (750+) typically qualify for the lowest rates, a 650 score doesn’t shut you out of the market; it simply means you’ll need to be more strategic. Understanding this perception is the first step towards a successful application.

Is Getting a Car Loan With a 650 Credit Score Possible? The Definitive Answer

Absolutely, getting a car loan with a 650 credit score is not only possible but quite common. Many lenders are willing to work with individuals in the fair credit range. The key difference compared to someone with a higher score will likely be in the interest rate and potentially the loan conditions. You might not qualify for the absolute best rates, but competitive offers are certainly within reach.

Success largely depends on how you present yourself as a borrower and the steps you take to strengthen your application. It requires preparation, diligent research, and a clear understanding of your financial situation. Don’t be discouraged by your score; instead, view it as a starting point from which to build a strong case for your loan approval.

Beyond the Score: Factors Lenders Consider

While your 650 credit score is important, it’s just one piece of the puzzle. Lenders look at a holistic view of your financial health to assess your ability to repay a loan. Understanding these additional factors can help you prepare a more compelling application.

Income and Employment Stability

Lenders want to see a steady and reliable income. This demonstrates your consistent ability to make monthly payments. They will typically ask for proof of income, such as pay stubs, W-2s, or tax returns. A stable employment history, ideally with the same employer for a year or more, also signals reliability.

Debt-to-Income (DTI) Ratio

Your DTI ratio is a crucial metric. It compares your total monthly debt payments to your gross monthly income. For example, if your total monthly debt (credit cards, student loans, mortgage, etc.) is $1,500 and your gross monthly income is $4,000, your DTI is 37.5%. Lenders generally prefer a DTI ratio below 43%, though lower is always better. A high DTI can signal that you’re already stretched thin financially, even with a decent income.

Down Payment Amount

The amount of money you put down upfront significantly impacts your loan. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your financial commitment to the purchase. We’ll explore this more in the strategies section, but know that a substantial down payment can be a game-changer for a 650 credit score for car loan approval.

Vehicle Type and Age

The car you choose also plays a role. Lenders often prefer newer, more reliable vehicles because they hold their value better. An older car might be seen as a higher risk because it could require more repairs, potentially impacting your ability to make loan payments. The value of the vehicle serves as collateral, so its marketability is important to the lender.

Loan Term

The length of your loan, or the term, affects your monthly payments and the total interest you pay. While a longer term can result in lower monthly payments, it also means you pay more in interest over time. Lenders will assess if the proposed loan term aligns with the vehicle’s expected lifespan and your ability to manage the payments without becoming "upside down" (owing more than the car is worth).

Strategies to Improve Your Chances of Approval and Get Better Terms

Even with a 650 credit score, you have significant power to influence your car loan outcome. Employing these strategies can lead to better interest rates, more favorable terms, and a smoother approval process.

1. Increase Your Down Payment

This is often the single most impactful factor you can control. A larger down payment reduces the amount you need to borrow, which directly lowers the lender’s risk. It also means smaller monthly payments and less interest paid over the life of the loan.

Based on my experience, a down payment of 10% to 20% or more can dramatically improve your chances of approval with a 650 credit score. It shows lenders you are serious about the purchase and have some financial reserves. Even a few extra hundred dollars can make a noticeable difference in the eyes of a lender.

2. Find a Co-signer

If you have a trusted friend or family member with an excellent credit score and a strong financial history, asking them to co-sign your loan can be incredibly beneficial. A co-signer essentially guarantees the loan, promising to make payments if you default. This significantly reduces the risk for the lender.

Pro tips from us: Choose a co-signer wisely. They must understand the responsibility, as their credit will also be affected if payments are missed. Ensure you can reliably make payments to protect their credit and your relationship.

3. Improve Your Credit Score (Even Slightly)

While a complete credit overhaul takes time, you can often make small improvements to your score in a relatively short period. Pay down any outstanding credit card balances to reduce your credit utilization ratio. Even paying off a small debt can provide a modest boost.

Common mistakes to avoid are applying for too much new credit right before a car loan application, as this can temporarily lower your score. Also, check your credit report for errors and dispute any inaccuracies promptly, as these can artificially depress your score.

4. Choose the Right Vehicle

Be realistic about what you can afford. Opting for a more affordable, reliable used car rather than a brand-new luxury model will make your application more appealing. A less expensive vehicle means a smaller loan amount, which translates to lower risk for the lender.

Consider vehicles that hold their value well. Lenders prefer these as collateral. Researching car reliability and resale value can also help you make a smart choice that aligns with your financial standing.

5. Get Pre-Approved for a Loan

Pre-approval is a powerful tool. It means a lender has reviewed your financial information and agreed to lend you a specific amount at a certain interest rate before you even step onto a dealership lot. This gives you a clear budget and significant negotiating power.

When you’re pre-approved, you’re essentially shopping as a cash buyer. You know your maximum loan amount and your interest rate, allowing you to focus on the car and haggle for the best price. This also prevents you from being swayed by potentially less favorable financing options offered by a dealership.

6. Shop Around for Lenders

Do not settle for the first offer you receive, especially with a 650 credit score. Different lenders have different criteria and risk appetites. Explore options from various sources:

- Banks: Traditional banks often offer competitive rates.

- Credit Unions: Known for member-friendly rates and terms.

- Online Lenders: Many specialize in fair credit loans and offer quick approvals.

- Dealership Financing: While convenient, compare their offers with your pre-approvals.

Based on my experience, shopping around can save you hundreds, if not thousands, over the life of the loan. The multiple credit inquiries within a short period (typically 14-45 days, depending on the scoring model) will usually be counted as a single inquiry, so it won’t significantly harm your score.

7. Prepare Your Documents

Having all your necessary documents ready beforehand streamlines the application process. This typically includes:

- Proof of identity (driver’s license, passport)

- Proof of income (pay stubs, W-2s, tax returns)

- Proof of residence (utility bill, lease agreement)

- Bank statements

- Social Security number

Being prepared shows responsibility and can expedite your loan approval, especially when dealing with a 650 credit score for car loan applications.

Understanding Interest Rates with a 650 Credit Score

With a 650 credit score, you should anticipate a higher interest rate compared to borrowers with excellent credit. This is simply due to the increased risk lenders perceive. However, "higher" doesn’t necessarily mean prohibitive.

The Annual Percentage Rate (APR) is the total cost of borrowing money, including the interest rate and any fees. For fair credit borrowers, APRs for new car loans can range from roughly 7% to 15%, while used car loans might see rates from 9% to 20% or even higher, depending on the lender and market conditions. These are general estimates, and your specific rate will depend on all the factors discussed, including your income, DTI, down payment, and the chosen loan term.

It’s crucial to compare APRs, not just monthly payments, when evaluating loan offers. A lower monthly payment achieved through a longer loan term might look appealing, but it often means paying significantly more in total interest. Always ask for the full APR to make an informed decision. For more detailed information on average car loan rates by credit score, a trusted resource like Experian often publishes up-to-date data.

The Application Process: A Step-by-Step Guide

Navigating the car loan application process with a 650 credit score can feel daunting, but breaking it down into manageable steps makes it much easier.

1. Check Your Credit Report and Score

Before anything else, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and check your score. Look for any errors and dispute them immediately. This gives you an accurate picture of what lenders will see.

2. Determine Your Budget

Realistically assess how much you can afford for a monthly car payment, including insurance, fuel, and maintenance. Don’t just focus on the loan; consider the total cost of ownership. This will help you choose an appropriate vehicle and loan amount.

3. Gather Your Documents

As mentioned, have all your financial documents ready. This includes proof of income, identification, and residence. Being organized will save you time and stress during the application phase.

4. Apply for Pre-Approval

Start by applying for pre-approval with several lenders (banks, credit unions, online lenders). This gives you a baseline for interest rates and a clear spending limit before you even visit a dealership. It’s a strategic move for anyone seeking a 650 credit score for car loan.

5. Shop for a Car

With your pre-approval in hand, you can now confidently shop for a car that fits your budget and needs. Remember the advice about choosing a reliable and affordable vehicle.

6. Finalize the Loan

Once you’ve chosen your car and negotiated a price, review all loan offers. Compare the APRs, loan terms, and total cost of the loan. If the dealership offers better terms than your pre-approval, great! If not, stick with your pre-approved offer. Read every line of the contract before signing.

Common Mistakes to Avoid When Getting a Car Loan with a 650 Credit Score

Even with a strong strategy, some common pitfalls can derail your efforts. Being aware of these can save you money and headaches.

1. Not Checking Your Credit Report

Failing to review your credit report for inaccuracies is a critical oversight. Errors can unfairly lower your score and lead to less favorable loan terms. Always be informed about your credit standing.

2. Only Applying at One Dealership

Relying solely on dealership financing without exploring outside options is a common mistake. Dealerships are businesses; their primary goal is to maximize profit, which may not always align with your best interests. Always compare their offer with external pre-approvals.

3. Taking the First Offer

Patience is a virtue, especially when dealing with financial products. The first loan offer you receive might not be the best. Shopping around, as discussed, is crucial for securing competitive rates and terms.

4. Buying More Car Than You Can Afford

It’s easy to get excited and overspend. However, committing to a car payment that strains your budget can lead to financial stress and even default, which would severely damage your credit. Stick to your predetermined budget.

5. Extending the Loan Term Excessively

While a longer loan term means lower monthly payments, it also means you pay significantly more in total interest. For example, extending a loan from 60 to 72 months might lower your payment by $50, but could cost you hundreds, even thousands, more over the life of the loan. It also increases the risk of being "upside down" on your loan.

6. Not Understanding the Fine Print

Common mistakes to avoid are signing without reading the entire contract. Pay close attention to the APR, any hidden fees, prepayment penalties, and gap insurance details. Ask questions until you fully understand every clause. Don’t be rushed.

Building Credit for Future Car Loans and Beyond

Securing a car loan with a 650 credit score is a significant achievement, but it’s also an opportunity to build an even stronger financial future. By managing your car loan responsibly, you can significantly improve your credit score over time, opening doors to even better rates for future loans and other financial products.

Pay On Time, Every Time

This is the golden rule of credit building. Your payment history accounts for the largest portion of your credit score. Set up automatic payments or reminders to ensure you never miss a due date on your car loan or any other credit account.

Keep Credit Utilization Low

For your credit cards, try to keep your balances well below your credit limits, ideally below 30%. This demonstrates responsible credit management.

Diversify Your Credit Responsibly

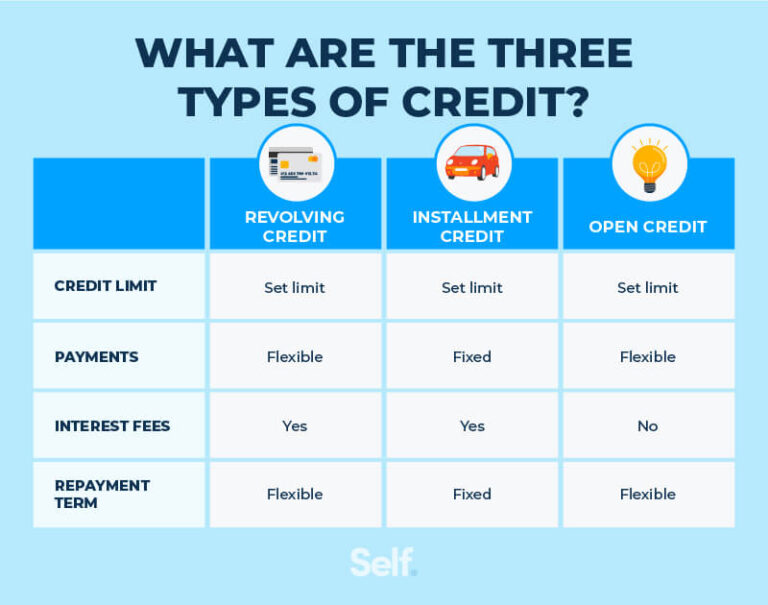

Having a mix of credit types (e.g., an installment loan like a car loan, and revolving credit like a credit card) can be beneficial, provided you manage them all responsibly. However, don’t open new accounts just for the sake of diversity if you don’t need them.

Monitor Your Credit Regularly

Continue to check your credit report annually for errors and to track your progress. Understanding your credit health is empowering. For more in-depth strategies on improving your credit score, you might find our article on "How to Boost Your Credit Score in 6 Months" helpful.

Conclusion: Your Road Ahead with a 650 Credit Score Car Loan

A 650 credit score for a car loan is a perfectly viable starting point. While it requires a thoughtful and strategic approach, the path to securing reliable transportation is well within your reach. By understanding what lenders look for, preparing your finances, and actively shopping for the best terms, you can navigate the process successfully.

Remember to prioritize a substantial down payment, explore co-signer options, and never settle for the first offer. Your diligence and preparation will not only lead to a successful car loan approval but also lay the groundwork for a stronger financial future. Drive confidently, knowing you’ve made an informed decision.