Navigating the Road to a Car Loan with a 666 Credit Score: Your Comprehensive Guide

Navigating the Road to a Car Loan with a 666 Credit Score: Your Comprehensive Guide Carloan.Guidemechanic.com

Getting a car is a significant life event, offering freedom, convenience, and independence. For many, securing a car loan is a crucial step in this journey. If you’ve checked your credit score and found yourself at a 666, you might be wondering what your options are. Is it a good score? Is it bad? Can you even get approved for a decent car loan?

The good news is: Yes, you absolutely can get a car loan with a 666 credit score. This score, while not in the "excellent" tier, certainly isn’t a barrier to financing. However, approaching the process strategically is key to securing the best terms. This comprehensive guide will walk you through everything you need to know, from understanding your credit score to negotiating like a pro, ensuring you drive away with a great deal.

Navigating the Road to a Car Loan with a 666 Credit Score: Your Comprehensive Guide

Understanding Your 666 Credit Score in the Auto Lending Landscape

Let’s demystify what a 666 credit score truly means. Credit scores, like those from FICO or VantageScore, range from 300 to 850. A score of 666 typically falls into the "Fair" to "Good" category, depending on the specific scoring model and lender’s criteria.

For many lenders, a score in the mid-600s is considered subprime but often still very lendable. It indicates that while you might have some areas for improvement in your credit history, you’re generally a responsible borrower. This isn’t a "bad credit" score that would severely limit your options, but it also isn’t a "prime" score that automatically unlocks the lowest interest rates.

Where Does 666 Sit on the Credit Spectrum?

To put it into perspective:

- Excellent: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

As you can see, your 666 credit score is right at the top end of the "Fair" category, often just a few points shy of "Good." This means lenders will likely view you as a moderate risk, but still a viable candidate for an auto loan.

The Reality of Getting a Car Loan with a 666 Credit Score

Securing an auto loan with a 666 credit score is a common scenario. Millions of Americans have credit scores in this range. The primary difference you’ll encounter compared to someone with an excellent score is the interest rate.

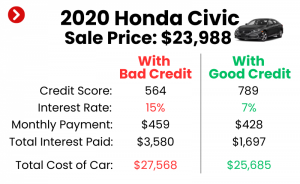

Lenders use credit scores to assess risk. A higher score means lower risk, which translates to lower interest rates. Conversely, a lower score implies higher risk, leading to higher interest rates to compensate the lender. With a 666 score, you’ll likely qualify for rates that are higher than the absolute best available, but significantly better than those offered to individuals with truly poor credit.

What to Expect: Approval and Interest Rates

Based on my experience, most lenders will be willing to approve a car loan with a 666 credit score. The challenge isn’t usually approval itself, but rather securing favorable terms. You should prepare for interest rates that might be a few percentage points higher than what someone with a 750+ score would receive.

For example, while a borrower with excellent credit might qualify for a 3-5% APR, someone with a 666 score might see rates in the 7-12% range, depending on market conditions, the loan term, and the specific lender. Don’t be discouraged by this; by employing smart strategies, you can still significantly improve your chances of getting a competitive offer.

Strategies for Securing the Best Car Loan with a 666 Credit Score

Getting a car loan when your credit score is 666 requires a proactive and informed approach. Here are the most effective strategies to help you get approved with the most favorable terms possible.

1. Know Your Numbers Inside and Out

Before you even step foot in a dealership or apply anywhere, thoroughly understand your credit situation. This empowers you during negotiations and helps you identify potential roadblocks.

Get Your Credit Report

Request a free copy of your credit report from all three major bureaus (Experian, Equifax, and TransUnion) at AnnualCreditReport.com. This is a critical first step. Review each report meticulously for any inaccuracies.

Based on my experience, errors on credit reports are more common than people think. Disputing and correcting these errors can potentially boost your score quickly. Even a small bump could move you into a better rate tier.

Understand Factors Affecting Your Score

A 666 score means there are likely areas that need attention. Common factors that impact your score include payment history, amounts owed, length of credit history, new credit, and credit mix. Identify what might be pulling your score down.

Knowing these details allows you to explain any past issues to a lender confidently, if necessary. It also gives you a roadmap for future credit improvement.

2. Save for a Substantial Down Payment

This is arguably one of the most impactful strategies for anyone, especially those with a 666 credit score. A larger down payment significantly reduces the risk for the lender.

When you put more money down, the loan amount decreases, meaning less money for the lender to lose if you default. It also shows the lender your commitment and financial stability. Pro tips from us: aim for at least 10-20% of the car’s purchase price as a down payment.

A larger down payment can often lead to a lower interest rate, a smaller monthly payment, or a shorter loan term. All of these outcomes benefit your financial health and make the loan more manageable.

3. Consider a Co-signer (If Necessary)

Bringing on a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. A co-signer essentially pledges their good credit, taking on equal responsibility for the loan.

However, this decision shouldn’t be taken lightly. Common mistakes to avoid are not fully understanding the co-signer’s liability. If you miss payments, it impacts both your credit and theirs. Ensure both parties are fully aware of the risks and responsibilities involved.

A co-signer can be a valuable asset, but only if you are confident in your ability to make all payments on time. It’s a relationship-based decision that requires trust and clear communication.

4. Shop Around Aggressively for Pre-approval

Do not simply walk into a dealership and accept their first financing offer. This is a common mistake. Instead, get pre-approved for a loan from multiple lenders before you start car shopping.

Seek pre-approvals from:

- Banks: Your current bank might offer competitive rates due to your existing relationship.

- Credit Unions: Often known for offering lower interest rates and more flexible terms to their members.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others specialize in online auto loans and can offer very competitive rates and convenience.

- Dealership Financing: While you should compare, some dealerships have strong relationships with various lenders and can find good deals.

Getting pre-approved gives you a solid offer in hand, acting as a benchmark. It tells the dealership that you’re a serious buyer with financing already secured, giving you leverage in negotiations. You can explore more about comparing loan offers from various sources here (external link to CFPB).

5. Choose the Right Vehicle for Your Budget

It’s easy to get carried away by the allure of a brand-new, fully loaded vehicle. However, with a 666 credit score, practicality should guide your choice. Opting for a more affordable car, perhaps a reliable used vehicle, can significantly impact your loan terms.

A less expensive car means a smaller loan amount, which reduces your monthly payments and the total interest paid over the life of the loan. This also makes you a less risky borrower in the eyes of lenders. Focus on what you need and what you can comfortably afford, rather than what you want.

6. Negotiate Beyond Just the Monthly Payment

Many buyers make the mistake of focusing solely on the monthly payment. While important, it’s not the only factor. Dealerships can stretch out loan terms (e.g., 72 or 84 months) to lower the monthly payment, but this often means you pay significantly more in total interest.

Pro tips from us: negotiate the total price of the car first, then the interest rate (APR), and finally the loan term. Understand the Annual Percentage Rate (APR), which includes all fees and charges, giving you the true cost of borrowing. A shorter loan term, even with a slightly higher monthly payment, can save you thousands in interest over time.

7. Improve Your Credit Score Before Applying (If Time Allows)

If you’re not in a rush to buy a car, taking a few months to boost your 666 credit score can yield substantial savings. Even a 20-30 point increase could move you into a "Good" credit tier, potentially unlocking lower interest rates.

Simple steps can make a big difference:

- Pay Down High-Interest Debt: Reducing your credit card balances can lower your credit utilization ratio, a major factor in your score.

- Make All Payments On Time: Payment history is the most critical factor. Set up autopay to ensure you never miss a due date.

- Avoid New Credit Applications: Each new application results in a hard inquiry, which can temporarily ding your score.

- Become an Authorized User: If a trusted individual with excellent credit adds you as an authorized user on one of their long-standing, well-managed credit accounts, it can positively impact your credit history.

For a more in-depth guide on enhancing your financial standing, check out our article on Boosting Your Credit Score for Better Loan Opportunities (internal link placeholder).

Types of Lenders for a 666 Credit Score

Not all lenders are created equal, especially when you have a credit score that’s not pristine. Knowing where to look can save you time and money.

- Traditional Banks: Large national and regional banks offer auto loans. If you have an existing relationship, they might be more willing to work with you.

- Credit Unions: These member-owned financial institutions often provide more flexible terms and lower interest rates compared to traditional banks, especially for members. It’s worth exploring if you qualify for membership.

- Online Lenders: Many online platforms specialize in auto financing for various credit tiers. They offer convenience, quick approvals, and competitive rates due to lower overheads. Examples include Capital One Auto Finance, Carvana, and many others.

- Dealership Financing: Dealerships work with a network of lenders. While convenient, always compare their offers with your pre-approvals to ensure you’re getting a fair deal.

- "Buy Here, Pay Here" Dealerships: These are typically a last resort. They directly finance the loan but often charge extremely high interest rates and may not report to all credit bureaus, limiting your ability to build credit. Avoid them if at all possible.

What to Bring to the Dealership or Lender

Being prepared makes the application process smoother and faster. Gather these documents before you go:

- Proof of Income: Recent pay stubs (1-2 months), W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Government-Issued ID: Driver’s license or state ID.

- Trade-in Details (if applicable): Title, registration, and loan payoff information for your current vehicle.

- Down Payment: The amount you plan to put down, whether in cash, cashier’s check, or proof of funds transfer.

- Proof of Insurance: You’ll need to show proof of insurance before driving off the lot.

Having everything organized demonstrates your readiness and can help expedite the process.

Common Mistakes to Avoid When Applying for a Car Loan with a 666 Credit Score

Even with a solid plan, it’s easy to fall into common traps. Avoid these pitfalls to protect your credit and your wallet.

- Applying Everywhere at Once: Each loan application results in a "hard inquiry" on your credit report, which can slightly lower your score. While multiple auto loan inquiries within a short period (typically 14-45 days, depending on the scoring model) are often grouped as a single inquiry, spreading them out too much can be detrimental. Focus your applications to a few strong contenders within a focused window.

- Not Getting Pre-approved: As mentioned, pre-approval is your power move. Without it, you’re negotiating blindly and at a disadvantage.

- Focusing Only on Monthly Payments: This is a classic dealer tactic. They might offer a low monthly payment by extending the loan term to 7 or 8 years, meaning you pay significantly more in interest over time. Always consider the total cost of the loan.

- Ignoring the Total Cost of Ownership: Beyond the loan, remember to factor in insurance, maintenance, fuel, and potential repairs. A car is an ongoing expense.

- Not Reading the Fine Print: Always read your loan agreement thoroughly before signing. Understand all terms, fees, and conditions. Don’t be afraid to ask questions.

- Buying More Car Than You Can Afford: This is the most common mistake. Stick to your budget. An expensive car with a high interest rate can quickly become a financial burden.

Beyond the Loan: Building a Better Financial Future

Securing a car loan with a 666 credit score is a significant achievement, but it’s also an opportunity to further improve your financial standing. Your new auto loan, if managed responsibly, can become a powerful tool for credit building.

Make every payment on time, every month. This consistent positive payment history will gradually boost your credit score over the loan’s term. As your score improves, you might even consider refinancing your auto loan down the line. If interest rates drop or your credit score improves significantly, refinancing could secure you a lower interest rate, saving you money and potentially reducing your monthly payments. Learn more about this option in our guide: Is Refinancing Your Auto Loan Right For You? (internal link placeholder).

Conclusion: Your 666 Credit Score is a Stepping Stone, Not a Stumbling Block

A 666 credit score puts you in a solid position to get a car loan, but it demands a strategic and informed approach. By understanding your credit, making a significant down payment, shopping around for the best rates, and choosing a vehicle that fits your budget, you can navigate the auto loan process successfully.

Remember, this isn’t just about getting a car; it’s about making a smart financial decision that serves your needs now and helps build a stronger credit future. With the right preparation and knowledge, you can confidently drive away in your new vehicle, knowing you secured the best possible deal for your 666 credit score. Happy driving!