Navigating the Road to a Car Loan with a 686 Credit Score: Your Ultimate Guide

Navigating the Road to a Car Loan with a 686 Credit Score: Your Ultimate Guide Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect, but the path can often feel complicated, especially when your credit score comes into play. If you’re looking for a car loan and your credit score hovers around 686, you’re in a unique position. This score falls squarely into what many lenders consider the "Good" or "Fair" category, meaning you’re not in the top tier, but you’re certainly not at the bottom either.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to secure a favorable 686 credit score car loan. We’ll delve deep into what this score means for your financing options, how to prepare for the application process, and crucial tips to ensure you drive away with the best possible deal. Our goal is to make this complex topic easy to understand, providing real value that helps you navigate the auto loan landscape with confidence.

Navigating the Road to a Car Loan with a 686 Credit Score: Your Ultimate Guide

Understanding Your 686 Credit Score: What It Means for a Car Loan

When a lender evaluates your creditworthiness, your credit score acts as a quick snapshot of your financial reliability. A 686 credit score indicates that you have a decent history of managing debt, but perhaps with a few minor blemishes or a shorter credit history compared to those with excellent scores. This positions you as a moderate risk borrower, making you an attractive candidate for many lenders, though you might not qualify for the absolute lowest interest rates.

Specifically, most credit scoring models, like FICO and VantageScore, categorize a 686 score as "Good" or "Fair." While "Good" usually starts around 670, you’re on the higher end of the "Fair" or lower end of the "Good" spectrum. This means you generally have a good chance of approval for a car loan with a 686 credit score, but the terms and interest rates will be more competitive than someone with a score in the 750s or 800s.

Your Approval Chances with a 686 Credit Score

The good news is that a 686 credit score puts you in a strong position for auto loan approval. Many lenders are willing to extend credit to individuals with scores in this range, recognizing that you’ve demonstrated a history of making payments on time, even if you don’t have a perfect record. Your chances of securing an auto loan with a 686 credit score are significantly higher than for someone with a subprime score.

However, approval is not just about your credit score alone. Lenders will also consider other factors, such as your income, employment history, debt-to-income ratio, and the amount of the loan you’re seeking. A robust income and stable job history can significantly bolster your application, even with a moderate credit score.

Expected Interest Rates with a 686 Credit Score

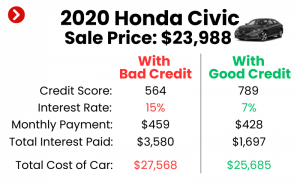

One of the most significant impacts of your 686 credit score will be on the interest rate you’re offered. While you won’t qualify for the rock-bottom rates reserved for borrowers with excellent credit (typically 750+), you also won’t be subjected to the exorbitant rates often seen with subprime loans. Based on my experience, borrowers with a 686 credit score can generally expect interest rates that are competitive, but still a few percentage points higher than the best rates available.

For example, if someone with an 800 credit score might get an APR of 3-5%, you might see offers in the 6-10% range, depending on market conditions, the loan term, and the lender. Every percentage point matters over the life of a loan, so understanding these expectations is crucial for budgeting and negotiation. It’s vital to shop around to find the most favorable terms for your 686 credit score car loan.

The Power of Preparation: Before You Even Look at Cars

Securing a great car loan with a 686 credit score isn’t just about showing up at the dealership. It’s about strategic preparation. Taking these proactive steps before you start car shopping can save you thousands of dollars and a lot of stress.

1. Know Your Score (and Report) Inside Out

Before you apply for any loan, the first and most critical step is to obtain your credit score and, more importantly, your full credit report. You are entitled to a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) annually via AnnualCreditReport.com. Reviewing this report allows you to understand the details behind your 686 score.

Common mistakes to avoid include assuming your score is accurate without checking. Look for any inaccuracies, such as accounts you don’t recognize, incorrect payment statuses, or outdated information. Disputing errors can potentially boost your score, even if only by a few points, which can make a difference in your loan terms.

2. Budgeting is Your Best Friend

Understanding what you can truly afford is paramount. This isn’t just about the monthly car payment; it includes insurance, fuel, maintenance, and registration fees. Create a detailed budget that accounts for all your monthly income and expenses. This will give you a clear picture of how much wiggle room you have for a car payment without overstretching your finances.

Lenders will look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI ratio makes you a less risky borrower. Aim for a DTI of 36% or less, though some lenders may approve higher, especially for auto loans.

3. The Down Payment Strategy: Your Secret Weapon

One of the most effective ways to improve your chances of getting a great 686 credit score car loan is by making a substantial down payment. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. It also signals to lenders that you are committed and have skin in the game.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price. For used cars, a higher percentage might be even more beneficial. A significant down payment can offset a slightly lower credit score, potentially qualifying you for better interest rates than you might otherwise receive.

4. Don’t Forget Ancillary Costs

Beyond the purchase price and loan interest, there are numerous other costs associated with car ownership. These include auto insurance, which can be surprisingly expensive, especially for newer vehicles or drivers with certain risk factors. Factor in registration fees, potential sales tax, and an emergency fund for unexpected maintenance.

Based on my experience, many first-time car buyers or those on a tight budget overlook these crucial expenses, leading to financial strain later on. Having a clear picture of the total cost of ownership will prevent unwelcome surprises and ensure your 686 credit score car loan is manageable in the long run.

Navigating the Lender Landscape with a 686 Credit Score

When seeking a 686 credit score car loan, it’s crucial to understand that not all lenders are created equal. Each type of lender offers different advantages and disadvantages. Shopping around extensively is not just recommended; it’s essential for securing the best possible terms.

Traditional Banks

Your local bank or a national banking institution can be a good starting point. If you have an existing relationship with a bank, they might be more inclined to offer you favorable terms, even with a 686 credit score. They often have competitive rates and a straightforward application process. However, their approval criteria can sometimes be stricter than other lenders.

Credit Unions

Credit unions are member-owned financial institutions known for often offering lower interest rates and more flexible terms than traditional banks. If you’re eligible to join one (often based on residency, employer, or association), they can be an excellent option for a car loan with a 686 credit score. Their focus on member service often translates to a more personalized approach to lending.

Online Lenders

The rise of online lenders has revolutionized the auto loan market. Companies like LightStream, Capital One Auto Finance, and others offer quick pre-approvals and competitive rates, often allowing you to compare multiple offers from the comfort of your home. This convenience and speed can be invaluable, especially if you’re trying to secure financing quickly.

Pro tips from us: Online lenders are excellent for comparing rates quickly. Submit a few pre-approval applications to get a sense of what rates you qualify for without impacting your credit score significantly (multiple inquiries within a short period for the same type of loan are usually counted as one for scoring purposes).

Dealership Financing

Most dealerships offer in-house financing or work with a network of lenders. While convenient, this option often comes with a markup on the interest rate, as the dealership acts as an intermediary. It’s best to secure pre-approval from an independent lender before you visit the dealership. This way, you have a benchmark for comparison and can negotiate from a position of strength.

Common mistakes to avoid are going to the dealership without pre-approval. This puts you at a significant disadvantage, as you won’t know if the rates they offer are truly competitive or if you could get a better deal elsewhere.

Optimizing Your Car Loan Application for a 686 Score

Once you’ve identified potential lenders and prepared your finances, it’s time to fine-tune your application strategy. Even with a 686 credit score, there are specific steps you can take to present yourself as the most attractive borrower possible.

Gathering Necessary Documents

Lenders require specific documentation to verify your identity, income, and financial stability. Having these ready will streamline the application process. Typically, you’ll need:

- Proof of identity (driver’s license, passport)

- Proof of residency (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of employment (employer contact information)

- Information about the vehicle you intend to purchase (if known)

Considering a Co-signer

If you’re looking to secure a better interest rate or increase your chances of approval for a 686 credit score car loan, a co-signer can be a valuable asset. A co-signer, typically someone with excellent credit and a stable financial history, agrees to take on the responsibility of the loan if you fail to make payments. This significantly reduces the risk for the lender.

Based on my experience, a co-signer can often be the difference between a high-interest loan and a much more affordable one. However, remember that co-signing is a serious commitment for both parties. If you default, it negatively impacts both your credit scores.

Choosing the Right Vehicle

The type of vehicle you choose also plays a role in your loan terms. Lenders often view newer, more reliable cars as less risky because they hold their value better and are less prone to immediate repair costs. Used cars can be a great value, but older, high-mileage vehicles might come with higher interest rates due to perceived higher risk of depreciation and potential mechanical issues.

Pro tips from us: Consider a slightly used car (1-3 years old). These vehicles have already taken the initial depreciation hit, offering better value, and often qualify for similar loan terms as new cars from many lenders.

The Art of Negotiation

Negotiation isn’t just for the price of the car; it also extends to the loan terms. With pre-approval in hand, you can confidently negotiate with the dealership’s finance department. Don’t be afraid to ask for a lower interest rate or a more favorable loan term. Remember, the dealer wants to sell you a car, and they have some flexibility.

Focus on the total cost of the loan, not just the monthly payment. A longer loan term might mean lower monthly payments but significantly higher total interest paid over time. Aim for a loan term that balances affordability with minimizing total interest.

Understanding Interest Rates with a 686 Credit Score

The interest rate is arguably the most critical factor in your 686 credit score car loan, as it directly impacts the total amount you’ll pay. Let’s break down what influences these rates and what you can expect.

What Influences Interest Rates?

Several factors beyond your credit score determine the interest rate you receive:

- Credit Score: As discussed, a 686 score is good, but not excellent, so rates will reflect that.

- Loan Term: Shorter loan terms (e.g., 36 or 48 months) generally have lower interest rates than longer terms (e.g., 60 or 72 months) because the lender assumes less risk over a shorter period.

- Lender: Different lenders have different risk appetites and pricing models.

- Vehicle Age and Type: Newer vehicles often secure lower rates due to their higher resale value and lower perceived risk.

- Market Conditions: Overall economic factors and the prime lending rate can influence auto loan rates across the board.

- Down Payment: A larger down payment reduces the loan amount and the lender’s risk, often leading to a lower rate.

Expected Range for a 686 Score

While exact rates fluctuate, borrowers with a 686 credit score can typically expect interest rates that fall into a "middle" range. For new cars, you might see rates anywhere from 6% to 10% APR. For used cars, these rates can be slightly higher, perhaps 7% to 12% APR, reflecting the increased risk associated with older vehicles.

Pro tips from us: Always compare the APR (Annual Percentage Rate), not just the stated interest rate. The APR includes all fees and charges associated with the loan, giving you the true cost of borrowing.

Impact of Even a Small Difference in APR

A seemingly small difference in APR can have a significant impact on the total cost of your loan. For example, on a $25,000 loan over 60 months:

- At 6% APR, your total interest paid would be approximately $3,950.

- At 8% APR, your total interest paid would be approximately $5,400.

- At 10% APR, your total interest paid would be approximately $6,880.

That’s a difference of over $2,900 between a 6% and 10% rate! This clearly illustrates why shopping for the best interest rates with a 686 credit score is so critical.

Beyond the Loan: Improving Your Credit Score for Future Savings

Securing your 686 credit score car loan is a great achievement, but the journey doesn’t end there. Continuously working to improve your credit score will unlock even better financial opportunities in the future.

Why Continuous Improvement Matters

Based on my experience, maintaining and improving your credit score is one of the most powerful financial habits you can adopt. A higher credit score doesn’t just mean lower interest rates on future car loans; it can also lead to better rates on mortgages, personal loans, credit cards, and even lower insurance premiums. It’s an investment in your financial future.

Strategies for Credit Score Improvement

Even if you’ve already secured your loan, you can still improve your 686 credit score:

- Pay Bills on Time, Every Time: Payment history is the most significant factor in your credit score. Make all your loan payments (including your new car loan!), credit card bills, and other debts on time.

- Reduce Existing Debt: Focus on paying down credit card balances. High credit utilization (the amount of credit you’re using compared to your available credit) can negatively impact your score.

- Avoid New Credit Inquiries: While shopping for an auto loan is an exception, try to avoid opening new credit accounts unnecessarily, as each inquiry can temporarily lower your score.

- Keep Old Accounts Open: The length of your credit history is another important factor. Don’t close old, paid-off credit card accounts, as this can shorten your average credit age.

- Monitor Your Credit Report: Regularly check your credit report for errors and identity theft. You can get free access to your credit reports annually at AnnualCreditReport.com.

Pro Tips for a Successful 686 Credit Score Car Loan Journey

To ensure you have the smoothest and most advantageous experience, here are some final expert recommendations:

- Shop Around Aggressively for Rates: This cannot be emphasized enough. Get pre-approved by at least 3-4 different lenders (banks, credit unions, online lenders) before stepping foot in a dealership. This gives you leverage.

- Don’t Just Focus on the Monthly Payment: While important, fixating solely on the monthly payment can lead you to accept longer loan terms with higher total interest. Always consider the total cost of the loan over its lifetime.

- Read the Fine Print: Before signing any loan agreement, meticulously read every detail. Understand all fees, the interest rate, the full loan term, and any penalties for early repayment or late payments. If something is unclear, ask for clarification.

- Understand Total Cost of Ownership: Beyond the loan, factor in insurance, maintenance, fuel, and depreciation. A slightly more expensive car with better fuel efficiency or lower insurance costs might be cheaper in the long run.

- Be Patient: Don’t rush into a decision. The car buying process can be lengthy, but patience will help you make informed choices and avoid costly mistakes.

Conclusion: Your Road to a Great Car Loan Starts Now

Securing a 686 credit score car loan is not just possible; it’s within your reach with the right approach. By understanding your credit score’s implications, preparing thoroughly, exploring all your lending options, and optimizing your application, you can drive away with a car loan that fits your budget and helps you build a stronger financial future. Remember, your credit score is a dynamic tool, and every on-time payment you make will contribute to its improvement.

Don’t let uncertainty hold you back. Start your preparation today, equip yourself with knowledge, and take control of your car buying experience. Your journey to owning the perfect vehicle on favorable terms begins with these informed steps.

Further Reading:

- Want to boost your credit score even higher? Check out our detailed guide on How to Improve Your Credit Score Fast: Actionable Strategies.

- Master the art of pre-approval with our Ultimate Guide to Car Loan Pre-Approval: Drive with Confidence.