Navigating the Road to a Car Loan with Bad Credit in Rockford, IL: Your Ultimate Guide

Navigating the Road to a Car Loan with Bad Credit in Rockford, IL: Your Ultimate Guide Carloan.Guidemechanic.com

Securing a car loan can feel like an uphill battle when your credit score isn’t pristine. For residents in Rockford, IL, the dream of reliable transportation often hits a roadblock when faced with the realities of a less-than-perfect credit history. However, having bad credit doesn’t mean your journey ends here.

This comprehensive guide is designed to empower you with the knowledge, strategies, and confidence needed to successfully obtain bad credit car loans in Rockford, IL. We understand the unique challenges you face and are here to show you that with the right approach, getting approved for a vehicle loan is not just possible, but an achievable step towards improving your financial standing. Let’s navigate this path together, transforming what might seem like an obstacle into an opportunity.

Navigating the Road to a Car Loan with Bad Credit in Rockford, IL: Your Ultimate Guide

Understanding Bad Credit and Its Impact on Car Loans

Before diving into the specifics of bad credit car loans in Rockford, IL, it’s crucial to understand what "bad credit" actually entails and why it affects lending decisions. Your credit score is a three-digit number that acts as a financial report card, indicating your creditworthiness to lenders. Scores typically range from 300 to 850.

Generally, a FICO score below 600-620 is considered "subprime" or "bad credit." This range signifies a higher risk for lenders because it suggests a history of late payments, defaults, bankruptcies, or high credit utilization. Lenders use this score to assess the likelihood of you repaying a loan.

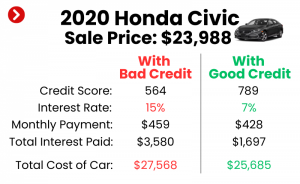

When you have bad credit, lenders perceive you as a higher risk. This often translates into less favorable loan terms, primarily higher interest rates. A higher interest rate means you’ll pay more over the life of the loan, increasing your total cost of ownership. It also limits your options, as some traditional lenders might simply decline your application.

Based on my experience, many people are surprised by their actual credit score, often underestimating or overestimating where they stand. It’s a critical first step to know your numbers accurately. Understanding this landscape is the foundation for successfully securing a car loan, even with a challenging credit history.

Is Getting a Car Loan with Bad Credit in Rockford, IL Possible? Absolutely!

The short answer is a resounding "Yes!" Getting bad credit car loans in Rockford, IL is not only possible but a common scenario for many individuals. The automotive financing market is diverse, and it includes a significant segment dedicated to helping those with less-than-perfect credit. This is often referred to as the "subprime lending" market.

Subprime lenders and specialized finance departments at dealerships understand that life happens. They recognize that a past financial stumble doesn’t define your current ability or willingness to repay a loan. These lenders are willing to take on more risk, albeit typically with different terms, to help you get into a reliable vehicle.

The key is knowing where to look and how to present yourself as a responsible borrower, despite your credit score. Many dealerships in and around Rockford, IL, have established relationships with multiple lenders, including those who specialize in bad credit financing. This means they can often find a solution tailored to your specific situation.

Pro tips from us: Don’t let a low score deter you entirely from exploring your options. The Rockford market has resources and professionals dedicated to assisting individuals with bad credit. Your journey to car ownership doesn’t have to end because of your credit history.

Preparing for Your Bad Credit Car Loan Application: Laying the Groundwork

Preparation is paramount when seeking bad credit car loans in Rockford, IL. Going into the process uninformed can lead to frustration and potentially less favorable outcomes. A little groundwork can significantly improve your chances of approval and help you secure better terms.

1. Check Your Credit Report and Score

Your credit report is more than just a number; it’s a detailed history of your borrowing and repayment activities. Before applying for any loan, obtain a copy of your credit report from all three major credit bureaus (Equifax, Experian, and TransUnion). You can do this for free annually at AnnualCreditReport.com.

Carefully review each report for inaccuracies. Errors, such as incorrect late payments or accounts that aren’t yours, can negatively impact your score. If you find any discrepancies, dispute them immediately. Correcting errors can sometimes boost your score, even if only slightly, which can make a difference in your loan approval and interest rate.

Based on my experience, a significant percentage of credit reports contain errors. Taking the time to check and correct these can save you money and headaches in the long run.

2. Understand Your Budget and Affordability

It’s tempting to focus solely on the car you want, but a critical step is determining what you can truly afford. This goes beyond just the monthly loan payment. Factor in:

- Insurance costs: Bad credit can sometimes lead to higher insurance premiums.

- Fuel expenses: Consider your commute and the car’s fuel efficiency.

- Maintenance and repairs: Older or high-mileage cars might require more upkeep.

- Registration and taxes: These are upfront or annual costs.

Use a budget planner to calculate your monthly income versus your expenses. A car payment should comfortably fit into your budget without straining your finances. Lenders will also look at your debt-to-income (DTI) ratio, which is the percentage of your gross monthly income that goes towards debt payments. A lower DTI is generally more favorable.

3. Save for a Down Payment

A down payment is one of the most powerful tools you have when applying for a bad credit car loan in Rockford, IL. Even a modest down payment can significantly improve your chances of approval and lead to better loan terms.

Here’s why a down payment helps:

- Reduces Lender Risk: It shows the lender you have "skin in the game" and are committed to the purchase. It also reduces the amount they need to finance.

- Lowers Loan Amount: A smaller principal means lower monthly payments and less interest paid over the life of the loan.

- Demonstrates Responsibility: Saving money indicates financial discipline, which can counteract some negative aspects of your credit history.

Aim for at least 10-20% of the vehicle’s price if possible. Even 5% is better than nothing. Common mistakes to avoid are applying without any down payment, as this often signals higher risk to lenders and can result in higher interest rates.

4. Gather Necessary Documents

Being prepared with all required documentation streamlines the application process and shows you’re serious. While requirements vary by lender, you’ll generally need:

- Proof of Identity: Valid driver’s license, state ID.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Proof of Income: Recent pay stubs (last 2-3 months), tax returns (if self-employed), bank statements.

- Proof of Employment: Employer contact information, sometimes recent W-2s.

- References: Sometimes required, typically 2-3 personal references.

- Trade-in Title (if applicable): If you’re trading in your current vehicle.

Having these documents organized and ready will make the application process much smoother. For more insights into how your credit score impacts your daily finances, you might find our article on (Internal Link Placeholder 1) particularly helpful.

Finding the Right Lender for Bad Credit Car Loans in Rockford, IL

Once you’ve prepared yourself and your finances, the next crucial step is finding the right lender. The landscape for bad credit car loans in Rockford, IL is varied, and knowing your options can help you make an informed decision.

1. Dealerships with Special Finance Departments

Many car dealerships, especially larger ones in the Rockford area, have dedicated "Special Finance" or "Second Chance Finance" departments. These departments specialize in working with customers who have less-than-perfect credit. They often have relationships with a wide network of subprime lenders, increasing your chances of approval.

- Pros: One-stop shop for car and financing, access to multiple lenders, staff experienced in bad credit situations.

- Cons: May sometimes push higher-interest loans or specific vehicles.

"Buy Here Pay Here" (BHPH) Dealerships: These are another option, where the dealership itself is the lender.

- Pros: High approval rates, often don’t rely heavily on credit scores, focus on income stability.

- Cons: Typically have much higher interest rates, limited vehicle selection, may not report payments to all credit bureaus (limiting credit building potential), and often require weekly or bi-weekly payments. Exercise caution and thoroughly review terms if considering a BHPH dealer.

2. Online Lenders and Lending Networks

The internet has opened up a world of possibilities for car loans, including those for bad credit. Many online lenders specialize in subprime auto financing. They allow you to apply for pre-qualification from the comfort of your home, often with just a soft credit inquiry that doesn’t harm your score.

- Pros: Convenience, quick pre-qualification, access to a wide range of lenders, ability to compare offers easily.

- Cons: Less personal interaction, may require more self-advocacy.

These platforms can connect you with lenders who are specifically looking for customers with your credit profile.

3. Credit Unions and Local Banks

While traditional banks often have stricter lending criteria for bad credit, local credit unions can sometimes be more flexible. Credit unions are member-owned and often prioritize helping their members, even those with challenging credit histories.

- Pros: Potentially lower interest rates than some subprime lenders, more personalized service, focus on member well-being.

- Cons: May still have higher credit score requirements than specialized bad credit lenders, might require you to be a member for a certain period.

It’s always worth checking with your local credit union in Rockford, IL, if you’re a member or eligible to join.

4. Comparing Offers

Pro tip from us: Always compare at least 3-4 offers to ensure you’re getting the best terms available for your situation. Apply for pre-qualification with several lenders or through a dealership that works with multiple finance companies. This allows you to see different interest rates, loan terms, and payment structures without committing to a specific loan.

Remember, a soft credit inquiry for pre-qualification doesn’t impact your credit score. Only a hard inquiry, which happens when you formally apply for a loan, affects your score. Multiple hard inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry, minimizing impact.

The Application Process: What to Expect

Once you’ve identified potential lenders for your bad credit car loan in Rockford, IL, understanding the application process will help you navigate it smoothly.

Pre-qualification vs. Full Application

It’s essential to distinguish between pre-qualification and a full application.

- Pre-qualification: This is an initial assessment where a lender reviews your basic financial information and gives you an estimate of what you might be approved for. It’s a "soft inquiry" on your credit and doesn’t affect your score. It’s a great way to gauge your options.

- Full Application: This is a formal request for a loan. It involves a "hard inquiry" on your credit report, which will temporarily lower your score by a few points. The lender will require all your documentation and conduct a thorough review before making a final decision.

Based on my experience, many applicants get confused between pre-qualification and pre-approval, thinking they are guaranteed a loan after pre-qualification. Always remember that pre-qualification is an estimate, not a guarantee.

Information Required

During the full application, lenders will ask for detailed information about your:

- Personal Information: Name, address, contact details, date of birth, Social Security Number.

- Employment History: Current employer, job title, length of employment, previous employers.

- Financial Information: Income, existing debts (mortgage/rent, credit cards, other loans), bank account details.

- Vehicle Information (if already chosen): Make, model, year, VIN.

Be honest and accurate with all the information you provide. Misrepresentation can lead to delays or rejection.

The Role of Co-Signers

If your credit is particularly challenged, a co-signer might significantly improve your chances of approval or help you secure a better interest rate. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you fail to make payments.

- Pros: Can make approval easier, potentially lower interest rates.

- Cons: The co-signer is fully liable for the debt, and their credit will be negatively impacted if you miss payments. This can strain relationships.

Carefully consider the implications for both you and your co-signer before pursuing this option.

Understanding Loan Terms

Before signing any agreement, ensure you fully understand the loan terms:

- Annual Percentage Rate (APR): This is the true cost of your loan, including interest and any fees, expressed as an annual percentage. For bad credit loans, APRs will be higher, potentially ranging from 10% to 25% or even more, depending on your credit profile and the market.

- Loan Term: The length of time you have to repay the loan, typically 36 to 72 months. Longer terms mean lower monthly payments but more interest paid over time.

- Monthly Payments: The fixed amount you’ll pay each month. Ensure this is manageable within your budget.

Don’t hesitate to ask questions if anything is unclear.

Negotiating Your Bad Credit Car Loan

Negotiating your bad credit car loan in Rockford, IL is a crucial step that many overlook. While your options might be more limited with bad credit, there’s still room to ensure you get the best possible deal.

Focus on the Total Cost, Not Just Monthly Payments

Dealerships often try to focus buyers on the monthly payment, making it seem affordable. However, a lower monthly payment achieved by extending the loan term (e.g., from 60 to 72 months) can significantly increase the total interest you pay over the life of the loan.

Always ask for the "out-the-door price" and the total cost of the loan, including all interest and fees. This comprehensive view allows for a more accurate comparison of offers.

Interest Rate Negotiation (if possible)

While your interest rate will likely be higher with bad credit, it’s not always set in stone. If you have multiple pre-approvals from different lenders, you can use them as leverage. For example, if one lender offers you 18% and another offers 16%, you can ask the first lender if they can match or beat the 16%.

Being prepared with a down payment and a clear budget can also give you more negotiating power.

Vehicle Price Negotiation

Remember, the car’s price is separate from the loan’s interest rate. Negotiate the selling price of the vehicle first, as if you were paying cash. Once you’ve agreed on a price, then discuss financing. This separates the two crucial elements of the deal and prevents confusion.

Common mistakes to avoid are falling in love with a car before negotiating the financing. This emotional attachment can lead you to accept less favorable loan terms.

Avoid Unnecessary Add-ons

Dealerships often offer various add-ons like extended warranties, GAP insurance, paint protection, or VIN etching. While some might be beneficial (like GAP insurance if you’re financing a large portion of the car’s value), others may not be worth the extra cost, especially when you’re already facing higher interest rates.

Carefully evaluate each add-on. Ask yourself if it’s truly necessary and if the benefit outweighs the added cost, which will also accrue interest over the loan term. You have the right to decline any add-on.

Beyond the Loan: Rebuilding Your Credit

Securing bad credit car loans in Rockford, IL isn’t just about getting a car; it’s a significant opportunity to rebuild your financial future. A car loan, when managed responsibly, can be a powerful tool for credit rehabilitation.

How a Car Loan Can Help Rebuild Credit

An auto loan is an installment loan, meaning you make fixed payments over a set period. Successfully managing this type of debt demonstrates your ability to handle credit responsibly, which is a major factor in your credit score (payment history accounts for 35% of your FICO score).

Here’s how it works:

- Consistent On-Time Payments: Each on-time payment you make is reported to the credit bureaus. Over time, a consistent record of timely payments will positively impact your credit score.

- Diversification of Credit Mix: Having a mix of credit types (revolving credit like credit cards and installment loans like car loans) can also positively influence your score.

- Building a Payment History: For those with little to no credit history, a car loan establishes a valuable payment record.

Pro tip from us: Think of your bad credit car loan not just as transportation, but as a powerful tool for credit rehabilitation. Every successful payment is a step towards a better financial future.

Strategies for Improving Credit Post-Loan

Beyond making your car payments, continue to implement other strategies to improve your credit score:

- Pay All Bills On Time: This includes utilities, rent, and other loans. Payment history is the most important factor.

- Keep Credit Card Balances Low: High credit utilization (using a large percentage of your available credit) negatively impacts your score. Aim to keep balances below 30% of your credit limit.

- Avoid Opening Too Many New Accounts: Each new credit application results in a hard inquiry, which can temporarily lower your score.

- Regularly Monitor Your Credit: Continue to check your credit report annually for errors and to track your progress.

By consistently applying these principles, you’ll see your credit score steadily improve. This will open doors to better interest rates on future loans and credit products. For more detailed advice on improving your financial standing, our guide on (Internal Link Placeholder 2) offers further insights.

FAQs About Bad Credit Car Loans Rockford, IL

Navigating the world of bad credit car loans in Rockford, IL often brings up several common questions. Here are answers to some of the most frequently asked:

Q1: Can I get a car loan with no down payment if I have bad credit?

A1: While possible, it’s significantly more challenging. Lenders prefer a down payment as it reduces their risk. A "no money down" option usually comes with higher interest rates and stricter approval criteria. We strongly recommend saving for a down payment.

Q2: What is a reasonable interest rate for a bad credit car loan?

A2: "Reasonable" is subjective and depends heavily on your specific credit profile. With bad credit, you can expect rates to be higher than average, potentially ranging from 10% to 25% or even higher. It’s crucial to compare offers and understand the total cost.

Q3: How long does the approval process take for bad credit car loans?

A3: The pre-qualification process can be very quick, sometimes just minutes online. A full application and approval can take anywhere from a few hours to a couple of days, especially if the lender needs to verify documentation. Being prepared with all your documents can speed up the process.

Q4: Do I always need a co-signer with bad credit?

A4: No, not always. Many individuals get approved for bad credit car loans without a co-signer. However, having one can increase your chances of approval or help you secure a lower interest rate, especially if your credit score is particularly low.

Q5: Can I refinance my bad credit car loan later?

A5: Yes, absolutely! Refinancing is a great strategy. As you make on-time payments and your credit score improves, you can apply to refinance your loan with a new lender at a lower interest rate. This can significantly reduce your monthly payments and the total amount of interest you pay over the life of the loan.

Q6: Are "no credit check" car loans legitimate?

A6: Be very cautious with "no credit check" loan offers. While some BHPH dealers might advertise this, they often compensate for the lack of a credit check with extremely high interest rates and unfavorable terms. Always ensure the lender is legitimate and transparent about all fees and rates.

For more information on understanding your credit score and its impact on borrowing, you can refer to trusted external sources like MyFICO: Understanding Your FICO Score.

Conclusion: Your Path to a Car Loan in Rockford, IL, is Clearer Than You Think

Securing bad credit car loans in Rockford, IL, might seem like a daunting task, but as we’ve explored, it’s a completely achievable goal with the right approach. Your credit history doesn’t have to be a permanent barrier to reliable transportation or financial improvement. With careful preparation, informed decision-making, and a commitment to responsible repayment, you can turn a challenging situation into a stepping stone towards a brighter financial future.

Remember the key takeaways: understand your credit, prepare your finances with a budget and down payment, explore diverse lending options in the Rockford area, negotiate wisely, and view your car loan as an opportunity to rebuild your credit. Many lenders in Rockford are ready to work with you, focusing on your current ability to pay and your commitment to improving your financial health.

Don’t let past financial difficulties dictate your future. Take the proactive steps outlined in this guide, and you’ll be well on your way to driving off the lot in Rockford, IL, with a car that meets your needs and a loan that helps you move forward. Your journey starts now.