Navigating the Road to a Car Loan: Your Comprehensive Guide to Getting Approved with a 577 Credit Score

Navigating the Road to a Car Loan: Your Comprehensive Guide to Getting Approved with a 577 Credit Score Carloan.Guidemechanic.com

The dream of owning a reliable vehicle is universal. It represents freedom, convenience, and often a necessity for daily life – commuting to work, running errands, or simply exploring. However, for many, the path to car ownership can feel daunting, especially when faced with a less-than-perfect credit score. If your credit score hovers around 577, you might be wondering if a car loan is even a realistic possibility. The good news? It absolutely can be.

Securing a car loan with a 577 credit score presents unique challenges, but it’s far from an insurmountable obstacle. This score typically falls into the "subprime" or "poor" category, meaning lenders perceive you as a higher risk. However, there are specific strategies, resources, and insights that can significantly increase your chances of approval and help you secure a manageable loan. In this super comprehensive guide, we’ll delve deep into everything you need to know about navigating the "577 Credit Score Car Loan" landscape, providing you with actionable advice and expert tips to drive away in your next vehicle.

Navigating the Road to a Car Loan: Your Comprehensive Guide to Getting Approved with a 577 Credit Score

Understanding Your 577 Credit Score and Its Impact on Car Loans

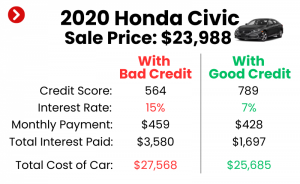

Before we dive into solutions, let’s first understand the landscape. A 577 credit score places you firmly in the "Fair" to "Poor" range, depending on the specific credit scoring model (like FICO or VantageScore). Lenders typically categorize scores below 620-660 as subprime.

What does this mean for a car loan? Essentially, it signals to lenders that you may have a history of missed payments, high credit utilization, or other financial challenges. Because of this perceived higher risk, lenders will often offer less favorable terms. This usually translates to higher interest rates, which directly impact your monthly payments and the total cost of the loan over its lifetime. It might also mean stricter approval criteria or requiring additional assurances.

However, it’s crucial to remember that a 577 score doesn’t automatically close the door to financing. Many lenders specialize in subprime auto loans, understanding that everyone deserves a second chance or experiences financial setbacks. Their business model is built around assessing and mitigating these risks, often through different loan structures or requirements.

Preparing for Your Car Loan Application: Essential Steps

Preparation is paramount when seeking a car loan with a 577 credit score. A well-prepared applicant demonstrates responsibility and seriousness, which can positively influence a lender’s decision.

1. Know Your Credit Report Inside Out

Your credit report is your financial resume. Before you even think about stepping into a dealership or applying for a loan, you must understand what’s on it.

- Check for Errors: Based on my experience, a surprising number of credit reports contain inaccuracies. These could be old debts that have been paid off, incorrect account statuses, or even fraudulent activity. Even a small error could be dragging your score down unnecessarily.

- Dispute Inaccuracies: If you find errors, dispute them immediately with all three major credit bureaus (Experian, Equifax, TransUnion). This process can take time, so start early. Correcting errors can sometimes boost your score.

- Understand Influencing Factors: Familiarize yourself with the factors impacting your 577 score. Is it late payments? High credit card balances? Collections? Knowing the root cause helps you address it, even if incrementally.

- Pro Tip from us: You are entitled to a free copy of your credit report from each of the three major credit bureaus once a year via AnnualCreditReport.com. Take advantage of this. Reviewing all three is vital because sometimes information isn’t consistently reported across them.

2. Budgeting Like a Pro: Determine What You Can Truly Afford

Don’t just think about the car’s price; think about the total cost of ownership.

- Realistic Monthly Payments: Beyond the loan principal and interest, factor in insurance, fuel, maintenance, and potential repair costs. A car is an ongoing expense.

- Create a Detailed Budget: Outline all your income and expenses. This helps you identify how much disposable income you genuinely have for a car payment without straining your finances.

- Debt-to-Income (DTI) Ratio: Lenders look at your DTI ratio (your total monthly debt payments divided by your gross monthly income). A lower DTI indicates you have more money available to pay new debts. Aim for a DTI below 43%, though lower is always better, especially with a 577 credit score.

3. Saving for a Down Payment: Your Best Ally

A significant down payment is arguably one of the most powerful tools you have when applying for a car loan with bad credit.

- Reduce Lender Risk: A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It shows commitment and financial stability.

- Lower Monthly Payments & Interest: A smaller loan amount means lower monthly payments and less interest paid over the life of the loan. This can save you thousands of dollars.

- Increase Approval Chances: Lenders are more likely to approve applicants with a substantial down payment, even with a lower credit score. Aim for at least 10-20% of the car’s value, if possible.

4. Consider a Co-signer (If Applicable)

If you have a trusted friend or family member with excellent credit and a stable income, a co-signer can dramatically improve your chances of approval and secure better loan terms.

- Who is a Good Co-signer? Someone with a high credit score, a low DTI, and a strong payment history. They should understand the responsibility they’re taking on.

- Pros and Cons: For you, it means better rates and approval. For the co-signer, it means they are equally responsible for the debt. If you default, their credit score will be negatively impacted, and they could be pursued for payment.

- Risks Involved: This is a serious commitment for both parties. Common mistakes to avoid include not having a clear agreement with your co-signer or taking on a loan you both can’t afford. Ensure open communication and a clear understanding of the implications.

Strategies for Securing a Car Loan with a 577 Credit Score

Once you’ve prepared your financial groundwork, it’s time to explore your lending options. Not all lenders are created equal, especially when dealing with subprime credit.

1. Exploring Lender Options

- Subprime Lenders/Special Finance Dealerships: These lenders and dealerships specialize in working with individuals who have lower credit scores.

- Their Business Model: They understand the unique challenges of bad credit borrowers and have different underwriting criteria. They often offer "buy here, pay here" options, where the dealership itself acts as the lender.

- How to Find Reputable Ones: Look for dealerships with positive reviews, particularly concerning their finance department. Ask for recommendations. Be wary of places that guarantee approval without asking for any financial details.

- What to Expect: Expect higher interest rates. Thoroughly review all terms and conditions.

- Credit Unions: Often overlooked, credit unions can be a fantastic resource for borrowers with less-than-perfect credit.

- More Flexible: They are member-owned and often more willing to work with members based on their overall financial picture, not just their credit score.

- Membership Requirements: You usually need to meet certain criteria to join (e.g., live in a specific area, work for a particular employer, or join an affiliated organization).

- Online Lenders Specializing in Bad Credit: The digital age has brought a surge of online lenders catering specifically to subprime borrowers.

- Convenience and Speed: Applications are often quick, and decisions can be made rapidly.

- Researching Legitimacy: This is crucial. Common mistakes to avoid are falling for predatory lenders who charge exorbitant fees or have unclear terms. Look for lenders with transparent rates, clear terms, and positive customer reviews. Check their standing with the Better Business Bureau.

2. Pre-Approval: Your Secret Weapon

Getting pre-approved for a loan before you even set foot on a car lot gives you significant advantages.

- Benefits of Pre-approval:

- Know Your Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Negotiating Power: You become a cash buyer in the eyes of the dealership. This puts you in a stronger position to negotiate the car’s price, as they know you already have financing secured.

- Focus on the Car: You can concentrate solely on finding the right vehicle, not simultaneously scrambling for financing.

- Soft vs. Hard Inquiries: Most pre-approvals involve a "soft inquiry" on your credit report, which doesn’t affect your score. Once you formally apply for the loan, it becomes a "hard inquiry," which can temporarily ding your score by a few points.

- Pro Tip from us: Shop around for pre-approvals within a short timeframe (usually 14-45 days, depending on the scoring model). This is because multiple inquiries for the same type of loan within a condensed period are often treated as a single inquiry, minimizing the impact on your credit score.

3. Choosing the Right Vehicle: Practicality Over Prestige

With a 577 credit score, your primary goal should be to secure reliable transportation, not necessarily your dream car.

- Focus on Reliability and Affordability: Opt for a vehicle known for its longevity and lower maintenance costs. A reliable car means fewer unexpected repair bills, which is vital when managing a tight budget.

- New vs. Used: Used cars almost always have lower price tags, which directly reduces the amount you need to borrow. This is a significant advantage for bad credit borrowers, as it lessens the loan amount and associated risk for the lender.

- Avoid Luxury or High-Performance Vehicles: These cars come with higher price tags, higher insurance costs, and often more expensive maintenance. Prioritize functionality and affordability.

Navigating the Loan Process and Maximizing Your Chances

Once you’ve identified potential lenders and a suitable vehicle, it’s time to finalize the deal. This stage requires diligence and a keen eye for detail.

1. Gathering Necessary Documents

Having all your paperwork in order streamlines the application process and demonstrates your preparedness.

- Proof of Income: Recent pay stubs (typically 2-3 months), tax returns (if self-employed), or bank statements showing regular deposits.

- Proof of Residency: Utility bills (electricity, water, gas) or a lease agreement with your name and current address.

- Identification: A valid driver’s license and sometimes a second form of ID.

- Bank Statements: Recent statements (usually 1-3 months) to show financial activity and stability.

2. Negotiating Loan Terms (Even with Bad Credit)

Many people assume that with a low credit score, they have no room to negotiate. This is a common misconception. While your leverage might be less, negotiation is still possible and necessary.

- Focus on the Total Price of the Car: Don’t get fixated solely on the monthly payment. A lower monthly payment over a longer term often means paying significantly more in total interest. Negotiate the vehicle’s selling price first.

- Interest Rate Negotiation (if possible): If you have pre-approval from another lender, you can use it to negotiate a better rate with the dealership’s finance department. They might be able to beat or match it to keep your business.

- Avoid Unnecessary Add-ons: Be cautious of dealer add-ons like extended warranties, rustproofing, paint protection, or VIN etching. While some might offer value, many are highly marked up and can significantly increase your loan amount. Understand each one thoroughly and only accept what you genuinely need.

- Based on my experience: Always question everything. Don’t be afraid to say "no" or ask for time to consider an offer. A reputable dealership will respect your decision.

3. The Power of a Lower Loan Amount

This cannot be stressed enough: the less you borrow, the better your position.

- Reduces Risk for the Lender: A smaller loan means less financial exposure for the lender, making them more comfortable approving your application.

- Ways to Achieve This:

- Larger Down Payment: As discussed, this is your most potent tool.

- Less Expensive Car: Choosing a more affordable, reliable used car rather than a brand-new model significantly reduces the principal amount.

- Trade-in Value: If you have an existing vehicle, getting a fair trade-in value can act as an additional down payment.

Beyond the Loan: Rebuilding Your Credit for the Future

Getting a car loan with a 577 credit score isn’t just about driving away in a new vehicle; it’s an incredible opportunity to improve your financial standing. This loan can be a stepping stone to a much healthier credit profile.

1. Making Timely Payments: Your Golden Rule

This is the single most important factor in credit score improvement. Payment history accounts for 35% of your FICO score.

- Consistency is Key: Make every payment on time, every month, without fail.

- Set Up Auto-Pay: To avoid missing a payment, set up automatic deductions from your bank account a few days before the due date.

- This Car Loan is an Opportunity: Successfully managing this loan will demonstrate responsible financial behavior to future lenders, gradually increasing your credit score.

2. Monitoring Your Credit Score

Don’t just set it and forget it. Regularly check your credit reports and monitor your score.

- Regular Checks: Use free credit monitoring services or your bank’s provided tools to keep an eye on your score’s progress.

- Tools and Services: Services like Credit Karma, Experian, or your credit card issuer often provide free credit scores and monitoring.

- Address Issues Promptly: If you see a dip or an unexpected entry, investigate it immediately.

3. Financial Discipline Beyond Your Car Loan

Improving your overall financial health will support your credit score growth.

- Maintain Low Credit Utilization: Keep balances on credit cards low – ideally below 30% of your credit limit, but lower is always better.

- Pay Down Other Debts: Reducing other outstanding debts, especially high-interest ones, frees up more disposable income and improves your DTI ratio.

- Build an Emergency Fund: Having a financial cushion prevents you from falling behind on payments if an unexpected expense arises.

Conclusion

Securing a car loan with a 577 credit score might seem like an uphill battle, but with the right knowledge, preparation, and strategic approach, it is absolutely achievable. This guide has provided you with a comprehensive roadmap, from understanding your credit score and preparing your finances to exploring various lender options and navigating the negotiation process.

Remember, your 577 credit score is a reflection of past financial activity, but it doesn’t dictate your future. By being proactive, disciplined, and informed, you can not only get approved for a car loan but also use this opportunity to significantly improve your credit score. This isn’t just about getting a car; it’s about taking a crucial step towards greater financial stability and opening doors to better opportunities down the road. Drive forward with confidence – your journey to a 577 credit score car loan success starts now!