Navigating the Road to a Car Loan: Your Ultimate Guide to Getting Approved with Bad Credit

Navigating the Road to a Car Loan: Your Ultimate Guide to Getting Approved with Bad Credit Carloan.Guidemechanic.com

Getting a car loan can feel like an uphill battle when your credit score isn’t pristine. Many people find themselves in this challenging situation, believing that their dream of owning a reliable vehicle is out of reach. But here’s the truth: securing a car loan with bad credit is absolutely possible. It simply requires a different approach, more preparation, and knowing exactly where to look.

As an expert blogger and SEO content writer, I understand the frustration and confusion that comes with bad credit auto financing. This comprehensive guide is designed to be your trusted roadmap, offering in-depth insights and actionable strategies to help you navigate the complexities of securing a car loan, even when your credit history has a few bumps. We’ll explore the best places to find lenders, how to boost your approval chances, and common pitfalls to avoid, ensuring you get real value and make an informed decision.

Navigating the Road to a Car Loan: Your Ultimate Guide to Getting Approved with Bad Credit

Understanding the "Bad Credit" Challenge in Auto Lending

Before we dive into solutions, let’s understand why bad credit poses a challenge. Lenders primarily assess risk. A low credit score, often falling below 620-660, signals to them that you might have had trouble managing debt in the past. This translates into a higher perceived risk of default on a new loan.

Based on my experience, many people mistakenly think a bad credit score is a permanent roadblock. While it certainly makes lending institutions more cautious, it doesn’t close all doors. The key is to demonstrate to potential lenders that you are a responsible borrower now, or that the circumstances leading to your bad credit are behind you.

The reality of lending with bad credit often involves higher interest rates. This is how lenders offset the increased risk they are taking on. Understanding this upfront helps you manage expectations and prepare for the financial implications of your loan. It’s not about finding a "guaranteed approval car loan" with no strings attached, but rather finding a fair loan that helps you get on the road and, ideally, rebuild your credit.

Preparation is Key: Boosting Your Chances Before You Apply

The most significant mistake people with bad credit make is applying for loans without any prior preparation. This scattergun approach can actually hurt your credit score further due to multiple hard inquiries. Instead, adopt a strategic mindset.

Knowing Your Credit Score Inside and Out

Your credit score is the first thing a lender will look at. It’s a three-digit number that summarizes your creditworthiness. You can get a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months at AnnualCreditReport.com. Many credit card companies and banks also offer free credit score monitoring services.

Understanding your score helps you gauge your standing and identify areas for improvement. It also gives you leverage when discussing loan terms, as you’ll know what lenders are seeing. Don’t be surprised by what’s on your report; proactively check it.

Reviewing Your Credit Report for Accuracy

Once you have your credit report, don’t just glance at the score. Carefully review every entry for errors. Mistakes on your credit report, such as incorrect late payments or accounts that aren’t yours, are surprisingly common. These errors can artificially lower your score.

If you find any inaccuracies, dispute them immediately with the credit bureau. Correcting errors can sometimes significantly improve your score in a relatively short period, potentially qualifying you for better loan terms. This due diligence is a powerful step in your preparation.

Saving for a Substantial Down Payment

A down payment is perhaps your strongest ally when applying for a car loan with bad credit. Putting down a significant amount of cash reduces the loan amount, which in turn reduces the lender’s risk. It shows commitment and financial responsibility.

Based on my experience, a down payment of 10% to 20% can make a huge difference in approval odds and interest rates. It demonstrates to the lender that you have skin in the game and are less likely to default. Even a few hundred dollars can be better than nothing, so start saving aggressively.

Establishing a Realistic Budget

Before you even look at cars, establish a clear budget. This isn’t just about the monthly payment; it’s about the total cost of ownership. Factor in insurance, fuel, maintenance, and the loan payment itself. Can you truly afford this car without stretching your finances to the breaking point?

Common mistakes to avoid are falling in love with a car beyond your means. Lenders want to see that you can comfortably afford the loan. A realistic budget ensures you don’t overcommit and can make every payment on time, which is crucial for rebuilding credit. For a deeper dive into understanding your budget and affordability, check out our guide:

Gathering Necessary Documents in Advance

Be prepared to present a range of documents. Lenders will typically ask for proof of income (pay stubs, tax returns), proof of residence (utility bills), a valid driver’s license, and potentially a list of references. Having these ready streamlines the application process.

The more organized you are, the more serious and reliable you appear to lenders. This small detail can subtly influence their perception of your creditworthiness, even with a lower score. It signals responsibility and preparedness.

Considering a Co-signer or Co-borrower

If you have a trusted family member or friend with excellent credit, asking them to co-sign your loan can dramatically improve your chances of approval and secure a better interest rate. A co-signer essentially guarantees the loan, taking on equal responsibility if you default.

Pro tips from us: While a co-signer is a powerful tool, it’s a serious commitment for them. Ensure you are absolutely confident in your ability to make payments on time, as any missed payments will negatively impact their credit as well. Discuss the responsibilities clearly before involving anyone.

The Best Places To Get A Car Loan With Bad Credit

Now that you’re prepared, let’s explore the specific avenues where you have the highest chance of securing a car loan with bad credit. Each option has its unique advantages and disadvantages.

A. Dealership Financing: Your One-Stop Shop

Many dealerships offer in-house financing or work with a network of lenders, some of whom specialize in subprime auto loans (loans for borrowers with less-than-perfect credit). This can be a convenient option, as you can often complete the entire car buying and financing process in one location.

How it Works: Dealerships act as intermediaries. They submit your application to various lenders in their network, including those that cater to bad credit scores. Some dealerships also offer "Buy Here, Pay Here" (BHPH) financing, where the dealership itself is the lender.

Pros:

- Convenience: You can choose a car and secure financing all in one visit. This streamlines the process significantly.

- Specialized Lenders: Dealerships often have relationships with lenders who are more willing to work with bad credit applicants. They understand the nuances of subprime lending.

- Flexibility: Dealers might have more leeway to adjust vehicle prices or financing terms to make a deal happen, especially for used cars.

Cons:

- Higher Interest Rates: Subprime loans through dealerships almost always come with higher interest rates due to the increased risk involved.

- Limited Vehicle Choice: Especially with BHPH lots, your car selection might be limited to older, higher-mileage vehicles.

- Potential for Predatory Terms: While not all dealerships are like this, some BHPH lots can have very high interest rates and unfavorable terms. Always read the fine print carefully.

From our perspective, while convenient, caution is paramount with dealership financing. Always compare the offer to what you might get elsewhere. Don’t feel pressured to sign on the spot.

B. Online Lenders Specializing in Bad Credit

The internet has revolutionized lending, opening up numerous options for those with bad credit. Many online lenders specifically cater to subprime borrowers, leveraging technology to quickly assess risk and offer pre-approvals.

How it Works: You typically fill out a single online application, and the platform then connects you with multiple lenders who are likely to approve your loan. These lenders often have less stringent credit requirements than traditional banks.

Pros:

- Quick Pre-qualification/Pre-approval: You can often get a decision within minutes, without impacting your credit score with a hard inquiry initially. This allows you to shop for rates before committing.

- Wider Network of Lenders: Online platforms can connect you to dozens of lenders, increasing your chances of finding an approval. This broad reach is a significant advantage.

- Competitive Rates (Sometimes): While rates will still be higher than for good credit, the competition among online lenders can sometimes lead to more favorable terms than a single dealership might offer.

- Convenience and Discretion: You can apply from the comfort of your home, without face-to-face pressure.

Cons:

- Need to Be Careful of Scams: The online space can attract less reputable lenders. Always verify the legitimacy of the company before providing personal information.

- Less Personal Interaction: If you prefer face-to-face discussions and personalized advice, online lending might feel impersonal.

- Varying Terms: Each lender will have different terms, so careful comparison is essential to avoid hidden fees or unfavorable clauses.

Pro tips from us: Look for lenders that offer "soft credit checks" for pre-qualification. This allows you to see potential rates without harming your score. Only proceed with a full application (which involves a hard credit check) once you’re serious about an offer.

C. Credit Unions: The Borrower-Friendly Option

Credit unions are non-profit financial cooperatives owned by their members. Unlike traditional banks, their primary goal isn’t maximizing profit for shareholders but serving their members. This philosophy often translates into more flexible lending practices and potentially better rates, even for those with bad credit.

How it Works: To get a loan from a credit union, you usually need to become a member first. Membership requirements are often broad, such as living in a certain geographic area, working for a specific employer, or being affiliated with a particular organization. Once a member, you can apply for an auto loan.

Pros:

- More Flexible Lending: Credit unions are often more willing to look beyond just your credit score. They might consider your overall financial situation, relationship with the credit union, and payment history.

- Community-Focused: They tend to be more understanding and willing to work with members facing financial challenges. This personal touch can make a big difference.

- Potentially Lower Rates: Because they are non-profit, credit unions can sometimes offer lower interest rates and fees compared to traditional banks or even subprime lenders.

Cons:

- Membership Requirements: You must meet specific criteria to join a credit union, which might limit your options.

- May Still Be Cautious: While more flexible, credit unions still need to mitigate risk. Very low scores or recent bankruptcies might still make approval challenging.

- Slower Application Process: Sometimes the application and approval process can take a bit longer than with online lenders.

If you qualify for membership, a credit union should absolutely be one of your first stops. Their member-first approach can be a significant advantage.

D. Traditional Banks (With Caveats)

While often the first place people think of for loans, traditional banks are generally the most challenging option for those with bad credit. They typically have stricter lending criteria and higher credit score requirements.

How it Works: You apply directly to a bank where you might already have an account. They will review your credit history, income, and debt-to-income ratio to determine eligibility.

Pros:

- Established Reputation: Banks are generally very stable and reputable institutions, offering a sense of security.

- Existing Relationship: If you have a long-standing banking relationship with a particular institution, they might be slightly more inclined to work with you, but this is not guaranteed with bad credit.

Cons:

- Very Difficult with Truly Bad Credit: Most traditional banks prefer borrowers with good to excellent credit. Their risk models are less equipped for subprime lending.

- Higher Score Requirements: You’ll likely need a credit score in the mid-600s or higher to even be considered by many major banks.

- Less Flexibility: They are less likely to make exceptions based on personal circumstances compared to credit unions.

Based on my experience, traditional banks are usually a long shot if your credit is severely damaged. However, if your bad credit is borderline (e.g., in the lower end of "fair" credit), it’s worth exploring if you have a strong existing relationship with your bank.

Navigating the Application Process with Bad Credit

Once you’ve identified potential lenders, understanding the application process and what to look for is crucial. This is where you protect yourself and secure the best possible terms.

Pre-qualification vs. Pre-approval: Know the Difference

These terms are often used interchangeably, but they have distinct meanings.

- Pre-qualification: This is a soft inquiry that doesn’t affect your credit score. It gives you an estimate of what you might qualify for, based on basic information. Use this to compare rates from multiple lenders.

- Pre-approval: This involves a hard inquiry on your credit report, which will slightly ding your score. It’s a conditional offer from a lender for a specific loan amount and interest rate, giving you concrete terms to work with.

Always aim for pre-qualification first to explore options without commitment. Only move to pre-approval when you’ve narrowed down your choices.

Understanding Your Loan Terms: APR, Loan Term, and Total Cost

Do not just focus on the monthly payment. This is a common trap.

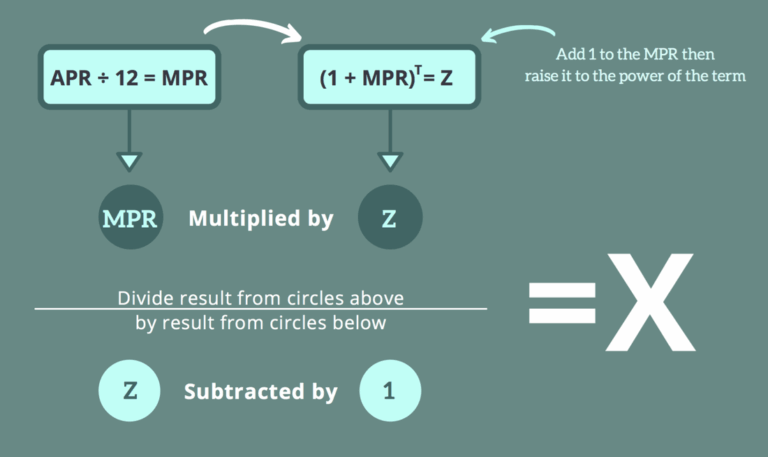

- APR (Annual Percentage Rate): This is the true cost of borrowing, including interest and some fees, expressed as a yearly percentage. With bad credit, your APR will be higher, potentially in the double digits or even higher.

- Loan Term: This is the length of time you have to repay the loan (e.g., 36, 48, 60, 72 months). Longer terms mean lower monthly payments but significantly more interest paid over the life of the loan.

- Total Cost of the Loan: This is the sum of the principal loan amount plus all the interest you will pay over the loan term. Always ask for this figure.

To fully grasp the nuances of loan terms and how they impact your overall cost, read our article:

The Power of a Down Payment (Revisited)

We mentioned this in preparation, but it bears repeating during the application phase. A larger down payment can not only increase your approval chances but also lower your monthly payments and reduce the total interest paid. It also means you’ll owe less than the car is worth sooner, avoiding "negative equity."

If you can wait and save an extra few hundred or thousand dollars, it will likely pay off in the long run. Don’t underestimate its impact on lenders.

Negotiating Your Loan: Yes, Even with Bad Credit

Many people with bad credit feel they have no room to negotiate, but this isn’t entirely true.

- Shop Around: The best negotiation tactic is having multiple offers. If Lender A offers 18% and Lender B offers 15%, you can try to leverage Lender B’s offer with Lender A.

- Be Prepared to Walk Away: If a deal feels too expensive or unfair, be willing to leave. There are always other options.

- Focus on the Total Cost: Negotiate the car’s price separately from the loan terms. A lower car price means a lower loan amount, which helps everyone.

Pro tips from us: Never discuss your financing situation until you’ve agreed on the car’s price. This prevents the dealer from shifting money around between the car price and the loan terms.

Common Pitfalls and How to Avoid Them

The subprime auto loan market can be tricky. Being aware of potential traps will help you make a smarter decision.

- High-Pressure Sales Tactics: Some dealerships or lenders might try to rush you into a deal. Don’t succumb to pressure. Take your time, read everything, and ask questions.

- Excessive Interest Rates: While higher rates are expected, some lenders might quote unreasonably high rates. This is why shopping around and knowing the average rates for your credit tier is essential.

- Unnecessary Add-ons: Be wary of extra products like extended warranties, GAP insurance (which can be useful but should be researched), or paint protection packages that inflate the loan amount. Only buy what you truly need and understand.

- Long Loan Terms (Stretching Payments): A 72- or 84-month loan might offer a low monthly payment, but you’ll pay significantly more in interest over the years. You might also end up owing more than the car is worth for a long time.

- Ignoring the Total Cost of the Loan: As mentioned, focusing only on the monthly payment blinds you to the true financial burden. Always calculate the total amount you’ll pay back.

Common mistakes to avoid are signing without fully understanding the fine print, accepting the first offer, and not asking for a breakdown of all costs. Your due diligence is your best defense.

Rebuilding Your Credit Through Your Car Loan

Securing a car loan with bad credit isn’t just about getting a vehicle; it’s a powerful opportunity to rebuild your credit history. This can be one of the most significant benefits of taking on a subprime loan.

How On-Time Payments Help: Your payment history is the single most important factor in your credit score. By making every car loan payment on time, consistently, you demonstrate responsible financial behavior to credit bureaus. This positive activity will be reported, gradually improving your credit score over time.

Importance of Making Every Payment: Even one late payment can set back your credit rebuilding efforts. Set up automatic payments if possible, and ensure you have sufficient funds in your account each month. Treat your car loan payment as a top priority.

As your credit score improves, you’ll gain access to better financial products, including lower interest rates on future loans and credit cards. It’s a stepping stone towards greater financial freedom. For more strategies on improving your financial health beyond car loans, visit the Consumer Financial Protection Bureau’s website for excellent resources:

Conclusion: Your Journey to a Car Loan with Bad Credit

Getting a car loan with bad credit is undoubtedly a challenge, but it is far from an impossible feat. The key lies in thorough preparation, knowing your options, and approaching the process with an informed and strategic mindset. By understanding your credit, saving for a down payment, exploring specialized lenders like online platforms and credit unions, and being vigilant against predatory practices, you significantly increase your chances of approval.

Remember, this isn’t just about getting a car; it’s about making a smart financial decision that can serve as a catalyst for rebuilding your credit. Take your time, compare offers, read every document, and don’t be afraid to walk away from a deal that doesn’t feel right. With the right approach, you can successfully navigate the road to a car loan, secure reliable transportation, and pave the way for a healthier financial future. Start preparing today, and empower yourself to drive off with confidence.