Navigating the Road to a New Ride: Understanding Your $30,000 Car Loan Payments

Navigating the Road to a New Ride: Understanding Your $30,000 Car Loan Payments Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is exciting, but it often comes with a significant financial decision: securing a car loan. For many, a $30,000 car strikes a perfect balance, offering a wide range of reliable and feature-rich options without venturing into luxury territory. However, understanding the intricacies of 30000 dollar car loan payments is crucial for making a smart, informed decision that aligns with your financial well-being.

This comprehensive guide will demystify the world of auto financing, providing you with the knowledge to confidently navigate your next car purchase. We’ll delve into all the factors that shape your monthly payments, helping you secure the best possible terms for your $30,000 car loan.

Navigating the Road to a New Ride: Understanding Your $30,000 Car Loan Payments

Why a $30,000 Car Loan is a Common Crossroads for Car Buyers

A $30,000 price point for a vehicle is incredibly popular, and for good reason. It opens up access to a vast array of new sedans, compact SUVs, and even some well-equipped mid-size vehicles. Furthermore, this budget can unlock premium trims of more economical models or allow for a robust selection of certified pre-owned vehicles with lower mileage and excellent features.

The sheer variety available at this price point makes it a sweet spot for many consumers looking for reliability, modern technology, and safety features. Consequently, understanding the car loan payments associated with this amount becomes a primary concern for a significant portion of the car-buying public. It’s about finding that ideal balance between desire and affordability.

The Pillars of Your $30,000 Car Loan Payments: What Really Drives the Numbers

When you’re looking at financing a car, especially a substantial sum like $30,000, several key elements combine to determine your precise monthly payment. It’s never just about the sticker price. Based on my experience, focusing solely on the advertised monthly payment without understanding these underlying factors is one of the most common mistakes car buyers make.

Let’s break down these critical components in detail.

1. The Interest Rate: Your Loan’s Invisible Cost Driver

The interest rate is arguably the single most impactful factor on your overall loan cost and, consequently, your monthly payments. This percentage represents the cost of borrowing money from a lender. A higher interest rate means you’ll pay more for the privilege of borrowing that $30,000, even if all other factors remain constant.

How Your Interest Rate is Determined:

- Credit Score: This is paramount. Lenders use your credit score as a primary indicator of your financial reliability. An excellent credit score (typically 750+) can unlock the lowest interest rates, sometimes even 0% APR promotions. A lower score, however, signals higher risk to lenders, resulting in significantly higher rates.

- Lender Type: Different lenders have different risk appetites and rate structures. Banks, credit unions, and dealership financing arms each offer unique packages. Shopping around is crucial here.

- Loan Term: Shorter loan terms often come with slightly lower interest rates because the lender’s money is tied up for a shorter period.

- Current Market Conditions: Broader economic factors, such as the prime rate set by the Federal Reserve, influence all lending rates. When the prime rate goes up, so do auto loan rates.

Pro Tip from Us: Even a small difference in your interest rate can translate into hundreds or thousands of dollars over the life of a $30,000 car loan. Always strive for the lowest possible rate by improving your credit and comparing multiple offers.

2. The Loan Term: How Long You’ll Be Paying

The loan term refers to the length of time you have to repay your loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor has a direct, inverse relationship with your monthly payment.

Shorter Loan Terms (e.g., 36-48 months):

- Pros: You’ll pay significantly less in total interest over the life of the loan. You’ll own the car outright much faster. There’s less risk of being "upside down" on your loan (owing more than the car is worth).

- Cons: Your monthly payments will be substantially higher, potentially stretching your budget.

Longer Loan Terms (e.g., 72-84 months):

- Pros: Lower monthly payments, making the car seem more affordable on a month-to-month basis. This can free up cash flow for other expenses.

- Cons: You’ll pay considerably more in total interest, sometimes thousands of dollars more. You’re more likely to be upside down on your loan, especially in the early years. The car will likely be older and have more wear and tear when you finally pay it off.

Common mistakes to avoid are extending the loan term simply to achieve a lower monthly payment without considering the total cost. While it might feel good now, it costs you more in the long run for your 30000 dollar car loan payments.

3. Your Down Payment: Reducing Your Borrowing Needs

A down payment is the initial amount of money you pay upfront toward the purchase price of the car. It directly reduces the principal amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay.

The Power of a Down Payment:

- Lower Monthly Payments: Less money borrowed means smaller installments.

- Reduced Interest Paid: You’re paying interest on a smaller principal amount.

- Improved Loan-to-Value (LTV): Lenders view a larger down payment favorably, as it shows your commitment and reduces their risk. This can sometimes lead to better interest rates.

- Avoid Being Upside Down: A substantial down payment creates equity in your vehicle from day one, helping you avoid owing more than the car is worth, especially if depreciation is rapid.

Based on my experience, aiming for at least a 10-20% down payment on a new car is a smart financial move. For a $30,000 car loan, that would be $3,000 to $6,000.

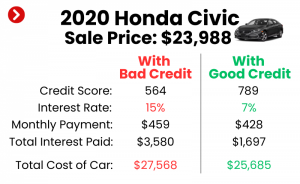

4. Your Credit Score: The Gateway to Better Terms

We touched upon this with interest rates, but your credit score’s influence extends beyond just the rate. It’s a comprehensive report card on your financial history, and lenders rely on it heavily for loan approval and setting the terms of your auto loan.

Credit Score Tiers and Their Impact:

- Excellent (750+): You’ll qualify for the best rates and most favorable terms.

- Good (670-749): Still qualify for competitive rates, though perhaps not the absolute lowest.

- Fair (580-669): Expect higher interest rates, and you might need a larger down payment or a co-signer.

- Poor (Below 580): Securing a loan can be challenging, and interest rates will be very high. Subprime lenders might be your only option, leading to significantly higher car loan payments.

Pro Tip from Us: Before you even step foot in a dealership, check your credit score. If it needs improvement, take steps to boost it, such as paying down debt or correcting errors on your credit report. This preparation can save you thousands on your 30000 dollar car loan payments.

5. Debt-to-Income Ratio (DTI): Are You Overburdened?

Your DTI ratio is another critical metric lenders use. It compares your total monthly debt payments (including your proposed car loan payment) to your gross monthly income. Lenders want to ensure you have enough disposable income to comfortably make your payments.

A low DTI ratio (typically below 36-40%) signals to lenders that you are a responsible borrower with the capacity to take on new debt. A high DTI might make securing a $30,000 car loan more difficult or lead to less favorable terms.

6. Trade-in Value: Your "Pre-Paid" Down Payment

If you have an existing vehicle, trading it in can act like a down payment, reducing the amount you need to finance for your new car. The equity in your trade-in (its market value minus any outstanding loan balance) directly lowers your principal.

Ensure you research your car’s trade-in value beforehand using sites like Kelley Blue Book or Edmunds. This prevents you from accepting an offer that undervalues your vehicle, effectively boosting your down payment for the new $30,000 car loan.

7. Additional Costs and Fees: The Hidden Surprises

Beyond the purchase price and interest, several other costs can influence the total amount you finance or pay out-of-pocket, indirectly affecting your car affordability and overall budget for 30000 dollar car loan payments.

- Sales Tax: Varies by state and can add a significant amount to your total cost.

- Registration and Licensing Fees: Required by your state’s DMV.

- Documentation Fees: Fees charged by the dealership for processing paperwork. These can often be negotiated.

- Extended Warranties: While they offer peace of mind, they add to the total cost and can sometimes be rolled into your loan. Consider their true value carefully.

- GAP Insurance: Guaranteed Asset Protection (GAP) covers the difference between what you owe on your loan and what your insurance pays if your car is totaled or stolen. It’s especially important if you make a small down payment or have a long loan term.

Common mistakes to avoid are not accounting for these additional costs in your budget. They can easily add several hundred to a few thousand dollars to your total out-the-door price.

Calculating Your Potential $30,000 Car Loan Payments: Real-World Scenarios

To illustrate how these factors come together, let’s look at a few hypothetical scenarios for a $30,000 car loan (assuming no trade-in, and after a $3,000 down payment, so you’re financing $27,000).

-

Scenario 1: Excellent Credit

- Amount Financed: $27,000

- Interest Rate: 4%

- Loan Term: 60 months

- Estimated Monthly Payment: ~$499

- Total Interest Paid: ~$2,940

-

Scenario 2: Good Credit

- Amount Financed: $27,000

- Interest Rate: 7%

- Loan Term: 60 months

- Estimated Monthly Payment: ~$534

- Total Interest Paid: ~$5,040

-

Scenario 3: Fair Credit with Longer Term

- Amount Financed: $27,000

- Interest Rate: 10%

- Loan Term: 72 months

- Estimated Monthly Payment: ~$485

- Total Interest Paid: ~$7,920

As you can see, even with a longer term, a higher interest rate in Scenario 3 results in a substantially higher total interest paid compared to Scenario 1, despite similar monthly payments. This highlights the importance of understanding total cost, not just the monthly figure.

You can use various online car loan calculators to get more precise estimates based on your specific figures. Sites like Bankrate or Edmunds offer excellent tools for this.

Budgeting for a $30,000 Car Loan: Beyond the Monthly Payment

Securing a $30,000 car loan is only one part of the equation. True car affordability means you can comfortably manage all associated costs without straining your finances.

The "20/4/10" Rule of Thumb

This popular guideline suggests:

- 20% down payment: This helps reduce your financed amount and monthly payments.

- 4-year (48-month) loan term: This minimizes interest paid and prevents you from being upside down on your loan for too long.

- 10% of your gross monthly income: This is the maximum you should spend on your car payment, including insurance.

While a good starting point, this rule can be flexible. However, it’s a solid benchmark for responsible budgeting for a car.

The True Cost of Car Ownership

Your monthly car payment is just one piece of the puzzle. Don’t forget these essential ongoing expenses:

- Car Insurance: This can be a significant cost, varying widely based on your age, driving record, location, and the vehicle itself. Get insurance quotes before finalizing your purchase.

- Fuel: Consider your daily commute and current gas prices. A more fuel-efficient car can save you hundreds annually.

- Maintenance and Repairs: Even new cars require routine maintenance (oil changes, tire rotations). Older or more complex vehicles might have higher repair costs.

- Registration and Inspections: Annual fees vary by state.

- Parking Fees/Tolls: If applicable to your daily routine.

Based on my experience, many buyers underestimate the cumulative impact of these hidden costs of car ownership. Always factor them into your overall budget to avoid financial surprises.

Strategies to Secure Favorable $30,000 Car Loan Terms

Getting the best deal on your 30000 dollar car loan payments requires proactive steps and smart planning.

- Improve Your Credit Score: This is foundational. Pay bills on time, reduce credit card debt, and avoid opening new lines of credit just before applying for a car loan.

- Save for a Larger Down Payment: As discussed, this significantly reduces your borrowing cost and monthly burden.

- Shop Around for Lenders: Don’t just accept the first offer, especially from the dealership. Get pre-approved by several banks and credit unions before you even visit a car lot. Credit unions often offer highly competitive rates.

- Get Pre-Approved: A pre-approval gives you a concrete loan offer (including rate and maximum amount) before you start shopping. This transforms you into a cash buyer, giving you significant negotiating power at the dealership.

- Negotiate the Car Price Separately: First, agree on the vehicle’s purchase price. Then, discuss financing. Don’t let them combine these negotiations, as it can make it harder to see where you might be overpaying.

- Consider a Co-signer: If your credit isn’t perfect, a co-signer with excellent credit can help you qualify for better rates. However, understand that the co-signer is equally responsible for the loan, which carries significant risk for them.

Common Mistakes to Avoid When Financing a $30,000 Car

As an expert blogger, I’ve seen countless individuals make preventable errors during the car financing process. Here are some of the most frequent pitfalls:

- Focusing Only on Monthly Payments: This is perhaps the biggest mistake. A low monthly payment can hide a higher interest rate or an excessively long loan term, leading to a much higher total cost. Always ask for the total cost of the loan.

- Not Getting Pre-Approved: Without a pre-approval, you’re negotiating blind. The dealership holds all the cards.

- Extending the Loan Term Too Much: While it lowers payments, it dramatically increases total interest and the risk of negative equity.

- Skipping a Down Payment: While possible, it’s almost always financially detrimental. It increases your payments, interest, and risk.

- Ignoring Additional Costs: Sales tax, registration, and other fees can quickly add up, turning a $30,000 car into a $32,000 or $33,000 financing need.

- Buying More Car Than You Can Afford: It’s easy to get caught up in the excitement, but stick to your budget. The stress of high payments can quickly overshadow the joy of a new car.

- Not Reading the Fine Print: Always thoroughly review your loan agreement before signing. Understand all terms, conditions, and fees.

What if Your Credit Isn’t Perfect for a $30,000 Car Loan?

If your credit score isn’t in the excellent or good range, securing a $30,000 car loan might be more challenging or come with less favorable terms. However, it’s not impossible.

- Subprime Loans: Some lenders specialize in loans for individuals with lower credit scores. Be prepared for significantly higher interest rates, which can drastically increase your 30000 dollar car loan payments.

- Building Credit First: If you can wait, taking time to improve your credit score can save you a substantial amount in interest. Consider a secured credit card or a credit-builder loan.

- Consider a Less Expensive Vehicle: A $20,000 or $25,000 car will result in smaller loan payments and potentially open up better financing options with your current credit.

- Secured Loans: Some lenders might offer a secured loan where the car itself acts as collateral.

- Co-signer: As mentioned, a co-signer with good credit can significantly improve your chances and terms.

Refinancing Your $30,000 Car Loan: A Second Chance at Better Terms

Even after you’ve secured your initial auto loan, the journey doesn’t have to end there. Refinancing your $30,000 car loan can be a smart move in certain situations.

When Refinancing Makes Sense:

- Your Credit Score Has Improved: If you’ve diligently worked on your credit since purchasing the car, you might qualify for a lower interest rate now.

- Interest Rates Have Dropped: General market rates for auto loans might have decreased since you took out your original loan.

- You Want a Lower Monthly Payment: Refinancing to a longer term (with caution) or a lower interest rate can reduce your monthly outflow.

- You Want to Shorten Your Loan Term: If you find yourself with more disposable income, you could refinance to a shorter term to pay off the car faster and save on total interest.

How to Refinance:

Shop around with different lenders, just like you did for your original loan. Compare offers, looking at the new interest rate, term, and any associated fees. Make sure the savings outweigh the costs.

Pro Tips from Us for Your Next Car Purchase

Based on years of observing the auto industry and helping individuals make informed financial decisions, here are some final pieces of advice:

- The Power of Research: Knowledge is your greatest asset. Research vehicles, compare prices, and understand financing options before you step onto a dealership lot. This article is a great starting point, and for more general car buying advice, you might find our guide on Smart Car Buying Strategies helpful.

- Get Your Ducks in a Row: Have your credit report reviewed, your budget established, and pre-approvals in hand.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, or if the numbers don’t add up, be prepared to leave. There’s always another car and another dealership.

- Consider Total Cost of Ownership: Beyond 30000 dollar car loan payments, think about insurance, maintenance, and fuel. For insights into managing one of these major expenses, you could check out our post on Understanding Car Insurance Costs.

- Understand Depreciation: Cars lose value over time. Factor this into your decision, especially if you plan to trade in or sell the car within a few years.

Conclusion: Driving Away with Confidence

Understanding 30000 dollar car loan payments is more than just knowing a monthly figure; it’s about grasping the interconnected financial components that make up the total cost of your vehicle. By paying close attention to interest rates, loan terms, down payments, and your credit score, you can significantly influence your financial outcome.

Armed with this in-depth knowledge, you’re now better equipped to make a truly informed decision. Don’t let the excitement of a new car overshadow the importance of sound financial planning. Do your homework, ask the right questions, and secure a car loan that puts you on the road to financial success, not stress. Start your research today and drive away with confidence!