Navigating the Road to a New Ride: Your Ultimate Guide to Pre-Approved Car Loans with Poor Credit

Navigating the Road to a New Ride: Your Ultimate Guide to Pre-Approved Car Loans with Poor Credit Carloan.Guidemechanic.com

Dreaming of a new car, but a less-than-stellar credit score has you pumping the brakes? You’re not alone. Many individuals face the challenge of securing vehicle financing when their credit history isn’t perfect. The good news? A "pre-approved car loan poor credit" isn’t just a hopeful phrase; it’s a very real possibility. This comprehensive guide will demystify the process, offering actionable strategies and expert insights to help you drive away in the car you need.

Based on my extensive experience in the financial and automotive sectors, understanding pre-approvals, especially with a challenging credit history, is your most powerful tool. It transforms you from a hopeful applicant into a confident buyer. Let’s unlock the secrets to making it happen.

Navigating the Road to a New Ride: Your Ultimate Guide to Pre-Approved Car Loans with Poor Credit

What Exactly is a Pre-Approved Car Loan, and Why Does it Matter for Poor Credit?

Before diving into the specifics of poor credit, let’s establish a clear understanding of what a pre-approved car loan entails. Simply put, a pre-approval is a conditional offer from a lender stating how much they are willing to lend you for a car, at what interest rate, and for what term. This offer is based on a preliminary review of your financial information.

It’s crucial to understand that it’s not a final loan agreement, but it’s a significant step. Think of it as getting a "green light" from a lender before you even set foot in a dealership. They’ve assessed your creditworthiness, even with a lower score, and have given you an estimate of what you can borrow.

The Power of Pre-Approval for Those with Less-Than-Perfect Credit

For individuals navigating the car buying journey with poor credit, a pre-approval carries even greater weight. It shifts the dynamics of the entire process in your favor.

Here’s why it’s so beneficial:

- Clarity on Your Budget: You’ll know your maximum loan amount and estimated monthly payments upfront. This prevents you from falling in love with a car outside your financial reach.

- Confidence in Negotiation: Walking into a dealership with a pre-approval is like having cash in hand. You’re a serious buyer, and this empowers you to negotiate the car’s price more effectively. You’re buying a car, not a loan.

- Avoiding Unnecessary Credit Checks: Many dealerships might run your credit multiple times, which can further ding your score. With a pre-approval, you minimize these "hard inquiries" because you already have a financing option secured.

- Focusing on the Car, Not Just the Loan: Your primary concern can be finding the right vehicle that fits your needs, rather than desperately seeking a loan approval. This reduces stress and helps you make a more informed decision.

- Spotting Bad Deals: You’ll have a benchmark interest rate and terms from your pre-approval. This makes it easier to identify if a dealership’s financing offer is genuinely better or if they’re trying to push you into a less favorable deal.

The Reality of Poor Credit and Car Loans: What to Expect

Let’s be candid: securing a car loan with poor credit presents unique challenges. Your credit score is a numerical representation of your creditworthiness, reflecting your history of borrowing and repayment. A low score signals higher risk to lenders.

How "Poor Credit" Impacts Your Loan Terms

When you have poor credit, lenders often compensate for the increased risk in several ways:

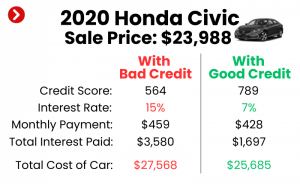

- Higher Interest Rates (APR): This is the most significant impact. Lenders charge more interest to offset the perceived higher chance of default. A higher APR means you’ll pay significantly more over the life of the loan.

- Shorter Loan Terms: Lenders might prefer shorter repayment periods. While this means higher monthly payments, it reduces the overall risk for them.

- Lower Loan Amounts: You might be approved for a smaller maximum loan amount compared to someone with excellent credit.

- Requirement for a Down Payment: A substantial down payment often becomes non-negotiable. This reduces the loan amount and shows the lender your commitment.

- Co-Signer Requirement: Some lenders might require a co-signer with good credit to mitigate their risk.

It’s important to define "poor credit" in this context. Generally, a FICO score below 580 is considered "poor," while scores between 580-669 are often labeled "fair" or "subprime." While challenging, neither category makes obtaining a car loan impossible, especially with a strategic approach.

Strategies to Secure a Pre-Approval with Poor Credit

Securing a pre-approved car loan with poor credit requires preparation and a targeted approach. This isn’t about magic; it’s about presenting yourself as the most responsible borrower possible, despite past financial hiccups.

1. Preparing Your Finances: Laying the Groundwork

Before you even think about applying, take these crucial steps to strengthen your position.

- Check Your Credit Report (and Fix Errors): This is non-negotiable. Obtain your credit reports from all three major bureaus (Equifax, Experian, Transunion) through AnnualCreditReport.com. Review them meticulously for any inaccuracies. Disputing and correcting errors can potentially boost your score quickly.

- Pro tip from us: Many people skip this step, but even a single incorrect late payment or an account you don’t recognize can significantly drag down your score. Cleaning it up is often the fastest way to see improvement.

- Save for a Down Payment: A significant down payment is your best friend when you have poor credit. It reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your financial commitment and ability to save. Aim for at least 10-20% of the car’s price, if possible.

- Common mistakes to avoid are underestimating the power of a down payment. Even a few thousand dollars can make a substantial difference in approval odds and interest rates.

- Budget and Understand Your Debt-to-Income (DTI) Ratio: Lenders look at your DTI ratio – your total monthly debt payments divided by your gross monthly income. A high DTI indicates you might be overextended. Create a realistic budget to ensure you can comfortably afford the car payment alongside your other expenses. Lenders prefer a DTI below 43%, though some subprime lenders might go higher.

2. Finding the Right Lenders: Where to Look

Not all lenders are created equal, especially when it comes to poor credit. You need to target lenders who specialize in or are more open to working with individuals in your situation.

- Specialized Bad Credit Lenders: These lenders specifically cater to borrowers with low credit scores. They understand the challenges and often have more flexible criteria, though their interest rates will likely be higher. Online searches for "bad credit car loans" will reveal many options.

- Credit Unions: Don’t overlook local credit unions. They are member-owned and often more willing to work with members who have less-than-perfect credit, sometimes offering more favorable terms than traditional banks. They prioritize member relationships.

- Online Lenders and Marketplaces: Many online platforms specialize in connecting borrowers with various lenders, including those who work with poor credit. These can be great for comparing multiple offers quickly without multiple hard inquiries. Examples include LendingTree, Carvana, or specialized bad credit auto loan sites.

- Dealership Financing (Use with Caution): While dealerships can offer financing, it’s often through their network of lenders. It’s usually best to get a pre-approval elsewhere first. Why? Because you’ll have a benchmark. If you walk in without one, you’re at their mercy.

- Pro tips from us: If a dealership insists on running your credit with multiple lenders, try to limit it to a short period (e.g., 14-45 days). Multiple inquiries within this window are typically treated as a single inquiry by credit bureaus for rate shopping purposes.

3. Strengthening Your Application: Presenting Your Best Self

Even with poor credit, you can make your application more appealing.

- Consider a Co-Signer: If you have a trusted family member or friend with excellent credit who is willing to co-sign, this can significantly improve your chances of approval and secure a better interest rate. A co-signer takes on equal responsibility for the loan, so ensure they understand the commitment.

- Common mistakes to avoid are asking someone to co-sign without fully explaining the risks and responsibilities involved. This can strain relationships.

- Provide Proof of Stable Income and Employment: Lenders want assurance that you can make payments. Provide clear documentation of consistent income (pay stubs, tax returns, bank statements) and a stable employment history. Longevity in your job is a strong positive signal.

- Show Responsible Payment History (Even on Other Bills): While your credit score reflects past issues, you can highlight current responsible behavior. If you’ve consistently paid rent, utilities, or other non-credit-reporting bills on time, gather evidence. Some alternative data lenders might consider these.

The Pre-Approval Process Step-by-Step

Once you’ve prepared your finances and identified potential lenders, the pre-approval process itself is relatively straightforward.

- Application Submission: You’ll fill out an application form, either online or in person. This will ask for personal details, employment history, income, and housing information.

- Required Documents: Be ready to provide documentation. This typically includes:

- Proof of identity (driver’s license, social security card)

- Proof of income (pay stubs, W-2s, tax returns, bank statements)

- Proof of residence (utility bill, lease agreement)

- Sometimes, bank account information

- Soft vs. Hard Credit Inquiry: Most pre-approval processes start with a "soft inquiry," which doesn’t affect your credit score. If you proceed with a full application, the lender will perform a "hard inquiry," which will temporarily lower your score by a few points.

- Understanding the Offer: If approved, you’ll receive an offer detailing:

- Maximum Loan Amount: The highest amount you can borrow.

- Annual Percentage Rate (APR): Your interest rate, crucial for calculating total cost.

- Loan Term: The length of time you have to repay (e.g., 48, 60, 72 months).

- Estimated Monthly Payment: Based on the above factors.

Read this offer carefully. Understand every line item. Don’t hesitate to ask questions.

Common Mistakes to Avoid & Pro Tips for Success

Even with a pre-approval in hand, the journey isn’t over. Avoiding common pitfalls can save you money and stress.

- Mistake 1: Accepting the First Offer: Just because you got a pre-approval doesn’t mean it’s the best offer. Apply to 2-3 different lenders who specialize in "pre approved car loans poor credit" to compare terms. This is why the "soft inquiry" phase is so valuable.

- Mistake 2: Applying Everywhere (Indiscriminately): While comparing is good, avoid submitting full applications to too many lenders in a short period. Multiple hard inquiries can negatively impact your credit score. Stick to a few targeted applications within a concentrated timeframe (typically 14-45 days, as mentioned).

- Mistake 3: Buying More Car Than You Can Afford: Your pre-approval states the maximum you can borrow, not necessarily what you should borrow. Factor in insurance, maintenance, fuel, and registration costs. A common mistake is getting caught up in the excitement and overspending, leading to financial strain.

- Based on my experience: Many people regret a high car payment more than almost any other debt. Be realistic about your budget.

- Mistake 4: Not Reading the Fine Print: Understand all fees, prepayment penalties, and specific terms of your loan. Don’t rush through the documents.

Pro Tips for Long-Term Success:

- Improve Your Credit Score Before Applying: Even small improvements can make a difference. Paying down existing debts, making all payments on time, and keeping credit utilization low can help. Check out for more in-depth advice.

- Understand the Total Cost of the Loan: Focus not just on the monthly payment, but on the total interest paid over the life of the loan. A lower monthly payment over a longer term often means significantly more interest paid.

- Be Patient: Getting a "pre approved car loan poor credit" might take a little more effort and time, but it’s worth it to secure favorable terms. Rushing can lead to costly mistakes.

- Consider a Used Car: If your credit is poor, a reliable used car is often a more financially sound choice than a brand-new vehicle. New cars depreciate rapidly, and the higher interest rates on bad credit loans compound this effect.

After Pre-Approval: Buying Your Car with Confidence

Once you have your pre-approval letter, you’re in the driver’s seat.

- Shop Like a Cash Buyer: Armed with your pre-approval, you can focus purely on the car’s price. You know your financing is already sorted.

- Still Compare Dealership Offers: Even with a pre-approval, always ask the dealership about their financing options. Sometimes, they might have a special promotion or a lender they work with who can beat your pre-approval rate. If they can’t, you have your pre-approval as a solid fallback.

- Finalizing the Loan: Once you’ve chosen your car and agreed on a price, you’ll finalize the loan paperwork with your chosen lender (either your pre-approved lender or the dealership’s lender if their offer is better).

Conclusion: Your Journey to a Car Loan with Poor Credit is Achievable

Securing a "pre approved car loan poor credit" is not just a pipe dream; it’s an achievable goal with the right approach. It requires preparation, diligent research, and a clear understanding of your financial standing. By checking your credit, saving for a down payment, targeting appropriate lenders, and understanding the terms, you can empower yourself to make a smart car-buying decision.

Remember, this isn’t just about getting a car; it’s an opportunity to rebuild your credit history responsibly. Making timely payments on your car loan can significantly improve your credit score over time, opening doors to better financial opportunities in the future. Don’t let a past credit stumble deter you from your present needs. With the insights provided here, you’re well-equipped to navigate the road ahead.

For more information on managing your credit and understanding loans, we recommend visiting a trusted source like the Consumer Financial Protection Bureau (CFPB) at https://www.consumerfinance.gov/. Their resources can provide further guidance on financial literacy.

Ready to take the first step? Start by checking your credit report today! Your new car awaits.