Navigating the Road to a New Ride: Your Ultimate Guide to the Best Car Loans for Average Credit

Navigating the Road to a New Ride: Your Ultimate Guide to the Best Car Loans for Average Credit Carloan.Guidemechanic.com

Finding the right car loan can feel like a daunting journey, especially when your credit score falls into the "average" category. Many people mistakenly believe that having average credit means you’re stuck with sky-high interest rates or limited options. But based on my extensive experience in the financial and automotive sectors, this simply isn’t true. With the right knowledge and strategic approach, securing an affordable car loan with average credit is not only possible but often leads to significant savings.

This comprehensive guide is designed to empower you with all the information you need. We’ll explore what average credit truly means, where to find the most favorable loan terms, and crucial strategies to improve your chances of approval. Our ultimate goal is to help you drive away in your dream car without financial strain, building a stronger credit future in the process.

Navigating the Road to a New Ride: Your Ultimate Guide to the Best Car Loans for Average Credit

Understanding "Average Credit" and Its Impact on Car Loans

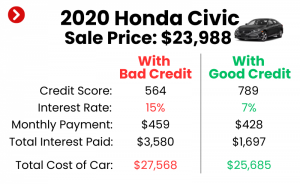

Before we dive into specific loan options, let’s clarify what "average credit" entails. Generally, credit scores range from 300 to 850. While excellent credit scores are typically 740 and above, and good credit falls between 670-739, average or "fair" credit usually lands in the 601-660 FICO score range. Some lenders might extend this slightly higher, up to 680.

It’s important to understand that lenders use your credit score as a primary indicator of your creditworthiness. A higher score signals less risk, often translating to lower interest rates and more flexible terms. Conversely, average credit suggests a moderate risk level. This means lenders might offer slightly higher interest rates compared to someone with excellent credit, but significantly better rates than those with poor credit.

Why Your Credit Score Matters for Car Financing

Your credit score isn’t just a number; it’s a financial snapshot that tells lenders several key things:

- Payment History: Have you paid your bills on time in the past? This is the most significant factor.

- Amounts Owed: How much debt do you currently carry relative to your credit limits?

- Length of Credit History: How long have you had credit accounts open?

- Credit Mix: Do you have a healthy mix of different credit types (e.g., credit cards, student loans, mortgages)?

- New Credit: How many new credit accounts have you recently opened?

For individuals with average credit, lenders often look closely at the details of their credit report. They want to see consistent, albeit not perfect, payment behavior. A history of stable employment and residence can also positively influence their decision, even with an average score.

Laying the Groundwork: Preparing for Your Car Loan Application

Preparation is paramount when seeking the best car loans for average credit. Taking these crucial steps beforehand can significantly improve your odds of approval and help you secure more favorable terms.

1. Know Your Credit Score and Report Inside Out

This is perhaps the most critical first step. You cannot effectively navigate the loan landscape if you don’t know where you stand.

- Get Your Free Reports: You are entitled to a free credit report from each of the three major bureaus (Experian, Equifax, and TransUnion) once every 12 months through AnnualCreditReport.com.

- Review for Accuracy: Carefully examine each report for any errors or discrepancies. Incorrect information, like an account that isn’t yours or an inaccurate late payment notation, could be dragging your score down. Disputing these errors can lead to a quick bump in your score.

- Understand Your Score: Many credit card companies now offer free access to your FICO or VantageScore. Knowing your exact score helps you set realistic expectations and target appropriate lenders.

- Pro Tip from us: Don’t just look at the number. Read the entire report. Understand why your score is what it is. This insight will guide your strategy moving forward.

2. Craft a Realistic Budget and Stick to It

Before you even start looking at cars, determine how much you can truly afford. This involves more than just the monthly car payment.

- Total Cost of Ownership: Factor in insurance, fuel, maintenance, and potential repairs. These can add hundreds of dollars to your monthly expenses.

- Debt-to-Income (DTI) Ratio: Lenders pay close attention to your DTI ratio, which compares your total monthly debt payments to your gross monthly income. A DTI below 36% is generally considered good, but many lenders prefer it to be even lower for car loans. A high DTI can signal that you’re overextended, even if your credit score is decent.

- Avoid Overextending: Common mistakes to avoid are focusing solely on the lowest possible monthly payment without considering the total cost of the loan, including interest. A longer loan term might mean lower monthly payments, but you’ll pay significantly more in interest over the life of the loan.

3. Save for a Substantial Down Payment

For those with average credit, a larger down payment is your secret weapon.

- Reduces Loan Amount: A bigger down payment directly lowers the amount you need to borrow, which can make your application more attractive to lenders. Less money loaned means less risk for them.

- Lowers Monthly Payments: With a smaller principal, your monthly payments will be more manageable.

- Shows Commitment: Lenders view a significant down payment as a sign of financial responsibility and commitment, which can offset some of the perceived risk associated with an average credit score.

- Reduces Interest Paid: Less principal means less interest accruing over the loan term.

- Based on my experience: Aim for at least 10-20% of the car’s purchase price. The more you put down, the better your chances of securing a favorable interest rate.

4. Understand Your Trade-In Value (If Applicable)

If you have an existing vehicle you plan to trade in, research its market value.

- Online Valuation Tools: Use reputable sites like Kelley Blue Book (KBB.com) or Edmunds.com to get an accurate estimate of your car’s trade-in value.

- Leverage as Down Payment: Your trade-in value can act as part of your down payment, further reducing the amount you need to finance.

- Negotiate Separately: Pro tips from us suggest negotiating your trade-in value and the new car’s price separately from the financing terms. This prevents the dealer from shifting numbers around to their advantage.

Where to Find the Best Car Loans for Average Credit

Now that you’re prepared, let’s explore the most promising avenues for securing a car loan when you have average credit. It’s crucial to shop around and compare offers from various sources.

1. Credit Unions: Often Your Best Bet

Credit unions are non-profit financial institutions owned by their members. This structure often translates to more competitive interest rates and flexible loan terms, especially for individuals with average credit.

- Member-Centric Approach: Unlike traditional banks, credit unions prioritize their members’ financial well-being. They may be more willing to work with you, even if your credit isn’t perfect, especially if you have an existing relationship with them.

- Lower Rates and Fees: They often have lower overhead costs and aren’t driven by shareholder profits, allowing them to offer more attractive rates and fewer fees.

- Personalized Service: You might find a more personalized approach at a credit union, where they take the time to understand your financial situation.

- How to Apply: You typically need to become a member to apply for a loan, which usually involves opening a savings account with a small deposit. Look for local credit unions or those you might be eligible for through your employer or community affiliation.

2. Online Lenders: Convenience and Competitive Offers

The digital landscape has brought forth a multitude of online lenders specializing in auto loans for various credit tiers, including average credit.

- Quick Pre-Approvals: Many online lenders offer fast, online pre-approval processes, often with a soft credit check that won’t impact your score. This allows you to compare offers quickly.

- Diverse Options: You’ll find a wide range of lenders, from those specializing in prime loans to those more comfortable with subprime (which average credit sometimes borders).

- Streamlined Process: The entire application process, from pre-approval to final funding, can often be completed online, making it incredibly convenient.

- Examples: Companies like Capital One Auto Finance, LightStream (a division of Truist Bank), Carvana, and various lending marketplaces can be good starting points.

- Common mistakes to avoid: Not reading the fine print. Ensure you understand all terms and conditions before committing to an online lender, as some might have less flexible customer service if issues arise.

3. Traditional Banks: Leverage Existing Relationships

Your current bank or a large national bank might also be a viable option, especially if you have a long-standing banking relationship.

- Familiarity: Applying with a bank where you already have accounts can sometimes streamline the process, as they already have some insight into your financial history.

- Relationship Benefits: Some banks offer preferential rates to existing customers with good standing.

- Compare Thoroughly: Don’t assume your bank will offer the best rate. Always compare their offer with those from credit unions and online lenders.

4. Dealership Financing: Convenience vs. Cost

Many dealerships offer in-house financing or work with a network of lenders. This can be convenient, as it’s a "one-stop shop" approach.

- Convenience: You can choose your car and arrange financing all in one place.

- Multiple Lenders: Dealerships often partner with various banks and financial institutions, potentially giving you multiple offers to choose from.

- Potential for Markups: Dealers sometimes add a markup to the interest rate offered by the lender, which is how they profit from financing. This means you might pay a higher rate than if you went directly to the lender.

- Pro tips from us: Get pre-approved elsewhere before visiting the dealership. This gives you a benchmark and leverage for negotiation. If the dealership can beat your pre-approval rate, great! If not, you have a solid backup.

5. (Caution!) Buy Here, Pay Here Dealerships: A Last Resort

While these dealerships specifically cater to individuals with poor or no credit, they are generally not the "best" option for average credit and should be considered a last resort.

- High Interest Rates: BHPH dealerships are notorious for extremely high interest rates, often at the maximum legal limit.

- Limited Vehicle Selection: The cars available are typically older, higher mileage, and may have reliability issues.

- Weekly/Bi-Weekly Payments: Payments are often structured on a more frequent basis, which can be challenging for budgeting.

- Based on my experience: If you have average credit, you have far better options available to you. Avoid BHPH dealerships unless every other avenue has been exhausted and you absolutely need a car immediately.

Strategies to Improve Your Chances and Get Better Terms

Even with average credit, there are powerful strategies you can employ to significantly boost your approval odds and secure more favorable loan terms.

1. Get Pre-Approved: Your Ultimate Negotiating Tool

Pre-approval is an absolute game-changer. It means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a particular interest rate.

- Know Your Buying Power: You’ll know exactly how much you can afford before stepping onto a dealership lot.

- Negotiate Like a Cash Buyer: With a pre-approval in hand, you effectively become a cash buyer to the dealership. You can focus on negotiating the car’s price, rather than getting caught up in financing details.

- Compare Offers: Apply for pre-approval with 2-3 different lenders (credit unions, online lenders, banks). This allows you to compare their rates and terms side-by-side. Multiple inquiries within a 14-45 day window for the same type of loan are usually treated as a single hard inquiry, minimizing the impact on your score.

- Internal Link: For a deeper dive into improving your credit score, check out our guide on .

2. Consider a Co-Signer: If Appropriate

A co-signer can significantly strengthen your loan application, especially if your credit is on the lower end of "average."

- Who is a Co-Signer? A co-signer is someone with excellent credit who agrees to take full legal responsibility for the loan if you fail to make payments.

- Benefits: Their strong credit history can help you qualify for a lower interest rate and better terms than you could get on your own.

- Risks: This is a serious commitment for the co-signer. If you miss payments, their credit score will be negatively affected, and they will be legally obligated to repay the debt. Only consider this option with someone you trust implicitly and if you are absolutely confident in your ability to make payments.

3. Opt for Shorter Loan Terms

While longer loan terms (e.g., 72 or 84 months) offer lower monthly payments, they dramatically increase the total interest you’ll pay over the life of the loan.

- Reduce Interest Paid: Shorter terms (e.g., 36 or 48 months) mean higher monthly payments, but you’ll pay significantly less interest overall.

- Faster Equity: You’ll build equity in your car more quickly, reducing the risk of being "upside down" (owing more than the car is worth).

- Based on my experience: If your budget allows, always choose the shortest loan term possible. This is a crucial strategy for saving money with an average credit score.

4. Don’t Be Afraid to Negotiate

Everything is negotiable when buying a car, from the price of the vehicle to the interest rate on your loan.

- Car Price First: Always negotiate the price of the car before discussing financing.

- Leverage Pre-Approval: Use your pre-approved loan offer as leverage to get the dealership to beat or match that rate.

- Walk Away: Be prepared to walk away if you’re not getting a fair deal. There are always other cars and other lenders.

5. Short-Term Credit Improvement Strategies

While improving your credit score takes time, a few quick actions can sometimes give it a small boost before you apply:

- Pay Down Credit Card Balances: Reducing your credit utilization ratio (how much credit you’re using compared to your limits) can have a rapid positive impact.

- Pay All Bills on Time: Ensure all your bills, especially credit card payments, are paid on time for the months leading up to your application.

- Address Minor Errors: As mentioned, disputing small inaccuracies on your credit report can sometimes yield quick results.

Common Mistakes to Avoid When Getting a Car Loan with Average Credit

Even with the best intentions, it’s easy to fall into common traps. Being aware of these pitfalls can save you money and stress.

- Not Checking Your Credit Report: As discussed, this is a fundamental error. Without knowing your credit standing, you’re flying blind.

- Only Applying to One Lender: Limiting yourself to a single lender means you’re missing out on potentially better offers. Always shop around!

- Focusing Solely on the Monthly Payment: This is perhaps the most common mistake. A low monthly payment can mask a very long loan term and a high interest rate, leading to you paying much more in total. Always consider the total cost of the loan.

- Buying More Car Than You Can Afford: It’s tempting to stretch your budget for a fancier model, but this can lead to financial strain down the road. Stick to your budget.

- Falling for Unnecessary Add-Ons: Dealerships often try to sell you extended warranties, paint protection, or other extras. While some might be useful, many are overpriced and can significantly inflate your loan amount. Carefully consider what you truly need.

After You Get the Loan: Building a Better Financial Future

Securing a car loan with average credit isn’t just about getting a new car; it’s an opportunity to build a stronger financial foundation.

- Make Payments On Time, Every Time: This is crucial. Consistent on-time payments will significantly improve your credit score over time, moving you from "average" to "good" or even "excellent."

- Consider Refinancing Down the Road: Once you’ve made 6-12 months of on-time payments and your credit score has improved, you might be eligible to refinance your car loan at a lower interest rate. This can save you a substantial amount of money over the remaining loan term.

- Use This Loan as a Stepping Stone: View this car loan as a tool to demonstrate responsible credit management. A positive payment history on an installment loan is excellent for your credit profile and will help you qualify for better rates on future loans, like mortgages.

- External Link: To understand the specifics of your FICO score and its impact on lending decisions, visit a trusted credit reporting agency’s educational resources, such as FICO.

Conclusion: Drive Confidently with Average Credit

Navigating the world of car loans with average credit doesn’t have to be intimidating. By understanding your credit, preparing thoroughly, exploring all your lending options, and employing smart strategies, you can secure a favorable loan that fits your budget. Remember, every on-time payment you make will not only get you closer to owning your car outright but will also pave the way for a healthier financial future.

Don’t let an average credit score hold you back from getting the vehicle you need. Start your preparation today, compare offers, and drive away knowing you’ve made a smart financial decision. Your journey to a new car, and better credit, begins now!

Internal Link: If you’re unsure about budgeting for a car, our comprehensive article on can provide further assistance.