Navigating the Road to Approval: Your Comprehensive Guide to a 609 Credit Score Car Loan

Navigating the Road to Approval: Your Comprehensive Guide to a 609 Credit Score Car Loan Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is exciting, but for many, the path is paved with questions, especially when it comes to financing. If you’ve recently checked your credit score and found yourself in the 609 range, you might be wondering: "Can I truly get a car loan with a 609 credit score?" The short answer is yes, absolutely! However, the process requires a strategic approach, a good understanding of your financial landscape, and a bit of savvy negotiation.

This isn’t just another article; it’s your definitive guide to understanding, preparing for, and successfully securing a 609 credit score car loan. We’ll delve deep into what a 609 score means for auto financing, uncover the best strategies for approval, and equip you with the knowledge to make informed decisions that benefit your wallet and your credit health. Our goal is to transform what might seem like a hurdle into a manageable step towards driving your next car.

Navigating the Road to Approval: Your Comprehensive Guide to a 609 Credit Score Car Loan

Understanding Your 609 Credit Score: What It Means for Car Loans

A credit score of 609 places you squarely within what’s often referred to as the "fair" or "subprime" credit range. While it’s certainly not in the excellent tier, it’s also a far cry from truly poor credit. This particular score indicates that while you likely have a history of managing credit, there might be some areas that lenders view as higher risk.

For auto lenders, a 609 credit score signals that you could be a moderately risky borrower. They’ll scrutinize your application more closely than someone with a 700+ score. This typically translates into higher interest rates, and potentially stricter loan terms, as lenders aim to offset the perceived increased risk. Don’t let this deter you; it simply means you need to be exceptionally well-prepared and strategic in your approach.

The Lender’s Perspective: Assessing Risk

When a lender evaluates your application for a 609 credit score car loan, they are primarily assessing their risk. They want to know the likelihood of you repaying the loan in full and on time. Your 609 score, while not ideal, tells them you have some credit history, which is better than no history at all.

Based on my experience in the lending industry, lenders will look beyond just the numerical score. They’ll dive into your full credit report to understand the story behind that 609. Are there recent late payments? High credit utilization? A short credit history? These details provide context and influence their decision more than the number alone.

The Reality of Car Loans with a 609 Credit Score

Securing a car loan with a fair credit score is absolutely achievable, but it comes with certain realities you must acknowledge. The most significant difference you’ll encounter compared to those with excellent credit is the interest rate. Lenders price their loans based on risk, and a 609 credit score falls into a higher risk category.

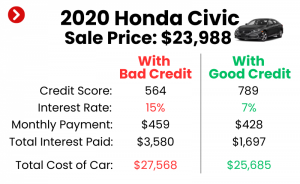

You should prepare for an Annual Percentage Rate (APR) that will be noticeably higher than the national average advertised for prime borrowers. While someone with a 750+ score might qualify for rates under 5%, a borrower with a 609 credit score might see rates anywhere from 8% to 15% or even higher, depending on market conditions, the lender, and other factors in your application. This higher interest rate means you’ll pay more over the life of the loan.

Navigating Potential Hurdles

Common hurdles for applicants seeking a 609 credit score car loan include:

- Higher Down Payment Requirements: Lenders often ask for a larger down payment to reduce their risk.

- Stricter Income Verification: You’ll need solid proof of stable income.

- Limited Vehicle Options: Some lenders might prefer to finance newer, lower-mileage vehicles for higher-risk borrowers.

It’s crucial to understand these realities upfront. This knowledge empowers you to proactively address potential concerns and present yourself as the most favorable borrower possible. Don’t view these as roadblocks, but rather as aspects to strategically navigate.

Key Strategies for Securing a Car Loan with a 609 Credit Score

Approaching the car loan process with a 609 credit score requires a well-thought-out plan. Here are the strategies that, based on my professional experience, significantly increase your chances of approval and help you secure the best possible terms.

1. Know Your Numbers (Beyond Just 609)

Your credit score is just one piece of the puzzle. Before you even step foot in a dealership or apply online, get your full credit report from all three major bureaus (Equifax, Experian, TransUnion). You can do this for free annually at AnnualCreditReport.com.

Review your report meticulously for any errors or inaccuracies. Disputing and correcting these can sometimes give your score a quick boost. Beyond the score, understand your debt-to-income (DTI) ratio, which is your total monthly debt payments divided by your gross monthly income. Lenders use DTI to gauge your ability to take on additional debt. A lower DTI makes you a more attractive borrower.

2. Save for a Substantial Down Payment

This is perhaps the single most impactful strategy for someone seeking a 609 credit score car loan. A significant down payment directly reduces the amount you need to borrow, which in turn lowers the lender’s risk. It also demonstrates your financial commitment and ability to save.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price as a down payment. If you can manage more, do it. A larger down payment can lead to lower monthly payments, better interest rates, and less negative equity in the early stages of your loan. It’s a powerful tool to offset a less-than-perfect credit score.

3. Consider a Co-signer

If you have a trusted family member or friend with excellent credit who is willing to co-sign your loan, this can dramatically improve your chances of approval and secure a better interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

While beneficial, understand the implications. The co-signer’s credit will also be impacted by the loan, and they are legally responsible for the debt if you can’t pay. Ensure both parties fully understand the commitment before pursuing this option. Choose a co-signer carefully, as this decision affects both your financial futures.

4. Explore Different Lender Types

Don’t limit yourself to just one type of lender. Different institutions have varying risk appetites and loan products, especially for those with fair credit.

- Traditional Banks and Credit Unions: While sometimes stricter, if you have an existing relationship (e.g., checking account), they might be more willing to work with you. Credit unions, in particular, are known for their more personalized approach and competitive rates for members.

- Dealership Financing: Many dealerships offer in-house financing or work with a network of lenders, including those specializing in subprime auto loans. They can often streamline the process.

- Online Lenders Specializing in Bad Credit: A growing number of online platforms specifically cater to borrowers with credit scores like 609. They often have quick approval processes and competitive rates tailored to this demographic.

- "Buy Here, Pay Here" Dealerships: These can be a last resort. While they often approve anyone, their interest rates are typically very high, and they may not report payments to all credit bureaus, limiting your ability to rebuild credit. Common mistakes to avoid are jumping into a "Buy Here, Pay Here" loan without exploring all other options due to their predatory potential.

5. Shop Around for Pre-Approval

Getting pre-approved for a car loan before you even start car shopping is a game-changer. It separates the financing from the vehicle selection process, allowing you to focus on each independently. Pre-approval gives you a clear understanding of how much you can borrow, at what interest rate, and for what terms.

This knowledge acts as leverage at the dealership. You walk in as a cash buyer, knowing exactly what financing you’re qualified for. This empowers you to negotiate vehicle prices more effectively, rather than getting caught up in monthly payment figures. Remember that multiple hard inquiries for auto loans within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry, minimizing impact on your score.

6. Be Realistic About the Car

With a 609 credit score car loan, affordability should be your top priority. While that brand-new luxury SUV might be tempting, a more modest, reliable used car is often the smarter choice. New cars depreciate rapidly, and with a higher interest rate, you could quickly find yourself "upside down" on your loan, owing more than the car is worth.

Focus on total cost, not just the monthly payment. A longer loan term (e.g., 72 or 84 months) can lower your monthly payment, but you’ll pay significantly more in interest over time. Aim for a shorter term and a car that truly fits your budget, considering not just the loan payment, but also insurance, fuel, maintenance, and registration.

7. Present Your Case (Be Prepared)

When applying for a loan, especially with a 609 credit score, preparation is key. Gather all necessary documentation beforehand:

- Proof of income (pay stubs, tax returns)

- Proof of residency (utility bills, lease agreement)

- Proof of stable employment (employment verification letter)

- Bank statements

- Valid driver’s license

If you have a legitimate reason for past credit issues (e.g., medical emergency, temporary job loss), be prepared to explain it concisely and positively to the lender. Show that those issues are behind you and that you are now in a stable financial position. This transparency can build trust and demonstrate your commitment to repayment.

Improving Your Credit Score While You Shop (and After)

Even if you’re actively seeking a 609 credit score car loan, there are steps you can take to potentially improve your score in the short term, and certainly for the long term. Every point counts, and a slightly higher score could lead to better terms.

For quick wins, focus on:

- Disputing Errors: As mentioned, check your credit report for inaccuracies and dispute them immediately.

- Paying Down Small Debts: Reducing the balance on a credit card or a small personal loan can quickly lower your credit utilization ratio, which is a significant factor in your score.

- Making All Payments On Time: Even small payments on other debts can demonstrate reliability.

For long-term credit health, commit to consistent on-time payments across all your accounts. Keep your credit utilization low (ideally below 30% on revolving accounts). Over time, these habits will steadily build a stronger credit profile, opening doors to even better financing options in the future, including the opportunity to refinance your car loan for a lower rate. For more detailed strategies on boosting your credit, you might find our guide on (placeholder for internal link 1) incredibly helpful.

Navigating the Loan Agreement: What to Watch For

Once you receive loan offers, it’s crucial to understand every detail of the agreement. Don’t rush through it. This is where many borrowers make costly mistakes.

- Annual Percentage Rate (APR): This is the true cost of borrowing, encompassing the interest rate and certain fees. Compare APRs, not just interest rates. A lower APR means a cheaper loan.

- Loan Term: As discussed, a shorter term means higher monthly payments but less total interest paid. A longer term reduces monthly payments but increases the overall cost. Evaluate what you can comfortably afford without extending the term excessively.

- Fees and Charges: Look out for origination fees, documentation fees, or any other charges tacked onto the loan. These can significantly increase the total amount you pay.

- Prepayment Penalties: While rare in auto loans, some lenders might charge a fee if you pay off your loan early. Always confirm whether such a clause exists. You want the flexibility to refinance or pay off your loan ahead of schedule if your financial situation improves.

Always read the fine print. If anything is unclear, ask questions until you fully understand. For a comprehensive understanding of auto loan terms, the Consumer Financial Protection Bureau (CFPB) offers excellent resources here.

Post-Approval: Building a Stronger Financial Future

Congratulations, you’ve secured your 609 credit score car loan! The journey doesn’t end here; in fact, it’s just beginning. This new loan is a powerful tool for rebuilding and strengthening your credit profile.

Make every single payment on time, every month. Consistent, timely payments are the most effective way to improve your credit score over time. As your score improves, you might be eligible to refinance your car loan for a lower interest rate in 12-18 months, potentially saving you thousands over the life of the loan.

Beyond the loan, commit to smart financial habits. Budget carefully for your car expenses, including fuel, insurance, and maintenance. Avoid taking on additional unnecessary debt. This disciplined approach will not only help you manage your current loan but also pave the way for a healthier financial future. If you need assistance with budgeting, consider checking out our article on (placeholder for internal link 2).

Common Mistakes to Avoid When Seeking a 609 Credit Score Car Loan

Knowing what not to do is just as important as knowing what to do. Based on my observations, these are some common pitfalls that borrowers with fair credit often encounter:

- Not Checking Your Credit Report: Going in blind is a huge disadvantage. You need to know your score and what’s on your report.

- Accepting the First Offer: Never take the first loan offer you receive. Shop around, compare, and use pre-approvals to your advantage.

- Stretching the Loan Term Too Long: While a longer term means lower monthly payments, it drastically increases the total interest paid and the risk of negative equity.

- Buying More Car Than You Can Afford: This is a recipe for financial stress. Stick to your budget, considering all costs, not just the monthly payment.

- Ignoring the Total Cost of Ownership: Beyond the loan, remember to factor in insurance, registration, maintenance, and fuel. These costs add up significantly.

- Falling for Predatory Lenders: Be wary of lenders promising guaranteed approval with no credit check. These often come with exorbitant interest rates and unfavorable terms. If an offer seems too good to be true, it probably is.

Conclusion: Your Road to a Car Loan with a 609 Credit Score is Open

Securing a 609 credit score car loan is not just a possibility; it’s an achievable goal with the right approach. While a fair credit score presents unique challenges, it also offers a valuable opportunity to demonstrate financial responsibility and rebuild your credit. By understanding your score, preparing thoroughly, exploring all your options, and negotiating wisely, you can drive away in a vehicle that meets your needs without breaking the bank.

Remember, this process is about empowerment. You are in control of your financial decisions. Take the time to research, compare offers, and ask questions. With patience, persistence, and the strategies outlined in this guide, you can successfully navigate the complexities of auto financing and set yourself on a path toward a stronger financial future. Your journey starts now – drive confidently!