Navigating the Road to Car Ownership: Your Expert Guide to Very Bad Credit Car Loans

Navigating the Road to Car Ownership: Your Expert Guide to Very Bad Credit Car Loans Carloan.Guidemechanic.com

The open road beckons, but a challenging credit history can often feel like a giant roadblock. Many people dream of the freedom and necessity of owning a car, only to be disheartened by a credit score that seems to slam the door shut on their aspirations. If you’re grappling with very bad credit and need a car loan, know this: your situation is not unique, and solutions do exist.

This comprehensive guide is crafted specifically for you. We’ll demystify the process of securing very bad credit car loans, equip you with expert strategies, and help you navigate the journey with confidence. Our ultimate goal is to empower you to drive away in a reliable vehicle, even when your credit score tells a less-than-perfect story.

Navigating the Road to Car Ownership: Your Expert Guide to Very Bad Credit Car Loans

Unpacking "Very Bad Credit": What It Means for Car Loans

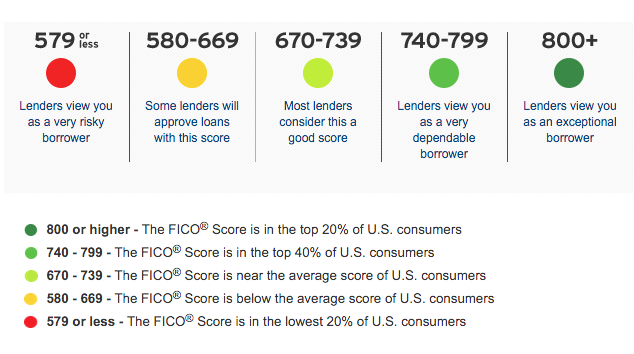

Before we dive into solutions, let’s understand the landscape. What exactly constitutes "very bad credit" in the eyes of an auto lender? Generally, credit scores fall into different ranges, and a score below 580 (on the FICO scale, for example) is typically considered "very poor" or "very bad." This range signifies a higher risk to lenders due to past financial challenges, late payments, defaults, or even bankruptcies.

Based on my experience in the financial sector, many people mistakenly think any credit hiccup automatically puts them in the "very bad" category. While any negative mark impacts your score, "very bad credit" often indicates a more extensive history of financial difficulties. Lenders perceive these scores as a strong indicator of potential future repayment issues, making them more cautious.

It’s crucial to distinguish between simply "bad credit" (often scores between 580-669) and "very bad credit." While both present challenges, the strategies and terms you’ll encounter will differ significantly. The lower your score, the more critical it becomes to present a compelling case for your ability to repay.

Is Getting a Car Loan with Very Bad Credit Really Possible? The Honest Truth

The short answer is yes, getting a car loan with very bad credit is absolutely possible. However, it’s vital to approach this reality with clear eyes and realistic expectations. The market for subprime auto loans is substantial, and many lenders specialize in assisting individuals with challenging credit histories.

Dispelling myths is important here. You might encounter advertisements promising "guaranteed approval car loans" with no strings attached. While approval rates can be high with specialized lenders, there are always underlying conditions. These often include demonstrating a stable income, having a reasonable down payment, or agreeing to higher interest rates. No reputable lender will offer a car loan without some form of financial assessment.

The key is not to get discouraged but to get informed. Understanding the factors lenders prioritize and preparing yourself accordingly will significantly boost your chances. This journey requires patience, thorough research, and a willingness to adapt your expectations.

Key Factors Lenders Consider for Bad Credit Applicants

When evaluating applicants with very bad credit, lenders shift their focus from primarily relying on your credit score to scrutinizing other indicators of your repayment capacity. They’re looking for reasons to say "yes," even if your credit history provides reasons to say "no."

Pro tips from us: Lenders prioritize your ability to repay over almost everything else. Your past credit issues are noted, but your current financial stability is paramount. Focus on demonstrating a strong, consistent ability to make payments.

Here are the critical factors they’ll weigh heavily:

- Stable Income and Employment History: This is perhaps the most significant factor. Lenders want to see consistent, verifiable income. They’ll typically ask for pay stubs, bank statements, or tax returns to confirm your employment and income level. A long, stable employment history at the same job signals reliability.

- Debt-to-Income (DTI) Ratio: Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess if you can comfortably afford additional loan payments. A high DTI might indicate you’re already overextended, regardless of your income.

- Down Payment: A substantial down payment is a game-changer for very bad credit car loans. It reduces the amount you need to borrow, lowers the lender’s risk, and shows your commitment to the purchase. It also often leads to better loan terms.

- Cosigner: Having a creditworthy cosigner can dramatically improve your approval odds and potentially secure better interest rates. A cosigner with good credit essentially guarantees the loan if you default, mitigating the lender’s risk.

- Vehicle Choice: Lenders are often more comfortable financing a less expensive, reliable used car for a bad credit applicant. High-end or brand-new luxury vehicles are usually out of reach until your credit improves. Focus on functionality and affordability.

Each of these elements tells a story about your financial present and future. By strengthening as many of these areas as possible, you present a much more appealing profile to potential lenders.

Strategic Moves: Securing Your Very Bad Credit Car Loan

Securing a car loan with very bad credit requires a strategic approach. It’s not about hoping for the best; it’s about actively improving your position and targeting the right opportunities.

Here are proven strategies to help you get approved:

1. Save for a Significant Down Payment

This cannot be stressed enough. A substantial down payment—ideally 10-20% of the vehicle’s purchase price, or even more—is your most powerful tool. It reduces the loan amount, thereby lowering your monthly payments and the total interest paid. More importantly, it signals to lenders that you are serious about this purchase and have a financial stake in its success.

A larger down payment also decreases the loan-to-value (LTV) ratio, making the loan less risky for the lender. Based on my experience, applicants with very bad credit who offer a solid down payment are often approved when others with similar credit scores are denied. It’s a tangible demonstration of your financial commitment.

2. Find a Reliable Cosigner

If you have a trusted friend or family member with good credit, asking them to cosign your loan can be incredibly beneficial. A cosigner essentially adds their creditworthiness to your application, reassuring the lender that the loan will be repaid. This often leads to approval and better interest rates than you could get on your own.

However, understand the gravity of this decision. A cosigner is legally responsible for the loan if you fail to make payments. Their credit will be impacted if you default, so ensure both parties fully understand the commitment. Choose someone who trusts you implicitly and with whom you have open communication.

3. Proactively Improve Your Credit Score (Even Slightly)

While a complete credit overhaul takes time, you can make small improvements that signal positive change to lenders. Start by checking your credit report for errors and disputing them. Pay down small debts, especially credit card balances, to reduce your credit utilization ratio. Even a few points increase can make a difference.

For more details on improving your credit score, check out our guide on (replace with actual internal link). Showing lenders you are actively working to improve your financial habits can work in your favor.

4. Explore Dealerships Specializing in Bad Credit

Not all dealerships are created equal when it comes to bad credit car loans. Some specialize in working with subprime lenders or offer "buy-here-pay-here" (BHPH) financing. BHPH dealerships act as both the seller and the lender, often approving loans that traditional banks would reject.

While BHPH can be a viable option, be aware that their interest rates are typically much higher, and vehicle choices might be limited. Always compare offers and understand the full terms. Subprime lenders, on the other hand, are third-party lenders who partner with dealerships and are more willing to take on higher-risk borrowers.

5. Research Diverse Loan Options

Don’t limit yourself to just one type of lender. Explore various avenues:

- Credit Unions: Often more flexible and member-focused than traditional banks, credit unions may offer slightly better rates or terms to individuals with challenging credit.

- Online Lenders: Many online platforms specialize in bad credit auto loans. They often have streamlined application processes and can provide multiple offers for comparison.

- Direct Lenders: Some lenders work directly with consumers rather than through dealerships. This can sometimes offer more transparency.

Cast a wide net, but always ensure the lenders are reputable. Common mistakes to avoid are applying everywhere at once, which can negatively impact your credit score through multiple hard inquiries. Instead, pre-qualify with a few select lenders.

6. Be Realistic About Your Vehicle Choice

With very bad credit, your priority should be securing reliable transportation, not a luxury vehicle. Focus on affordable, used cars that meet your essential needs. Lenders are more likely to approve a loan for a lower-priced car because it represents less risk.

Aim for a car that is well within your budget, not just for the monthly payment but also considering insurance, maintenance, and fuel costs. A modest choice now can help you rebuild your credit, opening doors to better vehicles in the future.

The Application Process: What to Expect

Once you’ve done your groundwork, the application process for very bad credit car loans has a few specific steps and considerations. Being prepared can make a world of difference.

- Gather Your Documents: Lenders will require extensive documentation to verify your identity, income, and residence. This typically includes:

- Government-issued ID (driver’s license)

- Proof of residency (utility bill, lease agreement)

- Proof of income (recent pay stubs, bank statements, tax returns if self-employed)

- References (sometimes required by BHPH dealers)

- Proof of insurance (before you drive off the lot)

- Pre-qualification vs. Full Application: Many online lenders and some dealerships offer pre-qualification. This involves a soft credit pull (which doesn’t impact your score) and gives you an idea of what you might be approved for. A full application, however, requires a hard credit inquiry and provides definitive loan offers.

- Understanding the Terms: This is where attention to detail is crucial. Lenders for very bad credit often offer higher interest rates and longer loan terms to make payments more "affordable." Focus on the Annual Percentage Rate (APR), which includes interest and fees, to understand the true cost. Be wary of excessively long loan terms (e.g., 72 or 84 months), as you could end up paying far more than the car is worth over time.

Based on my experience, thorough preparation can significantly speed up the process and prevent last-minute surprises. Have all your documents organized and questions ready before you even step into a dealership or submit an online application.

Navigating High Interest Rates and Loan Terms

It’s a reality that very bad credit car loans come with higher interest rates. This is simply how lenders offset the increased risk associated with your credit profile. While it’s disheartening, understanding why these rates are higher is the first step in managing them.

Pro tips from us: While high interest rates are unavoidable with very bad credit, focus on the long-term goal. Your primary objective with this loan is to establish a positive payment history, which will open doors to better rates in the future.

Here are strategies to mitigate the impact of high interest and long terms:

- Focus on Affordability, Not Just Monthly Payment: A longer loan term might reduce your monthly payment, but it drastically increases the total amount of interest you’ll pay over the life of the loan. Try to negotiate the shortest term you can comfortably afford.

- Make Extra Payments: If financially possible, making even small extra payments can reduce the principal faster, thereby cutting down on the total interest. Even paying bi-weekly instead of monthly can help.

- Refinance Later: This is a key strategy. After 12-18 months of consistent, on-time payments, your credit score should improve. At that point, you may qualify for refinancing at a lower interest rate, significantly reducing your overall cost. This should be a definite goal.

Post-Loan Approval: Building a Better Financial Future

Getting approved for a very bad credit car loan isn’t just about getting a car; it’s a golden opportunity to rebuild and improve your credit score. This loan can be a powerful tool for establishing a positive payment history, which is a cornerstone of a healthy credit profile.

The most critical step is consistent, on-time payments. Every payment you make on time is reported to the credit bureaus, gradually improving your score. It demonstrates financial responsibility and reliability, showing future lenders that you are a lower risk.

- Set Up Payment Reminders: Use calendar alerts, automatic payments, or budgeting apps to ensure you never miss a due date.

- Monitor Your Credit Score: Regularly check your credit score (many banks and credit card companies offer free access). Watch it improve over time as you consistently make payments. This positive feedback can be highly motivating.

- Plan for Refinancing: As mentioned, once your credit improves (typically after 12-18 months of perfect payments), actively seek to refinance your loan. A lower interest rate means more of your payment goes towards the principal, and you save a significant amount of money over the loan’s life.

Common Pitfalls and How to Avoid Them

The journey to securing a very bad credit car loan can have its share of traps. Being aware of these common mistakes will help you navigate the process safely.

- Falling for "Guaranteed Approval" Scams: Be extremely wary of any offer that promises "guaranteed approval" regardless of your credit history without any income or down payment requirements. These are often predatory lenders with exorbitant rates, hidden fees, or unfavorable terms.

- Taking on an Unaffordable Payment: Don’t let the excitement of getting a car overshadow financial prudence. A payment that stretches your budget thin is a recipe for default, further damaging your credit. Always factor in insurance, fuel, and maintenance costs.

- Ignoring the Fine Print: Read every single line of your loan agreement before signing. Understand the interest rate, APR, loan term, any prepayment penalties, and late fees. If something is unclear, ask for clarification.

- Impulse Buying: With limited options, it’s easy to jump at the first car offer. Resist the urge. Take your time to compare vehicles, lenders, and terms. A car is a significant financial commitment, especially with very bad credit.

Common mistakes to avoid are signing without fully understanding the terms and not budgeting for the total cost of car ownership beyond the monthly payment.

Choosing the Right Lender or Dealership

The choice of where you get your loan and car is just as important as the loan itself. For very bad credit car loans, not all lenders or dealerships operate with the same level of transparency or ethical standards.

- Reputation and Reviews: Do your homework. Look up reviews for both the dealership and the specific lender they work with. Check consumer protection websites and the Better Business Bureau.

- Transparency: A reputable lender will be upfront about all costs, terms, and conditions. They won’t pressure you into quick decisions or hide information.

- Ask the Right Questions: Don’t be afraid to ask about the APR, total loan cost, any hidden fees, and options for early payoff or refinancing. A good lender will patiently answer all your queries.

- Compare Offers: Even with very bad credit, try to get at least two or three loan offers to compare. This helps you identify the best available terms and avoid overpaying.

For additional guidance on recognizing and avoiding predatory lending practices, we recommend consulting trusted external sources such as the Consumer Financial Protection Bureau (CFPB) at www.consumerfinance.gov. They offer valuable resources to help consumers make informed financial decisions.

Driving Forward: Your Path to Car Ownership

Securing a car loan with very bad credit might seem like an uphill battle, but it is a journey many successfully complete. This article has equipped you with an in-depth understanding of the process, practical strategies, and crucial insights to navigate the challenges. Remember, the ultimate goal isn’t just to get a car, but to use this opportunity to responsibly manage a loan, rebuild your credit, and pave the way for a more secure financial future.

Start by gathering your documents, assessing your budget, and diligently researching your options. With patience, persistence, and the right approach, you can overcome the hurdle of very bad credit and drive away with the reliable transportation you need. The road ahead may have a few bumps, but with the right preparation, you’re more than capable of navigating them successfully.