Navigating the Road to Financial Freedom: Car Loan Vs. Mortgage – An In-Depth Guide

Navigating the Road to Financial Freedom: Car Loan Vs. Mortgage – An In-Depth Guide Carloan.Guidemechanic.com

Embarking on life’s major purchases often means navigating the complex world of loans. From the exhilarating freedom of a new car to the foundational stability of a home, these acquisitions represent significant milestones. Yet, the financial instruments that enable them – car loans and mortgages – are fundamentally different, each with its own structure, implications, and strategic considerations. Understanding these distinctions isn’t just about comparing interest rates; it’s about making informed decisions that shape your long-term financial health.

As an expert blogger and professional in personal finance, I’ve seen firsthand how a lack of clarity around these essential financial products can lead to missed opportunities or, worse, financial strain. This comprehensive guide aims to demystify the "Car Loan vs. Mortgage" debate, providing you with the in-depth knowledge needed to confidently steer your financial future. We’ll explore their unique characteristics, how they impact your finances, and crucial strategies for leveraging them wisely.

Navigating the Road to Financial Freedom: Car Loan Vs. Mortgage – An In-Depth Guide

Understanding the Basics: What Exactly is a Car Loan?

A car loan, also commonly referred to as an auto loan, is a secured loan specifically designed to finance the purchase of a vehicle. When you take out a car loan, a lender provides you with the funds to buy a car, and in return, you agree to repay that amount, plus interest, over a predetermined period. This period is known as the loan term.

The "secured" aspect is critical here. It means the car itself acts as collateral for the loan. If you fail to make your payments as agreed, the lender has the legal right to repossess the vehicle to recover their losses. This collateralized nature is why car loans are often more accessible than unsecured personal loans, as the lender’s risk is mitigated.

Based on my experience, many first-time car buyers overlook the full scope of what a car loan entails. It’s not just about the monthly payment; it’s about the total cost over the loan’s lifetime, including interest, and how quickly the asset you’re financing depreciates. A car loan is essentially a debt instrument that allows you to drive a car today while paying for it over several years, typically ranging from three to seven years.

Understanding the Basics: What Exactly is a Mortgage?

A mortgage, on the other hand, is a much larger and more complex financial commitment, specifically used to finance the purchase of real estate – primarily a home. Like a car loan, a mortgage is also a secured loan, but the collateral in this case is the property itself. If you default on your mortgage payments, the lender can initiate foreclosure proceedings to take ownership of your home.

The sheer scale and duration of a mortgage set it apart. Mortgage terms commonly span 15, 20, or even 30 years, reflecting the substantial investment involved in homeownership. Beyond the principal loan amount and interest, mortgage payments often include other components like property taxes and homeowners insurance, which are collected by the lender and held in an escrow account. This consolidated payment simplifies financial management for the homeowner.

Pro tips from us: always factor in closing costs and other upfront expenses when considering a mortgage, not just the monthly payment. These can add tens of thousands to your initial outlay. A mortgage is a powerful tool for building long-term wealth and stability, allowing individuals and families to acquire a significant asset that can appreciate in value over time.

The Fundamental Differences: A Side-by-Side Comparison

While both car loans and mortgages are secured debts, their core characteristics diverge significantly, impacting everything from your monthly budget to your long-term financial growth. Understanding these distinctions is paramount for strategic financial planning.

Collateral: Depreciating Asset vs. Appreciating Asset

One of the most profound differences lies in the nature of the collateral securing each loan. For a car loan, your vehicle serves as collateral. The challenge here is that cars are generally depreciating assets; their value typically decreases rapidly from the moment they leave the dealership lot. This means that for much of your car loan term, you might owe more on the car than it’s actually worth, a situation known as being "upside down" or having negative equity.

Conversely, with a mortgage, your home is the collateral. Real estate, historically, has been an appreciating asset. While market fluctuations occur, homes generally increase in value over the long term. This appreciation, combined with your principal payments, allows you to build equity in your home. Equity represents the portion of your home that you truly own, free and clear of the mortgage. This distinction between a rapidly depreciating car and a potentially appreciating home forms the bedrock of their differing financial implications.

Loan Amount and Term: Scale and Duration

The typical loan amounts and terms for car loans and mortgages vary dramatically. Car loans are usually for smaller sums, ranging from a few thousand to tens of thousands of dollars. Their repayment terms are also much shorter, generally between 3 to 7 years. This shorter term means higher monthly payments relative to the loan amount but a quicker path to debt freedom.

Mortgages, on the other hand, involve significantly larger sums, often hundreds of thousands or even millions of dollars. To make these large amounts manageable, mortgage terms are extended over much longer periods, commonly 15, 20, or 30 years. This extended duration results in lower monthly payments compared to what they would be on a shorter term, but it also means paying interest over a much longer timeframe.

Interest Rates: Factors and General Trends

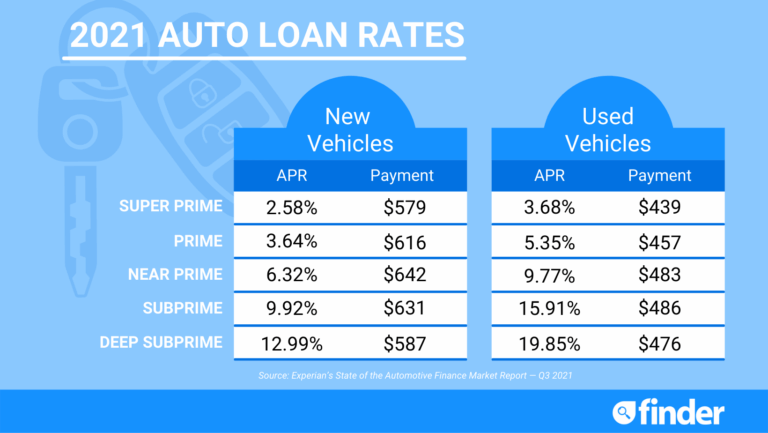

Interest rates for both types of loans are influenced by various factors, including your credit score, the overall economic environment, and the specific lender. However, there are some general trends. Car loan interest rates can vary widely but are often slightly higher than mortgage rates for borrowers with excellent credit, partly due to the car’s depreciating nature and the shorter loan term.

Mortgage interest rates, particularly for conventional 30-year fixed-rate mortgages, are a cornerstone of the economy. They tend to be highly sensitive to economic indicators and Federal Reserve policy. While specific rates fluctuate, mortgages generally offer some of the lowest interest rates available for secured debt, reflecting the lower risk profile associated with a long-term, appreciating asset.

Impact on Credit Score: A Shared Foundation

Both car loans and mortgages play a significant role in building and impacting your credit score. Successfully managing either type of loan by making on-time payments consistently will positively contribute to your credit history, payment history being the largest factor in credit scoring. Conversely, missed payments or defaults can severely damage your credit score, affecting your ability to secure future loans or favorable rates.

The long duration and substantial nature of a mortgage often have a more pronounced impact on your credit history over time, as it demonstrates a sustained ability to manage a large debt responsibly. Both, however, are major credit-building opportunities if handled correctly.

Down Payment: Initial Investment Requirements

While it’s possible to secure a car loan with no money down, making a down payment on a vehicle is always advisable. A larger down payment reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid. It also helps prevent you from being upside down on your loan if the car depreciates quickly.

For mortgages, a down payment is almost always expected and often required. While some programs allow for down payments as low as 3.5% or even 0% (for specific VA or USDA loans), a traditional down payment of 20% or more is often recommended. This larger down payment helps you avoid Private Mortgage Insurance (PMI), which is an additional monthly cost, and significantly reduces your monthly mortgage payment.

Equity: Wealth Building vs. Rapid Loss

The concept of equity is where the financial paths of car loans and mortgages truly diverge. With a mortgage, every principal payment you make, combined with any appreciation in your home’s value, builds equity. This equity is a tangible asset you own, which can be borrowed against later (through a home equity loan or line of credit) or realized when you sell the property. Building home equity is a primary driver of long-term wealth for many individuals.

In contrast, a car loan offers very limited, if any, equity-building potential. Because cars depreciate so rapidly, especially in the initial years, the principal you pay down often barely keeps pace with the vehicle’s loss in value. You’re essentially paying for the use of an asset that is quickly losing its worth, making car ownership more of a liability than an asset for wealth accumulation.

Amortization: The Payment Structure

Both car loans and mortgages are typically amortized loans, meaning your payments are structured to pay off both principal and interest over the loan term. However, the exact breakdown differs. In the early years of a mortgage, a much larger portion of your payment goes towards interest, with only a small fraction reducing the principal. As the loan matures, this ratio gradually shifts, with more going towards principal repayment.

For car loans, while the same principle applies, the shorter term means you often start paying down a more significant chunk of the principal earlier in the loan’s life, relative to the total amount. Nevertheless, the initial payments still heavily favor interest. Understanding amortization helps you see how much of your hard-earned money is truly reducing your debt versus just covering the cost of borrowing.

Key Factors Influencing Both Loans

While the specifics differ, several fundamental financial factors universally influence both car loans and mortgages, determining your eligibility and the terms you receive. Mastering these elements is crucial for securing the best possible rates and terms.

Credit Score: The Ultimate Financial Report Card

Your credit score is arguably the most significant factor lenders consider for both car loans and mortgages. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher credit score (typically FICO scores above 740) signals to lenders that you are a reliable borrower, leading to lower interest rates and more favorable loan terms.

For mortgages, an excellent credit score can translate into savings of tens of thousands of dollars over the life of the loan. For car loans, it can be the difference between a low-single-digit interest rate and a double-digit one. Regularly monitoring and improving your credit score is a continuous financial best practice that pays dividends across all lending products.

Debt-to-Income Ratio (DTI): Assessing Your Capacity

Your Debt-to-Income (DTI) ratio is another critical metric lenders use to assess your ability to manage monthly payments and repay debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. Lenders use DTI to determine how much additional debt you can realistically handle.

While DTI thresholds can vary by lender and loan type, a generally accepted guideline is to aim for a DTI of 36% or less, though some mortgage programs allow for higher DTIs. For mortgages, lenders scrutinize DTI very closely because of the long-term commitment. For car loans, while important, the shorter term and smaller amount might allow for slightly more flexibility, but a high DTI will still raise red flags.

Down Payment: Reducing Risk, Increasing Savings

The size of your down payment directly impacts the loan amount, your monthly payments, and the total interest paid. A larger down payment reduces the lender’s risk, often qualifying you for better interest rates. For car loans, a substantial down payment can prevent you from being underwater on your loan due to rapid depreciation.

For mortgages, a 20% down payment is often the benchmark, as it typically eliminates the need for private mortgage insurance (PMI), a costly monthly expense. Even a slightly larger down payment can save you thousands over the life of a mortgage. Pro tips from us: always prioritize saving for a significant down payment for a home, as its financial benefits are immense and long-lasting.

Loan Term: The Balance of Payment vs. Total Cost

The loan term, or repayment period, is a crucial decision that impacts both your monthly payment and the total cost of the loan. A shorter loan term means higher monthly payments but significantly less interest paid over the life of the loan. This is because you’re paying off the principal more quickly, giving interest less time to accrue.

Conversely, a longer loan term results in lower monthly payments, making the debt more affordable on a month-to-month basis. However, this convenience comes at a cost: you’ll pay substantially more in total interest over the life of the loan. This trade-off is particularly pronounced with mortgages due to their extended duration. Careful consideration of your budget and financial goals is essential when choosing a loan term.

Interest Rates: The Cost of Borrowing

The interest rate is the percentage charged by the lender for the use of their money. It’s the primary "cost of borrowing" and significantly impacts your total repayment amount. Even a seemingly small difference in interest rates can translate into thousands of dollars in savings or extra costs over the life of a loan, especially for a large, long-term mortgage.

Mortgages often offer both fixed-rate and adjustable-rate options. A fixed-rate mortgage ensures your interest rate and principal/interest payment remain constant for the entire loan term, providing predictability. An adjustable-rate mortgage (ARM) starts with a lower rate for an initial period, then adjusts periodically based on market indexes, introducing an element of risk and uncertainty. Car loans are almost exclusively fixed-rate, offering consistent payments.

Strategic Financial Planning: When to Prioritize One Over the Other

Understanding the mechanics of car loans and mortgages is one thing; knowing how to strategically prioritize them within your broader financial plan is another. This requires a holistic view of your financial goals and current situation.

Financial Goals: Short-Term Needs vs. Long-Term Wealth

Your overarching financial goals should dictate your approach to these loans. A car loan often serves a more immediate, functional need: reliable transportation for work, family, or personal use. While important, it’s generally a short-term financial commitment compared to a mortgage.

A mortgage, on the other hand, is typically a long-term investment aligned with wealth building, establishing roots, and potentially securing a significant appreciating asset. If your primary goal is to build long-term wealth and stability, prioritizing homeownership and managing your mortgage effectively often takes precedence over excessive car debt.

Budgeting & Cash Flow: Managing Monthly Commitments

Effective budgeting is non-negotiable when considering either loan. Before committing, meticulously assess how the monthly payments for a car loan or mortgage will fit into your overall budget. Remember that both come with additional costs beyond the principal and interest – car insurance, fuel, maintenance for a car; property taxes, homeowners insurance, and maintenance for a home.

Pro tips from us: use a conservative estimate for your budget. Don’t stretch yourself to the absolute limit, especially with a mortgage. Having a comfortable buffer in your monthly cash flow is crucial for financial resilience, allowing you to absorb unexpected expenses without jeopardizing your loan payments.

Wealth Building: Leveraging Assets and Liabilities

From a wealth-building perspective, the mortgage generally stands out as a more potent tool. While a car is a necessity for many, it’s typically a liability that depreciates. Its primary function is utility, not investment growth.

A home, however, is often considered a cornerstone of wealth. It provides shelter, can appreciate in value, and allows you to build equity over time. This equity can later be leveraged for other financial goals. When considering debt, it’s wise to weigh which loans are financing assets that build wealth versus those that finance rapidly depreciating liabilities.

Refinancing: Opportunities for Optimization

Both car loans and mortgages can potentially be refinanced, offering opportunities to optimize your financial situation. Refinancing a car loan might involve securing a lower interest rate, reducing your monthly payment, or changing the loan term. This can be beneficial if your credit score has improved or if market rates have dropped since you initially took out the loan.

Mortgage refinancing is a more common and often more impactful strategy. Homeowners frequently refinance to obtain a lower interest rate, reduce their monthly payment, convert an adjustable-rate mortgage to a fixed-rate one, or tap into their home equity. Each refinancing decision should be carefully evaluated against the associated costs and your long-term financial objectives.

The "Why" Behind the Comparison: Making Informed Decisions

Understanding the nuances between a car loan and a mortgage isn’t merely an academic exercise; it’s a fundamental aspect of sound personal finance and debt management. The "why" behind this deep dive is to empower you with the knowledge to make truly informed decisions that align with your financial goals and improve your overall financial well-being.

Ignoring these differences can lead to common mistakes. For instance, prioritizing an expensive car with a long loan term might significantly hinder your ability to save for a down payment on a home. Similarly, misunderstanding the impact of interest rates can cost you thousands of dollars over the life of either loan.

Based on my experience, many people get caught up in the excitement of a new purchase and overlook the long-term financial implications. This comparison illuminates the distinct roles these loans play in your financial ecosystem, encouraging a more strategic approach to borrowing. It’s about seeing beyond the monthly payment and recognizing the bigger picture of asset building, debt reduction, and financial freedom.

Pro Tips for Navigating Car Loans and Mortgages

Navigating the lending landscape requires a proactive and informed approach. Here are some expert tips to help you secure the best terms and manage your loans effectively:

- Get Pre-Approved: For both car loans and mortgages, getting pre-approved provides clarity on how much you can borrow and at what interest rate. This empowers you to shop for your car or home with confidence and a clear budget.

- Shop Around for Rates: Don’t just accept the first offer. Check rates from multiple lenders – banks, credit unions, and online lenders. Even a quarter-point difference in an interest rate can save you significant money over the loan’s term, especially with a mortgage.

- Understand All Terms and Conditions: Before signing any document, thoroughly read and understand every clause. Pay attention to prepayment penalties, late fees, and any hidden charges. If something is unclear, ask for clarification.

- Boost Your Credit Score: A higher credit score is your ticket to lower interest rates. Make sure your credit report is accurate, pay bills on time, and keep credit utilization low. For more insights into improving your credit score, check out our guide on .

- Prioritize Down Payments: While not always mandatory, a larger down payment reduces your loan amount, lowers your monthly payments, and can secure better interest rates. For mortgages, it can also help you avoid PMI.

- Consider Your Future Financial Stability: Think beyond your current income. Will your job be stable? Are there potential major life changes (e.g., starting a family, career change) that could impact your ability to make payments? Build a buffer.

- Budget Beyond the Payment: Remember to factor in all associated costs. For a car: insurance, fuel, maintenance. For a home: property taxes, homeowners insurance, utilities, and ongoing maintenance. If you’re looking to optimize your budget before taking on new debt, our comprehensive article on can provide valuable guidance.

- Leverage External Resources: Stay informed about current economic conditions and interest rate trends. For up-to-date information on current interest rates and economic forecasts, a trusted source like the Federal Reserve Economic Data (FRED) can be incredibly insightful, providing historical and current data on various financial indicators.

Common Misconceptions and Clarifications

Even with abundant information, certain misconceptions persist regarding car loans and mortgages. Let’s clarify a few:

- "All Debt is Bad Debt." This is a common oversimplification. While excessive, high-interest debt is certainly detrimental, "good debt" can be a powerful tool. A mortgage, for example, finances an appreciating asset and can build wealth. A car loan, while financing a depreciating asset, provides necessary transportation that can enable income generation. The key is understanding the purpose and cost of the debt.

- "Always Pay Cash for a Car." While paying cash avoids interest, it’s not always the best financial move. If your cash could be invested elsewhere for a higher return than your car loan interest rate, or if holding onto cash provides a critical emergency fund, financing might be more strategic. The opportunity cost of tying up a large sum of cash needs to be considered.

- "Interest Rates Are the Only Factor." While crucial, interest rates are just one piece of the puzzle. The loan term, fees, down payment requirements, and your overall financial situation (including your DTI) all play significant roles in the true cost and suitability of a loan. A slightly higher interest rate on a much shorter term, for example, might result in less total interest paid than a lower rate on a very long term.

Conclusion: Your Path to Informed Financial Decisions

The journey of acquiring significant assets like a car or a home is a defining aspect of modern financial life. While both car loans and mortgages serve as essential gateways to these acquisitions, their underlying structures, financial implications, and long-term impacts are distinctly different. A car loan typically finances a depreciating asset for a shorter term, fulfilling an immediate need for transportation. A mortgage, conversely, is a long-term commitment to an appreciating asset, serving as a powerful engine for wealth building and financial stability.

By thoroughly understanding these differences – from collateral and loan terms to interest rates and equity building potential – you empower yourself to make strategic choices. This deep dive into "Car Loan vs. Mortgage" is not just about comparing numbers; it’s about equipping you with the knowledge to navigate your financial landscape with confidence, avoid common pitfalls, and ultimately pave your road to financial freedom. Remember, informed decisions today lead to a more secure and prosperous tomorrow.