Navigating the Road to Financial Stability: A Comprehensive Guide to Car Loan Delinquency

Navigating the Road to Financial Stability: A Comprehensive Guide to Car Loan Delinquency Carloan.Guidemechanic.com

Owning a car is a cornerstone of modern life for many, providing freedom, convenience, and access to work and opportunities. For most, this essential asset is financed through a car loan. While the dream of driving off the lot in a new or pre-owned vehicle is exciting, the reality of consistent payments can sometimes become a challenging burden. When those payments are missed, you enter the precarious territory of car loan delinquency.

This isn’t just a minor oversight; it’s a serious financial situation with far-reaching consequences that can impact your credit, your assets, and your overall financial well-being for years to come. Based on my experience as a financial blogger and advisor, understanding car loan delinquency isn’t just about knowing the definition; it’s about recognizing the warning signs, understanding the repercussions, and, most importantly, knowing the proactive steps you can take to prevent it or mitigate its damage.

Navigating the Road to Financial Stability: A Comprehensive Guide to Car Loan Delinquency

This comprehensive guide will serve as your ultimate resource, breaking down every aspect of car loan delinquency, offering practical advice, and empowering you to make informed decisions. We aim to provide real value, ensuring you’re equipped to navigate these financial waters with confidence.

What Exactly is Car Loan Delinquency? Unpacking the Definition

At its core, car loan delinquency occurs when you fail to make your scheduled car loan payments on time. It’s more than just being a few days late; it signifies a breach of the loan agreement you signed with your lender. The moment your payment due date passes without the full payment being received, your account transitions from current to delinquent.

Most lenders offer a brief "grace period," typically ranging from 10 to 15 days, after your payment due date. During this grace period, you might incur a late fee, but your account might not yet be reported as delinquent to credit bureaus. However, once this grace period expires and the payment is still outstanding, your account officially enters delinquent status. This is a critical distinction, as true delinquency triggers a cascade of more severe consequences.

Think of it like a red flag. The longer your payment remains unpaid past the grace period, the deeper you fall into delinquency, and the more severe the potential repercussions become. Understanding this timeline is crucial for taking timely action.

The Alarming Causes: Why Borrowers Fall Behind on Car Payments

The reasons behind car loan delinquency are as varied as the individuals experiencing them, but they often stem from a combination of unforeseen circumstances and, sometimes, inadequate financial planning. Identifying the root cause is the first step toward finding a solution.

One of the most common causes is a sudden loss or reduction of income. This could be due to job loss, a reduction in work hours, or even a significant pay cut. When the primary source of income is disrupted, essential expenses like car payments can quickly become unsustainable. This is a scenario many people face unexpectedly, highlighting the fragility of financial stability without a robust safety net.

Another major factor is unexpected, significant expenses. Life has a way of throwing curveballs: a medical emergency, a major home repair, or even a sudden family crisis. These unbudgeted costs can quickly deplete savings and force individuals to prioritize, often leaving car payments by the wayside. Based on my experience, many people underestimate the financial shock these events can cause, especially without an emergency fund.

Poor financial planning and over-borrowing also play a significant role. Sometimes, borrowers take on a car loan that stretches their budget thin from the start. They might have qualified for a loan, but the monthly payment leaves little room for error. When even minor financial hiccups occur, these individuals are often the first to fall into delinquency because their budget was already at its breaking point.

Lastly, life changes such as divorce, the arrival of a new child, or other family obligations can significantly alter a household’s financial landscape. These events, while sometimes joyous, can add unexpected financial pressures that make consistent car loan payments challenging.

The Grave Consequences: What Happens When You’re Delinquent?

The impact of car loan delinquency extends far beyond simply owing money. It can create a ripple effect that damages various aspects of your financial life. Understanding these consequences is vital for appreciating the urgency of addressing the issue.

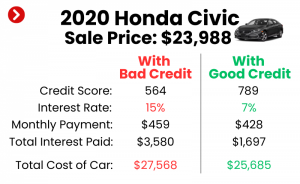

The most immediate and damaging effect is on your credit score. Once your payment is reported as 30, 60, or 90 days late to the major credit bureaus, your credit score will take a significant hit. A single 30-day late payment can drop your score by dozens of points, and longer periods of delinquency cause even more severe damage. This negatively impacts your ability to secure future loans (mortgages, credit cards, other car loans) and can even affect insurance premiums or job prospects.

Beyond credit scores, you’ll accumulate late fees and penalties. Lenders typically charge a flat fee or a percentage of the overdue amount for each missed payment. These fees quickly add up, increasing the total amount you owe and making it even harder to catch up. Pro tips from us: always read your loan agreement to understand the exact late fee structure.

If delinquency persists, your loan will eventually move into default status. This is a more severe stage where the lender deems you unable or unwilling to fulfill your loan obligations. Once in default, the lender has the right to take more drastic actions, most notably repossession. This is when the lender seizes your vehicle to recover their losses. The repossession process itself can incur additional costs for you, including towing, storage, and auction fees, which are often added to your outstanding debt.

Even after repossession, your financial obligations might not end. If the car sells for less than what you owe on the loan (which is common after factoring in fees), you could face a deficiency judgment. This means you’d still be legally responsible for paying the remaining balance, even though you no longer have the car.

Finally, we cannot overlook the emotional stress that accompanies car loan delinquency. The constant worry, the calls from collectors, and the fear of losing your vehicle can take a significant toll on mental and emotional well-being, affecting personal relationships and overall quality of life.

Spotting the Warning Signs Early: Don’t Ignore the Red Flags

Recognizing the early indicators of potential car loan delinquency is paramount. The sooner you identify these red flags, the more options you’ll have to correct your course and avoid the most severe consequences. Ignoring these signs is a common mistake that can lead to deeper financial trouble.

One of the clearest warning signs is struggling to make minimum payments consistently. If you find yourself frequently stretching your budget to the absolute limit just to cover your car payment, or if you’re consistently paying late, it’s a sign that your current financial setup isn’t sustainable. This isn’t just about missing a payment; it’s about the effort it takes to avoid missing one.

Another significant red flag is relying on credit cards or other forms of debt to cover your car payments. This practice, known as "robbing Peter to pay Paul," creates a dangerous cycle of increasing debt. You’re essentially taking on higher-interest debt to cover a lower-interest one, which is a losing strategy in the long run. Common mistakes to avoid are thinking this is a temporary fix; it often exacerbates the problem.

If you find yourself dipping into your savings account or emergency fund just to make your monthly car payment, that’s another serious indicator. An emergency fund is meant for unforeseen crises, not for covering regular monthly expenses. When it’s used for routine payments, it leaves you vulnerable to actual emergencies.

Finally, ignoring calls, emails, or letters from your lender is a major warning sign. While it might feel easier to avoid confrontation, this only makes the situation worse. Lenders are often more willing to work with you if you initiate contact early. Ignoring them signals a lack of cooperation, which can limit your options later on.

Proactive Strategies to Prevent Car Loan Delinquency

Prevention is always better than cure, especially when it comes to financial health. Implementing proactive strategies can significantly reduce your risk of car loan delinquency and help you maintain financial stability. These steps require discipline but offer immense peace of mind.

The foundation of financial stability is a robust budget. Create a realistic monthly budget that accounts for all your income and expenses, including your car payment. Track where every dollar goes. This helps you understand your true financial capacity and ensures your car payment is comfortably affordable, not a monthly struggle. Based on my experience, many people skip this crucial step, leading to surprises later on.

Building an emergency fund is another critical preventative measure. Aim to save at least three to six months’ worth of essential living expenses. This fund acts as a financial safety net, providing a buffer against unexpected income loss or significant expenses that could otherwise jeopardize your car payments. Without it, even minor setbacks can quickly escalate into delinquency.

Automating your car loan payments can prevent accidental missed due dates. Set up automatic transfers from your checking account to your lender a few days before the due date. This ensures payments are made consistently and on time, reducing the risk of late fees and credit score damage. It’s a simple step that offers huge benefits.

Regularly reviewing your loan terms is also important. Understand your interest rate, the total amount owed, and the exact payment schedule. Knowing the specifics empowers you to plan effectively. If your financial situation changes, you might consider options like refinancing. If interest rates have dropped or your credit score has improved, refinancing could lower your monthly payments, making them more manageable. For a deeper dive into improving your credit, check out our guide on .

Finally, consider the benefits of a larger down payment when purchasing a vehicle. A larger down payment reduces the amount you need to borrow, resulting in lower monthly payments and less interest paid over the life of the loan. This creates more breathing room in your budget from day one.

Navigating Delinquency: What to Do If You’re Already Behind

If you find yourself already in the throes of car loan delinquency, it’s crucial not to panic. While the situation is serious, inaction will only worsen it. Taking immediate, strategic steps can often mitigate the damage and help you get back on track.

The absolute first step is to communicate with your lender immediately. Do not wait for them to call you. Be proactive. Explain your situation honestly and clearly. Lenders are often more willing to work with borrowers who are upfront about their difficulties, as they prefer to avoid the costly and time-consuming process of repossession.

When you contact your lender, be prepared to explain your situation and discuss potential solutions. They may offer several options depending on your history and the severity of your delinquency. These options might include:

- Payment deferral or forbearance: This allows you to temporarily pause or reduce your payments for a specified period, with the understanding that you’ll make up the missed payments later.

- Loan modification: In some cases, the lender might be willing to permanently alter the terms of your loan, such as extending the loan term to lower your monthly payments.

- Temporary reduced payments: They might agree to lower your payment for a short period to help you get back on your feet.

Pro tips from us: Always get any agreement with your lender in writing. Verbal agreements are often difficult to enforce.

If your credit hasn’t been too severely damaged, refinancing your car loan might still be an option. A new loan with a lower interest rate or a longer term could reduce your monthly payments, making them more affordable. However, this is usually only feasible if your delinquency is recent and minor. If you’re considering refinancing, our comprehensive article, , offers valuable insights.

In some extreme cases, voluntary surrender of the vehicle might be your best option. This means you return the car to the lender yourself, avoiding the added costs and public embarrassment of repossession. While it will still negatively impact your credit and you may still owe a deficiency balance, it can sometimes be a less costly and less stressful alternative to forced repossession.

Finally, consider seeking guidance from a non-profit credit counseling agency. These organizations can help you assess your overall financial situation, create a debt management plan, and even act as an intermediary between you and your creditors. For reliable information and resources on credit counseling, visit the Consumer Financial Protection Bureau (CFPB) website.

Rebuilding After Repossession or Default: A Path Forward

Experiencing a car repossession or loan default is undoubtedly a difficult and disheartening event. However, it’s not the end of your financial journey. Understanding the aftermath and committing to a strategic rebuilding process can help you recover and regain financial stability.

First, understand the aftermath. Even after repossession, you might still owe a deficiency balance – the difference between what you owed on the car and what the lender sold it for, plus any fees. This debt will likely be pursued, and ignoring it can lead to further legal action or collections. Your credit report will also show the repossession, which will significantly impact your ability to get credit for several years.

The most critical step in rebuilding is credit repair. Start by obtaining copies of your credit reports from all three major bureaus (Experian, Equifax, TransUnion) and review them carefully for any inaccuracies. Dispute any errors immediately. Focus on paying down other outstanding debts and making all future payments on time. Consider secured credit cards or small, secured loans to demonstrate responsible borrowing habits and slowly rebuild your credit profile.

Financial discipline becomes even more crucial. Revisit your budget with a stricter eye, focusing on saving and minimizing unnecessary expenses. Build up your emergency fund again, ensuring you have a buffer against future financial shocks. This period is an opportunity to learn from past mistakes and establish healthier financial habits. Common mistakes to avoid are rushing into new credit or loans without a solid financial plan; this can easily lead back to square one.

When it comes to future borrowing, be realistic. It will be challenging to secure favorable loan terms immediately after a repossession or default. You might need to rely on public transportation, ride-sharing, or save up to purchase a less expensive vehicle outright. If you do need a loan, expect higher interest rates and be prepared to put down a substantial down payment. Focus on proving your financial reliability over time.

Conclusion: Taking Control of Your Financial Future

Car loan delinquency is a serious financial challenge, but it is not an insurmountable one. Throughout this comprehensive guide, we’ve explored its definition, the common causes, the severe consequences, and, most importantly, the proactive and reactive strategies you can employ to navigate these difficult waters. From meticulous budgeting and building an emergency fund to immediate communication with your lender and diligent credit repair, every step you take brings you closer to financial stability.

Remember, the key to overcoming or preventing delinquency lies in awareness, proactive planning, and decisive action. Don’t let fear or embarrassment prevent you from addressing the issue head-on. By understanding the gravity of the situation and utilizing the resources available, you can protect your credit, preserve your assets, and ultimately take control of your financial future.

We hope this pillar content provides you with the knowledge and confidence needed to make informed decisions about your car loan and overall financial health. Your journey to financial stability starts now.