Navigating the Road to Ownership: Your Comprehensive Guide to Car Loans for Subprime Credit

Navigating the Road to Ownership: Your Comprehensive Guide to Car Loans for Subprime Credit Carloan.Guidemechanic.com

Securing reliable transportation is a cornerstone of modern life for many, enabling commutes to work, school, and essential errands. Yet, for individuals navigating the complexities of subprime credit, the path to vehicle ownership can often feel like an uphill battle. If you’ve ever found yourself wondering, "Can I really get a car loan with bad credit?" or "What are my options for car loans for subprime credit?", you’re not alone. Millions of Americans face similar challenges, but the good news is that solutions exist.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to successfully secure a vehicle, even when your credit score isn’t perfect. We’ll delve deep into what subprime credit means, where to find specialized lenders, how to prepare for the application process, and most importantly, how to use a car loan as a powerful tool to rebuild your financial standing. Our ultimate goal is to provide you with a clear roadmap, transforming a potentially daunting process into an achievable journey towards owning the car you need.

Navigating the Road to Ownership: Your Comprehensive Guide to Car Loans for Subprime Credit

Understanding Subprime Credit and Car Loans

Before diving into the specifics of obtaining a loan, it’s crucial to understand what "subprime credit" truly signifies and why it impacts the lending landscape.

What Exactly is Subprime Credit?

In the world of personal finance, your credit score is a three-digit number that acts as a financial report card. It tells lenders how responsibly you’ve managed debt in the past. Credit scores typically range from 300 to 850. Generally, scores below 620 are considered "subprime" or "bad credit."

This designation usually means you have a history of late payments, high credit utilization, a limited credit history, or even past bankruptcies or collections. Lenders view these factors as indicators of higher risk when extending new credit.

Why Getting a Car Loan with Bad Credit Can Be Different

When you apply for a car loan with subprime credit, lenders perceive a greater chance that you might default on your payments. This elevated risk often translates into specific challenges for borrowers. You might encounter higher interest rates, stricter approval criteria, or require a larger down payment.

The terms and conditions for car loans for subprime credit are structured to mitigate the lender’s risk. This doesn’t mean you won’t get approved, but it does mean you’ll need to be more strategic and informed throughout the process.

The Importance of a Car in Daily Life

For many, a car isn’t a luxury; it’s a necessity. It provides access to employment opportunities that might be inaccessible via public transport, ensures children get to school, and connects families to essential services like healthcare and groceries. Without reliable transportation, improving one’s financial situation or even maintaining a steady job can become significantly harder.

Securing a car loan, even a subprime one, can be a vital step towards greater independence and stability. It’s about more than just getting a car; it’s about opening doors to a better quality of life and creating opportunities for financial growth.

Preparing for Your Subprime Auto Loan Journey

Preparation is key when seeking any loan, but it becomes absolutely critical when your credit history presents challenges. A well-prepared borrower often stands a much better chance of approval and securing more favorable terms.

Know Your Credit Score and Report Inside Out

The very first step is to understand exactly where you stand. Obtain copies of your credit report from all three major bureaus: Experian, Equifax, and TransUnion. You are entitled to a free report from each once every 12 months through AnnualCreditReport.com. Don’t just glance at the score; dive deep into the details.

Look for any inaccuracies or errors that might be negatively impacting your score. Disputing these can potentially improve your score relatively quickly. Understanding the specific reasons your credit is subprime will also help you address those issues and explain them to a lender if necessary.

Budgeting: What You Can Truly Afford

When considering car loans for subprime credit, it’s easy to focus solely on the monthly payment. However, a truly responsible budget goes far beyond that. Factor in all associated costs of car ownership: insurance (which can be higher for subprime borrowers and older vehicles), fuel, maintenance, and potential repairs.

Based on my experience, many borrowers overlook these crucial expenses, leading to financial strain later on. Create a realistic budget that accounts for these variables to ensure your car payment fits comfortably within your overall financial picture without causing undue stress.

Saving for a Down Payment: Your Best Ally

A significant down payment is one of the most powerful tools a subprime borrower has. It reduces the total amount you need to borrow, which in turn lowers your monthly payments and the overall interest paid over the life of the loan. More importantly, it signals to lenders that you are serious about your commitment and have some financial discipline.

Even a modest down payment can make a difference. Aim for at least 10-20% of the car’s purchase price if possible. This upfront investment significantly reduces the lender’s risk and can open doors to better loan offers.

Gathering Necessary Documents

Lenders will require various documents to verify your identity, income, and residence. Having these prepared in advance will streamline the application process and show your seriousness. Typically, you’ll need:

- Proof of Identity: Driver’s license or state ID.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Proof of Income: Recent pay stubs (usually 2-3 months), bank statements, or tax returns if self-employed.

- Proof of Insurance: You’ll need this before driving off the lot.

- References: Sometimes required, especially for buy-here-pay-here dealers.

Organizing these documents beforehand makes the application smooth and efficient, demonstrating your readiness to complete the transaction.

Where to Find Car Loans for Subprime Credit

The landscape for securing an auto loan with challenging credit can seem vast and confusing. However, several distinct avenues specialize in providing car loans for subprime credit borrowers. Knowing where to look can save you time and help you find the best possible terms.

Dealership Financing: A Common Starting Point

Many car dealerships offer in-house financing or work with a network of lenders, including those specializing in subprime loans. This can be convenient as you can shop for a car and arrange financing all in one place.

- Captive Lenders: These are financing arms of car manufacturers (e.g., Ford Credit, Toyota Financial Services). While they often target prime borrowers, some have programs for those with less-than-perfect credit.

- Third-Party Lenders: Dealers also partner with banks, credit unions, and independent finance companies. Many of these have specific programs tailored for subprime borrowers.

- Buy-Here-Pay-Here (BHPH) Dealerships: These dealerships act as both the seller and the lender. They typically cater exclusively to individuals with very poor credit or no credit history. While they offer convenience and almost guaranteed approval, they often come with significantly higher interest rates and less flexible terms. It’s often considered a last resort due to these higher costs.

Banks and Credit Unions: Traditional Lenders

While traditional banks and credit unions might have stricter lending criteria, they often offer more competitive interest rates if you qualify. Don’t assume you’ll be rejected outright.

- Credit Unions: These member-owned institutions are known for being more community-focused and can sometimes be more flexible with their lending decisions, especially if you have an existing relationship with them. Their rates are often among the best available.

- Local Banks: If you have an existing checking or savings account with a local bank, they might be more willing to work with you, leveraging your established banking relationship.

It’s always worth exploring these options, as a direct loan from a bank or credit union can potentially save you a lot of money in interest over the life of the loan.

Online Lenders and Loan Aggregators: Specializing in Bad Credit

The digital age has brought forth numerous online platforms that specialize in car loans for subprime credit. These lenders often have streamlined application processes and can provide quick pre-approvals.

- Dedicated Online Lenders: Companies like Capital One Auto Finance, myAutoloan, or Carvana (which also sells cars) have robust programs for various credit profiles, including subprime. They often use alternative data points in their approval process.

- Loan Aggregators: Websites like Credit Karma Auto or LendingTree allow you to fill out a single application and receive multiple loan offers from different lenders. This is a fantastic way to compare rates and terms without impacting your credit score with multiple hard inquiries (as these initial inquiries are often soft pulls).

Pro tips from us: Always compare offers from at least three different sources. Don’t jump at the first approval you receive. Different lenders have different appetites for risk, and shopping around can reveal significantly better terms, even with subprime credit.

Understanding the Terms of a Subprime Car Loan

When dealing with car loans for subprime credit, understanding the fine print and key loan terms is paramount. These elements directly impact the total cost of your vehicle and your ability to manage the payments.

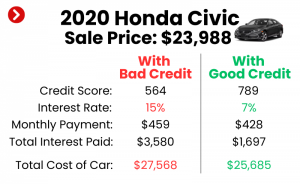

Interest Rates: The Big Factor

For subprime borrowers, interest rates will almost certainly be higher than for those with excellent credit. This is how lenders compensate for the increased risk they are taking. While a prime borrower might see rates below 5%, a subprime borrower could face rates anywhere from 10% to 25% or even higher, particularly with BHPH dealers.

Even a small difference in the interest rate can add up to thousands of dollars over the life of the loan. This is why shopping around and comparing offers is so critical. A higher interest rate means a larger portion of your monthly payment goes towards interest, not the principal balance.

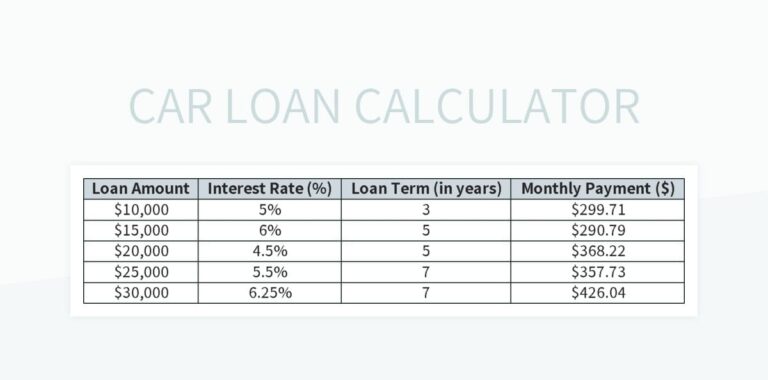

Loan Term: Shorter vs. Longer

The loan term refers to the length of time you have to repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months).

- Longer Terms (e.g., 72 months): These result in lower monthly payments, making the car seem more affordable in the short term. However, you’ll pay significantly more in total interest over the life of the loan, and the car might depreciate faster than you pay it off, leading to "negative equity" (owing more than the car is worth).

- Shorter Terms (e.g., 36-48 months): These lead to higher monthly payments but drastically reduce the total interest paid. You’ll also build equity in the car faster.

Common mistakes to avoid are: focusing exclusively on the lowest possible monthly payment. While affordability is important, extending the loan term excessively can cost you much more in the long run. Try to balance a manageable monthly payment with the shortest loan term you can realistically afford.

Down Payment: How Much is Enough?

As mentioned earlier, a down payment is incredibly beneficial. For subprime loans, lenders often require a down payment, sometimes as high as 10-20%. The more you can put down, the better.

A larger down payment reduces the principal amount borrowed, which means less interest accrues. It also makes you a more attractive borrower in the eyes of lenders, potentially leading to better terms and a higher chance of approval.

Fees and Other Charges

Beyond the interest rate, be aware of other potential fees:

- Origination Fees: A fee charged by the lender for processing the loan.

- Documentation Fees: Charged by the dealership for preparing paperwork.

- Late Payment Fees: Penalties if you miss a payment.

- Prepayment Penalties: Less common with auto loans, but check if you’re penalized for paying off the loan early.

Always ask for a full breakdown of all fees and charges before signing any agreement. Transparency is key.

Strategies for Improving Your Chances of Approval

Even with subprime credit, there are proactive steps you can take to bolster your application and increase your likelihood of approval for a car loan. These strategies demonstrate responsibility and reduce the perceived risk for lenders.

Having a Cosigner: A Helping Hand

If you have a trusted friend or family member with good credit, asking them to cosign your loan can significantly improve your chances of approval and potentially secure a lower interest rate. A cosigner essentially guarantees the loan, promising to make payments if you default.

However, this is a serious commitment for the cosigner. Their credit will be affected if you miss payments, and they will be legally responsible for the debt. Ensure both parties fully understand the implications before proceeding. It’s a powerful tool but one that should be used with great care and clear communication.

Choosing the Right Vehicle: Be Practical

While it might be tempting to eye a brand-new, fully loaded car, a more practical approach is best when seeking car loans for subprime credit. Opt for a reliable, used vehicle that meets your needs without overextending your budget.

- Affordability: Choose a car that is well within your budget, considering not just the loan payment but also insurance, maintenance, and fuel.

- Reliability: A car that frequently breaks down will quickly become a financial burden. Research models known for their dependability.

- Depreciation: New cars lose value rapidly. A slightly older, well-maintained used car holds its value better and is generally more affordable.

Lenders are also more comfortable financing a reasonably priced vehicle than an expensive one for a subprime borrower.

Showing Income Stability: A Solid Foundation

Lenders want to see that you have a consistent and verifiable source of income to repay the loan. Steady employment for an extended period (e.g., 6 months to 1 year or more at the same job) is a strong indicator of stability.

Be prepared to provide multiple pay stubs or bank statements that clearly show regular deposits. If you’re self-employed, tax returns and detailed bank statements will be essential. Any gaps in employment or highly variable income can make lenders hesitant.

Demonstrating Responsibility: A Positive Track Record

Even if your credit score is low, you can still show lenders that you’re working towards financial responsibility. If you have any active accounts (e.g., a secured credit card, a small personal loan), ensure you’re making all payments on time.

- Pay all bills on time: Not just credit accounts, but also utilities, rent, and phone bills. While these may not directly impact your credit score in the same way, consistent on-time payments demonstrate a commitment to your financial obligations.

- Reduce other debt: Lowering your existing debt burden can improve your debt-to-income ratio, making you a more attractive borrower.

Lenders often look beyond just the score, seeking evidence of current responsible financial behavior.

Rebuilding Your Credit with a Subprime Car Loan

Securing a car loan when you have subprime credit isn’t just about getting transportation; it’s a significant opportunity to improve your financial health. A properly managed auto loan can be a powerful tool for credit rebuilding.

Making On-Time Payments: The Most Crucial Step

This cannot be stressed enough: consistently making your car loan payments on time, every single month, is the single most effective way to improve your credit score. Payment history accounts for 35% of your FICO score, making it the largest factor.

Set up automatic payments if possible, or mark your calendar with reminders. Missing even one payment can set back your credit repair efforts by months or even years. This commitment is the cornerstone of leveraging your auto loan for positive credit growth.

The Power of a Positive Payment History

Each on-time payment you make is reported to the major credit bureaus. Over time, this creates a strong, positive payment history that directly counteracts past negative entries. As this positive history grows, lenders will begin to see you as a more reliable borrower, and your credit score will gradually rise.

Based on my experience, many individuals who diligently make their payments on time for 12-18 months see a noticeable improvement in their credit score, often moving them out of the "subprime" category. This opens doors to better financial products and opportunities in the future.

Refinancing Options: When Your Credit Improves

Once you’ve established a consistent record of on-time payments and your credit score has improved, you may be eligible to refinance your car loan. Refinancing means taking out a new loan to pay off your existing one, ideally with a lower interest rate and potentially more favorable terms.

This can significantly reduce your monthly payment and the total interest you pay over the remaining life of the loan. It’s a smart move to review your options for refinancing after about 12-18 months of consistent, on-time payments, especially if your initial loan came with a very high interest rate. For more insights on this, you might find our article on helpful.

Potential Pitfalls and How to Avoid Them

While car loans for subprime credit offer a vital pathway to vehicle ownership, the market can also present certain traps for the unwary. Being informed and cautious can protect you from costly mistakes.

High-Pressure Sales Tactics

Some dealerships, especially those specializing in subprime loans, might employ high-pressure sales tactics. They might try to rush you through the paperwork, discourage you from reading the fine print, or make you feel like this is your only chance to get a car.

Always take your time. If you feel pressured, walk away. A reputable lender or dealer will give you space to review documents and ask questions. Never sign anything you don’t fully understand or feel comfortable with.

Hidden Fees and Unnecessary Add-ons

Be vigilant about hidden fees or unnecessary add-ons that can inflate the total cost of your loan. These might include extended warranties you don’t need, VIN etching, fabric protection, or credit insurance. While some add-ons can be beneficial, many are overpriced and designed to boost the dealer’s profit.

Carefully review the itemized list of charges. Ask about anything you don’t recognize or understand. You have the right to decline most add-ons. Don’t let emotion or the excitement of getting a car cloud your judgment about these extra costs.

Predatory Lending Practices: What to Look Out For

Unfortunately, some lenders engage in predatory practices that exploit vulnerable borrowers. These can include:

- Excessively high interest rates: Rates far above market averages, even for subprime credit.

- Loan packing: Adding unnecessary products or services to the loan.

- Balloon payments: Large, single payments due at the end of the loan term, which can lead to refinancing or default.

- Flipping: Encouraging frequent refinancing of the loan, often with additional fees, to keep the borrower in debt.

If a deal seems too good to be true, or if you feel uncomfortable with the terms, it’s a red flag. Always get a second opinion if you suspect predatory lending.

Understanding the Fine Print

The loan agreement is a legally binding document. It contains all the critical details of your loan, including the interest rate, loan term, total amount financed, total cost of the loan, payment schedule, and any penalties.

Read every word of the contract before signing. Don’t be afraid to ask questions until you fully comprehend every clause. If a dealer or lender rushes you, or refuses to explain something clearly, consider it a warning sign. Bringing a trusted friend or advisor with you can also provide an extra pair of eyes and support.

Conclusion

Navigating the landscape of car loans for subprime credit can undoubtedly feel challenging, but it is far from impossible. By understanding what subprime credit entails, preparing diligently, knowing where to find reputable lenders, and critically evaluating loan terms, you can significantly improve your chances of securing the transportation you need.

Remember, a subprime car loan isn’t just a means to an end; it’s a potential stepping stone towards a stronger financial future. By consistently making on-time payments, you can actively rebuild your credit score, opening doors to better financial opportunities down the road, including refinancing for lower rates. Approach the process with knowledge, patience, and a commitment to responsible borrowing, and you will ultimately achieve your goal of vehicle ownership while simultaneously strengthening your financial foundation. For further guidance on managing your finances, check out our comprehensive guide on .