Navigating the Road to Two Car Loans: Your Expert Guide to Financing Multiple Vehicles

Navigating the Road to Two Car Loans: Your Expert Guide to Financing Multiple Vehicles Carloan.Guidemechanic.com

In today’s fast-paced world, having one car is often a necessity. But for many, a single vehicle simply isn’t enough to meet all their family, work, or lifestyle demands. Whether it’s a growing family, a need for a dedicated work vehicle, or the desire for a weekend cruiser alongside a daily driver, the idea of securing two car loans often comes up.

The question isn’t just "Is it possible?" but rather, "How do I do it smartly and responsibly?" Getting a second car loan can seem daunting, especially with the financial commitments involved. However, with the right strategy, a solid financial foundation, and a clear understanding of the process, it’s an achievable goal.

Navigating the Road to Two Car Loans: Your Expert Guide to Financing Multiple Vehicles

This comprehensive guide will demystify the process of financing two vehicles, offering expert insights, practical strategies, and essential considerations to help you navigate this significant financial decision. We’ll dive deep into eligibility, common pitfalls, and how to manage multiple auto loans effectively, ensuring you drive away with confidence.

The "Why" Behind Two Car Loans: Understanding Your Needs

Before even thinking about applying, it’s crucial to understand the driving force behind your need for a second vehicle. Lenders, while primarily focused on your financial capacity, also appreciate a clear rationale. More importantly, understanding your own "why" will help you make a more informed decision about the type of car and loan that suits you.

Based on my experience, many clients consider a second car for a variety of compelling reasons, often stemming from evolving life stages or professional requirements. It’s rarely a frivolous decision but rather a practical response to life’s demands.

Family Needs and Logistics

For many households, one car simply doesn’t cut it. Perhaps both spouses need a vehicle for their daily commutes, or teenagers in the household are starting to drive. A second car can significantly ease the logistical burden of school drop-offs, extracurricular activities, and grocery runs. It provides flexibility and independence, ensuring everyone can be where they need to be, when they need to be there.

Work and Business Demands

Your profession might be another strong motivator. If your job requires extensive travel, carrying specialized equipment, or having a presentable vehicle for client meetings, a second car might be a business necessity. Some entrepreneurs even finance a dedicated work vehicle separate from their personal car, which can have tax implications and keep business and personal expenses distinct. This separation can simplify accounting and provide a clear boundary.

Hobbies, Passions, and Lifestyle Choices

Sometimes, the desire for a second car stems from a passion. This could be a classic car project, an off-road vehicle for weekend adventures, or a convertible for leisurely drives. These are often considered "fun" cars, but they still represent a significant financial commitment. Understanding that this is a lifestyle choice rather than a necessity will influence your budget and the type of loan you seek. It’s about balancing desire with financial prudence.

Diverse Transportation Requirements

Different situations often call for different types of vehicles. You might need an economical sedan for daily city commuting and a larger SUV or truck for family road trips, towing, or hauling. These diverse needs make a compelling case for owning two distinct vehicles, each serving a specific purpose. It’s about optimizing your transportation solutions for various scenarios.

Can You Really Get Two Car Loans? The Lender’s Perspective

The short answer is yes, securing two car loans is absolutely possible. However, it’s not a walk in the park. Lenders evaluate every application for a second car loan with increased scrutiny, primarily because they are taking on a greater risk. They need to be confident that you can comfortably manage the payments for both vehicles, in addition to all your other existing financial obligations.

Lenders aren’t just looking at your enthusiasm for a new car; they’re meticulously analyzing your financial health. Their main concern is your ability to repay the loans without defaulting. This involves a deep dive into several key aspects of your financial profile, each playing a crucial role in their decision-making process.

The Credit Score: Your Financial Report Card

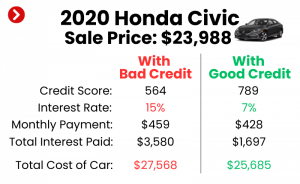

Your credit score is arguably the most critical factor when applying for any loan, especially a multiple car loan. A high credit score (generally 700+) signals to lenders that you are a responsible borrower with a history of timely payments. It indicates a lower risk of default. If your credit score is excellent, you’ll not only have a higher chance of approval but also qualify for better interest rates, saving you a substantial amount over the life of the loans.

A lower credit score, on the other hand, will make it much harder to get approved for a second car loan. Lenders will perceive you as a higher risk, and if approved, you’ll likely face significantly higher interest rates, making both loans more expensive.

Debt-to-Income (DTI) Ratio: The Ultimate Gatekeeper

This is where many aspiring two-car owners hit a roadblock. Your Debt-to-Income (DTI) ratio is a crucial metric lenders use to assess your ability to manage monthly payments. It compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover additional loan payments.

Adding a second car loan significantly increases your total monthly debt, directly impacting your DTI. Lenders typically prefer a DTI ratio below 36% to 43% for auto loans. If your DTI is already high with your existing car loan and other debts, adding another substantial payment could push you beyond an acceptable threshold, leading to a rejection. This is often the single biggest hurdle.

Income Stability and Amount

Lenders want to see a consistent and sufficient income stream. They’ll verify your employment history, salary, and any other verifiable income sources. A stable job with a good income provides reassurance that you have the means to consistently make your payments. Self-employed individuals may need to provide more extensive documentation, such as tax returns, to prove income stability. The higher and more stable your income, the more comfortable lenders will be with extending you additional credit.

Payment History and Existing Loans

Your track record with existing loans—including your first car loan, mortgage, credit cards, and student loans—is a strong indicator of your reliability. A history of on-time payments demonstrates responsible borrowing. Conversely, any missed or late payments will raise red flags and significantly hurt your chances of approval for a multiple car loan. Lenders want to see that you can handle your current financial obligations before taking on new ones.

Down Payment: Showing Your Commitment

While not always mandatory, making a substantial down payment on your second vehicle can dramatically improve your chances of approval. A larger down payment reduces the loan amount, thereby lowering your monthly payments and easing the impact on your DTI. It also shows lenders that you are financially committed to the purchase and have some savings, which implies greater financial stability. A 10-20% down payment is often recommended.

Vehicle Value and Collateral

The car itself acts as collateral for the loan. Lenders will assess the value of the vehicle you intend to purchase. A car that holds its value well or is less likely to depreciate rapidly can be viewed more favorably, as it reduces the lender’s risk in case of default. The type, age, and mileage of the vehicle will all play a role in this assessment.

Pro tips from us: Lenders look at your entire financial picture, not just isolated components. Prepare to present a clear, strong, and stable financial profile to maximize your approval odds for two car loans.

Deep Dive into DTI: The Ultimate Gatekeeper Explained

As we’ve highlighted, your Debt-to-Income (DTI) ratio is arguably the most critical factor in a lender’s decision to approve a second car loan. It’s a simple yet powerful indicator of your financial health and your capacity to take on more debt. Understanding it thoroughly is non-negotiable for anyone considering financing two vehicles.

What is DTI and How is it Calculated?

Your DTI ratio is a percentage that represents how much of your gross monthly income goes towards paying your monthly debts. It’s calculated by taking your total monthly debt payments and dividing them by your gross monthly income (income before taxes and deductions).

Calculation Example:

Let’s say your gross monthly income is $5,000.

Your current monthly debts include:

- First Car Loan Payment: $400

- Credit Card Minimum Payments: $150

- Student Loan Payment: $200

- Mortgage/Rent Payment: $1,200 (if applicable, though some lenders only consider "revolving" debt for auto loans, it’s safer to include all major payments for a holistic view)

Total Current Monthly Debts: $400 + $150 + $200 + $1,200 = $1,950

Current DTI: ($1,950 / $5,000) * 100% = 39%

Typical Acceptable DTI for Loans

For a single auto loan, many lenders prefer a DTI ratio below 36%. Some might go up to 43% for very strong applicants with excellent credit scores and stable employment. However, when you’re seeking two car loans, lenders become much more conservative. They want to see that you have ample wiggle room in your budget to absorb the additional payment without stretching yourself too thin.

Impact of Adding a Second Car Loan to Your DTI

Let’s continue our example. If you add a second car loan with an estimated monthly payment of $350, your total monthly debts would become:

New Total Monthly Debts: $1,950 (current) + $350 (new car loan) = $2,300

New DTI: ($2,300 / $5,000) * 100% = 46%

In this scenario, a DTI of 46% might be too high for many lenders to approve a second car loan, especially if they prefer applicants to stay below 40%. This illustrates why managing your DTI is paramount. Even if your credit score is stellar, a high DTI can be a deal-breaker.

Strategies to Improve Your DTI Before Applying

Improving your DTI before you apply for a multiple car loan is one of the smartest moves you can make. It demonstrates financial discipline and increases your approval odds.

- Pay Down Existing Debts: Focus on reducing credit card balances, personal loans, or any other high-interest debts. Even small reductions can lower your total monthly debt payments.

- Increase Your Income: Explore opportunities for a raise, take on a side hustle, or consider part-time work to boost your gross monthly income. Remember, only verifiable income counts.

- Delay Other Major Purchases: Avoid taking on new debts like personal loans or credit card balances right before applying for a second car loan.

- Wait for Existing Loans to Be Paid Off: If your first car loan is close to being paid off, waiting until it’s fully settled will significantly free up your monthly budget and lower your DTI.

Common mistakes to avoid are not calculating your DTI accurately before applying, or worse, not considering its impact at all. Many people assume a good credit score is enough, but a high DTI can easily overshadow it, leading to frustrating rejections. Always run these numbers yourself first.

Strategies for Successfully Securing Two Car Loans

Getting approved for two car loans requires more than just decent finances; it demands a strategic approach. You need to present yourself as a low-risk borrower, and that involves careful planning and execution.

A. Strengthen Your Financial Profile

Before you even fill out an application, dedicate time to optimizing your financial standing. This foundational work will pay dividends in approval rates and favorable terms.

- Improve Your Credit Score: This is paramount. Pay all your bills on time, every time. Reduce credit card balances to below 30% of your credit limit, and avoid opening new credit accounts unnecessarily. A higher credit score makes you a more attractive borrower and can unlock lower interest rates. For more tips on improving your credit score, check out our guide on .

- Increase Your Income: Actively seek ways to boost your gross monthly income. This could involve negotiating a raise, taking on overtime hours, or starting a profitable side gig. Lenders will look at your verifiable income, so ensure any new income sources are well-documented.

- Save for a Larger Down Payment: A substantial down payment not only reduces the amount you need to borrow but also signals to lenders your commitment and financial stability. Aim for at least 10-20% of the vehicle’s price, or even more if possible. This directly lowers your monthly payment and improves your DTI.

- Pay Down Existing Debts: Prioritize paying off high-interest debts like credit cards. Reducing these balances lowers your overall monthly debt obligations, which in turn improves your crucial DTI ratio. Even paying off a small personal loan can make a noticeable difference.

B. Smart Loan Application Tactics

Once your financial profile is in shape, adopt smart strategies when actually applying for the loans. This can significantly influence your success.

- Staggered Applications: If you already have one car loan and are seeking a second, it’s often better to let your first loan "season" for a while. Lenders prefer to see a consistent payment history on an existing loan before extending new credit. Applying for both simultaneously can sometimes be seen as a higher risk, especially if your DTI is already tight.

- Consider Different Lenders: Don’t just go to your primary bank. Shop around. Credit unions often offer more competitive rates and may be more flexible with their lending criteria for members. Online lenders are also an option. Compare offers from at least three to five different institutions.

- Apply with a Co-signer: If your DTI is a concern or your credit score isn’t stellar, a co-signer with excellent credit and a low DTI can significantly boost your approval chances. Remember, a co-signer is equally responsible for the debt, so choose someone you trust and who understands the commitment.

- Opt for a Cheaper Second Vehicle: While it might be tempting to get your dream car, choosing a more affordable second vehicle can be a wise strategic move. A lower loan amount means lower monthly payments, which keeps your DTI in check and makes approval much easier.

C. Vehicle Choice Matters

The car you choose for your second loan plays a larger role than you might think in the financing process and your long-term financial health.

- New vs. Used: While new cars come with the latest features, they also depreciate quickly and typically have higher price tags. A reliable, well-maintained used car can be a more budget-friendly option, leading to a smaller loan amount and lower monthly payments. However, sometimes interest rates on used cars can be slightly higher depending on the age of the vehicle and the lender.

- Reliability: Factor in the long-term costs. A car with a reputation for reliability will likely have lower maintenance and repair costs, reducing unexpected financial burdens that could jeopardize your ability to make loan payments. Research consumer reports and mechanic reviews.

- Insurance Costs: Don’t forget insurance! Get quotes for both vehicles before committing to a purchase. Insurance premiums can vary dramatically based on the vehicle’s make, model, age, and your driving history. High insurance costs can add significant strain to your monthly budget, so factor them in from the start.

Financial Implications and Risks of Juggling Two Car Loans

While getting two car loans is possible, it’s essential to understand the potential financial implications and risks involved. This isn’t just about securing the loan; it’s about managing the long-term commitment.

Increased Monthly Expenses

This is the most obvious impact. You’ll have two loan payments, two insurance premiums, double the fuel costs, and potentially double the maintenance expenses. This significantly increases your fixed monthly outgoings, leaving less room in your budget for other discretionary spending or savings.

Reduced Financial Flexibility

With a larger portion of your income tied up in car payments and related expenses, your financial flexibility will naturally decrease. This means less disposable income for vacations, entertainment, or even unexpected opportunities. It can feel like your budget is stretched thin, making it harder to adapt to financial changes.

Higher Risk of Default

The more debt you have, the higher the risk of default if your financial situation changes. Job loss, unexpected medical bills, or other major life events can suddenly make managing two car payments extremely difficult. Defaulting on even one loan can severely damage your credit score and lead to repossession, creating a ripple effect on your entire financial future.

Impact on Future Borrowing

Having multiple car loans can also affect your ability to secure other significant loans in the future, such as a mortgage or a business loan. Lenders for these larger financial products will look at your overall DTI and existing debt load. A high DTI due to two car loans could make it harder to qualify for a mortgage or force you into less favorable terms.

Depreciation of Assets

Cars are depreciating assets. They lose value over time, often quite rapidly. With two cars, you’re essentially doubling your exposure to this depreciation. While they provide utility, they aren’t investments that grow in value. Understanding this financial reality is crucial.

Pro tips from us: Always consider the long-term financial picture, not just the immediate monthly payment. Create a robust budget that accounts for all costs associated with both vehicles, including maintenance funds.

Alternatives to Taking Out Two Separate Car Loans

If the prospect of managing two car loans seems too financially challenging, or if you’re denied for a second car loan, don’t despair. There are several viable alternatives that can meet your transportation needs without the burden of additional debt.

Leasing a Second Vehicle

Leasing can be an attractive option for a second car, especially if you prefer driving newer models and don’t want the long-term commitment of ownership. Lease payments are typically lower than loan payments for a comparable vehicle because you’re only paying for the depreciation during the lease term, not the full purchase price. However, you won’t own the car at the end of the lease, and there are mileage restrictions and potential fees for excessive wear and tear.

Refinancing an Existing Loan

If your current car loan has a high interest rate, refinancing it could free up some cash flow. By securing a lower interest rate or extending the loan term (though this means paying more interest over time), you can reduce your monthly payment. This reduction could then improve your DTI, making it easier to qualify for a new car loan or simply easing your overall financial burden.

Using Public Transportation or Ride-Sharing

For some, especially those in urban areas, relying on public transportation, ride-sharing services (like Uber or Lyft), or even cycling for certain trips can negate the need for a second car entirely. Evaluate if one of your daily commutes or occasional errands could be managed without a personal vehicle. This is often the most cost-effective solution.

Buying a Cheaper Cash Car

If you have some savings, consider purchasing a reliable, inexpensive used car with cash. This completely avoids the need for a loan, additional interest payments, and the impact on your DTI. While it might not be the newest or most luxurious vehicle, a cash car provides the necessary transportation without adding to your debt load. Focus on models known for their longevity and low maintenance costs.

Family Sharing Arrangements

In some family setups, a shared vehicle for specific purposes (like weekend errands or a teenager’s occasional use) can be a practical solution. This requires clear communication and scheduling but can avoid the need for an additional car payment and all associated costs.

Managing Your Multiple Car Loans Effectively

Successfully securing two car loans is only half the battle. The real challenge, and where your financial discipline truly shines, is in managing them effectively over the long term. Poor management can quickly lead to financial stress and damaged credit.

Create a Detailed Budget

This is non-negotiable. You need a comprehensive budget that accounts for all vehicle-related expenses for both cars. This includes not just the loan payments, but also insurance, fuel, maintenance, registration, and potential emergency repairs. Track every dollar in and out to ensure you always know where you stand financially.

Automate Payments

Set up automatic payments for both car loans from your bank account. This ensures that payments are always made on time, preventing late fees and protecting your precious credit score. Timely payments are crucial for maintaining a healthy financial profile, especially with multiple car loans.

Build an Emergency Fund

Unexpected car repairs are a common occurrence, and with two vehicles, the chances of one needing attention double. Build a dedicated emergency fund specifically for car-related issues, or ensure your general emergency fund is robust enough to cover these costs without derailing your budget or forcing you to miss loan payments.

Regularly Review Your Loans

Interest rates can change, and your credit score might improve over time. Regularly review your loans to see if refinancing opportunities exist. If you can secure a lower interest rate on either loan, it could save you thousands of dollars over the loan term and reduce your monthly outgoings. This proactive approach ensures you’re always getting the best deal.

Prioritize Payments (If You Ever Face Hardship)

In the unfortunate event that you face financial hardship, you may need to prioritize which loan payments to make. Generally, secured debts like car loans (where the car is collateral) and mortgages should be prioritized to avoid repossession. If you anticipate difficulty, contact your lenders immediately to discuss potential solutions before you miss a payment.

External Link: For robust budgeting tools and further financial planning resources, consider exploring reputable personal finance websites like . These resources can provide invaluable assistance in managing complex financial situations.

Conclusion: Driving Forward with Confidence

Securing and managing two car loans is a significant financial undertaking, but it is entirely achievable with careful planning, a strong financial foundation, and a strategic approach. We’ve explored the "why" behind this decision, delved into the critical factors lenders assess like your DTI and credit score, and provided actionable strategies to improve your chances of approval.

Remember, the journey to financing two vehicles is about more than just getting the keys; it’s about responsible financial management. By strengthening your financial profile, employing smart application tactics, and diligently managing your multiple loans, you can navigate this road with confidence.

Whether it’s for family, work, or leisure, a second car can provide immense convenience and flexibility. Plan wisely, understand the implications, and drive confidently into your multi-car future.