Navigating the Road to Vehicle Ownership: Your Comprehensive Guide to Consumer Portfolio Services Car Loans

Navigating the Road to Vehicle Ownership: Your Comprehensive Guide to Consumer Portfolio Services Car Loans Carloan.Guidemechanic.com

For many individuals, owning a reliable vehicle is not just a luxury but a necessity for work, family, and daily life. However, navigating the world of auto financing can be challenging, especially if your credit history isn’t pristine. This is where specialized lenders like Consumer Portfolio Services (CPS) step in, offering a vital pathway to car ownership for those traditionally overlooked by conventional banks.

In this exhaustive guide, we’ll dive deep into Consumer Portfolio Services car loans, exploring everything you need to know from application to repayment. Our goal is to provide you with a unique, insightful, and practical understanding, helping you make informed decisions on your journey to securing a vehicle. We’ll cover who CPS is, how their loans work, and crucial tips for managing your financing effectively.

Navigating the Road to Vehicle Ownership: Your Comprehensive Guide to Consumer Portfolio Services Car Loans

What Exactly is Consumer Portfolio Services (CPS)?

Consumer Portfolio Services, often simply referred to as CPS, is an independent financial services company specializing in indirect auto financing. Unlike traditional banks or credit unions, CPS primarily focuses on the subprime auto loan market. This means they lend to individuals who may have a less-than-perfect credit history, including those with low credit scores, past bankruptcies, or repossessions.

Their business model involves partnering with a vast network of dealerships across the United States. When you apply for a car loan at a dealership, and your credit profile doesn’t fit the criteria of prime lenders, the dealer might submit your application to CPS. This allows them to serve a significant segment of the population that might otherwise struggle to obtain vehicle financing.

Who Can Truly Benefit from a Consumer Portfolio Services Car Loan?

The primary beneficiaries of a Consumer Portfolio Services car loan are individuals who face significant hurdles with traditional lending institutions. If you’ve been turned down for a car loan due to a low credit score, a history of late payments, or past financial difficulties, CPS could be a viable option. They are often considered a "second-chance" lender.

Based on my experience, many individuals who felt stuck due to their credit history have found a path to vehicle ownership through lenders like CPS. It’s not just about getting a car; it’s about rebuilding credit and gaining financial mobility. This makes CPS a crucial player for those working to improve their financial standing.

The Application Process for a CPS Car Loan: A Step-by-Step Guide

Securing a Consumer Portfolio Services car loan typically follows a straightforward process, though it differs slightly from applying directly to a bank. Here’s what you can expect:

- Find a Participating Dealership: CPS operates through a network of franchised and independent auto dealerships. Your first step is to visit a dealership that partners with CPS. The sales team will often know which lenders they work with for various credit tiers.

- Select Your Vehicle: Work with the dealer to choose a car that fits your needs and, importantly, your budget. Keep in mind that for subprime loans, lenders often have specific criteria for vehicle age and mileage.

- Submit Your Application: The dealership will help you complete a credit application. This application will then be sent to various lenders, including CPS, to see who is willing to offer financing based on your credit profile.

- Underwriting and Approval: CPS will review your application, looking at factors beyond just your credit score. They consider your income, employment stability, debt-to-income ratio, and the vehicle you’ve chosen. If approved, the dealership will present you with the loan terms.

- Finalize the Loan: Once you agree to the terms, you’ll sign the necessary paperwork at the dealership, and you can drive off in your new car. CPS then becomes your loan servicer.

Pro Tips from Us: Before heading to the dealership, gather essential documents like proof of income (pay stubs, bank statements), proof of residence (utility bills), and identification. Being prepared can significantly streamline the application process and demonstrate your reliability.

Key Factors CPS Considers for Loan Approval

While CPS is more lenient than prime lenders, they still have specific criteria they evaluate to assess risk. Understanding these factors can help you improve your chances of approval for a Consumer Portfolio Services car loan:

- Income Stability and Employment History: CPS wants to ensure you have a consistent source of income to make your monthly payments. They typically look for stable employment, often preferring a minimum time on the job.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to manage new debt.

- Down Payment: A significant down payment can dramatically improve your approval chances. It reduces the amount you need to borrow and signals your commitment to the loan.

- Vehicle Choice: Lenders often have restrictions on the age, mileage, and even type of vehicle they will finance for subprime loans. Newer, lower-mileage vehicles are generally preferred as they hold their value better.

- Co-signer: If your credit history is particularly challenging, having a co-signer with good credit can greatly enhance your application. The co-signer essentially guarantees the loan, reducing the risk for CPS.

Common mistakes to avoid are: applying for a loan without understanding your current financial standing, choosing a vehicle that’s beyond your means, or not being transparent about your income. Honesty and preparation are your best allies.

Understanding Your CPS Car Loan Terms

When you’re approved for a Consumer Portfolio Services car loan, it’s crucial to thoroughly understand the terms before signing. Subprime loans inherently come with different characteristics than prime loans.

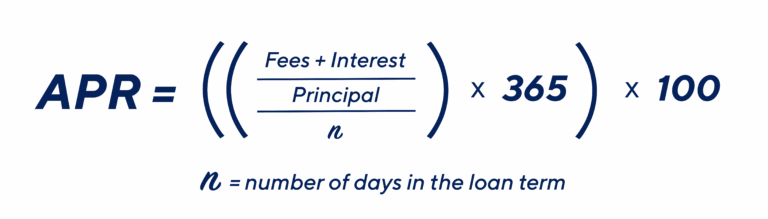

- Interest Rates (APRs): Expect higher Annual Percentage Rates (APRs) compared to traditional loans. This reflects the increased risk CPS takes on by lending to borrowers with less-than-perfect credit. While higher, these rates are often the gateway to obtaining financing when other options are closed.

- Loan Duration: Loan terms can vary, often ranging from 36 to 72 months or even longer. While longer terms mean lower monthly payments, they also mean you pay more interest over the life of the loan.

- Monthly Payments: Ensure your monthly payment is comfortably within your budget. Don’t stretch yourself too thin, as missing payments can further damage your credit.

- Fees and Charges: Be aware of any origination fees, late payment fees, or other charges outlined in your contract. Read the fine print carefully to avoid surprises.

Pro Tips from Us: Always ask for clarification on any term you don’t understand. Don’t feel pressured to sign until you’re completely comfortable with every aspect of the agreement. It’s your right to fully comprehend your financial commitment.

Managing Your CPS Car Loan: Payment Options and Best Practices

Once your Consumer Portfolio Services car loan is finalized, diligent management is key to successfully repaying it and improving your credit score.

CPS offers various convenient ways to make your monthly payments:

- Online Portal: Most borrowers find the online portal the easiest way to manage their account, view statements, and make payments.

- Phone Payments: You can typically make payments over the phone using a debit card or bank account.

- Mail: Traditional mail payments are also an option, though they require more planning to ensure on-time delivery.

- Auto-Pay: Setting up automatic payments directly from your bank account is an excellent way to ensure you never miss a due date.

The importance of on-time payments cannot be overstated. Every on-time payment reported to credit bureaus helps build a positive payment history, which is the single most significant factor in your credit score. This loan can be a powerful tool for credit rebuilding. For more tips on improving your credit score and managing debt effectively, check out our guide on How to Boost Your Credit Score Quickly (Simulated Internal Link).

If you anticipate missing a payment, or if an unexpected financial hardship arises, contact CPS immediately. Open communication can sometimes lead to temporary solutions or alternative arrangements, preventing late fees or adverse credit reporting.

Refinancing Your CPS Car Loan: When and How

Over time, as you make consistent on-time payments on your Consumer Portfolio Services car loan, your credit score is likely to improve. This opens up an exciting opportunity: refinancing. Refinancing means taking out a new loan, usually with a lower interest rate, to pay off your existing CPS loan.

When does it make sense to refinance?

- Improved Credit Score: If your credit score has significantly increased since you first took out the CPS loan.

- Lower Interest Rates: If current market interest rates are lower, or if your improved credit qualifies you for a much better rate.

- Reduced Monthly Payments: Refinancing can lead to a lower monthly payment, freeing up cash flow.

- Save Money on Interest: A lower interest rate over the remaining life of the loan can save you hundreds or even thousands of dollars.

From our observations, many borrowers successfully refinance their subprime auto loans within 12-24 months of consistent on-time payments. This strategy allows them to leverage their improved creditworthiness.

To refinance, you’ll typically apply to a new lender (a bank, credit union, or online lender). They will review your current credit and financial situation. If approved, the new lender will pay off CPS, and you’ll then make payments to your new lender under the new, hopefully more favorable, terms.

Pros and Cons of a Consumer Portfolio Services Car Loan

Like any financial product, a Consumer Portfolio Services car loan comes with its own set of advantages and disadvantages. A balanced perspective is crucial.

Pros:

- Access to Credit: Provides a vital financing option for individuals with poor or limited credit histories who might be denied elsewhere.

- Credit Building Opportunity: Making consistent, on-time payments can significantly improve your credit score, paving the way for better financial opportunities in the future.

- Quick Approval Process: Due to their specialized nature, CPS often has efficient approval processes, allowing you to drive away in a car relatively quickly.

- Dealer Network: Their extensive network of dealerships makes finding a car and financing in one place convenient.

Cons:

- Higher Interest Rates: Due to the higher risk associated with subprime lending, interest rates are typically much higher than prime auto loans. This means you pay more over the life of the loan.

- Potentially Stricter Terms: Loan terms might include shorter repayment periods or higher down payment requirements compared to prime loans.

- Limited Vehicle Choice: Lenders in the subprime market often have stricter requirements for the age, mileage, and type of vehicle they will finance, sometimes limiting your options.

- Focus on Subprime: While a pro for some, it means their products are specifically tailored for higher-risk borrowers, which might not be ideal if your credit is improving but not yet "prime."

Customer Service and Support: What to Expect from CPS

Managing your Consumer Portfolio Services car loan effectively involves knowing how to interact with their customer service. CPS offers various channels for support:

- Online Account Management: Their website typically provides a secure portal where you can view your loan details, payment history, and make payments.

- Phone Support: Customer service representatives are available by phone to answer questions, discuss payment options, and address concerns.

- Mail: You can also correspond with CPS via mail for official requests or inquiries.

When contacting customer service, have your account number and any relevant information ready. Clear and concise communication is key to resolving any issues efficiently.

Consumer Portfolio Services Reviews and Reputation

When researching Consumer Portfolio Services car loans, you’ll likely encounter a range of reviews online. It’s important to approach these with a critical eye. As a subprime lender, CPS often receives mixed reviews, which is common for companies operating in this segment of the market. Some customers praise them for providing an opportunity to get a car and rebuild credit, while others express frustration over high interest rates or perceived inflexibility.

It’s crucial to remember that individual experiences can vary widely. Factors like the specific dealership, the borrower’s understanding of the loan terms, and their ability to make on-time payments all play a role. Our advice is to always read your loan agreement thoroughly, understand all terms and conditions, and maintain open communication with your lender to ensure a positive experience.

Exploring Alternatives to CPS Car Loans

While a Consumer Portfolio Services car loan can be an excellent option for many, it’s always wise to explore alternatives if your situation allows.

- Credit Unions: Often offer competitive rates and more personalized service, especially for members. If your credit has slightly improved, they might be a good first stop.

- Other Subprime Lenders: There are other lenders in the subprime market; comparing offers from multiple sources can help you find the best terms.

- Buy Here Pay Here Dealerships: These dealerships act as both the seller and the lender. While they offer financing regardless of credit, their interest rates can be extremely high, and vehicle quality may vary. Proceed with extreme caution and thorough research.

- Saving for a Larger Down Payment: If possible, saving more for a down payment can significantly reduce the amount you need to finance, potentially qualifying you for better terms or a lower overall cost.

- Personal Loan (with caution): In some rare cases, if you have a stable job and need a small amount, a personal loan might be an option, but typically auto loans have lower rates.

Understanding the landscape of auto financing, particularly for subprime borrowers, is a crucial step towards making responsible financial decisions. For a deeper dive into understanding the nuances of subprime auto loans, you might find this external resource helpful: Investopedia on Subprime Auto Loans (External Link).

Conclusion: Driving Towards Financial Freedom with CPS

A Consumer Portfolio Services car loan represents a significant opportunity for individuals with challenging credit histories to gain vehicle ownership and, more importantly, to rebuild their financial standing. While they operate in a higher-risk segment, understanding their process, terms, and expectations can transform a potential obstacle into a stepping stone.

By carefully navigating the application, diligently managing your payments, and actively seeking opportunities to refinance as your credit improves, you can leverage a CPS loan to your advantage. Remember, informed decisions and responsible borrowing are the keys to turning a subprime loan into a pathway toward a healthier financial future. Start your journey to better credit and reliable transportation today, equipped with the knowledge to make the best choices for your needs.