Navigating the Road to Vehicle Ownership: Your Guide to the Easiest Car Loans with Bad Credit

Navigating the Road to Vehicle Ownership: Your Guide to the Easiest Car Loans with Bad Credit Carloan.Guidemechanic.com

Getting a car is often more than just a convenience; for many, it’s a necessity for work, family, and daily life. But what happens when past financial challenges have left you with less-than-perfect credit? The idea of securing an auto loan can feel daunting, even impossible.

As an expert blogger and professional SEO content writer, I understand this common predicament. The good news is, while it might require a slightly different approach, getting a car loan with bad credit is absolutely achievable. In this comprehensive guide, we’ll demystify the process, reveal the easiest paths to approval, and equip you with the knowledge to drive away in your next vehicle, all while potentially rebuilding your financial standing.

Navigating the Road to Vehicle Ownership: Your Guide to the Easiest Car Loans with Bad Credit

Understanding Bad Credit: More Than Just a Number

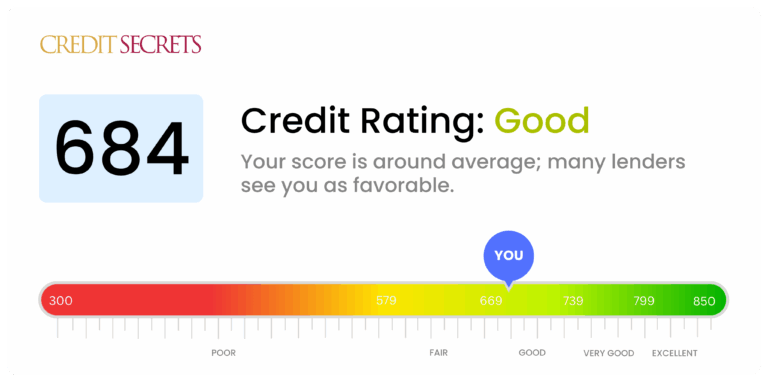

Before we dive into solutions, let’s clarify what "bad credit" truly means in the eyes of lenders. Your credit score, typically a FICO score, ranges from 300 to 850. Generally, a score below 600-620 is considered "subprime" or "bad credit."

This score is a numerical representation of your creditworthiness, reflecting your payment history, outstanding debts, length of credit history, new credit, and credit mix. A lower score signals a higher risk to lenders, making them hesitant to offer favorable terms, or even approve a loan at all.

Why Lenders Are Wary

From a lender’s perspective, a bad credit score indicates a higher likelihood of default. They view it as a historical pattern of missed payments, high debt, or other financial missteps. This doesn’t mean you’re a bad person; it simply means they need to mitigate their risk.

This risk mitigation often translates into higher interest rates, stricter terms, or requiring additional security measures for your loan. Understanding this perspective is the first step in successfully navigating the bad credit auto loan landscape.

Dispelling Myths and Setting Realistic Expectations

The internet is rife with promises of "guaranteed car loans with bad credit" or "no credit check auto loans." Based on my experience in the financial sector, it’s crucial to approach these claims with caution. While solutions exist, some common misconceptions need to be addressed head-on.

Myth 1: Guaranteed Approval for Everyone

No reputable lender can guarantee approval without some form of assessment. While some lenders specialize in bad credit, they still need to verify your income, stability, and ability to repay the loan. "Guaranteed approval" often comes with extremely high interest rates or hidden fees.

Myth 2: No Credit Check Loans Are the Best Option

"No credit check" loans often come from Buy Here Pay Here (BHPH) dealerships, which we’ll discuss in detail. While they bypass a hard credit inquiry, they typically charge significantly higher interest rates, and the loan terms can be less favorable. Furthermore, these loans sometimes don’t report to credit bureaus, meaning they won’t help you rebuild your credit.

Reality: Higher Interest Rates Are Common

With bad credit, expect to pay a higher Annual Percentage Rate (APR) compared to someone with excellent credit. This is the lender’s way of offsetting the perceived risk. Your goal should be to secure the most competitive rate you can, not necessarily the lowest overall rate on the market.

Focus on finding an affordable monthly payment that fits your budget. Remember, this loan can be a stepping stone to better credit, allowing you to refinance later at a lower rate.

Strategies for Securing an "Easiest" Car Loan with Bad Credit

Securing a car loan when your credit score isn’t ideal requires a strategic approach. It’s about presenting yourself as the most reliable borrower possible, despite your credit history. Here are the most effective strategies.

1. Target the Right Lenders

Not all lenders are created equal, especially when it comes to bad credit. Knowing where to look is half the battle.

Credit Unions: Your First Stop

Based on my experience, credit unions are often more forgiving than traditional banks. They are member-owned, meaning they prioritize their members’ financial well-being. They might be more willing to look beyond your credit score and consider your overall financial situation, your relationship with them, and your ability to repay.

If you’re already a member, start there. If not, consider joining one. Their rates for bad credit borrowers can often be more competitive.

Subprime Lenders/Specialized Bad Credit Lenders

These financial institutions specialize in lending to individuals with lower credit scores. Their business model is built around assessing and managing the risk associated with subprime borrowers. They understand that life happens and are set up to work with you.

You’ll often find these lenders through online marketplaces or specific dealerships that partner with them. Their approval criteria are tailored for those with credit challenges.

Online Loan Marketplaces: Comparison Shopping Made Easy

Websites like LendingTree, Auto Credit Express, or Carvana (which also offers financing) act as aggregators. You fill out one application, and they connect you with multiple lenders willing to work with bad credit. This allows you to compare offers without multiple hard inquiries impacting your score.

Pro tips from us: Always compare the APR, not just the monthly payment. A lower monthly payment over a longer term can mean paying significantly more interest overall.

Buy Here Pay Here (BHPH) Dealerships: A Last Resort

BHPH dealerships finance the car directly, cutting out third-party lenders. They often don’t perform traditional credit checks, focusing instead on your income stability. This makes them appear like an "easy" option.

However, common mistakes to avoid are rushing into a BHPH deal without understanding the drawbacks. BHPH vehicles often come with higher interest rates, limited inventory (older, higher mileage cars), and sometimes don’t report payments to credit bureaus, which means it won’t help rebuild your credit. Use them only if other options have been exhausted.

2. Strengthen Your Loan Application

Even with bad credit, you can significantly improve your chances of approval and potentially secure better terms by strengthening other aspects of your application.

A. Make a Larger Down Payment

This is perhaps the most impactful strategy. A substantial down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It shows commitment and financial responsibility.

Based on my experience, even 10-20% down can make a significant difference in a lender’s decision and your interest rate. It also reduces your monthly payments and the total interest paid over the life of the loan.

B. Find a Co-Signer with Good Credit

A co-signer is someone with good credit who agrees to take on responsibility for the loan if you default. This provides a safety net for the lender, significantly increasing your approval odds.

Choose a co-signer carefully, as their credit will be impacted if you miss payments. Ensure both parties understand the full implications before proceeding. This is a powerful tool, but it requires trust and responsibility.

C. Provide Proof of Stable Income

Lenders want assurance that you can consistently make your payments. Having a steady job with verifiable income is crucial. Be prepared to show pay stubs, bank statements, or tax returns.

A low debt-to-income (DTI) ratio is also favorable. Your DTI is the percentage of your gross monthly income that goes towards paying your monthly debt payments. Lenders prefer a DTI of 43% or lower.

D. Choose the Right Vehicle

Opt for an affordable, reliable used car rather than a brand-new, expensive model. Lenders are more comfortable financing a less expensive vehicle, as it reduces their exposure.

An affordable car means lower monthly payments, which is easier for you to manage and less risky for the lender. It also leaves more room in your budget for other expenses.

E. Get Pre-Approved

Seeking pre-approval from multiple lenders is a smart move. It involves a soft credit inquiry (which doesn’t harm your score) and gives you a realistic idea of how much you can borrow and at what interest rate.

Pre-approval empowers you to shop like a cash buyer, knowing your budget beforehand. This prevents you from falling in love with a car you can’t afford and gives you leverage during negotiations at the dealership.

3. Improve Your Credit Score (Even Slightly)

While you’re looking for a loan, take steps to improve your credit score. Even a few points can make a difference.

- Check Your Credit Report for Errors: Get free copies from AnnualCreditReport.com. Dispute any inaccuracies immediately. Errors are surprisingly common and can drag down your score.

- Pay Bills on Time: This is the most crucial factor. Even if it’s just your utility bills or a small credit card payment, consistent on-time payments demonstrate responsibility.

- Reduce Credit Card Balances: Lowering your credit utilization ratio (how much credit you’re using vs. your total available credit) can quickly boost your score. Aim to keep balances below 30% of your credit limit.

- Consider a Secured Credit Card: If you don’t have active credit, a secured credit card requires a deposit, acting as your credit limit. Using it responsibly and paying on time can build a positive credit history.

The Application Process: What to Expect

Once you’ve identified potential lenders and strengthened your application, the actual process isn’t as intimidating as it seems.

- Gather Your Documents: Have everything ready: driver’s license, proof of income (pay stubs, tax returns), proof of residence (utility bill), bank statements, and references if requested.

- Fill Out Applications Carefully: Be honest and thorough. Inaccurate information can lead to delays or rejection.

- Understand the Terms: Pay close attention to the APR, loan term, and any fees. Don’t be afraid to ask questions. If something isn’t clear, ask for clarification.

- Negotiate (Yes, Even with Bad Credit!): While your negotiation power might be limited, you can still try to negotiate the interest rate or the price of the car. Having pre-approval offers gives you leverage.

- Read the Fine Print: Before signing, read the entire contract. Understand all clauses, especially those related to late payments, repossession, and early payoff penalties.

Common Mistakes to Avoid When Seeking a Bad Credit Car Loan

Navigating bad credit auto financing can be tricky. Based on my experience, here are some common pitfalls that borrowers often fall into. Avoiding these can save you money and stress.

1. Applying Everywhere Indiscriminately

Each time you apply for credit, a "hard inquiry" is typically placed on your credit report, which can temporarily lower your score. While credit scoring models group similar inquiries (like auto loans) within a short period (usually 14-45 days) as a single event, applying broadly over a long stretch can be detrimental.

Pro tip from us: Use pre-qualification processes, which often only involve a soft inquiry, to gauge your options before committing to full applications.

2. Ignoring the APR and Focusing Only on Monthly Payments

Dealerships might try to sell you on a low monthly payment by extending the loan term significantly. While the payment might seem manageable, a longer loan term, especially with a high APR, means you’ll pay far more in interest over time.

Always look at the total cost of the loan and the APR. A slightly higher monthly payment over a shorter term can save you thousands in the long run.

3. Buying More Car Than You Can Afford

It’s tempting to want the newest model with all the bells and whistles. However, with bad credit, your priority should be reliable transportation that fits comfortably within your budget. Overextending yourself financially can lead to missed payments, further damaging your credit, and potentially repossession.

Factor in not just the loan payment, but also insurance, maintenance, and fuel costs.

4. Not Reading the Contract Thoroughly

This cannot be stressed enough. The loan contract is a legally binding document. It contains all the terms and conditions, including interest rates, fees, penalties for late payments, and repossession policies.

Common mistakes to avoid are signing without fully understanding every clause. If something is unclear, ask for an explanation or even take the contract home to review before signing.

5. Falling for "Guaranteed" or "No Credit Check" Scams

As mentioned earlier, legitimate lenders don’t offer "guaranteed approval." Similarly, "no credit check" loans often come with predatory interest rates and unfavorable terms. If an offer sounds too good to be true, it almost certainly is.

Stick with reputable lenders and dealerships, even if it means a slightly more rigorous application process.

Pro Tips from an Expert Blogger for Bad Credit Car Loans

Beyond the practical steps, adopting a strategic mindset can significantly improve your car loan journey.

- Be Honest and Transparent: Don’t try to hide your credit history or financial challenges. Lenders appreciate honesty. Being upfront allows them to work with you more effectively to find a viable solution.

- Focus on Rebuilding, Not Just Buying: View this car loan as an opportunity. Making timely payments can be a powerful tool for rebuilding your credit score. This will open doors to better financial products in the future.

- Consider a Short-Term Loan Strategy: If you’re stuck with a high-interest loan initially, plan to refinance it once your credit score improves (typically after 12-18 months of on-time payments). This can save you a substantial amount of money.

- Don’t Be Afraid to Walk Away: If the terms are unfavorable, the dealer is pressuring you, or you simply don’t feel comfortable, be prepared to walk away. There are always other options and other cars. Patience can pay off.

- Leverage Technology: Use online calculators to estimate payments and compare loans. Many websites offer tools to help you understand your budget and the impact of different loan terms. For deeper insights into managing your finances, you might find resources from the Consumer Financial Protection Bureau (CFPB) very helpful. External Link: Consumer Financial Protection Bureau – Auto Loans

- Understand Total Cost of Ownership: Beyond the loan, remember to budget for insurance, maintenance, and fuel. A low car payment won’t help if other car-related expenses break your budget. For more details on budgeting and financial planning, you can read our guide on "Understanding Car Loan Interest Rates". (Simulated internal link)

Beyond the Loan: Using Your Car Loan to Rebuild Credit

Getting approved for a car loan with bad credit isn’t just about driving away in a new vehicle; it’s a golden opportunity to improve your financial future.

Making Timely Payments is Key

Your payment history is the single most important factor in your credit score. Consistently making your car loan payments on time, every month, will have a profoundly positive impact on your credit report. Each on-time payment demonstrates your ability to manage debt responsibly.

This consistent positive reporting will gradually outweigh past negative marks, showing future lenders that you are a reliable borrower.

The Impact on Your Credit Score

As your credit score improves, you’ll gain access to better financial products, lower interest rates on future loans (including refinancing your current car loan), and even better rates on insurance. It’s a snowball effect that starts with discipline and consistency.

For more information on improving your credit, check out our article: "Improving Your Credit Score Fast: Actionable Steps for a Better Financial Future" (Simulated internal link).

Conclusion: Your Journey to Car Ownership and Financial Improvement

Securing an "easiest" car loan with bad credit is entirely within your reach. It requires a blend of realistic expectations, diligent research, and a strategic approach. By understanding your credit situation, targeting the right lenders, strengthening your application, and avoiding common mistakes, you can successfully navigate this journey.

Remember, this isn’t just about getting a car; it’s about taking a proactive step towards rebuilding your financial health. Every on-time payment you make will contribute to a stronger credit score, opening doors to a brighter financial future. Don’t let past credit challenges deter you. With the right knowledge and effort, you can hit the road with confidence.