Navigating the Road to Your Dream Car: A Comprehensive Guide to Choosing the Right Car Loan Providers

Navigating the Road to Your Dream Car: A Comprehensive Guide to Choosing the Right Car Loan Providers Carloan.Guidemechanic.com

The excitement of buying a new car is undeniable, whether it’s the sleek new model you’ve been eyeing or a reliable pre-owned vehicle perfect for your daily commute. However, for most people, this significant purchase isn’t possible without financial assistance. This is where car loan providers step in, offering the necessary funds to turn your automotive dreams into reality. But with a multitude of options available, how do you navigate this complex landscape to find the best fit for your needs?

Choosing the right car loan provider is arguably as crucial as selecting the car itself. A well-informed decision can save you thousands of dollars over the life of the loan, while a hasty one can lead to unnecessary financial strain. This comprehensive guide will equip you with the knowledge and insights needed to make smart choices, ensuring you drive away with not just a great car, but also a great deal. We’ll delve deep into the various types of providers, what factors to prioritize, and share expert tips to secure the most favorable terms.

Navigating the Road to Your Dream Car: A Comprehensive Guide to Choosing the Right Car Loan Providers

Understanding the Diverse Landscape of Car Loan Providers

The world of auto financing is broad, featuring several distinct types of lenders, each with its own advantages and disadvantages. Knowing these differences is the first step toward making an educated decision. Based on my experience in the financial sector, understanding these categories is paramount before you even start comparing rates.

1. Traditional Banks

Banks are often the first place people consider for a car loan, and for good reason. They are established financial institutions with a long history of lending. Major national banks and smaller community banks alike offer a range of auto loan products.

Their stability and widespread presence provide a sense of security for many borrowers. Banks typically offer competitive interest rates, especially to applicants with excellent credit scores. They also often have robust online platforms and customer service, making the application and management process relatively straightforward. However, their approval processes can sometimes be more stringent, and they might have less flexibility with borrowers who have less-than-perfect credit.

2. Credit Unions

Credit unions are member-owned, non-profit financial cooperatives. This unique structure often translates into significant benefits for their members, including car loan applicants. They are known for prioritizing member financial well-being over profit generation.

One of the primary advantages of credit unions is their typically lower interest rates compared to traditional banks. They also often have more flexible lending criteria and a more personalized approach to customer service, which can be particularly helpful for those with unique financial situations. To access these benefits, you usually need to become a member, which often involves meeting specific criteria like living in a certain area or working for a particular employer.

3. Dealership Financing

When you’re at the dealership, signing the paperwork for your new vehicle, you’ll almost certainly be offered financing options directly through the dealer. This is known as dealership financing, and it’s incredibly convenient, allowing you to complete your car purchase and secure a loan all in one place.

Dealerships work with a network of lenders, including captive finance companies (owned by the car manufacturer, like Ford Credit or Toyota Financial Services) and various third-party banks and finance companies. They can often offer promotional rates, especially on new vehicles, or special incentives. While convenient, the interest rate offered by a dealership might not always be the absolute best available, as their primary goal is to sell you a car, not necessarily to find you the cheapest loan.

4. Online Lenders

The digital age has brought forth a new breed of car loan providers: online lenders. These companies operate entirely online, streamlining the application and approval process. Their digital-first approach often translates into speed and efficiency, with many offering instant pre-approvals.

Online lenders typically have lower overhead costs than traditional brick-and-mortar institutions, which can sometimes allow them to offer highly competitive interest rates. They also specialize in a wide range of credit profiles, from excellent to subprime, making them a valuable option for borrowers who might struggle to get approved elsewhere. However, the lack of a physical presence might be a drawback for those who prefer face-to-face interaction or require more personalized guidance.

Key Factors to Consider When Evaluating Car Loan Providers

Choosing among the myriad of car loan providers can feel overwhelming. To simplify the process and ensure you make the best decision, focus on these critical factors. Based on my experience, overlooking any of these can lead to long-term financial regrets.

1. Interest Rates (Annual Percentage Rate – APR)

The interest rate is arguably the most critical factor influencing the total cost of your car loan. It’s the percentage of the loan amount that the lender charges you for borrowing their money. While often quoted as an interest rate, always look at the Annual Percentage Rate (APR).

The APR includes not only the interest rate but also any additional fees associated with the loan, giving you a more accurate picture of the total cost of borrowing. A lower APR directly translates to lower monthly payments and less money paid over the life of the loan. Even a seemingly small difference in APR can save you hundreds or even thousands of dollars on a car loan.

2. Loan Terms and Repayment Period

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor significantly impacts your monthly payment and the total interest you’ll pay. A longer loan term means lower monthly payments, which can make a car seem more affordable in the short term.

However, a longer term also means you’ll pay more in total interest over the life of the loan. Furthermore, you risk owing more on the car than it’s worth (being "upside down" or "underwater") as it depreciates, especially if you extend the loan too far. Pro tips from us: Aim for the shortest loan term you can comfortably afford, balancing monthly payments with the total cost.

3. Fees and Charges

Beyond the interest rate, various fees can add to the overall cost of your car loan. These can vary significantly between car loan providers. It’s crucial to ask about and understand all potential fees before signing any agreement.

Common fees include origination fees (for processing the loan), documentation fees, late payment fees, and sometimes even prepayment penalties if you pay off the loan early. While less common for car loans, always confirm there are no hidden charges. A transparent lender will clearly outline all fees upfront.

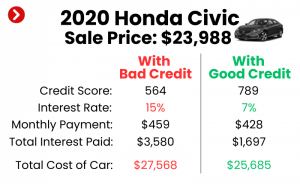

4. Credit Score Requirements

Your credit score is a major determinant of the interest rate and terms you’ll be offered. Car loan providers use your credit score to assess your creditworthiness and the risk involved in lending to you. Generally, the higher your credit score, the better the interest rate you can expect.

Lenders categorize borrowers into different tiers based on their credit scores (e.g., excellent, good, fair, poor). If you have a lower credit score, you might still qualify for a loan, but it will likely come with a higher interest rate to offset the perceived risk. Understanding your credit score before you apply can help you set realistic expectations and identify areas for improvement. For a deeper dive into improving your credit score, check out our guide on .

5. Customer Service and Reputation

While often overlooked, the quality of a car loan provider’s customer service and their overall reputation can greatly influence your borrowing experience. You want a lender that is responsive, transparent, and easy to communicate with if issues arise.

Researching online reviews, checking ratings with organizations like the Better Business Bureau, and asking for recommendations can provide valuable insights. A reputable lender will have clear communication channels and a history of treating customers fairly. Common mistakes to avoid are focusing solely on rates and neglecting the potential headache of dealing with a poorly rated provider.

6. Application Process and Speed of Approval

The ease and speed of the loan application and approval process can be a significant factor, especially if you’re in a hurry to purchase a vehicle. Some providers offer fully online applications with instant pre-approvals, while others may require more paperwork and a longer waiting period.

Consider your own preferences. Do you prefer a quick digital process, or are you comfortable with a more traditional, in-person approach? Online lenders and some credit unions are often lauded for their streamlined processes. Always ensure that a quick approval doesn’t come at the expense of a thorough understanding of the terms.

7. Pre-approval Options

Getting pre-approved for a car loan before you even step foot in a dealership is one of the smartest moves you can make. Pre-approval means a lender has reviewed your financial information and conditionally agreed to lend you a specific amount at a certain interest rate.

This process gives you significant leverage at the dealership. You walk in knowing your budget and what kind of interest rate you qualify for, essentially becoming a cash buyer in the eyes of the dealer. This allows you to negotiate the car price more effectively, separate from the financing discussion. Based on my experience, pre-approval empowers you and prevents you from being swayed by less favorable dealer financing offers.

The Car Loan Application Process: A Step-by-Step Guide

Securing a car loan doesn’t have to be a daunting task. By following a structured approach, you can navigate the process efficiently and confidently.

1. Assess Your Financial Situation and Budget

Before you even think about looking at cars, determine how much you can truly afford. This isn’t just about the monthly payment; it’s about the total cost of ownership, including insurance, fuel, maintenance, and the loan itself. Use online calculators to estimate potential monthly payments based on different loan amounts, interest rates, and terms.

Also, check your credit score. Knowing where you stand financially will help you set realistic expectations for interest rates and loan approvals. Aim to save for a down payment, as a larger down payment reduces the amount you need to borrow and can lead to better loan terms.

2. Gather Necessary Documents

Lenders will require various documents to verify your identity, income, and financial stability. Having these ready in advance can significantly speed up the application process.

Typically, you’ll need:

- Proof of identity (driver’s license, passport).

- Proof of residence (utility bill, lease agreement).

- Proof of income (pay stubs, tax returns, bank statements).

- Social Security number.

- Vehicle information (if you’ve already chosen a car).

3. Get Pre-approved by Multiple Car Loan Providers

As discussed, pre-approval is a game-changer. Apply to at least 2-3 different car loan providers – banks, credit unions, and online lenders – to get a range of offers. Remember, these initial applications are usually "soft inquiries" on your credit report, which don’t affect your score.

Once you have a pre-approval in hand, you have a solid benchmark. This allows you to shop for your car with confidence, knowing exactly what you can afford and what interest rate you qualify for.

4. Compare Offers Thoroughly

Don’t just look at the monthly payment. Compare the APR, total interest paid over the loan term, any fees, and the overall flexibility of each offer. Create a simple spreadsheet if needed to visualize the differences.

Pay close attention to the fine print. Are there any prepayment penalties? What are the late payment fees? Which offer provides the best value and terms for your specific financial situation?

5. Negotiate and Finalize

With a pre-approval offer from an outside lender, you can now approach the dealership with significant leverage. Ask the dealer if they can beat your pre-approved rate. They often have access to various lenders and might be able to find an even better deal, especially if they want to earn your business.

Once you’ve settled on a vehicle and the financing, review all loan documents carefully before signing. Ensure all terms, rates, and fees match what was discussed and agreed upon. Don’t feel rushed – ask questions until you fully understand every detail.

Types of Car Loans and How Providers Cater to Them

Car loan providers offer different products designed to meet various consumer needs and vehicle types. Understanding these distinctions helps you pinpoint the right loan for your situation.

1. New Car Loans

These loans are specifically for brand-new vehicles purchased directly from a dealership. New car loans typically come with the lowest interest rates because new cars are less risky collateral for lenders; they hold their value better initially and have fewer immediate maintenance concerns.

Providers are usually keen to offer competitive rates for new vehicles, and manufacturers often provide special financing incentives through their captive finance companies. If you’re weighing the pros and cons of new vs. used vehicles, our article on offers valuable insights.

2. Used Car Loans

Used car loans finance pre-owned vehicles. While still very common, they generally have slightly higher interest rates than new car loans. This is due to the higher perceived risk for the lender, as used cars can have unknown maintenance histories and depreciate more rapidly.

Despite this, excellent credit can still secure very favorable rates on used car loans from most car loan providers. The age and mileage of the used car can also influence the loan terms and interest rate offered.

3. Refinancing Car Loans

Refinancing involves taking out a new loan to pay off an existing car loan, ideally at a lower interest rate or with more favorable terms. This is a strategy many consumers use to save money or adjust their monthly payments.

Car loan providers, particularly online lenders and credit unions, actively compete for refinancing business. It’s a great option if your credit score has improved since you first took out the loan, if interest rates have dropped, or if you simply want to adjust your monthly payment.

4. Bad Credit Car Loans

For individuals with low credit scores (often below 620-660 FICO), securing a traditional car loan can be challenging. However, many car loan providers specialize in "bad credit" or "subprime" auto loans.

These loans typically come with significantly higher interest rates to compensate lenders for the increased risk. While more expensive, they offer an opportunity for individuals to purchase a car and, crucially, to rebuild their credit history through consistent, on-time payments. Online lenders and some specialized finance companies are particularly prominent in this segment.

Pro Tips for Securing the Best Car Loan

Navigating the car loan market can be complex, but armed with these expert strategies, you can significantly improve your chances of securing the most favorable terms. These are lessons learned from years in the financial industry.

- Improve Your Credit Score: This is fundamental. Even a modest improvement can unlock better interest rates. Pay down existing debts, make all payments on time, and avoid opening new credit accounts in the months leading up to your car loan application.

- Save for a Substantial Down Payment: The more money you put down upfront, the less you need to borrow. This reduces your monthly payments, lowers the total interest paid, and shows lenders you’re a serious and responsible borrower, often leading to better rates.

- Shop Around Aggressively: Never take the first offer, especially from a dealership. Compare rates from at least three to four different car loan providers – banks, credit unions, and online lenders. Competition works in your favor.

- Understand the Total Cost, Not Just Monthly Payments: Dealers often focus on making monthly payments seem low by extending loan terms. Always ask for the total amount you will pay over the life of the loan. A lower monthly payment over a longer term often means paying significantly more in total interest.

- Read the Fine Print: Before signing anything, thoroughly read and understand all loan documents. Look for prepayment penalties, late fees, and any other clauses that could impact you. If something isn’t clear, ask for clarification.

- Leverage Pre-approval: As mentioned, walking into a dealership with a pre-approved loan from an outside lender gives you immense negotiating power. It separates the car price negotiation from the financing, allowing you to focus on getting the best deal on the vehicle itself.

When to Consider Refinancing Your Car Loan

Refinancing isn’t just for mortgages; it’s a powerful tool for car owners too. Knowing when to consider this option can save you a significant amount of money or provide much-needed financial relief.

- Interest Rates Have Dropped: If market interest rates have decreased significantly since you took out your original loan, you might qualify for a lower rate now.

- Your Credit Score Has Improved: If you’ve diligently worked on improving your credit score since your initial purchase, you’re likely seen as a less risky borrower and can qualify for better terms.

- Your Financial Situation Has Changed: Perhaps you’ve received a promotion, paid off other debts, or simply have more disposable income. Refinancing could help you shorten your loan term and pay off the car faster, saving on interest.

- You Want to Lower Your Monthly Payments: If you’re experiencing financial hardship, refinancing to a longer term (though not always recommended due to increased total interest) could reduce your monthly burden.

- You Want to Remove a Cosigner: If you needed a cosigner initially, but your credit has improved, refinancing allows you to take sole responsibility for the loan.

Pro tips for refinancing: Shop around just as diligently as you did for your original loan. Get quotes from multiple car loan providers, and compare the APR, new monthly payment, and total interest saved. Don’t forget to factor in any fees associated with the refinancing process. For up-to-date information on average interest rates, a reliable source like a reputable financial data provider can provide valuable data.

Common Pitfalls and How to Avoid Them

Even with the best intentions, borrowers can fall into common traps when securing a car loan. Being aware of these pitfalls can help you steer clear of costly mistakes.

- Ignoring the Annual Percentage Rate (APR): Many people focus solely on the monthly payment. This is a common mistake. The APR is the true cost of borrowing and gives you a holistic view. Always compare offers based on their APR, not just the monthly payment figure.

- Focusing Only on Monthly Payments: Dealerships are skilled at manipulating loan terms to achieve a desired monthly payment. They might extend the loan duration to 72 or even 84 months, making the payment seem affordable. However, this dramatically increases the total interest paid and means you’ll be "underwater" (owe more than the car is worth) for a longer period.

- Not Getting Pre-approved: As emphasized throughout this article, skipping pre-approval puts you at a significant disadvantage. You lose your negotiating power and risk accepting a higher interest rate from the dealer simply out of convenience.

- Accepting the First Offer: Whether it’s from your bank or the dealership, never settle for the first loan offer you receive. Always compare at least three to four offers from different car loan providers to ensure you’re getting the best possible rate and terms.

- Over-extending Loan Terms: While a longer loan term reduces your monthly payment, it almost always means paying significantly more interest over time. It also increases the risk of negative equity, where your car is worth less than what you owe on it. Aim for the shortest term you can comfortably manage.

Conclusion: Your Smart Path to Car Ownership

Securing a car loan is a significant financial decision that impacts your budget for years to come. By approaching the process with knowledge and strategic planning, you can avoid common pitfalls and ensure you get the best possible deal. The journey to finding your dream car should be exciting, not financially stressful.

Remember to thoroughly research different car loan providers – from traditional banks and credit unions to modern online lenders and dealership financing options. Prioritize understanding the Annual Percentage Rate (APR), scrutinize all fees, and always, always get pre-approved before you step foot in a dealership. By focusing on the total cost of the loan, not just the monthly payment, and leveraging competition among lenders, you empower yourself to make a truly informed choice.

With the insights provided in this comprehensive guide, you are now well-equipped to navigate the complex world of auto financing. Take your time, compare diligently, and confidently choose the car loan provider that best fits your financial landscape. Your perfect ride, coupled with a smart financing plan, awaits!