Navigating the Road to Your Dream Car: A Comprehensive Guide to First Convenience Bank Car Loans

Navigating the Road to Your Dream Car: A Comprehensive Guide to First Convenience Bank Car Loans Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect. Whether it’s the allure of a brand-new model or the practicality of a reliable pre-owned car, securing the right financing is often the critical first step. Among the myriad of financial institutions, First Convenience Bank stands as a notable option for many prospective car buyers. But what exactly does a First Convenience Bank car loan entail? How does their process work, and what can you expect?

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto financing. My goal with this comprehensive guide is to provide you with an in-depth understanding of First Convenience Bank’s offerings, helping you make an informed decision that aligns with your financial goals. This isn’t just about getting a loan; it’s about understanding the entire ecosystem of auto financing with a trusted partner.

Navigating the Road to Your Dream Car: A Comprehensive Guide to First Convenience Bank Car Loans

Understanding First Convenience Bank and Its Approach to Auto Financing

First Convenience Bank (FCB) has carved out a unique niche in the banking sector, primarily serving customers through in-store branches, often located within retail giants like Walmart. This strategic placement makes them highly accessible, offering banking services where people already shop. When it comes to auto financing, FCB aims to extend this same convenience and personalized service.

Their philosophy often revolves around fostering relationships with their customers. Unlike some larger, more impersonal lenders, FCB often emphasizes a community-bank feel, even within its expansive reach. This can translate into a more human-centric approach when evaluating loan applications and assisting customers through the financing process. They understand that a car is more than just transportation; it’s a vital part of many people’s daily lives.

The First Convenience Bank Car Loan Landscape: What They Offer

First Convenience Bank provides a range of auto loan products designed to cater to different needs and financial situations. Understanding these options is the first step toward finding the perfect fit for your new vehicle.

New Car Loans

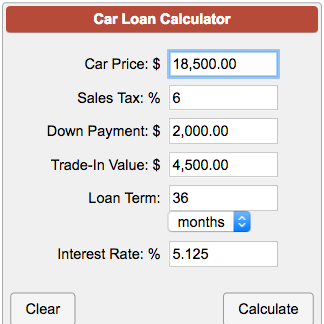

If you’re dreaming of that brand-new car with the latest features, FCB offers financing solutions tailored for new vehicle purchases. These loans typically come with competitive interest rates, often reflecting the lower risk associated with financing a new car. The terms can be flexible, allowing you to choose a repayment schedule that suits your budget.

When considering a new car loan, it’s crucial to look beyond just the monthly payment. We advise examining the total cost of the loan over its entire term. A lower monthly payment might seem appealing, but if it extends the loan term significantly, you could end up paying more in interest over time.

Used Car Loans

For those who prefer the value and cost-effectiveness of a pre-owned vehicle, First Convenience Bank also provides used car loans. These loans are designed for vehicles that have had previous owners but still offer plenty of life and utility. While interest rates for used car loans might be slightly higher than for new cars due to perceived increased risk, FCB strives to offer competitive rates based on the vehicle’s age, mileage, and your creditworthiness.

Pro Tip from us: When considering a used car loan, always get a pre-purchase inspection from an independent mechanic. This small investment can save you from significant repair costs down the road, ensuring your financed vehicle is a sound investment.

Auto Loan Refinancing Options

Perhaps you already have a car loan but are looking for a better deal. First Convenience Bank also offers auto loan refinancing. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. This can significantly reduce your monthly payments or the total interest paid over the life of the loan.

Based on my experience, refinancing is often a smart move if your credit score has improved significantly since you first took out the loan, or if market interest rates have dropped. It’s also beneficial if your current loan has an unmanageably high interest rate or if you want to adjust your loan term to better fit your current financial situation. Don’t assume your current rate is the best you can get; always explore refinancing possibilities.

Decoding the Application Process for a First Convenience Bank Car Loan

Applying for an auto loan can seem daunting, but First Convenience Bank aims to make the process as straightforward as possible. Understanding the steps involved will help you prepare and navigate it smoothly.

Step-by-Step Application Guide

- Initial Inquiry & Research: Start by visiting an FCB branch or their website to understand their current loan products and rates. This initial research helps you gauge if they’re the right fit.

- Pre-qualification (Optional but Recommended): Many lenders, including FCB, offer a pre-qualification process. This usually involves a soft credit check, which doesn’t impact your credit score, and gives you an estimate of how much you might be approved for and at what interest rate.

- Gathering Documents: Once you’re ready to formally apply, you’ll need to compile all necessary documentation. Being prepared beforehand can significantly speed up the approval process.

- Formal Application Submission: You can typically apply in person at one of their convenient branch locations or, in some cases, online. During this stage, you’ll provide detailed financial information.

- Underwriting and Review: FCB’s loan officers will review your application, credit history, and supporting documents. This is where they assess your creditworthiness and ability to repay the loan.

- Loan Offer & Negotiation: If approved, you’ll receive a loan offer detailing the interest rate, term, and monthly payments. This is your opportunity to review everything carefully and ask any questions.

- Closing and Funding: Once you accept the terms, you’ll sign the necessary paperwork, and the funds will be disbursed, allowing you to purchase your vehicle.

Required Documents for a Smooth Application

To ensure a seamless application, have the following documents ready. Based on my experience in financial applications, having these prepared in advance is a game-changer.

- Proof of Identity: A valid government-issued photo ID (driver’s license, state ID).

- Proof of Income: Recent pay stubs (typically 2-3 months), W-2 forms, or tax returns if self-employed.

- Proof of Residency: Utility bills, lease agreement, or mortgage statements.

- Social Security Number: Essential for credit checks.

- Vehicle Information: If you’ve already chosen a car, bring details like the VIN, make, model, year, and selling price.

- Down Payment Documentation: Proof of funds if you’re making a down payment.

Key Factors Influencing Your First Convenience Bank Car Loan Approval & Terms

Several factors play a pivotal role in determining whether your First Convenience Bank car loan application is approved and what interest rate and terms you receive. Understanding these elements empowers you to strengthen your application.

Your Credit Score: The Cornerstone of Loan Approval

Your credit score is arguably the most significant factor lenders consider. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher credit score signals lower risk to lenders, often resulting in better interest rates and more favorable loan terms.

FCB, like most financial institutions, will use your credit score to assess your reliability. While there isn’t a single "minimum" score for approval, generally, scores in the "good" to "excellent" range (typically 670 and above) open the door to the most competitive rates. Don’t be discouraged by a lower score, however; FCB might still offer solutions, albeit potentially with higher interest rates.

Debt-to-Income Ratio (DTI): A Measure of Your Financial Capacity

Your Debt-to-Income (DTI) ratio is another critical metric. It compares your total monthly debt payments to your gross monthly income. Lenders use DTI to evaluate your ability to manage additional debt. A lower DTI indicates you have more disposable income to cover new loan payments, making you a less risky borrower.

Pro Tip from us: Aim for a DTI ratio below 36%, if possible. While some lenders might approve higher, keeping it lower demonstrates strong financial health and improves your chances of securing the best rates.

The Power of a Down Payment

Making a significant down payment on your car loan offers several advantages. Firstly, it reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan’s life. Secondly, it demonstrates your commitment and reduces the lender’s risk, potentially qualifying you for better terms.

Common mistakes to avoid are underestimating the impact of a down payment. Even a 10-20% down payment can make a substantial difference in your long-term costs and loan approval odds. It also helps in avoiding being "upside down" on your loan, where you owe more than the car is worth.

Loan Term: Balancing Monthly Payments and Total Cost

The loan term refers to the length of time you have to repay the loan. Shorter terms typically mean higher monthly payments but less interest paid overall. Longer terms result in lower monthly payments but accumulate more interest over time.

FCB offers various loan terms to suit different budgets. When choosing a term, it’s essential to strike a balance between an affordable monthly payment and the total cost of the loan. Don’t automatically opt for the longest term just for the lowest payment; calculate the total interest to ensure it’s a financially sound decision.

Vehicle Specifics: Age, Mileage, and Condition

The car itself plays a role, especially for used car loans. Lenders consider the vehicle’s age, mileage, and overall condition. Newer cars with lower mileage are generally seen as less risky collateral, often leading to more favorable loan terms. Older vehicles or those with very high mileage might have stricter lending criteria or higher interest rates.

Maximizing Your Chances: Tips for a Smooth First Convenience Bank Car Loan Application

Securing the best possible car loan from First Convenience Bank involves more than just filling out an application. Strategic preparation and smart decision-making can significantly improve your odds of approval and help you get the most favorable terms.

Pre-qualification vs. Pre-approval: Know the Difference

While often used interchangeably, pre-qualification and pre-approval serve different purposes. Pre-qualification gives you an estimate of what you might qualify for, using a soft credit pull. It’s a good starting point for budgeting. Pre-approval, on the other hand, involves a more thorough review and a hard credit pull, providing you with a conditional loan offer before you even pick out a car.

Pro tips from us: Always aim for pre-approval from First Convenience Bank before stepping onto a dealership lot. This gives you concrete buying power, allows you to negotiate as a cash buyer, and helps you stick to your budget without dealer financing pressure.

Proactively Gather Your Documentation

As mentioned earlier, having all your required documents ready before you apply can dramatically streamline the process. Don’t wait until you’re asked for a specific document; anticipate what will be needed and have it organized. This shows preparedness and can prevent delays in your loan approval.

Focus on Improving Your Credit Score

If you have time before applying, focus on boosting your credit score. This could involve paying down existing debts, disputing inaccuracies on your credit report, or making sure all your payments are on time. Even a small improvement can lead to better interest rates, saving you hundreds or even thousands of dollars over the life of the loan. For more insights on improving your credit score, check out our detailed guide on .

Negotiate the Car Price First, Then Talk Financing

This is a crucial piece of advice often overlooked. Always negotiate the vehicle’s price independently of the financing. Dealerships often try to combine the two, making it harder to discern if you’re getting a good deal on the car or the loan. By securing your financing with First Convenience Bank first, you can focus solely on getting the best price for the car.

Common Mistakes to Avoid Are:

- Applying to too many lenders at once: Multiple hard inquiries in a short period can negatively impact your credit score.

- Not checking your credit report beforehand: Errors can occur, and they can hinder your approval or lead to worse terms.

- Focusing solely on the monthly payment: Always consider the total cost of the loan over its entire term.

- Overlooking additional fees: Be aware of any origination fees, documentation fees, or other charges that might be added to your loan.

Understanding Interest Rates and Fees

Beyond the principal amount of your loan, interest rates and various fees significantly impact the total cost of your First Convenience Bank car loan. A clear understanding of these components is essential for smart financial planning.

How Interest Rates Are Determined

The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. Several factors influence the interest rate you’re offered:

- Your Credit Score: As discussed, a higher score generally means a lower rate.

- Loan Term: Shorter terms often come with slightly lower rates due to less risk for the lender.

- Market Conditions: Overall economic conditions and the prime rate set by the Federal Reserve can influence prevailing auto loan rates.

- Down Payment: A larger down payment can reduce the perceived risk, potentially leading to a better rate.

- Vehicle Type: New cars often have lower rates than used cars.

First Convenience Bank will assess these factors to determine a personalized interest rate for your loan. It’s important to remember that the rate you see advertised might not be the rate you qualify for; it often represents the best-case scenario for highly qualified borrowers.

Types of Fees to Expect

While First Convenience Bank aims for transparency, it’s wise to be aware of potential fees associated with car loans:

- Origination Fee: A fee charged by the lender for processing the loan. Not all lenders charge this for auto loans, but it’s worth asking.

- Late Payment Fees: Penalties incurred if your monthly payment is not made on time.

- Prepayment Penalties: Some loans might charge a fee if you pay off the loan early. This is less common with auto loans but always check your loan agreement.

- Documentation Fees: Often charged by dealerships, not necessarily the bank, but they can be rolled into your total financed amount.

Always ask First Convenience Bank for a clear breakdown of all potential fees before finalizing your loan agreement.

Comparing APR vs. Interest Rate

When reviewing a loan offer, you’ll likely see both an interest rate and an Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing the principal. The APR, however, represents the total cost of the loan over a year, including the interest rate plus any additional fees and charges.

Pro tips from us: Always compare APRs when looking at different loan offers. The APR provides a more accurate picture of the total cost of borrowing, allowing for a true apples-to-apples comparison between lenders.

Beyond Approval: Managing Your First Convenience Bank Car Loan

Getting approved for a car loan is a significant milestone, but effective management of your loan is crucial for your long-term financial health. First Convenience Bank provides various tools and options to help you stay on track.

Convenient Payment Options

FCB typically offers multiple convenient ways to make your monthly car loan payments. These often include:

- Online Banking: Easily set up recurring payments or make one-time payments through your FCB online account.

- Automatic Payments: Enroll in auto-pay to ensure payments are always made on time, potentially even qualifying for a slight interest rate discount.

- In-Branch Payments: Pay in person at any First Convenience Bank location.

- Mail: Send a check or money order through traditional mail.

Choosing an automatic payment option is often the safest bet to avoid late fees and maintain a good payment history, which is vital for your credit score.

Early Payoff Considerations

Paying off your car loan earlier than scheduled can save you a substantial amount in interest. If you find yourself with extra funds, such as a bonus or a tax refund, consider making additional principal payments. This directly reduces the amount you owe interest on.

Before making extra payments, always confirm with First Convenience Bank that there are no prepayment penalties. While uncommon for auto loans, it’s a good practice to verify this in your loan agreement. An early payoff can be a smart financial move.

What If You Face Financial Hardship?

Life can be unpredictable, and sometimes financial difficulties arise that make it challenging to meet your car loan payments. If you anticipate or encounter such a situation, it’s crucial to act proactively.

Pro tips from us: Contact First Convenience Bank immediately if you foresee issues with making payments. They may offer options such as deferment, forbearance, or loan modification, depending on your circumstances. Ignoring the problem will only worsen it, potentially leading to vehicle repossession and severe damage to your credit score. Open communication is key to finding a viable solution.

Pros and Cons of Choosing First Convenience Bank for Your Auto Loan

Every financial decision involves weighing the advantages and disadvantages. Here’s a balanced perspective on securing your auto loan through First Convenience Bank.

Benefits of First Convenience Bank Auto Loans

- Accessibility and Convenience: With numerous in-store branches, FCB offers unparalleled accessibility for in-person service and applications. This can be particularly helpful for those who prefer face-to-face interactions.

- Personalized Service: As a bank that emphasizes community and relationship banking, you might experience more personalized service compared to larger, purely online lenders. This can be reassuring when navigating complex financial decisions.

- Existing Customer Relationships: If you already bank with First Convenience Bank, leveraging an existing relationship can sometimes streamline the application process and potentially lead to better offers.

- Range of Products: They offer loans for new and used cars, plus refinancing options, providing flexibility for various needs.

- Local Presence: For many, having a local branch where they can speak to a loan officer directly offers peace of mind and trust.

Potential Drawbacks to Consider

- Geographic Limitations: While widespread in certain retail environments, FCB’s physical presence is not universal across all states. If you move or are not near one of their branches, direct access might be limited.

- Interest Rates May Vary: While competitive, their rates might not always be the absolute lowest available in the entire market, especially when compared to niche online lenders with very specific criteria. It always pays to compare.

- Specific Lending Criteria: Like all lenders, FCB has specific criteria for loan approval. If your credit profile falls outside their preferred range, approval might be challenging or come with less favorable terms.

- Less Digital-First: While they offer online services, some customers accustomed to fully digital, app-based lending experiences might find certain aspects less streamlined than pure online lenders. If you’re also considering personal loans, read our comparison of .

Frequently Asked Questions (FAQ)

Q1: What credit score do I need for a First Convenience Bank car loan?

While there’s no official minimum, generally, a credit score of 670 or higher (considered "good") will give you the best chance for competitive rates. However, FCB may consider applicants with lower scores depending on other factors like income and down payment.

Q2: Can I apply for a First Convenience Bank car loan online?

Yes, depending on their current offerings and your location, you can often start or complete the application process online, or visit one of their convenient in-store branches for personalized assistance.

Q3: Does First Convenience Bank offer pre-approval for car loans?

Yes, First Convenience Bank typically offers pre-approval. This allows you to know how much you can borrow and at what rate before you shop for a car, giving you stronger negotiating power.

Q4: What documents are required for a First Convenience Bank car loan application?

You’ll generally need proof of identity, income verification (pay stubs, W-2s), proof of residency, and your Social Security Number. If you’ve chosen a vehicle, you’ll also need its details.

Q5: Can I refinance my existing car loan with First Convenience Bank?

Yes, First Convenience Bank offers auto loan refinancing options. This can be beneficial if you want to lower your interest rate, reduce your monthly payments, or change your loan term.

Conclusion: Your Road Ahead with First Convenience Bank

Securing a car loan is a significant financial commitment that requires careful consideration. First Convenience Bank offers a compelling option for many, particularly those who value accessible in-person service, personalized attention, and a range of flexible auto financing products. By understanding their offerings, preparing your documentation, and strategically navigating the application process, you can significantly improve your chances of securing a First Convenience Bank car loan with favorable terms.

Remember, the goal isn’t just to get a loan, but to get the right loan that aligns with your financial well-being. Take the time to research, compare, and ask questions. With the insights provided in this comprehensive guide, you are now better equipped to make an informed decision and confidently drive away in your next vehicle, financed by a partner you trust. Happy driving!

External Link: For general guidance on understanding auto loans and your consumer rights, you can visit the Consumer Financial Protection Bureau (CFPB) website at https://www.consumerfinance.gov/consumer-tools/auto-loans/.