Navigating the Road to Your Dream Car: A Comprehensive Guide to Looking For A Car Loan

Navigating the Road to Your Dream Car: A Comprehensive Guide to Looking For A Car Loan Carloan.Guidemechanic.com

The journey to owning a new vehicle is often exciting, filled with visions of open roads and newfound freedom. However, before you can cruise off into the sunset, there’s a crucial step that many find daunting: securing the right car loan. Finding the perfect car financing can feel like a complex maze, but with the right knowledge and preparation, it becomes a straightforward path to unlocking your automotive aspirations.

This article is designed to be your ultimate guide, offering an in-depth look at everything you need to know when looking for a car loan. We’ll demystify the process, share expert insights, and equip you with the tools to make informed decisions. Our goal is to empower you to find a car loan that not only gets you behind the wheel but also fits comfortably within your financial landscape, ensuring a smooth ride for years to come.

Navigating the Road to Your Dream Car: A Comprehensive Guide to Looking For A Car Loan

Understanding Car Loans Before You Start Your Search

Before diving into applications and interest rates, it’s essential to grasp the fundamental concepts of car loans. A car loan is essentially an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that amount, plus interest, over a predetermined period. This understanding forms the bedrock of a successful financing journey.

Many people jump straight into car shopping without fully understanding how these financial products work. This often leads to confusion and less favorable terms down the line. Taking the time to educate yourself upfront can save you significant money and stress. It’s about empowering yourself as a consumer.

What Exactly Is a Car Loan?

At its core, a car loan is a secured loan, meaning the vehicle you purchase acts as collateral. If you fail to make your payments as agreed, the lender has the right to repossess the car. This security allows lenders to offer more competitive interest rates compared to unsecured loans, as their risk is mitigated.

The principal amount of the loan is the actual cost of the car you are financing. Over time, you will repay this principal along with the interest charged by the lender. Understanding this basic mechanism is the first step in responsibly managing your car purchase.

Exploring the Different Types of Car Loans

Not all car loans are created equal, and knowing the distinctions can significantly impact your search. The type of loan you choose can affect your interest rate, repayment terms, and even the vehicles you qualify for. It’s about finding the right fit for your specific circumstances.

First, there are new car loans and used car loans. New car loans often come with lower interest rates due to the vehicle’s higher value and lower risk of mechanical issues. Used car loans, while typically carrying slightly higher rates, allow you to finance a pre-owned vehicle, which can be a more budget-friendly option upfront.

Next, consider secured versus unsecured loans. As mentioned, most car loans are secured by the vehicle itself. Unsecured personal loans can be used to buy a car, but they are much rarer and typically carry much higher interest rates because there’s no collateral backing the loan. For car purchases, secured loans are the standard.

Finally, you’ll encounter direct lending and dealership financing. Direct lending involves applying for a loan directly with banks, credit unions, or online lenders before you visit a dealership. Dealership financing, on the other hand, is arranged through the car dealership, which acts as an intermediary with various lenders. We’ll delve deeper into these options later.

Key Terms You Must Understand

Navigating the world of car loans requires familiarity with specific terminology. These terms will frequently appear in loan offers and agreements, and a clear understanding will prevent any unwelcome surprises. Don’t be afraid to ask for clarification if something isn’t clear.

Annual Percentage Rate (APR) is perhaps the most critical term. It represents the true annual cost of borrowing money, encompassing not just the interest rate but also certain fees. Comparing APRs, not just interest rates, gives you the most accurate picture of a loan’s total cost. A lower APR means less money paid over the life of the loan.

The Loan Term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer term means lower monthly payments, it also means paying more in interest over time. Conversely, shorter terms have higher monthly payments but save you money on interest.

Principal is the original amount of money you borrow. As you make payments, a portion goes towards the principal and a portion towards interest. The Interest is the cost of borrowing the principal, calculated as a percentage of the outstanding loan balance.

A Down Payment is the initial sum of money you pay upfront towards the purchase of the car. Making a larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

Finally, a Co-signer is someone who agrees to be equally responsible for the loan if you are unable to make payments. This can be beneficial if you have a limited credit history or a lower credit score, as it provides additional assurance to the lender. However, it’s a significant commitment for the co-signer.

Based on my experience, many people overlook the importance of understanding these terms thoroughly. They simply look at the monthly payment without considering the total cost or the implications of a longer loan term. This can lead to financial strain and buyer’s remorse later on.

The Pre-Application Checklist: Gearing Up for Success

Success in securing a favorable car loan begins long before you even step foot in a dealership or fill out an online application. A well-prepared approach can significantly improve your chances of approval and help you lock in the best possible terms. This proactive stance puts you in a position of strength.

Think of this stage as your strategic planning phase. Just as you wouldn’t embark on a long road trip without checking your car’s fluids and tires, you shouldn’t pursue a car loan without first assessing your financial health. This preparation saves time and potential disappointment.

Check Your Credit Score: Your Financial Report Card

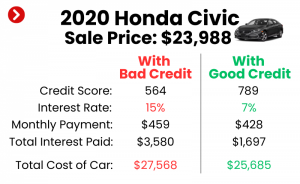

Your credit score is arguably the most influential factor in determining the interest rate you’ll be offered. Lenders use it as a snapshot of your creditworthiness, assessing your likelihood of repaying the loan based on past financial behavior. A higher credit score signals lower risk to lenders.

FICO scores, which range from 300 to 850, are widely used. Generally, a score of 700 or above is considered good, while scores in the excellent range (750+) qualify for the most competitive rates. If your score is lower, it doesn’t mean you can’t get a loan, but you might face higher interest rates.

It’s crucial to obtain your credit report from all three major bureaus (Equifax, Experian, TransUnion) and review them for accuracy. Errors can negatively impact your score. You are entitled to a free report from each bureau annually. provides more detailed strategies if you find your score needs improvement.

Determine Your Budget: How Much Can You Truly Afford?

Before you fall in love with a particular car, establish a realistic budget. This isn’t just about the car’s sticker price; it includes monthly loan payments, insurance, fuel, maintenance, and registration fees. Overlooking these additional costs can lead to financial strain.

A common guideline is that your total car expenses (payment, insurance, fuel) should not exceed 10-15% of your net monthly income. Also, consider your debt-to-income (DTI) ratio, which is the percentage of your gross monthly income that goes towards debt payments. Lenders typically prefer a DTI ratio below 36%.

Pro tips from us include creating a detailed spreadsheet of your monthly income and expenses. This allows you to see exactly how much disposable income you have available for a car payment without jeopardizing other financial goals. Be honest with yourself about what you can comfortably manage.

Save for a Down Payment: The Power of Upfront Cash

While it’s possible to get a car loan with no down payment, making one offers significant advantages. A substantial down payment reduces the amount you need to borrow, which lowers your monthly payments and the total interest you’ll pay over the loan term. It also reduces your loan-to-value (LTV) ratio, making you a less risky borrower.

A common recommendation is to aim for at least 10% for a used car and 20% for a new car. Beyond financial benefits, a larger down payment gives you immediate equity in the vehicle, protecting you from becoming "upside down" on your loan (owing more than the car is worth), which is particularly relevant in the initial years of ownership.

Gather Necessary Documents: Be Ready to Go

When you apply for a car loan, lenders will require several documents to verify your identity, income, and financial stability. Having these ready in advance streamlines the application process and prevents delays. Being organized shows you are a serious and prepared applicant.

Typically, you’ll need a valid driver’s license, proof of income (pay stubs, tax returns if self-employed), proof of residency (utility bill), and potentially bank statements. If you’re trading in a vehicle, you’ll also need its title and registration. Prepare a folder with all these documents to make the application process seamless.

Where to Look for a Car Loan: Your Lender Options

With your financial house in order, the next step is to explore where you can actually get a car loan. The lending landscape is diverse, offering various options, each with its own set of advantages and disadvantages. Understanding these differences will help you choose the best fit.

Don’t limit yourself to just one type of lender. Shopping around and comparing offers from multiple sources is one of the most effective strategies for securing a competitive interest rate and favorable terms. This competitive approach ensures you get the best deal.

Banks and Credit Unions: Traditional Lenders

Traditional financial institutions like banks and credit unions are popular choices for car loans. They often offer competitive rates, especially to customers with good credit, and provide a sense of security and familiarity. Many people prefer to work with institutions they already bank with.

Banks are typically larger, for-profit institutions. They offer a wide range of financial products and services and can provide competitive rates, particularly if you have an existing relationship with them. However, their approval criteria can sometimes be stricter.

Credit unions are non-profit organizations owned by their members. They are renowned for often offering lower interest rates and more flexible terms than traditional banks, as their primary goal is to serve their members. Becoming a member is usually straightforward, often requiring just a small deposit or meeting certain affiliation criteria.

Common mistakes to avoid are not checking with your existing bank or credit union first. Often, they offer special rates or expedited processes for current members. It’s always worth inquiring about their current auto loan offerings.

Online Lenders: Convenience and Variety

The digital age has brought forth a plethora of online lenders specializing in auto financing. These platforms offer unparalleled convenience, allowing you to apply and get pre-approved from the comfort of your home, often within minutes. This speed and accessibility are a major draw.

Online lenders typically have lower overhead costs than traditional banks, which can sometimes translate into more competitive interest rates. They also often cater to a broader range of credit profiles, including those with less-than-perfect credit, making them a valuable option for many.

When considering online lenders, always research their reputation, read customer reviews, and ensure they are legitimate and secure. Look for lenders with transparent terms and excellent customer service. This due diligence is crucial before sharing your personal financial information.

Dealership Financing: The On-Site Option

Dealership financing is often the most convenient option, as it allows you to handle the car purchase and loan application all in one place. Dealerships work with a network of lenders and can often present you with several financing options directly. This can save you time and effort.

However, convenience doesn’t always equate to the best deal. While dealerships can sometimes offer promotional rates from manufacturer-affiliated lenders, their primary goal is to sell cars. They may mark up interest rates to earn a commission, or they might steer you towards a loan that benefits them more than you.

It’s wise to enter the dealership with a pre-approved loan offer from a bank, credit union, or online lender. This gives you leverage during negotiations. If the dealership can beat your pre-approved rate, fantastic! If not, you have a solid backup. This strategy ensures you don’t overpay for financing.

The Application Process: Step-by-Step Guidance

Once you’ve done your research and identified potential lenders, it’s time to navigate the application process. This stage is where your preparation pays off, allowing you to confidently move towards securing your car loan. A structured approach minimizes stress and maximizes efficiency.

Remember, this isn’t just about getting approved; it’s about securing the best possible terms. Every step in this process is an opportunity to improve your financial outcome and ensure a smooth transaction.

Pre-Approval: Your Secret Weapon

Seeking pre-approval is arguably the most powerful step you can take when looking for a car loan. Pre-approval means a lender has reviewed your credit and financial information and determined that you qualify for a specific loan amount at a particular interest rate, usually for a set period (e.g., 30-60 days).

Why is pre-approval so crucial? First, it gives you a clear budget, so you know exactly how much car you can afford before you start shopping. This prevents you from falling in love with a vehicle outside your price range. Second, it transforms you into a cash buyer at the dealership, giving you significant negotiating power.

Based on my experience, walking into a dealership with a pre-approval letter in hand changes the dynamic entirely. You’re no longer solely dependent on their financing options, and they know they have to compete for your business. This often leads to better car prices and potentially even better financing offers from the dealership itself.

Comparing Loan Offers: Look Beyond the Monthly Payment

Once you have a few loan offers (ideally including a pre-approval), it’s time to compare them meticulously. Don’t just focus on the lowest monthly payment; this can be misleading if it comes with a significantly longer loan term or higher total interest paid. A comprehensive comparison is key.

Compare the Annual Percentage Rate (APR) first and foremost. This is the true cost of the loan. Then, look at the loan term and the total amount of interest you will pay over the life of the loan. Also, check for any fees, such as origination fees or prepayment penalties, which can add to the overall cost.

Create a side-by-side comparison. A slightly higher monthly payment over a shorter term can save you thousands in interest in the long run. Use online car loan calculators to visualize different scenarios and understand the impact of varying APRs and terms.

Submitting Your Application: The Final Push

Once you’ve selected the best loan offer, the final step is to formally submit your application and provide any remaining documentation the lender requires. This usually involves completing a detailed application form and signing various disclosures. Ensure all information is accurate and consistent.

Be prepared for the lender to perform a "hard inquiry" on your credit report at this stage. While this can temporarily ding your credit score by a few points, multiple hard inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are usually grouped as one by credit bureaus, recognizing that you are rate shopping.

If you are asked for additional documentation, provide it promptly. Clear communication and quick responses can expedite the final approval and funding process. Remember, the lender wants to verify your ability to repay the loan.

Understanding the Loan Agreement: Read Every Line

Before you sign any loan agreement, read it thoroughly, line by line. This document is a legally binding contract outlining your obligations and the lender’s terms. Do not hesitate to ask questions about anything you don’t understand.

Pay close attention to the APR, loan term, monthly payment amount, late payment penalties, and any clauses regarding early payoff. Ensure there are no hidden fees or unexpected conditions. If something seems off or confusing, get clarification before putting your signature on the dotted line. It’s your right to fully understand what you’re committing to.

Special Considerations for Your Car Loan Journey

While the general car loan process applies to most, certain situations require specific approaches. Understanding these nuances can save you time and help you navigate unique challenges or opportunities. These considerations add another layer of expertise to your car financing strategy.

Bad Credit Car Loans: A Path Forward

Having a low credit score or limited credit history can make securing a traditional car loan challenging, but it’s certainly not impossible. Many lenders specialize in bad credit car loans, often referred to as subprime loans. These loans help individuals rebuild their credit while getting the transportation they need.

Expect higher interest rates and potentially stricter terms with bad credit car loans. Lenders take on more risk, and they compensate for that risk through higher charges. However, making timely payments on a bad credit loan can significantly improve your credit score over time, paving the way for better rates in the future.

Strategies for securing a bad credit car loan include making a larger down payment, finding a co-signer with good credit, or considering a less expensive vehicle. Some dealerships also offer "buy here, pay here" options, but these often come with very high interest rates and should be approached with extreme caution. Always compare multiple offers.

Refinancing Your Car Loan: A Second Chance

If you’ve already secured a car loan but your financial situation has improved, or interest rates have dropped, refinancing your car loan might be a smart move. Refinancing involves taking out a new loan to pay off your existing car loan, ideally with better terms.

Common reasons to refinance include lowering your interest rate, reducing your monthly payments (by extending the term), or shortening your loan term (to save on total interest). If your credit score has significantly improved since you first took out the loan, you are a prime candidate for refinancing.

Before refinancing, compare the potential savings against any fees associated with the new loan. Calculate whether the interest savings outweigh any new costs. It’s a financial decision that requires careful evaluation, but it can lead to substantial long-term savings.

Leasing vs. Buying: A Quick Look

While this article focuses on looking for a car loan for a purchase, it’s worth a brief mention of leasing. Leasing a car is essentially renting it for a fixed period (typically 2-4 years) with mileage restrictions. At the end of the lease, you return the car or have the option to buy it.

Leasing often results in lower monthly payments than buying, as you’re only paying for the depreciation of the vehicle during the lease term, plus interest and fees. However, you don’t own the car, and you’re bound by mileage limits and wear-and-tear clauses. For those who enjoy driving new cars frequently and don’t drive excessive miles, leasing can be appealing. For long-term ownership and equity building, buying with a car loan is the way to go.

Post-Approval: Managing Your Car Loan Responsibly

Getting approved for a car loan is a significant achievement, but it’s just the beginning. Responsible management of your loan is crucial for maintaining your financial health and eventually achieving full ownership of your vehicle. This phase requires discipline and ongoing attention.

Your actions during the repayment period directly impact your credit score and future financial opportunities. Treating your car loan seriously is a testament to your financial maturity and commitment.

Making Timely Payments: The Golden Rule

The most critical aspect of managing your car loan is making every payment on time, every month. Late payments not only incur fees but also negatively impact your credit score, making it harder and more expensive to borrow money in the future. Consistency is key to building a strong credit history.

Consider setting up automatic payments from your bank account to avoid missing deadlines. Most lenders offer this convenient option. If you anticipate difficulty making a payment, contact your lender immediately. They may offer hardship options or payment deferrals, but communication is vital.

Understanding Early Payoff Options: Saving Money

Many car loans allow for early payoff without penalty, which can save you a substantial amount of money in interest. If your financial situation improves, making extra payments or paying off the loan entirely ahead of schedule is a smart financial move.

Always double-check your loan agreement for any prepayment penalties. While these are less common with car loans than with mortgages, they do exist. If no penalties are present, consider putting any unexpected windfalls, like a tax refund or bonus, towards your loan principal to accelerate your payoff.

Protecting Your Investment: Beyond the Loan

Remember that the car itself is the collateral for your loan. Protecting this asset is not only wise for your peace of mind but also a requirement from your lender. This means maintaining adequate insurance coverage and keeping the vehicle in good working condition.

Lenders typically require comprehensive and collision insurance coverage for the duration of the loan to protect their investment against damage or theft. provides more details on choosing the right coverage. Regular maintenance also ensures the car retains its value and remains reliable, reducing unexpected repair costs that could strain your ability to make loan payments.

Conclusion: Your Road to Car Loan Success

Looking for a car loan doesn’t have to be a stressful ordeal. By understanding the fundamentals, preparing thoroughly, exploring your lending options, and approaching the application process strategically, you can secure financing that empowers you to drive away in your dream car without financial regret. Remember, knowledge is power, and diligence is your greatest asset in this journey.

From checking your credit score and budgeting meticulously to comparing APRs and understanding your loan agreement, every step you take contributes to a more informed and advantageous outcome. Embrace the process, ask questions, and never settle for the first offer. Your financial future, and your new car, deserve your best effort. Start your car loan journey today with confidence and clarity, and enjoy the open road ahead!