Navigating the Road to Your Dream Car: A Comprehensive Guide to Securing Reliable Car Loans

Navigating the Road to Your Dream Car: A Comprehensive Guide to Securing Reliable Car Loans Carloan.Guidemechanic.com

The open road, the scent of a new car, the freedom of personal transportation – for many, owning a vehicle is an integral part of life. But before you hit the gas, there’s a crucial step: securing a car loan. This isn’t just about finding the lowest interest rate; it’s about finding a reliable car loan that aligns with your financial well-being and helps you achieve your dreams without unnecessary stress.

In this comprehensive guide, we’ll peel back the layers of car financing, offering insights, expert advice, and practical strategies to ensure your journey to car ownership is smooth and financially sound. Our goal is to equip you with the knowledge to make informed decisions, understand the nuances of the market, and ultimately drive away with confidence, knowing you’ve secured a truly dependable financing option.

Navigating the Road to Your Dream Car: A Comprehensive Guide to Securing Reliable Car Loans

What Exactly Makes a Car Loan "Reliable"? Beyond Just the Numbers

When we talk about reliable car loans, we’re referring to more than just the interest rate or the monthly payment. A truly reliable loan is one that is transparent, fair, sustainable, and comes from a trustworthy source. It’s about peace of mind throughout the entire loan term.

Based on my experience in the financial landscape, many people fixate solely on the Annual Percentage Rate (APR), which, while important, is only one piece of the puzzle. A low APR with hidden fees or restrictive terms can quickly turn an attractive offer into a financial headache. It’s essential to look at the holistic picture.

Transparency in Terms and Conditions

A hallmark of a reliable car loan is absolute clarity. Every single term, condition, and potential fee should be explicitly laid out and easy for you to understand. There should be no jargon designed to confuse or obscure the true cost of borrowing.

This includes understanding how interest is calculated, what penalties apply for late payments, and if there are any charges for early repayment. A reliable lender prides itself on making sure you fully comprehend your commitment. They will take the time to explain everything without rushing you or glossing over details.

Fair and Sustainable Repayment Structure

A reliable loan means a payment plan that genuinely fits your budget without stretching you too thin. It’s about securing a loan where the monthly installments are manageable, allowing you to comfortably meet your other financial obligations. The loan term should also be appropriate for your financial goals.

Avoid loans that promise extremely low monthly payments over an excessively long term, as this often means you’ll pay significantly more in interest over the life of the loan. A fair structure balances affordability with the total cost of borrowing. It empowers you to pay off your debt responsibly and efficiently.

Reputable Lender and Excellent Customer Service

The source of your loan matters immensely. A reliable car loan comes from a reputable financial institution or lender with a proven track record of ethical practices and strong customer support. This means they are responsive, helpful, and willing to work with you if unexpected circumstances arise.

Pro tips from us: Always research the lender’s reputation, read customer reviews, and check for any complaints filed with regulatory bodies. A lender that values its customers will offer accessible support and clear communication channels, ensuring you feel supported throughout your loan journey.

The Essential Pre-Loan Homework: Your Financial Health Check

Before you even step foot in a dealership or apply for a loan, the most critical step is to conduct a thorough financial health check. This groundwork is instrumental in securing the best car loan rates and ensuring a smooth approval process. Understanding your financial standing empowers you to negotiate confidently and choose wisely.

Many common mistakes to avoid are rooted in a lack of preparation. Rushing into a loan without knowing your financial capabilities can lead to high interest rates, unfavorable terms, or even rejection. Take the time to build a strong foundation.

Your Credit Score: The Key to Unlocking Better Rates

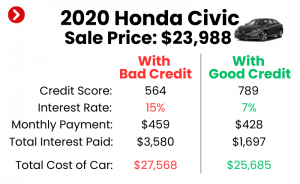

Your credit score is arguably the most significant factor lenders consider. It’s a three-digit number that represents your creditworthiness, indicating how likely you are to repay borrowed money. A higher score typically translates to lower interest rates and more favorable loan terms.

Based on my experience, a good credit score (generally 670 and above) can save you thousands of dollars over the life of a car loan. It’s crucial to check your credit score and report well in advance of applying. You can get free copies of your credit report annually from each of the three major credit bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com.

If you find errors, dispute them immediately, as they can negatively impact your score. If your score isn’t where you want it to be, take steps to improve it, such as paying down existing debts or making all payments on time. This proactive approach significantly boosts your chances of securing reliable car loans.

Budgeting: What You Can Truly Afford

Beyond the sticker price of the car, you need to budget for the total cost of car ownership. This includes not just the monthly loan payment, but also insurance, fuel, maintenance, registration fees, and potential repairs. Many first-time buyers underestimate these additional costs.

Create a detailed monthly budget that accounts for all your income and expenses. Determine a comfortable maximum monthly payment for your car loan that doesn’t strain your finances. Remember, a reliable loan is one you can consistently afford without sacrificing other necessities or financial goals.

The Power of a Down Payment

Making a down payment significantly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. It also shows lenders that you are a serious and committed borrower, potentially leading to better terms.

While there’s no magic number, a down payment of at least 10-20% of the car’s purchase price is often recommended. For used cars, a smaller percentage might be acceptable. Pro tips from us: A larger down payment can even help you avoid being "upside down" on your loan, meaning you owe more than the car is worth, especially if the car depreciates quickly.

Understanding Your Debt-to-Income (DTI) Ratio

Lenders also assess your debt-to-income (DTI) ratio, which is the percentage of your gross monthly income that goes towards paying debts. A lower DTI ratio indicates that you have more disposable income available to manage new debt, making you a less risky borrower.

To calculate your DTI, add up your total monthly debt payments (credit cards, student loans, mortgage, etc.) and divide that by your gross monthly income. Most lenders prefer a DTI ratio below 43%, though it can vary. A healthy DTI is another indicator that you are ready for a reliable car loan.

Navigating the Lender Landscape: Where to Find Reliable Car Loans

Once your financial house is in order, the next step is to explore your options for lenders. The landscape for car loan lenders is diverse, ranging from traditional banks to online platforms, each offering different advantages. It’s crucial to shop around and compare offers to find the most suitable and reliable option.

Common mistakes to avoid are taking the first offer you receive, especially if it’s from a dealership without having explored other avenues. This can often lead to missing out on significantly better terms. A little comparison shopping goes a long way.

Banks and Credit Unions: Traditional and Trustworthy

Traditional banks and credit unions are often excellent sources for reliable car loans. They typically offer competitive interest rates, especially to customers with good credit, and have established reputations. Credit unions, in particular, are known for their member-focused approach and often provide slightly better rates or more flexible terms due to their non-profit structure.

Building a relationship with a local bank or credit union can also be beneficial for future financial needs. They often prioritize their existing members, potentially offering preferential rates or streamlined application processes. Don’t hesitate to check with your current financial institution first.

Dealership Financing: Convenience with Caveats

Dealerships offer financing as a one-stop shop convenience, allowing you to choose a car and secure a loan all in one place. They work with a network of lenders and can often provide quick approvals. Sometimes, they even offer promotional low-interest rates, especially on new vehicles.

However, based on my experience, dealership financing can sometimes be less transparent. The convenience might come at the cost of a higher interest rate compared to what you could secure independently. Always compare their offer with pre-approvals you’ve received elsewhere to ensure you’re getting a competitive deal. Remember, the dealer’s primary goal is to sell you a car, and financing is part of that sales process.

Online Lenders: Speed and Comparison

The rise of online lenders has revolutionized the car loan market, offering a convenient way to compare multiple offers from various financial institutions without leaving your home. Many online platforms specialize in connecting borrowers with a wide range of lenders, including those offering bad credit car loans.

These platforms often provide quick pre-approvals and allow for easy comparison of interest rates, terms, and monthly payments. They are excellent for efficiency and broad market access. However, ensure the online lender is reputable and secure, always reading reviews and checking their credentials.

The Power of Pre-Approval

One of the smartest strategies for securing a reliable car loan is getting pre-approved before you start shopping. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a certain amount at a specific interest rate. This is a game-changer for several reasons.

Firstly, it gives you a clear budget, so you know exactly how much car you can afford. Secondly, it transforms you into a cash buyer at the dealership, giving you significant negotiation power on the vehicle’s price. You’re no longer negotiating two things at once (car price and loan terms), but focusing solely on the car. For a deeper dive into this, check out our guide on .

Understanding the Anatomy of Your Car Loan: Key Terms & Concepts

Securing a reliable car loan means thoroughly understanding the contract you’re signing. Beyond the monthly payment, several key terms and concepts dictate the true cost and structure of your loan. Being knowledgeable about these elements empowers you to make informed decisions and avoid unpleasant surprises.

Common mistakes to avoid include signing a loan agreement without fully grasping what each clause means. Every detail matters, and understanding them ensures you’re getting a fair deal.

Interest Rate (APR): The Cost of Borrowing

The interest rate, often expressed as an Annual Percentage Rate (APR), is the cost you pay to borrow money, calculated as a percentage of the principal loan amount. This is perhaps the most critical number to understand. A lower APR means you pay less over the life of the loan.

Car loan interest rates can be fixed or variable. Most auto loans are fixed-rate, meaning your interest rate and monthly payment remain the same throughout the loan term. Variable rates can fluctuate with market conditions, which might seem appealing initially but can lead to unpredictable payments.

Loan Term: How Long You’ll Be Paying

The loan term is the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer loan term means lower monthly payments, it also means you’ll pay more in total interest over the life of the loan.

Conversely, a shorter loan term results in higher monthly payments but significantly reduces the total interest paid. When considering understanding car loan terms, it’s vital to strike a balance between an affordable monthly payment and minimizing the overall cost of borrowing.

Principal: The Amount You Borrow

The principal is the original amount of money you borrowed to purchase the car, before any interest or fees are added. As you make payments, a portion of each payment goes towards reducing the principal, and another portion goes towards interest. The goal is to pay down the principal as quickly as possible.

Understanding the principal is crucial for knowing how much equity you have in your car and for calculating future interest savings if you decide to make extra payments. It’s the foundation upon which all other loan calculations are built.

Monthly Payment: Your Regular Obligation

Your monthly payment is the fixed amount you agree to pay each month until the loan is fully repaid. This amount is calculated based on the principal loan amount, the interest rate, and the loan term. It’s the most immediate and tangible aspect of your loan.

It’s vital that this payment fits comfortably within your budget, allowing you to meet your other financial commitments without strain. Always factor in potential future financial changes when assessing the long-term affordability of your monthly payment.

Fees: The Hidden Costs

Car loans can come with various fees that can add to the total cost. These might include origination fees, documentation fees, processing fees, or even prepayment penalties. A prepayment penalty is a fee charged if you pay off your loan early, which some lenders impose to recover lost interest.

Pro tips from us: Always ask for a full breakdown of all fees associated with the loan. A truly reliable car loan will have transparent fees, and a reputable lender will be upfront about them. Ideally, look for loans with minimal or no prepayment penalties, giving you the flexibility to pay off your debt faster.

Collateral: The Car Itself

In a secured car loan, the vehicle you are purchasing serves as collateral. This means if you fail to make your loan payments as agreed, the lender has the legal right to repossess the car to recover their losses. This is why lenders are willing to offer more favorable terms on car loans compared to unsecured personal loans.

Understanding that the car itself is collateral underscores the importance of making timely payments. It’s not just your credit score at stake, but also your mode of transportation.

The Application Process: Step-by-Step to Approval

Navigating the car loan application process can feel daunting, but with proper preparation, it becomes a straightforward path. Knowing what to expect and having your documents ready will streamline the journey to securing your reliable car loan.

Many people find the application process intimidating, but breaking it down into manageable steps makes it much easier. Don’t be afraid to ask questions at any stage.

Gathering Your Documents

Before you apply, assemble all necessary documentation. This typically includes:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs (from the last 1-3 months), W-2s, tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Proof of Insurance: You’ll need to show proof of auto insurance before driving off with the car.

- Social Security Number: For credit checks.

Having these documents ready will significantly speed up the application process and demonstrate your preparedness to the lender.

Filling Out the Application

Whether online or in person, the application will ask for personal, financial, and employment information. Be accurate and honest in your responses. Lenders use this information to assess your creditworthiness, verify your income, and determine your ability to repay the loan.

Double-check all entries for accuracy before submitting. Errors or inconsistencies can cause delays or even lead to denial. A clean and complete application reflects positively on you as a borrower.

The Approval or Denial Process

Once submitted, the lender will review your application, pulling your credit report and verifying your income and other details. This process can take anywhere from a few minutes for online pre-approvals to a few business days for more complex cases.

If approved, you’ll receive a loan offer detailing the principal amount, interest rate, term, and monthly payment. If denied, the lender is legally required to provide you with a reason for the denial. This information is crucial for understanding what areas you might need to improve for future applications.

Negotiating Terms (If Applicable)

If you’ve received multiple pre-approvals or are working with a dealership, you might have room to negotiate the terms. Use competing offers to your advantage. For instance, if one lender offers a lower APR, see if another lender can match or beat it.

Remember, everything is negotiable, from the interest rate to potential fees. Don’t be afraid to ask for better terms; the worst they can say is no. This negotiation can lead to a more reliable car loan that saves you money.

Special Considerations for Different Situations

The path to a reliable car loan isn’t always a straight line. Various life circumstances can influence your options and strategies. Understanding how to navigate these situations is key to securing appropriate financing.

Many people face unique challenges, from past credit issues to being a first-time borrower. Knowing the specific advice for your situation can make a huge difference.

Bad Credit Car Loans: Strategies for Approval

Having a less-than-perfect credit score doesn’t necessarily mean you can’t get a car loan, but it does mean you’ll likely face higher interest rates. Lenders view borrowers with bad credit as higher risk. However, there are still ways to find reliable car loans in this scenario.

- Subprime Lenders: Some lenders specialize in working with bad credit borrowers. They might offer higher rates but provide an opportunity to rebuild your credit.

- Secured Loans: Consider a secured personal loan where you put up collateral (other than the car) if available, which can sometimes lower the risk for the lender.

- Co-signer: A co-signer with good credit can significantly improve your chances of approval and help you secure better terms. However, remember they are equally responsible for the loan.

- Larger Down Payment: A substantial down payment reduces the loan amount and signals to lenders that you are serious about repayment.

- Focus on Affordability: Prioritize a car you can comfortably afford, even with a higher interest rate, to ensure you make all payments on time and improve your credit.

Pro tips from us: The most important strategy for bad credit car loans is to make every payment on time. This consistency will gradually improve your credit score, opening doors to better rates in the future, possibly through refinancing.

First-Time Buyers: Navigating the Unknown

First-time car buyers often lack a significant credit history, which can make securing a loan challenging. Lenders prefer to see a track record of responsible borrowing. However, there are avenues for reliable car loans for newcomers.

- Secured Credit Card or Small Loan: Building a positive credit history with a secured credit card or a small personal loan, paid diligently over 6-12 months, can establish creditworthiness.

- Co-signer: As with bad credit, a co-signer with established credit can be invaluable.

- Dealership Programs: Some dealerships have specific programs for first-time buyers, though terms might be less competitive.

- Credit Unions: Often more willing to work with individuals building credit, thanks to their community focus.

Start small, build good habits, and demonstrate financial responsibility. This foundational work will pay dividends for your first car loan and beyond.

Refinancing Your Car Loan: A Second Chance for Better Terms

If you’ve already secured a car loan but your financial situation has improved (e.g., your credit score has increased, or interest rates have dropped), refinancing your car loan could be a smart move. Refinancing involves taking out a new loan to pay off your existing car loan, often at a lower interest rate or with different terms.

Reasons to consider refinancing:

- Lower Interest Rate: If your credit score has improved or market rates have dropped, you could qualify for a significantly lower APR, saving you money over time.

- Lower Monthly Payments: Extending the loan term (though this increases total interest) can reduce your monthly burden.

- Shorter Loan Term: If you can afford higher payments, shortening the term can save you a lot in interest.

- Remove a Co-signer: If your credit has improved sufficiently, you might be able to refinance and release a co-signer from their obligation.

For a detailed exploration of when and how to refinance, consult our article on . Refinancing can turn an initially less-than-ideal loan into a more reliable car loan.

Avoiding Common Pitfalls and Ensuring Long-Term Success

Even after securing what appears to be a reliable car loan, there are still common mistakes to avoid that can undermine your financial success. Being vigilant and maintaining good financial habits throughout the loan term is paramount.

Pro tips from us: The agreement is just the beginning. Your actions during the loan repayment period are equally important for a positive outcome.

Don’t Focus Solely on the Monthly Payment

While an affordable monthly payment is crucial, fixating on it exclusively can lead to a longer loan term and significantly higher total interest paid. Salespeople might try to distract you with a low monthly figure, but always ask for the total cost of the loan, including all interest and fees.

A lower monthly payment over 84 months often means you’re paying far more in the long run than a slightly higher payment over 60 months. Always consider the total financial commitment.

Read the Fine Print, Every Single Word

This cannot be stressed enough. Before signing any document, thoroughly read and understand every clause in your loan agreement. Pay close attention to sections on interest rates, fees, prepayment penalties, default clauses, and what happens if you miss a payment.

Common mistakes to avoid are skimming or trusting that everything is "standard." If there’s anything you don’t understand, ask for clarification. A reputable lender will patiently explain every detail.

Beware of Unnecessary Add-ons

Dealerships often try to upsell you on various add-ons like extended warranties, GAP insurance (Guaranteed Asset Protection), VIN etching, or fabric protection. While some, like GAP insurance, can be valuable in certain situations, others might be overpriced or redundant.

Always consider if these add-ons are truly necessary and if you can purchase them cheaper elsewhere. Adding them to your loan increases your principal, and thus your monthly payment and total interest. Evaluate each one critically.

Understand Early Payoff Clauses

As mentioned, some loans come with prepayment penalties. These clauses can negate the financial benefit of paying off your loan early. Always confirm whether your loan has such a penalty before signing.

A truly flexible and reliable car loan will allow you to make extra payments or pay off the loan in full without incurring additional charges. This flexibility gives you more control over your finances.

Maintain Good Financial Habits

Once you have your car and your loan, the journey isn’t over. Continue to make all your payments on time, or even consider paying a little extra each month if your budget allows. This not only keeps your credit score healthy but also helps you pay down the principal faster, saving you interest.

Regularly review your financial situation and consider refinancing if conditions change in your favor. Consistent financial responsibility ensures that your reliable car loan remains a positive asset in your financial life.

Conclusion: Driving Forward with Confidence

Securing a reliable car loan is a pivotal step on your journey to vehicle ownership. It’s a decision that impacts your financial health for years to come, and one that demands careful consideration, thorough research, and a proactive approach. From understanding your credit score and budgeting effectively to navigating the myriad of lenders and deciphering complex loan terms, every step plays a crucial role.

By embracing the strategies outlined in this guide – conducting diligent pre-loan homework, comparing offers from various reputable lenders, understanding the full anatomy of your loan, and avoiding common pitfalls – you empower yourself to make a truly informed choice. Remember, a reliable loan isn’t just about a low number; it’s about transparency, fairness, sustainability, and the peace of mind that comes with a financially sound decision.

Don’t let the excitement of a new car overshadow the importance of smart financing. Take control of your car buying journey, arm yourself with knowledge, and drive away not just with your dream car, but with a reliable car loan that sets you up for long-term financial success. Your road ahead should be as smooth and dependable as your new ride.