Navigating the Road to Your Dream Car: A Comprehensive Guide to the Credit Application for Car Loan

Navigating the Road to Your Dream Car: A Comprehensive Guide to the Credit Application for Car Loan Carloan.Guidemechanic.com

The open road, the feel of a new car, and the freedom it brings – for many, owning a vehicle is more than just transportation; it’s a significant life milestone. However, transforming that dream into reality often involves a crucial step: securing a car loan. The credit application for a car loan isn’t just a formality; it’s your financial passport to vehicle ownership, and mastering it can save you thousands of dollars and countless headaches.

In this exhaustive guide, we’ll peel back the layers of the car loan application process. We’ll equip you with the knowledge, strategies, and insider tips you need to navigate this journey with confidence. From understanding your credit score to choosing the right lender and avoiding common pitfalls, consider this your definitive roadmap to getting approved for the best possible car loan. Let’s get you ready to drive away in your dream car!

Navigating the Road to Your Dream Car: A Comprehensive Guide to the Credit Application for Car Loan

Understanding the Landscape: Why Your Car Loan Application Matters

A car loan application is far more than just filling out a few forms. It’s a comprehensive evaluation of your financial health, presented to a potential lender. This document acts as your financial resume, detailing your ability and willingness to repay borrowed money. Every piece of information you provide plays a critical role in the lender’s decision-making process.

The outcome of your application directly impacts the interest rate you’ll pay, the length of your loan term, and ultimately, the total cost of your vehicle. A strong application can unlock lower interest rates and more favorable terms, leading to significant savings over the life of the loan. Conversely, a weak or poorly prepared application can result in higher costs, less desirable terms, or even outright rejection.

From the lender’s perspective, they are assessing risk. They want to know how likely you are to make your payments on time and in full. Your application helps them gauge this risk, allowing them to determine if you’re a reliable borrower. Understanding this underlying dynamic is the first step towards crafting an application that stands out for all the right reasons.

The Foundation: Before You Even Apply

Before you even think about stepping into a dealership or clicking "submit" on an online application, thorough preparation is paramount. This foundational work will not only streamline the process but significantly improve your chances of securing a favorable loan.

Knowing Your Credit Score: Your Financial Report Card

Your credit score is arguably the single most influential factor in your car loan application. It’s a three-digit number that summarizes your creditworthiness, based on your payment history, outstanding debts, length of credit history, and other factors. Lenders use this score to quickly assess your risk profile.

A higher credit score signals to lenders that you are a responsible borrower with a history of managing debt effectively. This typically translates into lower interest rates, as lenders view you as less risky. Conversely, a lower score can lead to higher interest rates or even difficulty getting approved, as it suggests a greater risk of default.

Based on my experience, a higher score is your golden ticket to unlocking the best car loan rates and terms. It’s the difference between paying thousands more over the life of your loan versus significant savings. You can obtain a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once a year at AnnualCreditReport.com. Reviewing these reports is crucial for identifying any errors that could be dragging your score down.

Understanding Your Budget & Affordability: Beyond the Monthly Payment

It’s tempting to focus solely on the monthly payment, but a truly responsible approach to car buying requires a broader perspective. You need to understand the total cost of ownership, which extends far beyond just the loan payment. Consider expenses like car insurance, fuel, routine maintenance, unexpected repairs, and registration fees.

Creating a realistic budget involves analyzing your income and all your existing expenses. A key metric lenders consider is your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to comfortably cover a new car payment, making you a more attractive borrower.

Setting a realistic price range for your vehicle before you apply prevents you from falling in love with a car you can’t truly afford. It’s better to be pre-approved for a loan amount that aligns with your budget, rather than getting caught up in the excitement and overextending yourself. Remember, the goal is sustainable ownership, not just initial acquisition.

Saving for a Down Payment: A Smart Financial Move

While some lenders offer 100% financing, making a down payment is almost always a smart financial decision. A substantial down payment reduces the total amount you need to borrow, which directly translates into lower monthly payments and less interest paid over the life of the loan. It also helps you build equity in your vehicle faster.

From a lender’s perspective, a down payment signifies your commitment and reduces their risk. If you have equity in the car from day one, you’re less likely to default on the loan. Typically, a down payment of 10-20% of the car’s purchase price is recommended, especially for new vehicles. For used cars, even a smaller down payment can make a difference.

Pro tips from us: Even if you can secure a loan without a down payment, seriously consider putting some money down. It provides a financial buffer and strengthens your application, often leading to better interest rates. It’s a clear signal of your financial stability and commitment.

Gathering Essential Documents: Be Prepared

A smooth application process hinges on having all your necessary documents organized and ready. Lenders will require various forms of identification and proof of your financial situation. Gathering these in advance saves time and prevents last-minute scrambling.

Common documents you’ll need include:

- Proof of Identity: Valid driver’s license, state ID, or passport.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, tax returns (for self-employed individuals), or bank statements.

- Proof of Residency: Utility bills, lease agreement, or mortgage statements showing your current address.

- Proof of Insurance: While you might not have it for the specific car yet, lenders will want to know you’re insurable and will require proof before you drive off the lot.

- Trade-in Information (if applicable): Title or registration for your current vehicle.

Having these documents readily available streamlines the application process significantly. It shows the lender you are organized and serious, helping to move your application through the system much faster.

Navigating the Car Loan Application Process: A Step-by-Step Guide

With your groundwork laid, you’re now ready to tackle the application itself. This section breaks down the process into actionable steps, guiding you from initial inquiry to final approval.

Step 1: Get Pre-Approved (Strongly Recommended)

Getting pre-approved for a car loan is perhaps the most powerful tool in your car-buying arsenal. Pre-approval means a lender has reviewed your credit and financial information and tentatively agreed to lend you a specific amount of money at a certain interest rate, even before you’ve picked out a car. It’s essentially a commitment from the lender, subject to the final vehicle details.

The benefits of pre-approval are substantial. First, it gives you a firm understanding of your budget, preventing you from falling in love with a car outside your financial reach. Second, and crucially, it transforms you into a cash buyer at the dealership. You can negotiate the car’s price based on its value, not on your ability to secure financing. This removes a layer of negotiation for the dealer, often leading to a better deal on the vehicle itself.

It’s important to distinguish between "soft" and "hard" credit inquiries. A pre-approval typically involves a soft inquiry, which doesn’t negatively impact your credit score. Once you proceed with a specific loan, a hard inquiry will be made. Pro tips from us: Pre-approval is a game-changer because it gives you leverage. You walk into the dealership with financing already secured, putting you in a much stronger negotiating position.

Step 2: Choose Your Lender Wisely

The financial market offers a variety of lenders, each with its own advantages and disadvantages. Shopping around and comparing offers is crucial for securing the best terms.

- Banks: Traditional banks are a common source for car loans, often offering competitive rates for customers with good credit. They might also offer discounts for existing customers.

- Credit Unions: Often non-profit organizations, credit unions are known for offering lower interest rates and more personalized service to their members. Membership requirements usually involve a common affiliation or geographic location.

- Dealership Financing: Dealerships act as intermediaries, working with a network of lenders to secure financing for you. While convenient, their offers might not always be the most competitive, though they can sometimes offer special promotions.

- Online Lenders: A growing number of online platforms specialize in car loans, often offering quick application processes and competitive rates, particularly for those with varying credit profiles.

Comparing interest rates (APR), loan terms, and any associated fees from several lenders is a non-negotiable step. Don’t just take the first offer; a few percentage points difference in APR can save you hundreds or even thousands of dollars over the life of the loan.

Step 3: Completing the Application Form Accurately

Whether you’re applying online or in person, the application form will request detailed personal, employment, and financial information. This includes your full name, address, Social Security number, date of birth, employment history, annual income, and details of your current debts and assets.

Accuracy and honesty are paramount. Providing incomplete or inaccurate information can lead to delays, rejection, or even legal issues if discovered later. Take your time to fill out every section thoroughly. If you’re unsure about a question, don’t guess; ask for clarification from the lender.

Common mistakes to avoid are incomplete information, typos in critical data like your Social Security number, or understating your existing debt. Lenders verify much of this information, and discrepancies will raise red flags. Be precise and truthful in every detail.

Step 4: Providing Supporting Documentation

Once your application is submitted, the lender will likely request the supporting documents you gathered earlier. This is where your preparation pays off. Promptly providing clear, legible copies of your driver’s license, pay stubs, bank statements, and other requested items will keep the process moving smoothly.

Ensure that all documents are up-to-date. For example, if your pay stubs are several months old, the lender may request more recent ones. The goal is to provide a complete and current picture of your financial situation. Any delays in providing these documents can hold up your approval.

Step 5: Understanding the Offer & Terms

If your application is approved, the lender will present you with a loan offer detailing the terms. This is a critical moment for careful review. Pay close attention to the following:

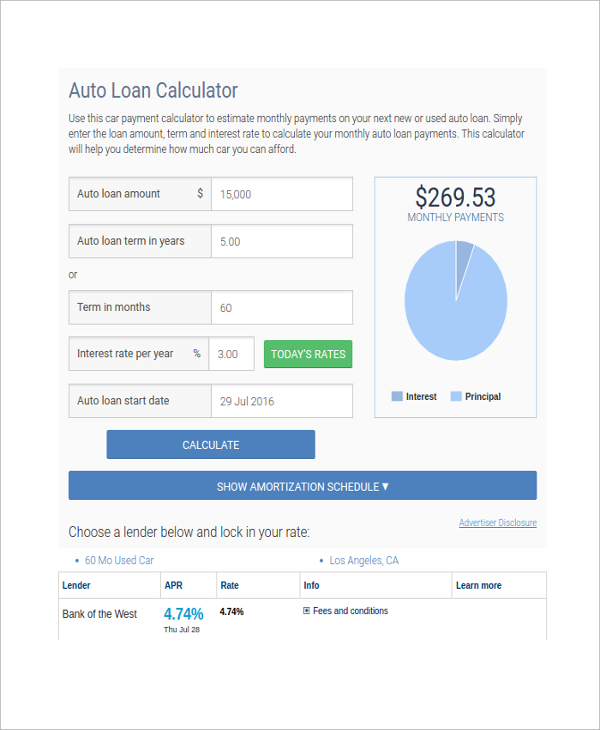

- Annual Percentage Rate (APR): This is the true cost of borrowing, including the interest rate and any fees. It allows for an "apples-to-apples" comparison between different loan offers.

- Loan Term: This is the length of time you have to repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months). A longer term means lower monthly payments but more interest paid overall.

- Monthly Payment: The exact amount you’ll owe each month.

- Total Cost of the Loan: Understand the total amount you will pay over the entire loan term, including interest.

- Fees and Penalties: Look for any origination fees, prepayment penalties (though rare for car loans), or late payment fees.

Don’t hesitate to ask questions about anything you don’t understand. If you have multiple offers, compare them side-by-side to ensure you’re getting the best deal. Sometimes, there’s room for negotiation on certain aspects, especially if you have a strong credit profile.

Boosting Your Chances: Tips for Car Loan Approval

Even if you’ve followed all the steps above, there are additional strategies you can employ to further strengthen your car loan application and increase your likelihood of approval, especially with favorable terms.

Improve Your Credit Score

Your credit score is dynamic and can be improved over time. Before applying, take steps to boost it. This includes paying all your bills on time, every time, as payment history is the biggest factor. Reduce existing debt, especially on credit cards, to lower your credit utilization ratio. Also, review your credit reports for any errors and dispute them promptly. Correcting even a small mistake can sometimes significantly improve your score.

For more detailed strategies on enhancing your financial profile, check out our comprehensive article on .

Reduce Debt-to-Income Ratio

Lenders prefer borrowers with a low DTI ratio, as it indicates less financial strain. If your DTI is high, consider paying down existing debts, particularly those with high interest rates, before applying for a car loan. Avoid taking on new debt during the period leading up to and during your car loan application process. Even small credit card balances can impact this ratio.

Consider a Co-signer (If Necessary)

If your credit score is low or you have limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

However, this is a serious commitment for the co-signer, as the loan will appear on their credit report, and their credit score will be affected if payments are missed. Only consider this option with someone you trust implicitly and who fully understands the responsibilities involved.

Be Realistic About the Car

While it’s exciting to dream big, choosing a car that is well within your financial means is a practical and wise decision. Don’t overextend your budget for a vehicle that will strain your finances. Lenders are more likely to approve loans for vehicles that are reasonably priced relative to your income and credit profile. A more affordable car might also lead to a lower interest rate, as it represents less risk to the lender.

Show Stability

Lenders favor stability in a borrower’s life. This means consistent employment history, ideally with the same employer for a significant period. Proof of residency at the same address for several years also signals stability. While you can’t magically change your history, presenting your current situation as stable and reliable will work in your favor.

Special Situations: What If Your Credit Isn’t Perfect?

Life happens, and not everyone has a pristine credit history. If your credit isn’t perfect, or you have no credit history at all, securing a car loan can be more challenging, but it’s not impossible.

Bad Credit Car Loans

For individuals with low credit scores, "bad credit car loans" are an option, though they come with distinct characteristics. Expect significantly higher interest rates and potentially shorter loan terms to mitigate the lender’s increased risk. These loans are often offered by subprime lenders who specialize in working with higher-risk borrowers.

While the terms might not be ideal, securing and successfully repaying a bad credit car loan can be a stepping stone to rebuilding your credit. Focus on making every payment on time. Over time, as your credit improves, you might be able to refinance the loan for better terms.

No Credit History

If you’re a first-time car buyer with no established credit history, lenders have no data to assess your risk. This can be as challenging as having bad credit. However, several options exist:

- First-Time Buyer Programs: Some dealerships and lenders offer specific programs designed for individuals with limited or no credit.

- Secured Loans: You might be able to secure a loan using other assets as collateral, though this carries a higher risk.

- Co-signer: As mentioned earlier, a co-signer with good credit can significantly improve your chances.

- Smaller Down Payment with a Shorter Term: A substantial down payment combined with a shorter loan term can sometimes sway a lender.

The key is to start building credit responsibly. Even a small credit card used sparingly and paid off in full each month can help establish a positive credit history. For further insights into building credit from scratch, the Consumer Financial Protection Bureau offers valuable resources.

The Post-Approval Phase: What Happens Next?

Congratulations, your credit application for a car loan has been approved! But the journey isn’t quite over. There are a few final steps to take before you can truly enjoy your new ride.

First, you’ll finalize the loan documents. Read every line carefully, ensuring all the terms match what you were offered and agreed upon. This includes the interest rate, loan term, monthly payment, and any fees. Don’t be afraid to ask for clarification on any clauses you don’t understand. Once signed, these documents are legally binding.

Next, you’ll need to arrange for car insurance. Lenders require proof of full coverage insurance before you can drive the vehicle off the lot. Shop around for the best rates and have your policy in place. Finally, the dealership or your lender will handle the vehicle registration and titling processes, but always confirm these steps are being taken care of.

Once you have the keys, the most important step is to consistently make your loan payments on time. This is crucial for maintaining good credit and will help you build an even stronger financial profile for future endeavors. Managing your car finances effectively is key to long-term financial health. Read our guide on to stay on track.

Conclusion: Drive Away with Confidence

The credit application for a car loan can seem daunting, but with the right knowledge and preparation, it becomes a manageable and even empowering process. By understanding your credit, setting a realistic budget, gathering your documents, and strategically navigating the application steps, you position yourself for success.

Remember, preparation is your most powerful tool. Getting pre-approved, shopping around for lenders, and being meticulously accurate in your application are not just recommendations; they are vital strategies for securing the best possible terms. Even if your credit isn’t perfect, there are pathways available, often requiring a bit more diligence and a focus on long-term credit improvement.

Ultimately, your goal is to drive away in a vehicle that meets your needs without creating undue financial stress. By following the advice in this comprehensive guide, you’re not just applying for a car loan; you’re making an informed financial decision that will serve you well for years to come. So, go ahead, prepare thoroughly, apply wisely, and get ready to enjoy the open road with confidence!