Navigating the Road to Your Dream Car: A Deep Dive into Fifth Third Bank Car Loans

Navigating the Road to Your Dream Car: A Deep Dive into Fifth Third Bank Car Loans Carloan.Guidemechanic.com

Getting behind the wheel of a new or used car is an exciting milestone. For many, this dream becomes a reality through a car loan, and understanding your options is the first crucial step. While "5 3 Car Loan" might initially seem like a cryptic term, it most commonly refers to the comprehensive auto financing options provided by Fifth Third Bank. As a prominent financial institution, Fifth Third Bank offers a range of car loan products designed to help individuals purchase vehicles, refinance existing loans, or even buy out a lease.

This ultimate guide will take you on an in-depth journey through Fifth Third Bank’s car loan offerings. We’ll explore everything from the types of loans available to the application process, eligibility criteria, and crucial tips for securing the best rates. Our goal is to equip you with the knowledge needed to make an informed decision, ensuring your path to car ownership is as smooth and stress-free as possible.

Navigating the Road to Your Dream Car: A Deep Dive into Fifth Third Bank Car Loans

What Exactly is a Fifth Third Bank Car Loan?

At its core, a Fifth Third Bank car loan is a financial product that provides you with the funds to purchase a vehicle. You borrow a specific amount of money from the bank, and in return, you agree to repay that amount, plus interest, over a predetermined period, typically ranging from 24 to 84 months. The vehicle itself usually serves as collateral for the loan, meaning the bank can repossess it if you fail to make your payments.

Fifth Third Bank, like other major lenders, structures its auto loans to cater to various needs and financial situations. They aim to provide competitive rates and flexible terms, making car ownership accessible to a broader range of customers. Understanding these fundamental principles is key before diving into the specifics of their offerings.

The Distinct Advantages of Choosing Fifth Third Bank for Your Auto Financing

When you’re shopping for a car loan, you have numerous lenders to choose from. So, why might Fifth Third Bank stand out as a strong contender? Based on my experience in the automotive and finance sectors, several key advantages often draw customers to their services.

Firstly, Fifth Third Bank boasts a long-standing reputation as a reliable financial institution. This legacy often translates into a sense of trust and stability for borrowers, knowing they are dealing with an established entity. Their broad presence, with numerous branches, also offers the convenience of in-person assistance for those who prefer face-to-face interactions.

Secondly, they often provide a diverse array of loan products, not just generic auto loans. This flexibility means they can tailor solutions whether you’re buying new, used, or even considering refinancing. Competitive interest rates and flexible repayment terms are also frequently highlighted benefits, designed to fit various budgets and financial goals.

Exploring the Spectrum of Car Loans Offered by Fifth Third Bank

Fifth Third Bank doesn’t offer a one-size-fits-all solution when it comes to car financing. They understand that different car-buying scenarios require different loan structures. Here’s a breakdown of the primary types of auto loans you can typically find:

1. New Car Loans

If you’re eyeing that brand-new model fresh off the dealership lot, a new car loan from Fifth Third Bank is specifically designed for you. These loans often come with the lowest interest rates compared to used car loans. This is because new vehicles generally hold their value better in the initial years, presenting less risk to the lender.

The terms for new car loans can be quite flexible, allowing you to choose a repayment period that aligns with your financial comfort. Longer terms might mean lower monthly payments, but you’ll pay more interest over the life of the loan. Shorter terms, conversely, result in higher monthly payments but less overall interest paid.

2. Used Car Loans

Purchasing a pre-owned vehicle can be a smart financial move, and Fifth Third Bank offers robust options for used car financing. While the interest rates might be slightly higher than for new cars due to the perceived higher risk and depreciation, they are still designed to be competitive. These loans are typically available for vehicles that meet certain age and mileage criteria set by the bank.

It’s crucial to check the bank’s specific requirements for used vehicles, as they can vary. Some might have limits on the car’s age or total mileage. Securing a used car loan allows you to enjoy the cost savings of a pre-owned vehicle while spreading out the purchase price over manageable monthly payments.

3. Auto Loan Refinancing

Perhaps you already have a car loan but are looking for a better deal. Fifth Third Bank’s auto loan refinancing option could be your answer. Refinancing involves taking out a new loan, often with a lower interest rate or different terms, to pay off your existing car loan. This can be incredibly beneficial if your credit score has improved since you first took out the loan, or if market rates have dropped.

Refinancing can lead to lower monthly payments, a reduced total interest paid over the loan term, or even a shorter repayment period. It’s a strategic move to optimize your car ownership costs and improve your financial flexibility. Consider exploring this option if your current loan feels burdensome or if you believe you qualify for better terms.

4. Lease Buyout Loans

For those who are currently leasing a vehicle and have fallen in love with it, Fifth Third Bank may offer lease buyout loans. At the end of a lease term, you typically have the option to purchase the car for a predetermined residual value. A lease buyout loan provides the funds to make this purchase, allowing you to transition from leasing to owning.

This type of loan can be advantageous if the car’s market value is higher than its residual value, or simply because you want to keep a vehicle you’ve grown accustomed to. It’s important to understand the residual value stated in your lease agreement and compare it to the current market value before committing to a buyout.

Navigating the Eligibility Requirements for a Fifth Third Bank Car Loan

Securing a car loan isn’t just about finding the right vehicle; it’s also about meeting the lender’s criteria. Fifth Third Bank, like all financial institutions, has specific eligibility requirements that potential borrowers must satisfy. Understanding these beforehand can significantly improve your chances of approval.

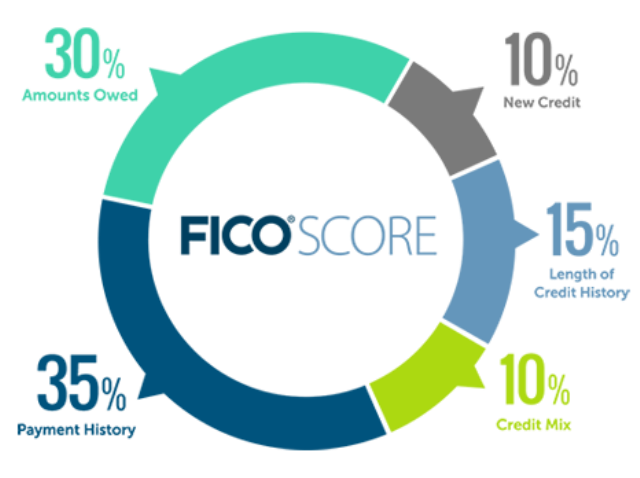

1. Credit Score

Your credit score is arguably the most critical factor. It’s a three-digit number that reflects your creditworthiness based on your borrowing and repayment history. Generally, a higher credit score indicates lower risk to the lender, often translating into better interest rates and easier approval. While Fifth Third Bank may offer loans to individuals with a range of credit scores, those with excellent to good credit (typically 670 and above) will receive the most favorable terms.

2. Income and Employment History

Lenders want to ensure you have a stable source of income to repay the loan. Fifth Third Bank will typically require proof of consistent employment and sufficient income. This might include recent pay stubs, W-2 forms, or tax returns if you’re self-employed. A steady job history, usually for at least two years, demonstrates reliability.

3. Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover new loan payments, making you a less risky borrower. While the ideal DTI varies, most lenders prefer it to be below 43%, though this can sometimes be more flexible depending on other strong application factors.

4. Down Payment

While not always strictly required, making a down payment on your car loan can significantly improve your chances of approval and secure better terms. A down payment reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid. It also shows the bank your commitment to the purchase. Based on my experience, a down payment of 10-20% is often recommended for new cars, and sometimes more for used cars.

5. Vehicle Information

The car itself plays a role. Fifth Third Bank will assess the vehicle’s age, mileage, make, and model to determine its value and suitability as collateral. This is particularly relevant for used car loans, where older or higher-mileage vehicles might face stricter scrutiny or different loan terms.

The Step-by-Step Fifth Third Bank Car Loan Application Process

Applying for a car loan can feel daunting, but breaking it down into manageable steps makes it much clearer. Fifth Third Bank aims to streamline this process, offering both online and in-person application options.

Step 1: Research and Pre-Qualification

Before you even step foot in a dealership, it’s wise to research interest rates and loan terms. Fifth Third Bank often allows you to get pre-qualified online. This involves providing some basic financial information to get an estimate of how much you might be approved for and at what interest rate, without impacting your credit score significantly (it’s usually a "soft pull"). Pre-qualification gives you a strong negotiating tool at the dealership and sets realistic expectations.

Step 2: Gather Required Documents

Once you’re ready to formally apply, ensure you have all necessary documents handy. This typically includes:

- Proof of identity (driver’s license, state ID)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, W-2s, tax returns)

- Social Security number

- Vehicle information (if you’ve already chosen a car)

Having these ready expedites the application process significantly.

Step 3: Complete the Application

You can apply for a Fifth Third Bank car loan in several ways:

- Online: Their website typically features a user-friendly online application portal. This is often the quickest method.

- In-Branch: Visit a local Fifth Third Bank branch and speak with a loan officer. This option is great if you have questions or prefer personalized assistance.

- Through a Dealership: Many dealerships have relationships with Fifth Third Bank and can submit an application on your behalf.

Be prepared to provide detailed financial information and authorize a credit check (a "hard pull" that may temporarily affect your credit score).

Step 4: Await Approval and Review Offer

After submitting your application, Fifth Third Bank will review your financial profile and the vehicle information. This process can take anywhere from a few minutes for online applications to a few business days. If approved, you’ll receive a loan offer outlining the approved amount, interest rate, loan term, and monthly payment.

Carefully review all the terms and conditions. Don’t hesitate to ask questions if anything is unclear.

Step 5: Finalize the Loan and Purchase Your Car

Once you’re satisfied with the loan offer, you’ll sign the necessary paperwork. The funds will then be disbursed, either directly to you, to the dealership, or used to pay off your previous loan in the case of refinancing. With the financing secured, you can then complete the purchase of your new vehicle.

Key Factors Influencing Your Loan Approval and Interest Rate

Beyond the basic eligibility, several nuances can sway Fifth Third Bank’s decision and the interest rate you receive. Understanding these can empower you to strengthen your application.

1. Your Credit Score, Revisited

We can’t stress this enough: your credit score is paramount. A higher score directly correlates with lower perceived risk for the bank. This means they are more likely to offer you a lower Annual Percentage Rate (APR), which translates to less money paid in interest over the life of the loan. Conversely, a lower score might still get you approved, but at a significantly higher APR.

2. Loan Term Length

The length of your loan (e.g., 36, 60, or 72 months) impacts both your monthly payment and the total interest. Longer terms mean lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay more in total interest over the longer period. Shorter terms have higher monthly payments but save you money on interest in the long run. Banks also often offer slightly lower interest rates for shorter terms because their money is at risk for a shorter duration.

3. Amount of Down Payment

A substantial down payment not only reduces the amount you need to borrow but also signals to the bank that you’re a serious and responsible borrower. It immediately reduces the loan-to-value (LTV) ratio of the vehicle, which is favorable for the lender. This can sometimes lead to a slightly better interest rate or make approval easier, especially if other aspects of your financial profile are borderline.

4. Vehicle’s Age and Condition

For used cars, the age and condition of the vehicle are critical. Banks assess the collateral value. An older car or one with high mileage might be seen as a higher risk because its depreciation rate is often faster, and potential repair costs could affect your ability to pay. Some lenders might have maximum age or mileage limits for vehicles they finance, or they might offer less favorable terms for such vehicles.

Pro Tips from Us: Securing a Smooth Application and Better Rates

Based on my years of observing successful auto loan applications, here are some insider tips to help you navigate the process with Fifth Third Bank:

- Boost Your Credit Score: Before applying, take steps to improve your credit. Pay down existing debts, dispute any errors on your credit report, and make all payments on time. Even a small improvement can make a difference in your interest rate.

- Get Pre-Approved: As mentioned, pre-approval gives you leverage. It shows the dealership you’re a serious buyer with financing in hand, allowing you to focus on negotiating the car price, not the financing terms.

- Shop Around (But Not Too Much): While Fifth Third Bank might be your primary choice, it’s wise to compare offers from a few other lenders. This ensures you’re getting the most competitive rate. However, limit your applications to a short window (14-45 days) to minimize the impact on your credit score, as multiple hard inquiries within this period are often treated as a single inquiry.

- Consider a Co-Signer: If you have a lower credit score or limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. Ensure both parties understand the responsibilities involved.

- Negotiate the Car Price First: Always try to negotiate the price of the car before discussing financing. Dealers might try to make up for a low car price with a higher interest rate, or vice-versa. Separate these two crucial steps.

- Read the Fine Print: Thoroughly review the loan agreement before signing. Understand all fees, the total amount you’ll pay, and any prepayment penalties.

Common Mistakes to Avoid When Applying for a Car Loan

Even experienced borrowers can make missteps. Here are some common pitfalls to steer clear of when seeking a Fifth Third Bank car loan:

- Not Checking Your Credit Report: Many people apply without knowing their credit score or history. This is a critical error. Always check your report for inaccuracies and understand where you stand before applying.

- Focusing Only on Monthly Payments: While monthly payments are important, fixating solely on them can lead you to accept longer loan terms and pay significantly more in total interest. Always consider the total cost of the loan.

- Skipping the Down Payment: As tempting as it is to finance 100% of the car, avoiding a down payment can lead to higher interest rates, negative equity (owing more than the car is worth), and greater overall cost.

- Ignoring Additional Fees: Be aware of any origination fees, documentation fees, or other charges associated with the loan. These can add to the total cost.

- Getting Emotionally Attached: Don’t let emotions drive your car-buying and loan-taking decisions. Stick to your budget and walk away if the terms aren’t favorable.

- Not Understanding the Terms: Don’t sign anything you don’t fully comprehend. If you have questions about the APR, loan term, or any clauses, ask for clarification.

Fifth Third Bank’s Customer Service and Support

A bank’s support system is just as important as its products. Fifth Third Bank offers various channels for customer assistance. You can typically reach them via phone, through their online banking portal, or by visiting one of their physical branches. They also often provide educational resources on their website to help customers understand their loan options and financial health better. This accessibility and commitment to customer education can be a significant advantage when you need guidance or have questions about your loan.

Comparing Fifth Third Bank to Other Lenders

While this article focuses on Fifth Third Bank, it’s important to remember that they are one of many options. Credit unions often offer highly competitive rates, especially for members. Online lenders can also be very agile and provide quick approvals. When comparing, look beyond just the interest rate. Consider:

- Fees: Are there any hidden charges?

- Customer Service: How easy is it to reach a representative?

- Flexibility: Do they offer options for different credit scores or loan types?

- Pre-qualification options: Can you get an estimate without a hard credit pull?

By comparing a few different lenders, you can ensure that Fifth Third Bank’s offering truly aligns with your needs and is the best fit for your financial situation.

Refinancing Your Car Loan with Fifth Third Bank: A Second Chance at Better Terms

If you currently have a car loan with another institution, or even with Fifth Third Bank, and are looking to improve your terms, refinancing could be a smart move. As mentioned earlier, Fifth Third Bank offers refinancing options. This is particularly beneficial if:

- Your credit score has improved significantly since you originally took out the loan.

- Interest rates have dropped in the market.

- You want to lower your monthly payments by extending the loan term (though this means more interest over time).

- You want to shorten your loan term to pay off the car faster and save on interest (which will increase monthly payments).

To refinance with Fifth Third Bank, you’ll essentially go through a similar application process, providing updated financial information. They will assess your current creditworthiness and the value of your vehicle. It’s always worth exploring if refinancing could save you money or provide more financial breathing room.

Frequently Asked Questions (FAQs) About Fifth Third Bank Car Loans

To round out our comprehensive guide, let’s address some common questions about Fifth Third Bank car loans.

Q1: How long does it take to get approved for a Fifth Third Bank car loan?

A1: Online applications can sometimes provide instant decisions or within a few hours. In-branch applications might take a bit longer, typically within one to two business days, depending on the complexity of your financial profile and the completeness of your documentation.

Q2: Can I apply for a Fifth Third Bank car loan with bad credit?

A2: Fifth Third Bank considers applicants with a range of credit scores. While a higher score will yield better rates, they may offer solutions for those with less-than-perfect credit, potentially requiring a larger down payment or a co-signer. It’s always best to apply and see what terms you qualify for.

Q3: Does Fifth Third Bank offer pre-qualification for car loans?

A3: Yes, Fifth Third Bank typically offers a pre-qualification process online. This allows you to check your estimated rates and terms without impacting your credit score with a hard inquiry.

Q4: Are there any prepayment penalties with Fifth Third Bank car loans?

A4: Most consumer car loans, especially from major banks, do not have prepayment penalties. However, it’s crucial to always confirm this directly in your loan agreement before signing. Our pro tip is to always look for loans without these penalties.

Q5: What is the maximum loan term offered by Fifth Third Bank?

A5: Loan terms can vary, but for new and used car loans, Fifth Third Bank often offers terms up to 72 or even 84 months. Remember, longer terms mean lower monthly payments but more interest paid over time.

Conclusion: Driving Towards Your Auto Loan Goals with Fifth Third Bank

Navigating the world of car loans requires careful consideration and thorough research. If "5 3 Car Loan" led you to Fifth Third Bank, you’re looking at a reputable institution with a diverse array of auto financing solutions. From new car purchases to refinancing and lease buyouts, they offer options designed to fit various financial situations.

By understanding the eligibility requirements, preparing your documentation, and applying the pro tips we’ve shared, you can significantly enhance your chances of securing a favorable loan. Remember to focus not just on the monthly payment, but on the total cost of the loan, and always read the fine print. With the right approach, Fifth Third Bank can be a reliable partner on your journey to owning the car of your dreams.

Ready to explore your options further? Visit Fifth Third Bank’s official auto loan page to get started or speak with a loan officer. . And for more tips on smart car buying, don’t forget to check out our other guides, like . Happy driving!