Navigating the Road to Your Dream Car: A Deep Dive into Huntington Car Loans

Navigating the Road to Your Dream Car: A Deep Dive into Huntington Car Loans Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect, but the financing aspect can often feel like a complex maze. For many aspiring car owners, securing a reliable and affordable car loan is the key to unlocking their automotive dreams. Among the myriad of financial institutions, Huntington Bank stands out as a prominent player, offering a range of auto financing solutions designed to meet diverse needs.

This comprehensive guide is crafted to serve as your ultimate resource on Huntington Car Loans. We’ll peel back the layers, exploring everything from the distinct advantages of choosing Huntington to the intricate details of their application process, eligibility criteria, and expert tips for securing the best possible rates. Our aim is to equip you with the knowledge and confidence to make informed decisions, ensuring a smooth and successful car buying experience. Let’s rev up and explore how Huntington can help you get behind the wheel.

Navigating the Road to Your Dream Car: A Deep Dive into Huntington Car Loans

Why Consider a Huntington Car Loan? Unpacking the Benefits

When it comes to financing a significant purchase like a car, choosing the right lender is paramount. Huntington Bank has cultivated a strong reputation in the financial sector, and their car loan offerings come with several compelling advantages that make them a worthy contender. It’s not just about getting a loan; it’s about securing a partnership that supports your financial goals.

A Legacy of Trust and Reliability:

Huntington Bank boasts a long-standing history, serving communities with a commitment to customer satisfaction. This established presence instills confidence, assuring borrowers that they are dealing with a stable and reputable institution. Based on my experience in the financial landscape, working with a bank with a solid foundation like Huntington often translates into a more consistent and transparent lending experience, free from unexpected hurdles.

Customer-Centric Approach and Personalized Service:

One of Huntington’s hallmarks is its dedication to understanding individual customer needs. They don’t offer a one-size-fits-all solution; instead, they strive to tailor financing options that align with your specific financial situation and vehicle aspirations. Whether you prefer online interactions or face-to-face consultations at one of their many branches, their customer service is designed to guide you through every step, demystifying the often-intimidating world of auto financing.

Competitive Rates and Flexible Terms:

Securing a car loan with a favorable interest rate and manageable repayment terms is crucial for long-term financial health. Huntington is known for offering competitive rates that can help reduce the overall cost of your vehicle. Furthermore, they provide a range of loan terms, allowing you to choose a payment schedule that fits comfortably within your monthly budget. This flexibility is a significant advantage, empowering you to manage your finances effectively without feeling overstretched.

Convenient and Streamlined Application Process:

In today’s fast-paced world, efficiency is key. Huntington understands this and has developed a user-friendly application process that can often be initiated online. This convenience saves valuable time and simplifies what could otherwise be a cumbersome procedure. From pre-qualification to final approval, their digital tools and readily available support make the journey straightforward, allowing you to focus more on finding your perfect car and less on bureaucratic red tape.

Understanding Huntington’s Diverse Car Loan Offerings

Huntington Bank recognizes that every car buyer’s situation is unique, which is why they offer a versatile suite of auto financing products. Whether you’re eyeing a brand-new model, a reliable pre-owned vehicle, or seeking to improve your current loan terms, Huntington has a solution tailored for you. Understanding these distinct offerings is the first step toward choosing the right path.

New Car Loans:

For those who dream of being the first owner of a shiny new vehicle, Huntington’s new car loans are designed to make that dream a reality. These loans typically come with competitive interest rates and flexible terms, reflecting the lower risk associated with financing a brand-new asset. They cover vehicles purchased directly from dealerships, providing the funds needed to drive off the lot with confidence. Pro tips from us: always compare the dealership’s financing offers with what Huntington can provide; you might find better terms independently.

Used Car Loans:

Opting for a used car can be a smart financial move, offering excellent value and often a lower price point. Huntington provides robust financing options for used vehicles, helping you secure a pre-owned car without compromising on quality or affordability. While rates for used cars might be slightly higher than new car loans due to perceived age-related risk, Huntington strives to keep them competitive. It’s essential to note that eligibility for used car loans often considers the vehicle’s age and mileage, so be prepared with this information during your application.

Auto Loan Refinancing:

Perhaps you already have a car loan but are looking for ways to reduce your monthly payments or lower your interest rate. Huntington’s auto loan refinancing service is specifically designed for this purpose. Refinancing allows you to replace your existing car loan with a new one, potentially with more favorable terms. This can be particularly beneficial if your credit score has improved since you first took out the loan, or if market interest rates have dropped. We’ll delve deeper into refinancing later, but it’s a powerful tool for optimizing your existing car financing.

Lease Buyout Loans:

Many drivers choose to lease a car, enjoying the flexibility of lower monthly payments and the ability to drive a new vehicle every few years. However, at the end of a lease term, you might fall in love with your car and decide you want to keep it. Huntington offers lease buyout loans, providing the financing necessary to purchase your leased vehicle outright. This option allows you to transition from leasing to ownership smoothly, often without the hassle of finding a new car.

Eligibility Requirements: What Huntington Looks For in a Borrower

Securing a Huntington Car Loan, like any financial product, hinges on meeting specific eligibility criteria. Lenders assess various factors to determine your creditworthiness and ability to repay the loan. Understanding these requirements beforehand can significantly improve your chances of approval and help you prepare a strong application.

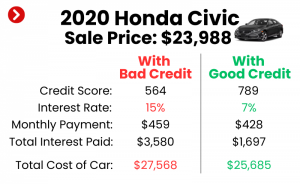

Your Credit Score: A Key Indicator:

Your credit score is arguably the most critical factor Huntington will evaluate. It’s a numerical representation of your credit history, reflecting your past borrowing and repayment behavior. A higher credit score (generally 670 and above) indicates a lower risk to lenders, often qualifying you for the most competitive interest rates. While Huntington may offer loans to individuals with less-than-perfect credit, a strong score is always an advantage. For more details on improving your credit score, check out our guide on .

Stable Income and Employment History:

Huntington needs assurance that you have a consistent and sufficient income to comfortably make your monthly loan payments. They will typically look for a stable employment history, often preferring applicants who have been with their current employer for at least six months to a year. Your income will be verified through pay stubs, tax returns, or bank statements. The goal here is to demonstrate a reliable source of funds for repayment.

Debt-to-Income (DTI) Ratio:

Your Debt-to-Income (DTI) ratio is another crucial metric. This ratio compares your total monthly debt payments (including the potential car loan payment) to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to manage new debt, making you a more attractive borrower. Huntington, like most lenders, looks for a manageable DTI to ensure you won’t be overburdened by the new loan.

Vehicle Information and Value:

The car you intend to purchase also plays a role in your loan eligibility. Huntington will assess the vehicle’s make, model, year, mileage, and overall condition, especially for used cars. They typically require the vehicle’s value to align with the loan amount to ensure they are not over-financing an asset. This is often done by consulting industry guides like Kelley Blue Book or NADA.

Residency and Age Requirements:

Naturally, applicants must be of legal age (typically 18 years or older) and be a U.S. citizen or permanent resident with a valid Social Security Number. Huntington will also require proof of residency. These are standard requirements across virtually all financial institutions to comply with regulations and verify identity.

The Huntington Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan can seem daunting, but Huntington has worked to streamline the process, making it as straightforward as possible. By understanding each step, you can approach your application with confidence and efficiency. This systematic approach ensures all necessary information is gathered, leading to a quicker decision.

Step 1: Online Pre-qualification or Pre-approval:

The journey often begins with a pre-qualification or pre-approval. Pre-qualification gives you an estimate of what you might be approved for, usually with a soft credit inquiry that doesn’t impact your score. Pre-approval is a more robust step, involving a hard credit pull, but it provides a firm offer of a loan amount and interest rate. Pro tips from us: always opt for pre-approval if possible, as it gives you significant bargaining power at the dealership and a clear budget.

Step 2: Gathering Required Documents:

Before submitting your full application, compile all necessary documents. This typically includes proof of identity (driver’s license, Social Security card), proof of income (recent pay stubs, W-2s, or tax returns), proof of residence (utility bill, lease agreement), and details about the vehicle you intend to purchase. Having these ready prevents delays and demonstrates your preparedness.

Step 3: Submitting the Full Application:

Once you’ve found the car you want and have all your documents in order, you can submit your full loan application to Huntington. This can often be done online, over the phone, or in person at a branch. You’ll provide detailed personal, financial, and vehicle information. Be accurate and thorough, as any discrepancies could slow down the process.

Step 4: Credit Review and Decision:

After submission, Huntington’s underwriting team will review your application, credit history, income, and the vehicle details. This involves a comprehensive assessment of your financial health. They will perform a hard inquiry on your credit report, which might temporarily ding your score by a few points. Based on their evaluation, they will make a decision: approval, conditional approval (requiring more information or a co-signer), or denial.

Step 5: Funding and Vehicle Purchase:

Upon approval, you’ll receive the final loan documents outlining the terms, interest rate, and repayment schedule. Once you sign these agreements, Huntington will disburse the funds directly to the dealership or, in some cases, to you for a private sale. With the financing secured, you can then complete your vehicle purchase and drive away in your new car. This final step marks the culmination of your efforts and the beginning of your ownership journey.

Securing the Best Rates and Terms: Pro Tips from Us

While Huntington offers competitive rates, there are several proactive steps you can take to ensure you secure the most favorable terms for your car loan. A little preparation and strategic planning can lead to significant savings over the life of your loan. Based on my extensive experience, these tips are universally effective.

1. Improve Your Credit Score:

This is perhaps the most impactful step. A higher credit score signals to lenders that you are a responsible borrower, directly translating to lower interest rates. Before applying, check your credit report for errors and work on reducing existing debt, paying bills on time, and avoiding new credit inquiries. Even a small bump in your score can make a difference. For instance, consider using a tool like Experian Boost (external link: https://www.experian.com/boost/) to potentially improve your score with utilities and streaming services.

2. Make a Substantial Down Payment:

A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. It also signals to Huntington that you are financially committed to the purchase, reducing their risk. Aim for at least 10-20% of the vehicle’s purchase price if possible.

3. Choose a Shorter Loan Term:

While a longer loan term means lower monthly payments, it also means you’ll pay more in total interest over time. Opting for the shortest loan term you can comfortably afford will save you a substantial amount of money in the long run. Calculate different scenarios to find your sweet spot between affordability and total cost.

4. Shop Around and Compare Offers:

Even if you’re set on Huntington, it’s wise to compare their offer with other lenders, such as credit unions or other major banks. This gives you leverage and ensures you’re getting the most competitive rate available. Common mistakes to avoid are accepting the first offer you receive without exploring alternatives.

5. Consider a Co-signer:

If your credit score is less than ideal or your income is borderline, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate. A co-signer essentially guarantees the loan, providing an added layer of security for Huntington. Just remember, a co-signer is equally responsible for the debt if you default.

Common Mistakes to Avoid When Applying for a Car Loan

Navigating the car loan application process can be tricky, and certain missteps can lead to higher interest rates, loan denial, or unnecessary financial strain. Being aware of these common pitfalls can help you avoid them, ensuring a smoother and more favorable outcome for your Huntington Car Loan.

1. Applying with a Low or Unchecked Credit Score:

One of the most frequent mistakes is not checking your credit score and report before applying. A low score can lead to rejection or very high interest rates. Furthermore, errors on your credit report can negatively impact your score. Always review your credit beforehand and address any inaccuracies.

2. Not Getting Pre-Approved:

Many buyers walk into a dealership without pre-approval, putting them at a disadvantage. Without a pre-approved loan, you don’t have a clear budget or a competitive offer to compare against dealership financing. This can lead to hurried decisions and less favorable terms. Pre-approval is a powerful negotiation tool.

3. Ignoring the Total Cost of the Loan:

Focusing solely on the monthly payment is a common trap. It’s crucial to consider the total cost of the loan, including interest, fees, and any additional charges. A lower monthly payment over a longer term often means paying significantly more in interest over time. Always ask for the total amount repayable.

4. Failing to Budget for Ownership Costs:

Beyond the loan payment, owning a car involves other substantial costs: insurance, fuel, maintenance, and potential repairs. Common mistakes to avoid are underestimating these expenses, which can strain your budget even if your loan payment is manageable. Create a comprehensive budget that includes all car-related expenses.

5. Not Reading the Fine Print:

Loan agreements can be lengthy and filled with legal jargon, but it’s imperative to read every clause carefully. Pay close attention to the interest rate (APR), fees (origination, late payment), prepayment penalties (if any), and the total loan amount. Don’t hesitate to ask Huntington representatives for clarification on anything you don’t understand.

Refinancing Your Car Loan with Huntington: A Path to Savings

If you’re already making car loan payments, you might be wondering if there’s an opportunity to improve your current terms. Huntington’s auto loan refinancing option offers a strategic way to potentially save money, reduce your monthly outgo, or even adjust your loan term to better suit your financial situation.

When is Refinancing a Good Idea?

Refinancing is typically beneficial in several scenarios. If your credit score has significantly improved since you first took out the loan, you might qualify for a lower interest rate. Similarly, if market interest rates have dropped, refinancing can help you capitalize on the more favorable environment. Another reason might be if you need to lower your monthly payments due to a change in your financial circumstances, or if you want to shorten your loan term to pay off the car faster. Pro tips from us: use an online refinancing calculator to estimate your potential savings before you commit.

The Refinancing Process:

The refinancing process with Huntington is quite similar to applying for a new loan. You’ll typically start by gathering your current loan details, including your current lender, outstanding balance, and interest rate. Then, you’ll apply to Huntington, providing your personal and financial information. They will review your credit and make an offer. If approved, Huntington will pay off your old loan, and you’ll begin making payments to them under the new, hopefully more advantageous, terms.

Benefits of Refinancing:

The primary benefits of refinancing include reducing your interest rate, which translates to lower overall costs. You can also lower your monthly payments by extending the loan term, providing more breathing room in your budget. Alternatively, you might choose to shorten the loan term to pay off the debt faster and reduce the total interest paid. Refinancing can also simplify your finances if you consolidate multiple car loans into one.

Beyond the Loan: Huntington’s Customer Support and Resources

A good financial partner offers more than just the product; they provide ongoing support and resources to empower their customers. Huntington Bank excels in this area, ensuring that once you have your car loan, you also have the tools and assistance to manage it effectively.

Online Banking and Account Management:

Huntington’s robust online banking platform and mobile app allow you to manage your car loan with ease. You can view your account details, make payments, set up automatic transfers, and track your payment history from anywhere, at any time. This digital convenience ensures that managing your loan fits seamlessly into your busy life.

Financial Education Resources:

Huntington often provides access to a wealth of financial education resources. These can include articles, calculators, and tools designed to help you understand personal finance better, manage debt, and plan for your future. These resources are invaluable for making informed financial decisions beyond just your car loan.

Alternatives to Consider (Briefly)

While Huntington Car Loans offer compelling advantages, it’s always wise to be aware of other financing avenues. This broader perspective ensures you’ve explored all options before making a final decision. Other lenders might cater to specific niche needs or offer different structures.

Credit Unions: Often known for competitive rates and a member-focused approach, credit unions can be a great alternative, especially if you qualify for membership.

Dealership Financing: Dealerships offer convenience and sometimes special manufacturer incentives, but their rates might not always be the most competitive compared to independent lenders.

Other Major Banks: Institutions like Chase, Bank of America, or Wells Fargo also offer robust auto loan programs, each with their own set of criteria and benefits.

Frequently Asked Questions (FAQs) About Huntington Car Loans

Navigating the specifics of a car loan can often lead to common questions. Here, we address some of the most frequently asked queries about Huntington Car Loans, providing clear and concise answers to help you on your journey.

1. How long does it typically take to get approved for a Huntington Car Loan?

The approval timeline can vary, but Huntington strives for efficiency. Often, you can receive a pre-qualification or pre-approval decision within minutes for online applications. For a full application, once all necessary documents are submitted, a final decision can typically be made within one to two business days. The speed often depends on the completeness of your application and the complexity of your financial profile.

2. Can I get a Huntington Car Loan with bad credit?

While a strong credit score significantly improves your chances and secures better rates, Huntington may consider applications from individuals with less-than-perfect credit. However, you might face higher interest rates or require a larger down payment or a co-signer. It’s always best to speak directly with a Huntington loan officer to discuss your specific situation and explore available options.

3. What documents do I need to apply for a Huntington Car Loan?

Generally, you’ll need a valid government-issued ID (like a driver’s license), your Social Security Number, proof of income (recent pay stubs, W-2s, or tax returns), proof of residency (utility bill or lease agreement), and details about the vehicle you intend to purchase (VIN, mileage, year, make, model). Having these ready will expedite your application.

4. Can I change my car loan payment date with Huntington?

Huntington often offers flexibility for customers to adjust their payment due date, provided it meets certain criteria and is within their policy guidelines. If you need to change your payment date to better align with your pay schedule, it’s recommended to contact Huntington’s customer service directly to discuss your options and ensure any changes are processed correctly.

5. What if I want to pay off my Huntington Car Loan early? Are there penalties?

Many borrowers are keen to pay off their loans ahead of schedule to save on interest. Fortunately, most Huntington Car Loans do not include prepayment penalties. This means you can make extra payments or pay off your loan in full at any time without incurring additional fees. However, it’s always a good practice to confirm this specific detail in your loan agreement or with a Huntington representative.

Conclusion: Your Road to Vehicle Ownership with Huntington

Securing a car loan is a significant financial decision, and choosing the right lender can profoundly impact your experience and your wallet. Huntington Car Loans offer a compelling package of competitive rates, flexible terms, and a customer-focused approach, backed by a legacy of trust and reliability. From new car purchases to refinancing existing loans, they provide tailored solutions designed to meet a diverse range of needs.

By understanding the eligibility requirements, meticulously navigating the application process, and implementing our pro tips for securing the best rates, you can confidently embark on your journey to vehicle ownership. Remember to avoid common pitfalls, ask questions, and leverage Huntington’s resources for a seamless experience. With Huntington, you’re not just getting a car loan; you’re gaining a financial partner committed to helping you drive away with peace of mind. Take the next step today and explore how a Huntington Car Loan can put you in the driver’s seat of your dream car.