Navigating the Road to Your Dream Car: A Deep Dive into The Car Loan Company

Navigating the Road to Your Dream Car: A Deep Dive into The Car Loan Company Carloan.Guidemechanic.com

The open road, the feel of the steering wheel in your hands, the freedom of movement – for many, owning a car represents more than just transportation; it’s a symbol of independence and a gateway to new experiences. However, the path to car ownership often involves a crucial partner: The Car Loan Company. These financial institutions are the unsung heroes that transform aspirations into reality, bridging the gap between desire and affordability.

But what exactly is a car loan company, and how do you choose the right one? This comprehensive guide will peel back the layers, offering an in-depth look at everything you need to know. We’ll empower you with the knowledge to make informed decisions, ensuring your journey to car ownership is smooth, transparent, and financially sound.

Navigating the Road to Your Dream Car: A Deep Dive into The Car Loan Company

Understanding "The Car Loan Company": More Than Just Lenders

At its core, a car loan company is a financial institution that provides funds to individuals or businesses specifically for the purchase of a vehicle. In return, the borrower agrees to repay the loan amount, plus interest, over a predetermined period. This arrangement makes car ownership accessible to millions who might not have the upfront cash to buy a vehicle outright.

These companies come in various forms, each with its own characteristics and advantages. Understanding these distinctions is your first step toward finding the perfect financial partner.

The Different Faces of Car Loan Companies

Not all lenders are created equal, and knowing the types can help you narrow your search. Each offers a slightly different approach to car financing.

-

Traditional Banks: These are the familiar financial giants. They offer a broad range of products, including auto loans, and often have competitive rates for customers with strong credit histories. Their established presence can offer a sense of security.

-

Credit Unions: Member-owned and non-profit, credit unions are known for often offering lower interest rates and more flexible terms than traditional banks. They prioritize their members’ financial well-being, making them an excellent choice if you qualify for membership.

-

Captive Finance Companies: These are financial arms directly associated with specific car manufacturers. Think Toyota Financial Services or Ford Credit. They primarily finance vehicles from their parent company, often offering special incentives, rebates, or lower interest rates on new cars to boost sales.

-

Independent Lenders (Online Lenders/Finance Companies): This category includes a wide array of specialized auto loan providers. Many operate exclusively online, streamlining the application process and sometimes catering to specific niches, such as bad credit car loans or unique vehicle types. They offer convenience and often quick decisions.

Choosing the right type of lender can significantly impact your loan terms and overall satisfaction. Each has its strengths, and your personal financial situation will often dictate which one is the best fit for you.

The Journey to Your Dream Car: Navigating the Car Loan Process

Securing a car loan might seem daunting, but breaking it down into manageable steps makes the process clear and straightforward. Based on my experience in the financial sector, a well-prepared borrower is always a successful borrower.

Step 1: Assessing Your Financial Health and Getting Pre-Approved

Before you even step foot on a dealership lot, understanding your financial standing is paramount. This initial assessment will determine what you can realistically afford and what kind of loan terms you might qualify for.

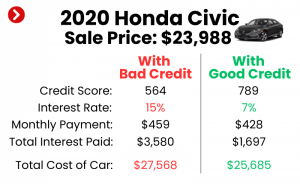

- Credit Score Importance: Your credit score is a three-digit number that tells lenders how responsibly you’ve managed debt in the past. A higher score typically translates to lower interest rates, as it signals less risk to the lender. If your score isn’t where you want it to be, taking steps to improve it before applying can save you thousands.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders use it to gauge your ability to take on additional debt. A lower DTI ratio indicates you have more disposable income to cover your car payments.

- Budgeting Realistically: Don’t just think about the monthly car payment. Factor in insurance, fuel, maintenance, and potential parking costs. A car is an ongoing expense, and understanding the total cost of ownership is crucial for long-term financial health.

Pro tip from us: Get pre-approved car loan before you start serious car shopping. Pre-approval gives you a clear budget and acts like cash in hand at the dealership, strengthening your negotiating position. It also separates the financing discussion from the car price discussion, simplifying both.

Step 2: Researching Loan Options & Comparing Offers

Once you know your financial standing, it’s time to shop for the loan itself. This is where you compare different car loan rates and terms.

- Understanding APR vs. Interest Rate: While the interest rate is the cost of borrowing the principal amount, the Annual Percentage Rate (APR) includes the interest rate plus any additional fees or charges associated with the loan. APR provides a more accurate picture of the total cost of borrowing. Always compare APRs when evaluating loan offers.

- Comparing Terms and Fees: Don’t just look at the monthly payment. A longer loan term might mean lower monthly payments but significantly higher total interest paid over the life of the loan. Also, be vigilant about origination fees, application fees, or prepayment penalties that can add to the overall cost.

- Utilizing Online Tools: Numerous online calculators and comparison websites allow you to input your credit score, desired loan amount, and term to get estimated rates from multiple lenders. This makes comparing offers efficient and transparent.

Step 3: Application and Documentation

When you’ve found a promising car loan company, the next step is the formal application. This involves providing detailed personal and financial information.

- Required Documents: You’ll typically need government-issued identification (driver’s license), proof of income (pay stubs, tax returns), proof of residency (utility bill), and potentially information about your employment and other debts. Having these documents ready beforehand speeds up the process.

- Completing the Application: Be thorough and accurate. Any discrepancies or incomplete information can delay your application or even lead to denial.

Common mistakes to avoid are: submitting an incomplete application or providing inconsistent information. Double-check everything before hitting submit.

Step 4: Loan Approval & Negotiation

If your application is approved, the lender will present you with a loan offer outlining the interest rate, term, monthly payment, and total cost.

- Understanding the Offer: Take your time to review every detail. Don’t feel rushed. If anything is unclear, ask for clarification.

- Negotiating Terms: While interest rates are often fixed based on your credit, you might have some room to negotiate other aspects, especially with independent lenders or if you have multiple offers. For instance, you might negotiate on fees or a slight adjustment to the loan term.

- Reading the Fine Print: This cannot be stressed enough. Understand all clauses, including late payment penalties, early payoff options, and any default provisions.

Step 5: Finalizing the Deal and Driving Away

Once you’re satisfied with the loan terms, it’s time to sign the dotted line.

- Signing the Contract: This legally binding document formalizes your agreement with the car loan company. Make sure all the terms you agreed upon are accurately reflected in the final contract.

- Understanding Payment Schedules: Know your due date, how to make payments, and who to contact if you have questions or encounter issues. Set up automatic payments if possible to avoid missing due dates.

Key Factors to Evaluate When Choosing a Car Loan Company

Selecting the right car loan company is a critical decision that impacts your finances for years. Beyond just the interest rate, several factors warrant careful consideration.

1. Interest Rates & APR: The True Cost of Borrowing

This is often the first thing borrowers look at, and for good reason. The interest rate dictates how much extra you’ll pay on top of the principal amount.

- How They’re Determined: Interest rates are influenced by your credit score, the loan term, the economy’s prime rate, and the lender’s risk assessment. A borrower with excellent credit will almost always qualify for a lower rate than someone with a fair or poor credit history.

- Impact on Total Cost: Even a seemingly small difference in interest rate can translate into thousands of dollars over a typical 5-year auto loan. For instance, on a $30,000 loan, a 1% difference in interest could mean paying an extra $800-$1000 over the loan term.

- Pro tip from us: Don’t just accept the first rate you’re offered. Shop around with at least three different lenders to ensure you’re getting the most competitive rate available to you.

2. Loan Terms: Finding Your Repayment Sweet Spot

The loan term is the duration over which you agree to repay the loan, typically measured in months (e.g., 36, 48, 60, 72, or even 84 months).

- Short vs. Long Terms: Shorter terms (e.g., 36 or 48 months) usually mean higher monthly payments but significantly less total interest paid because you’re borrowing money for a shorter period. Longer terms (e.g., 72 or 84 months) offer lower monthly payments, making the car more "affordable" on a month-to-month basis, but you’ll pay much more in interest over the life of the loan.

- The Right Balance: The ideal loan term balances manageable monthly payments with a reasonable total cost. Avoid extending the loan term simply to reduce the monthly payment if it means paying excessive interest or ending up "upside down" on your loan (owing more than the car is worth).

3. Fees & Charges: Uncovering Hidden Costs

Beyond the interest rate, various fees can inflate the overall cost of your car loan.

- Common Fees: Look out for origination fees (a charge for processing the loan), documentation fees, late payment fees, and sometimes even prepayment penalties (a fee for paying off your loan early).

- Prepayment Penalties: Some lenders charge a fee if you pay off your loan ahead of schedule. While less common with auto loans, it’s crucial to confirm whether your chosen car loan company imposes such a penalty, especially if you plan to pay off your debt early.

- Common mistakes to avoid are: overlooking these fees when comparing offers. Always ask for a full breakdown of all potential charges associated with the loan.

4. Customer Service & Reputation: Beyond the Numbers

While rates and terms are crucial, the quality of customer service and the lender’s reputation can significantly impact your experience, especially if you encounter issues.

- Online Reviews and Ratings: Check reviews on independent platforms, the Better Business Bureau (BBB), and consumer advocacy sites. Look for patterns in complaints or praises regarding responsiveness, transparency, and problem resolution.

- Accessibility and Responsiveness: How easy is it to reach a human being if you have a question? Does the company have clear communication channels? A lender that is difficult to contact can add unnecessary stress.

- Based on my experience: A reputable car loan company doesn’t just process loans; they act as a financial partner. They are transparent about their terms, responsive to inquiries, and willing to work with you if you face unexpected financial hardship. Trustworthiness is invaluable.

5. Flexibility & Special Programs: Tailored Solutions

Some car loan companies offer specialized programs or greater flexibility that might benefit specific borrowers.

- Refinancing Options: Does the lender offer options to refinance car loan in the future if interest rates drop or your credit score improves? This flexibility can save you money down the line. (Internal link suggestion: Refinancing Your Car Loan: When and Why It Makes Sense)

- First-Time Buyer Programs: Some lenders have programs designed to help individuals with limited credit history secure their first auto loan.

- Bad Credit Car Loans: For those with less-than-perfect credit, some specialized lenders focus on bad credit car loans, offering solutions where traditional banks might not. While rates may be higher, these loans can be a pathway to improving credit if managed responsibly.

The Benefits of Partnering with the Right Car Loan Company

Choosing the right car loan company offers numerous advantages beyond simply acquiring a vehicle.

- Accessibility to a Vehicle: The most obvious benefit is the ability to purchase a car without depleting your savings. This provides essential transportation for work, family, and daily life.

- Building Credit History Responsibly: Consistently making on-time payments on an auto loan is an excellent way to build a positive credit history. This can open doors to better rates on future loans, mortgages, and credit cards. (Internal link suggestion: Understanding Your Credit Score: A Comprehensive Guide)

- Predictable Budgeting: A fixed-rate car loan provides predictable monthly payments, making it easier to manage your budget and plan your finances.

- Financial Flexibility: By financing your car, you keep your savings intact for emergencies, investments, or other significant life events, maintaining greater financial liquidity.

Common Pitfalls and How to Avoid Them

Even with the best intentions, borrowers can sometimes fall into traps. Being aware of these common mistakes can help you navigate the process successfully.

- Not Shopping Around: This is perhaps the biggest mistake. Settling for the first loan offer, especially from a dealership, can cost you hundreds or even thousands of dollars in higher interest rates. Always compare at least three different loan offers.

- Ignoring Your Credit Score: Not knowing your credit score before applying means you’re going into negotiations blind. It’s your most powerful tool for securing favorable rates.

- Focusing Only on Monthly Payments: Dealerships and some lenders might try to "sell" you on a low monthly payment by extending the loan term. While the payment might seem appealing, it often results in paying significantly more interest over time. Always consider the total cost of the loan.

- Skipping the Fine Print: As mentioned earlier, hidden clauses, unexpected fees, or restrictive terms can reside in the details of the loan agreement. Take the time to read and understand everything before signing.

- Getting Upsold on Add-ons: Be wary of high-pressure sales tactics for unnecessary add-ons like extended warranties, GAP insurance (which can be valuable but often cheaper elsewhere), or rustproofing that might be inflated in price. Evaluate these separately and only if you truly need them.

Common mistakes to avoid are: feeling pressured into making a quick decision. Take your time, do your research, and ensure you’re comfortable with every aspect of the loan before committing.

Future Trends in Car Financing

The world of car financing is constantly evolving, driven by technological advancements and changing consumer expectations. Keeping an eye on these trends can help you anticipate future opportunities.

- Digital Lending Platforms: The rise of online-only lenders has made the application and approval process faster and more convenient. Expect more seamless digital experiences, from application to document submission.

- AI-Driven Credit Assessment: Artificial intelligence is increasingly being used to analyze a broader range of data points beyond traditional credit scores, potentially offering more personalized loan terms and making financing accessible to a wider demographic.

- Flexible Payment Models: Innovations like subscription models for cars or more flexible payment schedules tailored to individual income patterns might become more prevalent.

- Green Car Incentives: As environmental concerns grow, expect more specialized loan products and incentives for electric and hybrid vehicles, potentially offering lower rates or unique terms.

For more information on understanding consumer finance and making informed decisions, you can visit the Consumer Financial Protection Bureau (CFPB) website, a trusted external source for financial education and resources: Consumer Financial Protection Bureau.

Conclusion: Empowering Your Car Ownership Journey

The journey to owning your ideal car is an exciting one, and The Car Loan Company plays a pivotal role in making that dream a reality. By understanding the different types of lenders, meticulously navigating the loan process, and diligently evaluating key factors like interest rates, terms, and reputation, you empower yourself to make the best financial decision.

Remember, a car loan isn’t just a transaction; it’s a significant financial commitment. Approaching it with knowledge, patience, and a willingness to shop around will not only secure you a better deal but also set a strong foundation for your financial future. Drive away with confidence, knowing you’ve made an informed choice that serves your best interests. Start your research today, compare options, and take the first step toward the open road.