Navigating the Road to Your Dream Car: An In-Depth Guide to Capital One Credit Car Loans

Navigating the Road to Your Dream Car: An In-Depth Guide to Capital One Credit Car Loans Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect, but the financing aspect can often feel like a complex maze. For many prospective car owners, securing a reliable and affordable auto loan is the crucial first step. Among the prominent financial institutions offering vehicle financing, Capital One stands out with its unique approach, particularly its emphasis on credit-based solutions and user-friendly tools.

In this comprehensive guide, we’ll dive deep into everything you need to know about Capital One Credit Car Loans. We’ll explore their unique features, the application process, eligibility requirements, and expert tips to help you secure the best possible deal. Whether you have excellent credit, are rebuilding your financial standing, or simply exploring your options, understanding Capital One’s offerings can pave a smoother path to getting behind the wheel of your next car.

Navigating the Road to Your Dream Car: An In-Depth Guide to Capital One Credit Car Loans

What Exactly is a Capital One Credit Car Loan?

At its core, a Capital One Credit Car Loan is a financial product designed to help individuals purchase a vehicle, with the terms and approval largely dependent on the applicant’s creditworthiness. Unlike some traditional lenders that might focus solely on high-credit applicants, Capital One aims to serve a broader spectrum of consumers, making vehicle ownership accessible to more people. They leverage credit data to assess risk and offer personalized financing solutions.

Capital One’s approach to auto financing often begins with their innovative Auto Navigator tool. This online platform allows you to pre-qualify for a car loan without impacting your credit score, giving you a clear picture of your potential interest rate and monthly payment before you even step foot in a dealership. This transparency and preliminary understanding are key differentiators.

Based on my experience, many people feel overwhelmed by the car buying process, especially the financial part. Capital One tries to demystify this by putting crucial information, like your potential loan terms, right at your fingertips early in your search. This empowers buyers to shop with confidence, knowing what they can realistically afford.

How Capital One Approaches Auto Financing

Capital One views auto loans through the lens of credit and convenience. They’ve built a system that integrates credit assessment with a vast network of participating dealerships. This means your credit profile plays a significant role in determining not just whether you’re approved, but also the specific rates and terms you’ll be offered.

Their model focuses on providing a streamlined experience. From pre-qualification online to selecting a vehicle at an approved dealership, the process is designed to be as straightforward as possible. This integration helps reduce the stress and uncertainty commonly associated with car financing.

Why Consider Capital One for Your Car Loan?

There are several compelling reasons why Capital One has become a popular choice for auto financing. One of the primary advantages is their commitment to helping customers understand their financing options upfront. This proactive approach allows you to tailor your car search to what you’ve already been pre-qualified for.

Furthermore, Capital One’s willingness to work with a range of credit profiles makes them a viable option for many individuals who might face challenges with other lenders. While having excellent credit will undoubtedly secure you the best rates, Capital One often provides solutions for those with good, fair, or even rebuilding credit.

Understanding Capital One’s Auto Navigator Tool

The Capital One Auto Navigator is arguably the cornerstone of their auto loan experience. This powerful online platform revolutionizes how people shop for cars and secure financing, shifting much of the control back to the consumer. It’s designed to give you a personalized financing offer even before you visit a dealership.

This tool is more than just an application; it’s a comprehensive resource. It allows you to search for vehicles, estimate payments, and get pre-qualified all in one place. This level of upfront information can save you considerable time and potential frustration during the car buying process.

The Pre-Qualification Advantage

One of the most significant benefits of using Auto Navigator is the pre-qualification feature. When you pre-qualify, Capital One performs a "soft inquiry" on your credit report. This type of inquiry does not affect your credit score, which is a massive advantage. You can see your personalized rate and terms without any commitment or credit score impact.

This pre-qualification gives you tangible figures to work with. You’ll know your potential interest rate, the maximum loan amount, and an estimated monthly payment. Armed with this knowledge, you can approach dealerships with confidence, knowing exactly what you can afford and what your financing terms might look like.

How Auto Navigator Simplifies the Car Buying Journey

The Auto Navigator streamlines the entire car buying journey. After pre-qualifying, you can then browse vehicles from participating dealerships directly through the platform. This means you’re looking at cars that are available within your pre-qualified budget, avoiding the disappointment of falling in love with a vehicle you can’t finance.

It also connects you with Capital One’s network of approved dealerships. This takes the guesswork out of finding a dealer that accepts Capital One financing, ensuring a smoother transition from online pre-qualification to final purchase. The entire process is designed for efficiency and clarity.

Personalized Offers at Your Fingertips

The offers you receive through Auto Navigator are personalized based on your credit profile. This means the rates and terms are specific to your financial situation, rather than generic estimates. This personalization ensures that the financing options presented are realistic and tailored to your individual needs.

Having a personalized offer in hand provides significant leverage when negotiating at the dealership. You’re not starting from scratch; you already have a strong financing offer to compare against any offers the dealership might present. This transparency is invaluable.

Eligibility Requirements: Are You Ready for a Capital One Credit Car Loan?

Before you jump into the application process, it’s crucial to understand the eligibility criteria for a Capital One Credit Car Loan. While Capital One aims to be inclusive, there are fundamental requirements that all applicants must meet. Knowing these in advance can help you prepare and increase your chances of approval.

These requirements typically revolve around your financial stability and credit history. Capital One, like any lender, wants to ensure you have the capacity and willingness to repay the loan. Being prepared for these assessments is key to a successful application.

Credit Score: The Foundation

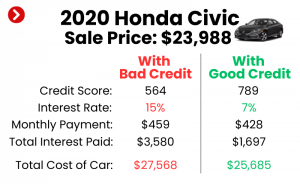

Your credit score is arguably the most influential factor in your loan application. Capital One considers a range of credit scores, but a higher score generally translates to better interest rates and more favorable terms. While there isn’t a single "minimum" score publicly stated, most successful applicants will have at least a fair credit score or better.

Based on my experience working with various lenders, a FICO score of 600 or above is often a good starting point for general auto loan consideration, with scores in the good (670-739) to excellent (740+) ranges unlocking the most competitive offers. If your score is lower, Capital One might still offer financing, but it could come with a higher interest rate to offset the perceived risk.

Income and Employment Stability

Lenders need to see that you have a consistent and sufficient income to cover your monthly loan payments, along with your other financial obligations. Capital One will typically require proof of income, such as recent pay stubs, tax returns, or bank statements. Stable employment history is also a significant plus.

A consistent work history demonstrates reliability and a steady flow of income. Lenders often prefer to see at least six months to a year of continuous employment. This gives them confidence in your ability to manage ongoing financial commitments.

Debt-to-Income Ratio (DTI)

Your debt-to-income (DTI) ratio is another critical metric. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income available to manage new debt, such as a car loan.

While specific DTI thresholds can vary, a ratio below 40% is generally considered favorable. If your DTI is too high, it might signal to Capital One that adding another monthly payment could put a strain on your finances, potentially impacting your approval or the terms offered.

Residency and Age Requirements

Like all financial products, there are basic demographic requirements. You must be at least 18 years old (or 19 in Alabama and Nebraska) and a permanent U.S. resident. You’ll also need to provide a valid U.S. street address. These are standard checks to ensure legal eligibility and proper identification.

It’s important to have all your personal identification documents readily available. This includes a valid driver’s license or state-issued ID, which will be necessary not just for the loan but also for registering your new vehicle.

The Application Process: Your Step-by-Step Guide

Securing a Capital One Credit Car Loan is a relatively straightforward process, especially when utilizing their Auto Navigator tool. Understanding each phase can help you navigate it efficiently and confidently. There are distinct steps, starting from initial inquiry to final vehicle purchase.

This phased approach is designed to give you control and clarity at each stage. It minimizes surprises and ensures you’re well-informed before making any major commitments.

Phase 1: Pre-Qualification (Soft Credit Pull)

The journey begins with pre-qualification through the Capital One Auto Navigator. This is where you input basic personal and financial information, such as your name, address, income, and desired loan amount. As mentioned, this involves a soft inquiry on your credit report, which means no impact on your credit score.

Within minutes, you’ll receive personalized offers, including your potential interest rate and monthly payment. This step is crucial for understanding your financial boundaries before you start serious car shopping. It’s an excellent way to get a realistic picture without any commitment.

Phase 2: Visiting a Participating Dealership

Once you have your pre-qualification offer, the next step is to visit one of the thousands of dealerships in Capital One’s network. You can find these dealerships directly through the Auto Navigator tool, ensuring you select a dealer that accepts Capital One financing.

When you arrive, inform the sales team that you have a Capital One pre-qualification. They will then help you find a vehicle that meets both your needs and your pre-qualified loan terms. This makes the shopping experience much more focused and less stressful.

Phase 3: Finalizing Your Loan (Hard Credit Pull)

After you’ve selected your vehicle, the dealership will work with Capital One to finalize your loan. At this stage, Capital One will perform a "hard inquiry" on your credit report. This hard inquiry is a standard part of any formal loan application and will temporarily affect your credit score by a few points.

The dealership will submit your full application to Capital One, confirming all your details and the chosen vehicle. Once approved, you’ll sign the final loan documents, and you’re ready to drive off the lot in your new car. The entire process from pre-qualification to final signing is designed to be as seamless as possible.

Pro Tip: What to Bring to the Dealership

To expedite the final loan process, ensure you have these documents ready when you visit the dealership:

- Your Capital One pre-qualification offer (printout or digital access).

- Valid driver’s license.

- Proof of income (recent pay stubs, bank statements, or tax returns).

- Proof of residence (utility bill, lease agreement).

- Proof of insurance (or be prepared to obtain it on the spot).

- Trade-in title/registration (if applicable).

Decoding Interest Rates and Loan Terms

Understanding the interest rate and loan terms is vital, as they directly impact the total cost of your car loan and your monthly payments. Capital One, like all lenders, calculates these based on a variety of factors, and being informed can help you make the best financial decisions.

Don’t just look at the monthly payment in isolation; consider the total cost of the loan over its entire duration. A lower monthly payment often means a longer loan term, which can result in paying significantly more in interest over time.

Factors Influencing Your Rate

Several elements come into play when Capital One determines your interest rate. Your credit score is paramount; a higher score generally indicates lower risk and therefore qualifies you for a lower rate. Other factors include the loan term (shorter terms often have slightly lower rates), the amount you’re borrowing, and the age and mileage of the vehicle.

The current market interest rates also play a role. When overall interest rates are high, auto loan rates tend to follow suit. Capital One takes all these variables into account to provide you with a personalized offer that reflects your unique financial profile and the economic climate.

The Power of a Down Payment

Making a down payment is one of the smartest moves you can make when financing a car. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. It also signals to Capital One that you are a serious and committed borrower.

A significant down payment can also help you secure a better interest rate, especially if your credit score is not in the excellent range. It reduces the lender’s risk, making them more inclined to offer favorable terms. Even a modest down payment can make a noticeable difference.

Choosing the Right Loan Term

Capital One typically offers various loan terms, ranging from 36 to 72 months, and sometimes even longer. While a longer term will result in lower monthly payments, it also means you’ll pay more in interest over the life of the loan. Conversely, a shorter term will have higher monthly payments but save you money on interest in the long run.

It’s crucial to strike a balance between affordability and total cost. Consider your budget carefully and choose a term that you can comfortably manage without overextending your finances. Pro tips from us suggest aiming for the shortest term you can reasonably afford.

Common Mistake to Avoid: Focusing Only on the Monthly Payment

Many car buyers make the mistake of focusing solely on the monthly payment. While it’s important for budgeting, it can be misleading. A low monthly payment might sound appealing, but if it’s stretched over an excessively long term, you could end up paying thousands more in interest. Always consider the total cost of the loan and the interest rate, not just the monthly outlay.

Credit Score and Its Pivotal Role

Your credit score isn’t just a number; it’s a reflection of your financial responsibility and directly impacts your ability to secure a Capital One Credit Car Loan, as well as the terms you’re offered. Understanding how Capital One views your credit and how you can improve it is fundamental.

A good credit score opens doors to more favorable lending opportunities. It demonstrates to lenders that you have a history of managing debt responsibly and are a lower risk for defaulting on payments.

How Capital One Views Your Credit

Capital One utilizes your credit report and score to assess your creditworthiness. They look for patterns of on-time payments, low credit utilization, and a diverse credit history. A strong credit profile indicates a reliable borrower who is likely to repay their auto loan as agreed.

Conversely, a history of late payments, defaults, or high credit card balances can signal higher risk. While Capital One does work with various credit profiles, these factors will likely lead to higher interest rates or stricter loan terms to mitigate the perceived risk.

Improving Your Credit Before Applying

If your credit score isn’t where you want it to be, taking steps to improve it before applying for a Capital One Credit Car Loan can significantly benefit you. Pro tips from us include:

- Pay bills on time: Payment history is the biggest factor in your credit score.

- Reduce credit card balances: Lowering your credit utilization ratio can quickly boost your score.

- Check your credit report for errors: Disputing inaccuracies can improve your score.

- Avoid opening new lines of credit: New credit inquiries can temporarily lower your score.

Even small improvements can translate into better loan offers. Planning ahead and giving yourself a few months to focus on credit repair can pay off handsomely in lower interest costs.

The Impact of Your Loan on Your Credit History

Successfully managing a Capital One Credit Car Loan can have a positive impact on your credit history. Making consistent, on-time payments demonstrates responsible credit behavior, which can gradually improve your credit score. This is especially beneficial if you’re looking to build or rebuild your credit.

However, missing payments or defaulting on the loan will severely damage your credit score, making it harder to obtain future credit. Treat your car loan as a serious financial commitment, and it can serve as a powerful tool for establishing a strong credit foundation.

New vs. Used Vehicles: Capital One’s Stance

Capital One provides financing for both new and used vehicles, but there can be subtle differences in the terms and conditions based on the car’s age and mileage. It’s important to understand these distinctions as you shop for your next ride.

Whether you’re eyeing a brand-new model or a pre-owned gem, Capital One aims to offer flexible solutions. However, the perceived risk associated with older vehicles can sometimes influence loan specifics.

Financing a New Car

Financing a new car with Capital One is generally straightforward. New vehicles typically present less risk to lenders due to their lower likelihood of immediate mechanical issues and higher resale value. This can sometimes translate into slightly better interest rates or more flexible terms for well-qualified borrowers.

The Auto Navigator tool will seamlessly guide you through new car options within their dealership network, making it easy to see what you’re pre-qualified for. New car loans often have longer terms available, though it’s always wise to consider the total cost over time.

Financing a Used Car (Vehicle Age/Mileage Limits)

Capital One also offers robust financing for used cars, which is a popular choice for many budget-conscious buyers. However, there are usually specific criteria for the used vehicles they will finance. Typically, Capital One has limits on the age and mileage of the used cars they will lend on.

While these limits can vary, common restrictions might be a maximum of 10 years old and/or 120,000 to 150,000 miles. These limits help mitigate the risk associated with older, higher-mileage vehicles that may be more prone to mechanical failures. Always check the most current guidelines on the Auto Navigator tool when considering a used vehicle.

Refinancing Your Existing Car Loan with Capital One

Did you know Capital One also offers options for refinancing an existing car loan? If you’ve previously financed a vehicle with another lender, and your financial situation or credit score has improved, refinancing could be a smart move to save money.

Refinancing means taking out a new loan, often with a lower interest rate or different terms, to pay off your current car loan. This can lead to lower monthly payments or significant savings over the life of the loan.

When Refinancing Makes Sense

Refinancing with Capital One makes sense in several scenarios:

- Improved Credit Score: If your credit score has significantly increased since you took out your original loan, you might qualify for a much lower interest rate.

- Lower Interest Rates: If market interest rates have dropped since your initial purchase, refinancing could secure you a better deal.

- High Original Rate: Perhaps you had poor credit when you first bought the car and received a high interest rate. Refinancing can help you escape that costly rate.

- Lower Monthly Payments: You might want to extend your loan term to reduce your monthly payments, though be mindful of increased total interest.

Pro tips from us suggest regularly checking your credit score and current auto loan rates. If there’s a significant difference, exploring Capital One’s refinancing options could be highly beneficial.

The Refinancing Process

The process for refinancing a car loan with Capital One is similar to applying for a new loan. You’ll typically start by applying for pre-qualification online. Capital One will assess your creditworthiness and provide you with potential new rates and terms.

If you like the offer, you’ll proceed with the full application, and Capital One will work to pay off your old loan. It’s a straightforward way to potentially reduce your financial burden and gain more favorable terms on your existing vehicle. For more detailed information, consider reading our (placeholder for internal link).

Advantages of Choosing Capital One for Your Car Loan

Capital One has carved out a strong niche in the auto loan market, offering several distinct advantages that appeal to a wide range of consumers. Their approach is designed for clarity, convenience, and accessibility.

Understanding these benefits can help you decide if Capital One is the right fit for your vehicle financing needs. Their commitment to technology and customer experience sets them apart.

Streamlined Pre-Qualification

The ability to pre-qualify online without impacting your credit score is a major selling point. This feature provides immediate feedback on your potential loan terms, empowering you to shop for cars with a precise budget in mind. It removes much of the guesswork from the initial stages of car buying.

This pre-qualification process saves time at the dealership and reduces the anxiety often associated with negotiating financing. You walk in with a solid offer, putting you in a stronger position.

Extensive Dealership Network

Capital One boasts a vast network of participating dealerships across the country. This means you’re likely to find an approved dealer near you, offering a wide selection of vehicles that can be financed through Capital One. The Auto Navigator tool helps you locate these dealerships easily.

This extensive network ensures that your pre-qualification is widely accepted, simplifying the transition from online research to an in-person purchase. It creates a cohesive car buying experience.

User-Friendly Online Tools

Beyond the Auto Navigator, Capital One provides excellent online account management tools. Once your loan is active, you can easily manage payments, view statements, and access loan details from the comfort of your home. This digital convenience is a significant advantage in today’s fast-paced world.

Their commitment to digital solutions makes the entire loan lifecycle, from application to repayment, more manageable and accessible. This reduces the need for phone calls or physical visits to manage your account.

Flexible Options for Various Credit Profiles

Capital One is known for its willingness to work with a broader range of credit scores compared to some other prime lenders. While excellent credit will always yield the best rates, they often provide viable financing solutions for individuals with good, fair, and even some subprime credit histories.

This inclusivity makes Capital One an attractive option for those who might be rebuilding their credit or have faced challenges in the past. It offers a pathway to vehicle ownership that might not be available elsewhere.

Potential Downsides and Considerations

While Capital One offers many benefits, it’s also important to be aware of potential downsides and considerations. No financial product is perfect for everyone, and understanding these aspects will help you make a fully informed decision.

A balanced perspective is key. What might be a minor inconvenience for one person could be a significant hurdle for another, depending on individual circumstances.

Specific Dealership Network

While Capital One has an extensive network of participating dealerships, it’s not every dealership. This means you are somewhat restricted to purchasing from dealers within their network if you want to use your Capital One pre-qualification. If you find a perfect car at a non-participating dealer, you might need to seek alternative financing.

This limitation means you should always verify if a dealership is part of the Capital One network before getting too attached to a specific vehicle on their lot. The Auto Navigator tool is your best friend here.

Rates Might Vary

While Capital One aims to provide competitive rates, the actual interest rate you receive will depend heavily on your credit profile, the loan term, and the current market conditions. For those with lower credit scores, the rates offered might be higher than what prime borrowers receive from other lenders.

It’s always wise to compare your Capital One offer with pre-approvals from other lenders, especially if you have excellent credit, to ensure you’re getting the most competitive rate available. Shopping around is always a good strategy.

No Direct Private Party Sales

Capital One Auto Loans are typically for vehicles purchased from their network of approved dealerships. They generally do not finance private party sales (i.e., buying a car directly from an individual owner). This is a common restriction for many large auto lenders due to the increased risk and complexity involved.

If your heart is set on a specific car being sold by a private seller, you would need to explore other financing options, such as a personal loan from a bank or credit union, which might have different terms and rates.

Expert Tips for a Smooth Capital One Car Loan Experience

To maximize your chances of a successful and stress-free Capital One Credit Car Loan experience, here are some expert tips and common mistakes to avoid. These insights come from years of observing the auto financing landscape and helping consumers make informed decisions.

Preparation and prudence are your best allies when navigating the world of car loans. A little foresight can save you a lot of money and headaches.

Pro Tip 1: Know Your Budget Before You Start

Before you even look at cars or apply for pre-qualification, determine your overall budget. This isn’t just about the monthly payment; it includes insurance, fuel, maintenance, and potential registration fees. Understand what you can truly afford without stretching your finances too thin.

Having a clear budget in mind will help you set realistic expectations for your loan amount and vehicle choice. It prevents "payment shock" down the line and ensures your new car is a joy, not a burden.

Pro Tip 2: Don’t Skip Pre-Qualification

This cannot be emphasized enough. Using the Capital One Auto Navigator for pre-qualification is a game-changer. It gives you a clear financial picture without impacting your credit score. You’ll know your rate, terms, and maximum loan amount before engaging with any salesperson.

Walking into a dealership with a pre-qualification offer puts you in a position of power. You’re negotiating for the car price, not just the monthly payment, and you already have financing secured.

Pro Tip 3: Negotiate the Car Price, Not Just the Payment

Salespeople often try to focus on the monthly payment. While important, always negotiate the total price of the car first. Once you’ve agreed on a price, then you can discuss the financing details, leveraging your Capital One pre-qualification.

If you negotiate solely on monthly payment, dealers can manipulate the loan term or add unnecessary extras to keep the payment low, ultimately costing you more in the long run. Separate the car negotiation from the financing negotiation.

Pro Tip 4: Understand All Fees

Before signing any documents, thoroughly review all fees associated with the loan and the vehicle purchase. This includes documentation fees, registration fees, extended warranty costs, and any other add-ons. Question anything you don’t understand or feel is unnecessary.

Common mistakes to avoid are blindly accepting all add-ons. Many extras, like extended warranties or GAP insurance, can be purchased separately or might not be necessary for your situation. Always evaluate their value critically.

Pro Tip 5: Consider a Co-Applicant

If your credit score is on the lower side or your income is just sufficient, consider applying with a co-applicant who has a stronger credit profile. This can significantly improve your chances of approval and help you secure a lower interest rate.

A co-applicant shares responsibility for the loan, and their good credit can bolster the application. Just ensure both parties understand the commitment, as both will be legally responsible for the debt.

Common Mistakes to Avoid Are:

- Overextending Your Budget: Don’t let the excitement of a new car push you into a loan that makes your monthly budget uncomfortably tight.

- Ignoring Your Credit Report: Always check your credit report for errors before applying for any loan. Incorrect information can negatively impact your rates.

- Rushing the Process: Car buying and financing should not be rushed. Take your time, do your research, and read all documents carefully before signing.

- Not Shopping Around: Even with a Capital One pre-qualification, it’s wise to compare offers from a few different lenders to ensure you’re getting the best possible deal. (placeholder for internal link).

Managing Your Capital One Auto Loan

Once you’ve secured your Capital One Credit Car Loan and driven off the lot, the journey isn’t over. Effective management of your loan is crucial for maintaining good financial health and potentially improving your credit score. Capital One provides robust tools to make this easy.

Responsible loan management ensures you avoid late fees, maintain a positive payment history, and ultimately pay off your vehicle as planned. It’s an ongoing commitment that contributes to your overall financial well-being.

Online Account Access

Capital One offers a user-friendly online portal and mobile app where you can manage your auto loan account. Through these platforms, you can:

- View your loan balance and payment history.

- Set up automatic payments.

- Make one-time payments.

- Access your statements and tax documents.

- Update your contact information.

This digital access puts you in control, allowing you to monitor your loan from anywhere at any time. It’s a convenient way to stay on top of your financial obligations.

Payment Options

Capital One provides several convenient payment options to ensure you never miss a due date. You can set up automatic payments directly from your bank account, make one-time payments online, pay by phone, or even send payments by mail.

Choosing the method that works best for your financial habits is important. Automatic payments are often recommended to ensure timely payments and avoid late fees, which can negatively impact your credit score.

Customer Service

Should you have any questions or encounter issues with your Capital One auto loan, their customer service channels are readily available. You can typically reach them via phone, email, or through secure messaging within your online account.

Having reliable customer support is reassuring, knowing that help is available if you need to discuss payment options, resolve discrepancies, or understand specific loan terms. For official contact information and resources, always refer to the Capital One Auto Navigator website.

Conclusion: Driving Forward with Confidence

Securing a Capital One Credit Car Loan can be a straightforward and empowering experience, especially when you leverage their innovative tools like the Auto Navigator. By understanding the pre-qualification process, eligibility requirements, and the various factors that influence your loan terms, you can approach car financing with confidence and clarity.

Remember, the goal is not just to get a car, but to secure financing that aligns with your financial goals and capabilities. By following our expert tips, avoiding common mistakes, and managing your loan responsibly, you’ll be well on your way to enjoying your new vehicle without unnecessary financial stress. Capital One offers a pathway for many to