Navigating the Road to Your Dream Car: How Do Car Loans Work Through A Bank?

Navigating the Road to Your Dream Car: How Do Car Loans Work Through A Bank? Carloan.Guidemechanic.com

The exhilarating prospect of owning a new car is often intertwined with the practical reality of financing. For many, a car loan from a bank is the most common and reliable path to making that dream a reality. However, the process can sometimes feel like a complex labyrinth of jargon and requirements. Understanding "how do car loans work through a bank" is not just about getting approved; it’s about securing the best terms, saving money, and driving away with peace of mind.

As an expert in automotive financing, I’ve seen countless individuals navigate this journey. My mission in this comprehensive guide is to demystify the entire process, providing you with the knowledge and confidence to approach bank car loans effectively. We’ll explore every facet, from initial preparation to the final signature, ensuring you’re well-equipped to make informed decisions.

Navigating the Road to Your Dream Car: How Do Car Loans Work Through A Bank?

The Foundation: What Exactly is a Car Loan?

At its core, a car loan is a sum of money borrowed from a financial institution, like a bank, specifically for the purpose of purchasing a vehicle. In exchange for this loan, you agree to repay the borrowed amount, known as the principal, along with an additional charge called interest, over a predetermined period, or term.

The bank acts as the lender, providing the capital necessary for your purchase. They do this with the expectation of a return on their investment, which comes in the form of the interest you pay. This financial agreement is a binding contract, outlining your repayment obligations and the bank’s rights as a lienholder on the vehicle until the loan is fully satisfied.

Setting Yourself Up for Success: Pre-Loan Preparation is Key

Before you even step into a dealership or submit an application, a crucial phase of preparation can significantly influence the success and affordability of your car loan. This proactive approach allows you to understand your financial standing and position yourself as an attractive borrower.

Your Credit Score: The Ultimate Financial Report Card

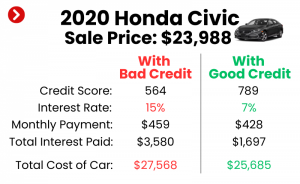

Your credit score is arguably the most critical factor banks consider when evaluating your loan application. This three-digit number, generated from your credit history, provides lenders with a snapshot of your financial reliability. It reflects your past behavior in managing debt, including how consistently you make payments and your overall debt load.

Banks use your credit score to assess the risk associated with lending you money. A higher credit score, typically above 700, indicates a lower risk, often translating into more favorable interest rates and better loan terms. Conversely, a lower score might lead to higher interest rates or even loan denial, as it suggests a greater risk of default.

Based on my experience, consistently paying bills on time, keeping credit utilization low, and avoiding excessive new credit applications are excellent strategies for maintaining a strong credit profile. It’s always wise to check your credit report for inaccuracies before applying for a major loan like a car loan.

Budgeting and Affordability: Knowing Your Limits

It’s tempting to focus solely on the car’s sticker price, but a responsible car purchase hinges on understanding your true affordability. This goes beyond just the monthly loan payment. You need to account for all associated costs, including insurance, fuel, maintenance, and registration fees. These often overlooked expenses can quickly add up, straining your budget.

A key metric banks consider is your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments (including the proposed car loan) to your gross monthly income. Lenders prefer a lower DTI, as it indicates you have sufficient income to manage your existing obligations and take on new ones. A high DTI can signal financial strain, making banks hesitant to approve additional credit.

Pro tips from us: Create a realistic budget that factors in all potential car ownership costs. Use online calculators to estimate various loan scenarios, including different interest rates and terms, to see how they impact your monthly payment. This foresight prevents financial stress down the line.

The Power of a Down Payment

A down payment is an upfront sum of money you pay towards the purchase of the car, reducing the total amount you need to borrow. This seemingly simple act carries significant weight in the eyes of a bank and offers several advantages to you as a borrower.

Firstly, a substantial down payment reduces the principal loan amount, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. Secondly, it signals to the bank that you are a serious and committed borrower, often leading to better interest rates. Thirdly, a larger down payment can help you avoid being "upside down" on your loan, where you owe more on the car than it’s worth, especially in the early years of ownership when depreciation is highest.

Common mistakes to avoid are underestimating the value of a down payment or skipping it entirely. Even a modest down payment can make a noticeable difference in your loan terms and overall financial health. Aim for at least 10-20% of the car’s purchase price if your budget allows.

The Application Process: Step-by-Step Through the Bank

Once your financial house is in order, the next phase involves actively engaging with banks to secure your car loan. This process typically involves pre-approval, the formal application, and the bank’s underwriting review.

Pre-Approval: Your Strategic Advantage

Seeking pre-approval from a bank is a highly recommended first step before you even visit a dealership. During pre-approval, the bank evaluates your creditworthiness and provides you with an estimated loan amount and interest rate, without committing to a specific vehicle. This gives you a clear budget and an idea of the financing terms you qualify for.

The benefits of pre-approval are numerous. It empowers you to negotiate with confidence at the dealership, knowing exactly how much financing you have secured independently. It also streamlines the car-buying process, allowing you to focus on choosing the right vehicle rather than scrambling for financing on the spot. Furthermore, a pre-approval gives you a benchmark to compare against any financing offers the dealership might present.

The Formal Application and Required Documentation

Once you’ve identified a specific vehicle and are ready to proceed, you’ll submit a formal car loan application to your chosen bank. This application will require detailed personal and financial information to enable the bank to make a definitive lending decision.

Typically, you’ll need to provide:

- Personal Identification: Driver’s license, social security number.

- Proof of Income: Pay stubs, tax returns, employment verification.

- Proof of Residency: Utility bills, lease agreement.

- Credit History: The bank will pull your credit report.

- Vehicle Information: Make, model, year, VIN (Vehicle Identification Number), and purchase price.

Ensure all your documentation is accurate and readily available. Incomplete applications can cause delays and frustration, potentially impacting your approval timeline.

Underwriting and Review: The Bank’s Assessment

After you submit your application, it enters the underwriting phase. This is where the bank’s loan officers meticulously review all the provided information to assess the risk of lending to you. They scrutinize several key factors:

- Creditworthiness: Your credit score and history are paramount. They look for consistent payment history, reasonable credit utilization, and a manageable number of existing credit accounts.

- Income Stability: They want to see a steady and sufficient income source to ensure you can comfortably afford the monthly payments.

- Debt-to-Income Ratio: As discussed, a healthy DTI ratio demonstrates your ability to manage existing and new debt.

- Vehicle Value: The bank will also assess the car itself, ensuring its value aligns with the loan amount. Since the car often serves as collateral, its worth is important to the lender.

Common mistakes to avoid are applying with multiple lenders simultaneously, which can temporarily ding your credit score with numerous hard inquiries, or providing inconsistent information across different applications. Be transparent and accurate to facilitate a smooth review process.

Understanding the Fine Print: Key Elements of Your Car Loan

Securing a car loan involves more than just a monthly payment. It’s crucial to understand the various components that make up your loan agreement. Each element plays a significant role in the overall cost and structure of your financing.

Principal Amount: The Core of Your Loan

The principal amount is the actual sum of money you borrow from the bank to purchase the car. It’s the purchase price of the vehicle minus any down payment, trade-in value, or other upfront credits. This is the base figure upon which all interest calculations are made.

For example, if a car costs $30,000 and you make a $5,000 down payment, your principal loan amount would be $25,000. Understanding this figure is essential because it directly impacts your monthly payments and the total interest you’ll accrue.

Interest Rate (APR): The Cost of Borrowing

The interest rate is essentially the cost you pay to the bank for borrowing the principal amount. It’s expressed as a percentage of the principal and is a critical factor in determining your monthly payment and the total cost of the loan over its term. Banks typically quote an Annual Percentage Rate (APR), which includes the interest rate plus certain fees, giving you a more comprehensive picture of the loan’s annual cost.

Factors influencing your interest rate include your credit score, the loan term, the down payment size, and current market interest rates. A lower APR means less money spent on interest over the life of the loan. Based on my experience, even a slight difference in APR can save you hundreds, if not thousands, of dollars over several years.

Loan Term: How Long You’ll Be Paying

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). The loan term has a direct impact on both your monthly payment and the total interest paid.

- Shorter terms (e.g., 36 or 48 months) generally result in higher monthly payments but lower total interest paid because you’re paying off the principal faster.

- Longer terms (e.g., 72 or 84 months) offer lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll end up paying significantly more in total interest over the longer duration.

Pro tips from us: While a longer term might reduce your monthly burden, always calculate the total cost over the life of the loan. Sometimes, a slightly higher monthly payment for a shorter term is a much better long-term financial decision.

Monthly Payments: Your Regular Obligation

Your monthly payment is the fixed amount you pay to the bank each month until the loan is fully repaid. This payment is comprised of a portion of the principal amount and a portion of the interest. In the early stages of a loan, a larger percentage of your payment goes towards interest, gradually shifting to more principal as the loan matures.

It’s crucial to ensure your monthly payment fits comfortably within your budget, allowing for other essential expenses and savings. Missing payments can lead to late fees, negative impacts on your credit score, and eventually, vehicle repossession.

Fees and Charges: Beyond Principal and Interest

While principal and interest are the main components, car loans can sometimes include additional fees. These might include:

- Origination fees: A charge for processing the loan.

- Documentation fees: For handling paperwork.

- Late payment fees: Penalties for missed or delayed payments.

- Prepayment penalties: Less common with car loans, but some lenders might charge a fee if you pay off your loan early. Always check for this in your loan agreement.

Always ask for a full disclosure of all fees before signing any loan agreement. Transparency is key to understanding your total financial commitment.

Collateral: The Car as Security

In the context of a car loan, the vehicle itself serves as collateral. This means that if you fail to make your loan payments as agreed, the bank has the legal right to repossess the car to recover their losses. This is why banks are very particular about the car’s value and condition.

Because the car acts as security, the bank maintains a lien on the vehicle title until the loan is fully paid off. Once you’ve made your final payment, the bank releases the lien, and you receive a clear title, indicating full ownership.

Approval, Acceptance, and Beyond: What Happens Next?

Once the bank has processed your application and you’ve understood the loan components, the final stages involve accepting the offer and managing your new financial commitment.

Reviewing the Loan Offer

If your loan application is approved, the bank will present you with a formal loan offer. This document outlines all the terms and conditions of your loan, including the principal amount, interest rate (APR), loan term, monthly payment, and any associated fees.

It is absolutely critical to read this offer thoroughly. Don’t hesitate to ask questions about anything you don’t understand. Ensure the terms match what you discussed and that there are no hidden clauses. This is your final opportunity to clarify any ambiguities before committing.

Acceptance and Closing the Deal

Once you are satisfied with the loan offer, you will formally accept it by signing the loan agreement. This makes the agreement legally binding. At this point, you’re committing to the repayment schedule and terms outlined in the document.

The "closing" typically involves the finalization of paperwork, where all parties (you, the bank, and sometimes the dealership) sign the necessary documents. This step confirms your acceptance of the financing and moves the process forward.

Disbursement of Funds

After the loan agreement is signed, the bank will disburse the funds. In most car loan scenarios, the money is not directly given to you. Instead, the bank will transfer the approved loan amount directly to the car dealership to cover the purchase price of the vehicle. This is a seamless process that usually occurs electronically, allowing you to take possession of your new car.

Making Payments and Managing Your Loan

With the car in your driveway, your primary responsibility shifts to making your monthly payments on time, every time. Most banks offer various convenient payment methods, including online payments, automatic deductions from your bank account, or payments by mail. Setting up auto-pay is a common strategy to ensure payments are never missed.

It’s also wise to keep track of your loan balance and payment history. Many banks provide online portals where you can monitor your loan’s progress. Staying informed helps you manage your finances effectively and detect any discrepancies early.

Early Payoff Options

Many borrowers consider paying off their car loan earlier than the scheduled term to save on interest. Most bank car loans do not have prepayment penalties, meaning you can pay extra towards your principal each month or make lump-sum payments without incurring additional fees.

Before doing so, always confirm your loan agreement’s specifics regarding early payoff. If no penalties exist, paying off your loan sooner is an excellent way to reduce the total interest paid and free up your monthly budget for other financial goals.

The Pros and Cons of Bank Car Loans

While bank car loans are a popular choice, it’s helpful to weigh their advantages and disadvantages compared to other financing options.

Advantages of Bank Car Loans:

- Competitive Interest Rates: Banks often offer some of the most competitive interest rates, especially for borrowers with strong credit, due to their large lending capacities and established financial models.

- Established Reputation and Trust: Major banks are well-known, regulated institutions, providing a sense of security and reliability in your lending relationship.

- Variety of Loan Products: Banks typically offer a range of loan terms and options, allowing you to find a structure that best fits your financial situation.

- Transparency: Reputable banks are usually very clear about their terms and conditions, making it easier to understand your loan.

- Pre-Approval Power: The ability to get pre-approved gives you strong negotiating power at the dealership.

Disadvantages of Bank Car Loans:

- Stricter Credit Requirements: Banks generally have more stringent credit score and debt-to-income ratio requirements compared to some dealership financing options, especially for subprime borrowers.

- Potentially Slower Process: While pre-approval is quick, the full underwriting process can sometimes take a bit longer than getting financing directly through a dealership, which often has instant approval mechanisms.

- Less Flexibility for Bad Credit: If your credit score is low, banks might offer less flexible terms or higher interest rates, or even deny the loan altogether.

Pro Tips for Securing the Best Bank Car Loan

Based on my years of experience, here are some actionable strategies to help you secure the most advantageous bank car loan:

- Shop Around Extensively: Don’t just apply to one bank. Contact several banks and credit unions to compare their pre-approval offers. Even a small difference in APR can save you a significant amount over the loan term. This competitive shopping is your best leverage.

- Negotiate, Don’t Just Accept: While interest rates are largely determined by your credit profile and market conditions, there might be some room for negotiation on fees or slight adjustments to the rate, especially if you have multiple offers.

- Prioritize Credit Improvement: If you’re not in a rush, dedicate a few months to improving your credit score before applying. Pay down existing debts, make all payments on time, and avoid opening new credit lines. A higher score translates directly to better rates.

- Consider a Co-Signer (If Necessary): If your credit isn’t ideal, a co-signer with excellent credit can significantly boost your chances of approval and help you secure a lower interest rate. Remember, a co-signer is equally responsible for the loan.

- Read Every Word of the Fine Print: I cannot emphasize this enough. Understand all the terms, conditions, fees, and penalties before signing. Don’t be afraid to ask for clarification on anything that’s unclear.

- Factor in Insurance Costs: Get insurance quotes for the cars you’re considering before finalizing your purchase. Insurance can be a substantial ongoing cost, and some vehicles are much more expensive to insure than others.

Driving Away with Confidence

Understanding how car loans work through a bank is an essential skill for any prospective car owner. It empowers you to navigate the complexities of financing with clarity, allowing you to make choices that align with your financial goals and lead to a more affordable and stress-free car ownership experience. From improving your credit score to meticulously reviewing loan offers, every step contributes to a successful outcome.

By taking the time to prepare, compare, and comprehend, you’re not just getting a car loan; you’re investing wisely in your future. Remember, knowledge is power, especially when it comes to your finances. Drive informed, drive confident, and enjoy the journey in your new vehicle!

For more insights into personal finance and smart borrowing, visit the Consumer Financial Protection Bureau (CFPB) at https://www.consumerfinance.gov/.