Navigating the Road to Your Dream Car: The Ultimate Guide to Car Finance & Loans

Navigating the Road to Your Dream Car: The Ultimate Guide to Car Finance & Loans Carloan.Guidemechanic.com

Buying a car is an exciting milestone for many, offering unparalleled freedom and convenience. However, the prospect of funding this significant purchase can often feel overwhelming. For most people, outright cash payment isn’t a realistic option, making car finance or a car loan an essential pathway to vehicle ownership. Understanding the intricacies of car finance is crucial for making a smart, informed decision that aligns with your financial well-being.

This comprehensive guide will demystify the world of car loans and auto finance, offering you an expert perspective on everything from different financing options to securing the best possible deal. Our goal is to equip you with the knowledge needed to navigate this journey confidently, ensuring you drive away not just with your dream car, but also with a finance package that truly works for you. Let’s hit the road to financial clarity!

Navigating the Road to Your Dream Car: The Ultimate Guide to Car Finance & Loans

What Exactly Is Car Finance? Demystifying the Process

At its core, car finance refers to the various methods available to fund the purchase of a vehicle without paying the full price upfront. Instead of handing over a lump sum, you essentially borrow money from a lender and repay it, usually with interest, over an agreed period. This allows individuals to spread the cost of a new or used car into manageable monthly installments.

The concept is straightforward: a financial institution or dealership provides the capital, and you, the borrower, commit to regular payments. These arrangements are designed to make car ownership accessible to a wider audience, transforming a large, one-off expense into a predictable monthly outgoing. Understanding the basic principle is the first step towards choosing the right vehicle finance option for your needs.

Unpacking Your Options: The Main Types of Car Finance

When exploring car financing options, you’ll encounter several popular choices, each with its own structure, benefits, and drawbacks. Based on my experience in the finance industry, selecting the right type is paramount to your long-term satisfaction and financial stability. It’s not just about the monthly payment; it’s about ownership, flexibility, and overall cost.

Let’s delve into the primary types of car loans available today:

1. Hire Purchase (HP)

Hire Purchase (HP) is a traditional and straightforward way to finance a car. With an HP agreement, you essentially "hire" the car from the finance company for a set period, making fixed monthly payments. You don’t own the car outright until you’ve made the very last payment, including a small "option to purchase" fee.

This method is ideal for those who want eventual ownership of their vehicle without any balloon payments or mileage restrictions. It’s a clear path to owning the asset, making it a popular choice for many car loan applicants. The total cost is generally clear from the outset, allowing for easy budgeting.

2. Personal Contract Purchase (PCP)

Personal Contract Purchase (PCP) has become incredibly popular in recent years, especially for new cars. It offers lower monthly payments compared to HP because you’re only financing the depreciation of the car over the term, not its full value. At the end of the agreement, you have three options:

- Return the car: Hand the car back to the dealer, assuming you’ve stayed within mileage limits and the car is in good condition.

- Pay the "balloon payment": This final, larger payment, known as the Guaranteed Minimum Future Value (GMFV), allows you to own the car outright.

- Part-exchange the car: Use any equity (if the car is worth more than the GMFV) towards a deposit on a new car and a new PCP deal.

PCP offers great flexibility and allows drivers to regularly update their vehicle. However, it’s crucial to understand the implications of mileage limits and the balloon payment, as these can significantly impact your final decision. Many people choose PCP because it allows them to drive a newer, more expensive car than they might otherwise afford on HP.

3. Personal Loan (Unsecured)

A personal loan, often obtained from a bank or building society, is an unsecured loan that provides you with a lump sum of cash. You then use this cash to buy the car outright, meaning you own the vehicle from day one. The car acts as collateral for the lender in the case of a secured loan. However, most personal loans used for car purchases are unsecured.

The key advantage here is that you own the car immediately, giving you full control over it without mileage restrictions or end-of-contract choices. You’ll make fixed monthly repayments to the bank, separate from the car dealership. This option can be very competitive, especially if you have an excellent credit score, potentially offering lower interest rates than some dealership-specific finance.

4. Leasing (Personal Contract Hire – PCH)

While not strictly a "car finance" option in the sense of eventual ownership, Personal Contract Hire (PCH), or leasing, is a common alternative for those who simply want to drive a new car without the hassle of ownership. With PCH, you essentially rent the car for a fixed period (typically 2-4 years) and then return it at the end of the term.

Monthly payments cover the depreciation of the vehicle, plus a maintenance package if chosen. You never own the car, and there’s no option to buy it at the end. This is perfect for individuals or businesses who want predictable motoring costs, regularly updated vehicles, and no concerns about depreciation or selling the car. It’s an excellent choice for those who prioritize convenience over ownership.

Where to Find Your Car Finance: Dealership, Bank, or Specialist?

Once you understand the types of finance, the next question is where to get it. You essentially have three main avenues for securing a car loan:

- Dealership Finance: This is often the most convenient option, as you can arrange finance directly at the point of sale. Dealerships work with various lenders and can sometimes offer promotional rates. Based on my experience, their convenience is a major draw, but it’s always wise to compare their offers.

- Bank Loans: Your own bank or other high-street banks can offer personal loans specifically for car purchases. As mentioned, these are typically unsecured, meaning the car isn’t used as collateral. They can be very competitive, especially if you have a strong relationship with your bank.

- Specialist Lenders/Brokers: Many finance companies specialize solely in auto finance. Brokers can compare deals from a wide range of lenders to find the best rates for your circumstances. This avenue can be particularly helpful if your credit score isn’t perfect, as specialist lenders might be more flexible.

Pro tips from us: Always get quotes from at least two of these sources before committing. This allows you to compare interest rates, terms, and overall costs to ensure you’re getting the most competitive deal.

The Car Finance Application Process: What to Expect

Applying for car finance involves a few key steps and requires some preparation. Understanding this process can significantly smooth your journey to securing an affordable car finance package.

1. The Impact of Your Credit Score

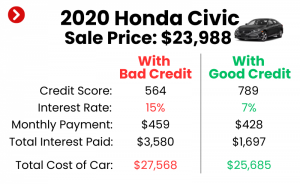

Your credit score is arguably the most critical factor lenders consider. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher credit score indicates a lower risk to lenders, often resulting in better interest rates and more favorable terms.

Before applying, it’s a wise move to check your credit report from agencies like Experian, Equifax, or TransUnion. This allows you to identify any errors and understand where you stand. A strong credit history built on timely payments and responsible borrowing will significantly improve your chances of approval for the best car loan rates.

2. Essential Documents You’ll Need

Lenders require specific documentation to verify your identity, income, and financial stability. While the exact list can vary, common documents include:

- Proof of Identity: Driving license or passport.

- Proof of Address: Utility bill or bank statement (dated within the last three months).

- Proof of Income: Recent payslips, bank statements, or tax returns (if self-employed).

- Bank Details: For setting up direct debits.

Having these documents ready before you apply can streamline the entire process, preventing unnecessary delays.

3. Pre-Approval vs. Full Application

Many lenders offer a "pre-approval" or "soft search" option. This allows you to get an indication of how much you might be able to borrow and at what interest rate, without it impacting your credit score. It’s an excellent way to shop around for finance before you even choose a car.

Once you’ve found the right car and are happy with a finance offer, you’ll proceed with a full application. This involves a "hard search" on your credit file, which will be visible to other lenders for a period. It’s important to only make full applications when you are serious about proceeding, as multiple hard searches in a short period can negatively affect your credit score.

Key Factors to Consider Before Applying for a Car Loan

Securing car finance isn’t just about getting approved; it’s about getting the right approval. Several critical factors will influence the overall cost and suitability of your auto finance agreement.

1. Budgeting and Affordability

Before you even look at cars, establish a realistic budget. This isn’t just about the monthly finance payment; it includes insurance, fuel, maintenance, road tax, and any potential repair costs. Common mistakes to avoid are getting swept away by the excitement of a new car and overlooking these ongoing expenses.

Pro tips from us: Use a budgeting app or spreadsheet to itemize your monthly income and outgoings. This will give you a clear picture of how much you can truly afford to allocate to your vehicle. Remember, a car should enhance your life, not strain your finances.

2. Interest Rates (APR)

The Annual Percentage Rate (APR) is one of the most significant factors determining the total cost of your car loan. It represents the annual cost of borrowing, including interest and any mandatory fees. A lower APR means you’ll pay less over the life of the loan.

Always compare APRs across different lenders, but be aware that the advertised rate might not be the rate you receive, as it often depends on your credit score. Based on my experience, even a small difference in APR can save you hundreds, if not thousands, of pounds over a multi-year term.

3. Loan Term

The loan term is the length of time you have to repay the finance. Longer terms typically result in lower monthly payments, making the car seem more affordable in the short term. However, a longer term also means you’ll pay more interest overall, increasing the total cost of the car finance.

Conversely, a shorter term means higher monthly payments but less interest paid and you’ll own the car sooner (for HP or personal loans). It’s a balance between affordability and total cost. Carefully consider your financial capacity for higher payments versus the desire to pay less interest.

4. Down Payment

A down payment (or deposit) is an upfront sum of money you pay towards the car’s purchase price. While not always mandatory, making a larger down payment can significantly reduce the amount you need to borrow, thus lowering your monthly payments and the total interest paid.

It also demonstrates your commitment to the lender, potentially improving your chances of approval and even securing a better interest rate. Pro tips from us: If you can afford a substantial down payment, it’s almost always a smart financial move.

5. Balloon Payment (PCP Only)

If you opt for a PCP agreement, the balloon payment (GMFV) at the end of the term is a critical consideration. This is the amount you’d need to pay to own the car outright. Ensure you understand this figure and consider whether you would realistically be able to pay it if you wanted to keep the vehicle.

Don’t let the low monthly payments of a PCP overshadow the potential final cost. It’s a significant financial commitment that needs to be planned for.

6. Mileage Limits (PCP & Leasing)

For PCP and PCH agreements, mileage limits are a fundamental part of the contract. Exceeding these agreed-upon limits can result in hefty excess mileage charges at the end of the term. Be realistic about your annual driving habits when setting these limits.

Common mistakes to avoid are underestimating your mileage to secure lower monthly payments. This can lead to unexpected costs that negate any initial savings.

7. Early Repayment Penalties

Some car loan agreements include penalties for settling the finance early. While many modern finance agreements offer flexibility, it’s essential to check the terms and conditions regarding early repayment. Understanding these clauses can save you money if your financial situation improves and you wish to clear your debt sooner.

8. Guarantors

If you have a limited or poor credit history, a lender might ask for a guarantor. A guarantor is someone (usually a family member or close friend) who agrees to take over your payments if you’re unable to meet them. This provides an additional layer of security for the lender.

While a guarantor can help you secure finance, it’s a significant responsibility for that individual. Ensure both parties fully understand the implications before proceeding.

Common Mistakes to Avoid When Applying for Car Finance

Based on my extensive experience, many individuals make preventable errors during the car finance process that can cost them money or lead to disappointment. Being aware of these pitfalls can save you a lot of hassle and expense.

- Not Checking Your Credit Score: As mentioned, your credit score is vital. Failing to check it means you go into the application blind, potentially applying for finance you won’t qualify for, or missing out on better rates.

- Only Applying to One Lender: Relying on the first offer you receive, especially from a dealership, means you might miss out on a more competitive deal elsewhere. Always shop around.

- Focusing Only on Monthly Payments: While important, solely looking at the monthly payment can be misleading. A low monthly payment might mean a longer loan term and a higher total cost. Always consider the total amount payable.

- Underestimating Running Costs: Beyond the finance, cars have ongoing costs. Neglecting to factor in insurance, fuel, maintenance, and potential repairs can lead to financial strain.

- Ignoring the Small Print: The terms and conditions of any car loan agreement are crucial. Don’t skim over details like early repayment penalties, excess mileage charges, or end-of-contract fees.

- Impulse Buying: Getting emotionally attached to a car before thoroughly researching finance options can lead to poor financial decisions. Take your time and make a rational choice.

Pro Tips for Securing the Best Car Finance Deal

To truly get the most out of your car finance journey, here are some expert tips to put you in the driver’s seat:

- Boost Your Credit Score: Before applying, take steps to improve your creditworthiness. Register on the electoral roll, pay bills on time, reduce existing debt, and avoid making multiple credit applications in a short period.

- Save for a Deposit: A larger down payment reduces the loan amount, lowers monthly payments, and often leads to better interest rates.

- Compare, Compare, Compare: Don’t settle for the first offer. Get quotes from banks, dealerships, and specialist auto finance brokers. Use soft searches to compare without impacting your credit score.

- Know Your Budget (and Stick to It): Understand your absolute maximum affordable monthly payment and total budget, including all running costs, before you start car shopping.

- Negotiate the Car Price First: When buying from a dealership, try to negotiate the car’s cash price before discussing finance. A lower purchase price means you borrow less, regardless of the finance deal.

- Be Honest in Your Application: Providing accurate information is crucial. Misrepresenting your income or financial situation can lead to rejection or even legal consequences.

- Consider a Used Car: Used cars depreciate slower than new cars and can be significantly more affordable to finance, potentially offering affordable car finance options. You can read more about the pros and cons of new vs. used car financing in our detailed article on buying a used car.

Understanding Your Rights and Responsibilities

As a borrower, you have certain rights and responsibilities under any car finance agreement. It’s essential to be aware of these to protect yourself and ensure a smooth experience.

Your rights typically include the right to receive clear information about the loan terms, the right to a cooling-off period, and in some cases, the right to voluntary termination (especially with HP and PCP agreements after a certain percentage of the loan is repaid). You can find detailed information on consumer credit rights from trusted sources like the Financial Conduct Authority (FCA) in the UK, or the Consumer Financial Protection Bureau (CFPB) in the US. For example, the Consumer Financial Protection Bureau (CFPB) offers extensive resources on auto loans, detailing borrower rights and protections: https://www.consumerfinance.gov/consumer-tools/auto-loans/.

Your responsibilities include making payments on time, maintaining the vehicle as per the agreement (especially with PCP and PCH), adhering to mileage limits, and informing the lender of any changes to your personal circumstances that might affect your ability to pay. Failing to meet these responsibilities can lead to penalties, repossession, and damage to your credit score.

Refinancing Your Car Loan: When and Why?

Sometimes, circumstances change, and your initial car loan might no longer be the best fit. Refinancing involves taking out a new loan to pay off your existing car finance agreement, potentially securing better terms.

You might consider refinancing if:

- Your credit score has improved: A better credit score can qualify you for a lower interest rate, saving you money over the remaining term.

- Interest rates have dropped: If market rates have fallen since you took out your original loan, refinancing could lead to significant savings.

- You need lower monthly payments: Extending the loan term through refinancing can reduce your monthly outgoings, though it might increase the total interest paid.

- You want to shorten your loan term: If your financial situation has improved, you might refinance to a shorter term to pay off the loan faster and reduce total interest.

- You want to remove a co-signer: If a co-signer was needed initially, you might be able to refinance the loan in your name alone once your credit is strong enough.

Before refinancing, always calculate the total savings and consider any early repayment penalties on your current loan or fees associated with the new loan. It’s a strategic move that requires careful calculation. You might also want to read our guide on managing debt effectively for more insights on optimizing your financial obligations.

Driving Forward with Confidence: Your Car Finance Journey

Navigating the world of car finance might seem complex at first glance, but with the right knowledge and a methodical approach, it becomes a straightforward path to securing your ideal vehicle. From understanding the different types of car loans like HP and PCP, to knowing the importance of your credit score and the art of comparing deals, every step is crucial.

Remember, the goal isn’t just to get a car, but to secure affordable car finance that aligns with your financial goals and capabilities. By avoiding common mistakes and applying our pro tips, you’re well on your way to making a smart, informed decision. So, take the time to research, compare, and plan, and you’ll soon be driving your dream car with complete peace of mind. Happy motoring!