Navigating the Road to Your Dream Car: The Ultimate Guide to the Car Loan Interest Rate Calculator

Navigating the Road to Your Dream Car: The Ultimate Guide to the Car Loan Interest Rate Calculator Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but the financial journey to ownership can often feel like navigating a complex maze. One of the most critical elements, and often the most misunderstood, is the car loan interest rate. Understanding this rate and how it impacts your overall cost is paramount to making a smart financial decision. This is where the Car Loan Interest Rate Calculator becomes your most powerful tool.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals dive into car purchases without fully grasping the nuances of their financing. This comprehensive guide will demystify car loan interest rates, empower you with the knowledge to use a calculator effectively, and equip you with strategies to secure the best possible deal. Our ultimate goal is to transform you from a confused buyer into a confident negotiator, ensuring your car ownership journey starts on the right financial foot.

Navigating the Road to Your Dream Car: The Ultimate Guide to the Car Loan Interest Rate Calculator

What is a Car Loan Interest Rate Calculator and Why You Need It

At its core, a Car Loan Interest Rate Calculator is a digital tool designed to estimate your potential monthly car loan payments and the total interest you’ll pay over the life of the loan. It takes into account key variables such as the loan amount, the interest rate, and the loan term (number of months). Think of it as your personal financial crystal ball for car financing.

Many people make the mistake of focusing solely on the monthly payment, without considering the total cost of borrowing. A calculator helps you look beyond that immediate figure. It reveals the true financial burden, allowing you to compare different loan scenarios side-by-side before you even step foot in a dealership.

Beyond Simple Math: The Power of Foresight

Based on my experience, the real power of this calculator lies in its ability to provide foresight. It’s not just about crunching numbers; it’s about understanding the financial implications of every decision. Will a longer loan term reduce your monthly payment but increase your total interest paid? Will a larger down payment significantly lower your overall cost?

These are the critical questions a car loan interest rate calculator helps you answer. It empowers you to experiment with different figures, giving you a clear picture of how each variable influences your financial outlay. This proactive approach saves you money and prevents future financial stress.

Key Variables That Influence Your Car Loan Interest Rate

Your interest rate isn’t a random number; it’s a carefully calculated figure based on several crucial factors. Understanding these variables is the first step toward securing a favorable rate. Let’s dive into what lenders scrutinize.

Credit Score: Your Financial Report Card

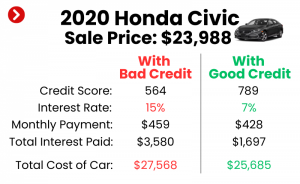

Your credit score is arguably the most significant factor determining the interest rate you’ll be offered. It’s a three-digit number that summarizes your financial history, indicating your reliability as a borrower. Lenders use it to assess the risk of lending money to you.

A higher credit score (generally above 700-750) signals to lenders that you have a strong history of managing debt responsibly. This translates into lower perceived risk for them, and consequently, they are willing to offer you more competitive, lower interest rates. Conversely, a lower score suggests a higher risk, leading to higher interest rates to compensate the lender for that increased risk.

Loan Term: The Time-Value Trade-off

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer loan term might make your monthly payments seem more affordable, it comes with a significant trade-off.

Longer terms often result in paying more total interest over the life of the loan, even if the interest rate itself is slightly lower. This is because the money is borrowed for a longer period, giving interest more time to accrue. Shorter terms, while having higher monthly payments, usually lead to less total interest paid and faster car ownership.

Down Payment: Reducing Risk, Reducing Cost

A down payment is the initial sum of money you pay upfront towards the purchase price of the car. It reduces the amount you need to borrow, which directly impacts your loan. Lenders view a substantial down payment favorably.

A larger down payment signals to the lender that you are committed to the purchase and have a lower likelihood of defaulting. This reduced risk often encourages them to offer a lower interest rate on the remaining loan balance. Furthermore, borrowing less money inherently means less interest will accrue over time.

Vehicle Age & Type: Asset vs. Liability

The type and age of the vehicle you’re financing also play a role. New cars, being a more secure asset with predictable depreciation, often qualify for lower interest rates compared to used cars. Used cars, especially older models, carry a higher risk for lenders due to potential mechanical issues and faster depreciation.

Specialty or luxury vehicles might also have different lending terms. Lenders consider the resale value and overall risk associated with the specific vehicle as collateral. Generally, a car that holds its value better and is less prone to costly repairs might secure a slightly better rate.

Market Conditions & Lender Type: External Influences

Beyond your personal financial situation and the car itself, broader economic factors and the specific lender can influence your rate. General interest rate trends set by central banks impact the cost of borrowing across the board. When these rates rise, car loan rates tend to follow suit.

Different lenders – banks, credit unions, and dealership financing – also have varying lending criteria and overheads, leading to different rate offerings. Credit unions, for example, are often known for offering more competitive rates due to their member-focused structure. Shopping around is key here.

How to Effectively Use a Car Loan Interest Rate Calculator

Now that you understand the variables, let’s put that knowledge into action. Using a Car Loan Interest Rate Calculator is straightforward, but interpreting the results effectively is where the real value lies.

Step-by-Step Guide: Inputting Your Data

Most online calculators are intuitive, but here’s a general process:

- Enter the Loan Amount: This is the total price of the car minus any down payment or trade-in value. Be sure to include sales tax and any applicable fees in your total loan amount.

- Input the Interest Rate (APR): This is crucial. If you don’t have a pre-approved rate, you might need to use an estimated rate based on your credit score and current market averages. Aim for a realistic figure.

- Specify the Loan Term: Choose the number of months you plan to take to repay the loan. Common options are 36, 48, 60, or 72 months.

- Click "Calculate": The calculator will instantly display your estimated monthly payment and often the total interest paid over the loan term.

Pro tip from us: Always use the Annual Percentage Rate (APR) when inputting the interest rate. APR includes not just the interest but also certain fees, giving you a more accurate picture of the true cost of borrowing.

Interpreting the Results: What Do the Numbers Mean?

Once you hit calculate, you’ll typically see two main figures:

- Estimated Monthly Payment: This is the amount you’ll need to pay each month to cover your loan. It’s essential to ensure this figure fits comfortably within your monthly budget without straining your finances.

- Total Interest Paid: This figure shows the cumulative amount of interest you’ll pay over the entire loan term. This is where the long-term cost becomes evident. A seemingly small difference in the interest rate can lead to thousands of dollars in extra interest over several years.

It’s easy to get fixated on the monthly payment. However, based on my experience, focusing on the total interest paid reveals the true efficiency of your loan. A lower total interest paid means you’re getting a better deal in the long run.

Scenario Planning: Comparing Different Options

The true power of the calculator shines when you use it for "what-if" scenarios.

- Vary the Down Payment: See how increasing your down payment impacts both your monthly payment and total interest.

- Adjust the Loan Term: Compare a 60-month loan versus a 72-month loan. Notice how the monthly payment changes, but more importantly, how the total interest paid can skyrocket with a longer term.

- Hypothetical Interest Rates: If you’re pre-approved for multiple rates, or want to see the benefit of improving your credit, plug in different interest rates to understand their impact.

This scenario planning helps you identify the sweet spot where your monthly payments are manageable, and your total interest paid is as low as possible. It’s an invaluable step before engaging with any lender.

Beyond the Calculator: Essential Tips for Securing the Best Rate

While the Car Loan Interest Rate Calculator is a fantastic tool, it’s just one piece of the puzzle. Here are additional strategies to help you secure the most favorable car loan terms.

Pre-Approval Power: Shop Smart

One of the most effective strategies is to get pre-approved for a car loan before you visit a dealership. This means applying for a loan with a bank, credit union, or online lender beforehand. Pre-approval gives you a firm offer for a loan amount and interest rate.

Armed with a pre-approval, you walk into the dealership as a cash buyer, knowing exactly how much you can spend and what your interest rate will be. This takes the pressure off discussing financing at the dealership and allows you to focus solely on negotiating the car’s price. It also provides a benchmark against which you can compare any financing offers from the dealer.

Negotiation Know-How: Don’t Settle

Once you have your pre-approval and have used the calculator to understand ideal scenarios, you’re in a strong position to negotiate. Don’t be afraid to haggle for a better interest rate, especially if the dealership offers financing. They might be able to beat your pre-approved rate to secure your business.

Remember, every percentage point matters. A small reduction in your interest rate can save you hundreds, even thousands, of dollars over the life of the loan. Always ask if there’s any flexibility in the rate they’re offering.

Read the Fine Print: Hidden Fees and Terms

Common mistakes to avoid are signing without fully understanding the loan agreement. Always meticulously read the fine print of any loan offer. Look out for hidden fees, such as origination fees, documentation fees, or prepayment penalties. These extra charges can significantly increase the actual cost of your loan, even if the stated interest rate seems low.

Ensure you understand all the terms, including late payment penalties, grace periods, and any clauses related to defaulting on the loan. Clarity upfront prevents costly surprises later on.

Improving Your Credit: A Long-Term Strategy

If your credit score isn’t where you’d like it to be, investing time in improving it can yield substantial savings on your car loan and future borrowing. This is a long-term strategy, but a powerful one. Steps include:

- Paying all your bills on time, every time.

- Reducing existing debt, especially credit card balances.

- Checking your credit report for errors and disputing any inaccuracies.

- Avoiding opening too many new credit accounts simultaneously.

Even a modest improvement in your credit score can move you into a better interest rate tier, translating to significant savings over the loan term. For more detailed information on credit scores, you might find valuable resources at the Consumer Financial Protection Bureau (CFPB) website .

Common Mistakes to Avoid When Using a Car Loan Calculator

Even with the best intentions, it’s easy to make mistakes that can skew your results or lead to poor financial decisions. Based on my experience, here are some common pitfalls to sidestep.

Ignoring APR vs. Interest Rate

This is a critical distinction. The interest rate is simply the cost of borrowing the principal amount. The Annual Percentage Rate (APR), however, includes the interest rate plus certain fees associated with the loan, such as origination fees. It represents the true annual cost of your loan.

Many calculators ask for an "interest rate," but when you’re comparing actual loan offers, always use the APR for an apples-to-apples comparison. Failing to do so can make one loan appear cheaper than it actually is.

Forgetting Additional Costs

When calculating your loan amount, it’s easy to focus solely on the car’s sticker price. However, remember to factor in sales tax, registration fees, documentation fees, and potentially extended warranties or other add-ons that might be rolled into your financing.

These additional costs can significantly increase your total loan amount, which in turn means higher monthly payments and more interest paid. Always include these figures in your calculator inputs for the most accurate estimation.

Not Shopping Around

Relying on the first loan offer you receive, especially from a dealership, is a common and costly mistake. Dealerships often mark up interest rates to increase their profit. By not shopping around and comparing offers from multiple lenders (banks, credit unions, online lenders), you could be leaving money on the table.

Use the car loan interest rate calculator with different estimated rates from various lenders to see how much you could save by finding the most competitive offer. This small effort can lead to substantial long-term savings.

Overlooking Prepayment Penalties

While not as common as they once were, some loan agreements include prepayment penalties. These are fees charged if you pay off your loan early. If you anticipate being able to pay off your car loan ahead of schedule to save on interest, ensure your loan agreement does not include such a penalty.

Always check this clause in the fine print. A prepayment penalty can negate the financial benefit of paying off your loan early, making it a crucial detail to verify.

The Long-Term Impact: Why a Small Rate Difference Matters

It’s easy to dismiss a difference of half a percentage point in an interest rate. After all, what’s 0.5%? However, when applied to a large sum like a car loan over several years, that small difference can translate into a significant amount of money.

Total Cost of Ownership: Beyond the Monthly Payment

Let’s consider an example: A $30,000 car loan over 60 months.

- At 5.0% APR: Monthly payment ~$566, Total interest ~$3,960.

- At 5.5% APR: Monthly payment ~$572, Total interest ~$4,320.

That seemingly small 0.5% difference results in an extra $360 in interest paid over the life of the loan. Now imagine a larger loan amount or a longer term, and the difference becomes even more substantial. This highlights why the Car Loan Interest Rate Calculator is so vital for understanding the true total cost of ownership, not just the monthly outlay.

Financial Flexibility: Your Future Self Will Thank You

Every dollar saved on interest is a dollar you can put towards other financial goals – building an emergency fund, saving for a down payment on a house, investing, or simply enjoying life. A lower interest rate means more of your monthly payment goes towards the principal balance, accelerating your path to ownership and freeing up cash flow sooner.

Empowering yourself with the knowledge from a calculator and securing a better rate provides greater financial flexibility. It allows you to achieve your financial objectives faster and reduces the overall burden of debt.

Pro Tips from an Expert: Mastering Your Car Loan Journey

As someone who has navigated the intricacies of consumer finance for years, I can offer a few advanced tips to help you truly master your car loan journey.

Leverage Technology

Beyond basic calculators, explore advanced online tools that allow for amortization schedules. These schedules break down each payment, showing how much goes towards interest and how much towards the principal. This visual representation can be incredibly motivating and help you understand how extra payments can drastically reduce your total interest.

Consider using budgeting apps that integrate with your bank accounts to monitor your loan payments and overall financial health. For other financial planning advice, you might find valuable insights in our article on .

Consider Refinancing

If you’ve already purchased a car and your credit score has improved significantly since then, or if market rates have dropped, consider refinancing your car loan. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

Use the Car Loan Interest Rate Calculator to compare your current loan terms against potential new ones. A lower interest rate from refinancing can significantly reduce your monthly payments or the total interest paid, putting more money back in your pocket.

Build an Emergency Fund

While not directly related to the calculator, having a robust emergency fund is crucial when taking on any debt, including a car loan. Life is unpredictable, and unexpected expenses can arise. An emergency fund acts as a financial buffer, preventing you from missing loan payments if you face a sudden job loss, medical emergency, or major home repair.

Missing payments can damage your credit score and incur late fees, making your car loan more expensive in the long run. A strong financial safety net ensures you can weather any storm without jeopardizing your car ownership.

Empowering Your Car Purchase

The journey to buying a car doesn’t have to be fraught with financial anxiety. By understanding the critical role of the Car Loan Interest Rate Calculator and leveraging the insights it provides, you gain immense power. This tool, combined with a proactive approach to understanding interest rate variables, pre-approval, and careful negotiation, transforms a potentially stressful process into an empowering one.

Remember, a car loan is a significant financial commitment. Arm yourself with knowledge, use the calculator as your guide, and don’t be afraid to ask questions and negotiate. Your future self, and your wallet, will thank you for making an informed and intelligent decision. Drive confidently, knowing you’ve secured the best possible deal.