Navigating the Road to Your Dream Car: Ultimate Car Loan Help Through Credit Score Mastery

Navigating the Road to Your Dream Car: Ultimate Car Loan Help Through Credit Score Mastery Carloan.Guidemechanic.com

Securing a car loan can feel like navigating a complex maze, especially when the crucial role of your credit score comes into play. For many, the journey to purchasing a new vehicle is not just about finding the right make and model, but also about understanding how their financial history impacts their ability to get approved and, more importantly, the terms of that approval. This comprehensive guide offers essential car loan help credit score insights, empowering you to approach the financing process with confidence and secure the best possible deal.

Your credit score isn’t just a number; it’s a powerful financial narrative that lenders read to assess your trustworthiness. A strong score can unlock lower interest rates, more flexible terms, and a smoother approval process, potentially saving you thousands of dollars over the life of your loan. Conversely, a less-than-stellar score can lead to higher costs, stricter conditions, or even outright rejection. This article will demystify the credit score, reveal how it influences your car loan, and provide actionable strategies to improve it, ensuring you’re well-equipped for your next vehicle purchase.

Navigating the Road to Your Dream Car: Ultimate Car Loan Help Through Credit Score Mastery

Understanding Your Credit Score: The Foundation of Car Loan Help

Before you even start browsing for vehicles, it’s paramount to grasp what your credit score represents and why it holds so much sway in the world of auto financing. Simply put, a credit score is a three-digit number that reflects your creditworthiness based on your financial history. It’s a snapshot of how reliably you’ve managed debt in the past, and lenders use it to predict your likelihood of repaying a new loan.

Based on my experience working with countless individuals on their financing journeys, the credit score is often the single most significant factor in determining not just whether you get approved, but how much you pay. A higher score signals less risk to lenders, making them more willing to offer favorable terms. This translates directly into lower interest rates, which means smaller monthly payments and less money paid overall.

There are two primary credit scoring models: FICO and VantageScore. While both assess similar data points, they can produce slightly different scores. Most auto lenders primarily rely on FICO scores, which typically range from 300 to 850. Understanding where you stand within this range is the first critical step in getting effective car loan help credit score advice.

- Excellent Credit (780-850): This range often qualifies you for the absolute best interest rates and loan terms available. Lenders see you as a very low-risk borrower.

- Good Credit (670-779): Borrowers in this category generally receive competitive rates and have a high likelihood of approval. You’re considered a reliable borrower.

- Fair/Average Credit (580-669): This range can present more challenges. You might still get approved, but likely with higher interest rates and less flexible terms.

- Poor Credit (300-579): Securing a traditional car loan can be difficult with a score in this range. If approved, you can expect significantly higher interest rates and potentially a requirement for a larger down payment.

Knowing your score isn’t about judgment; it’s about preparation. It allows you to set realistic expectations, identify areas for improvement, and strategize your approach to car financing effectively.

Decoding the Factors That Influence Your Credit Score

Your credit score isn’t an arbitrary number; it’s a sophisticated calculation based on specific elements of your financial behavior. Understanding these components is crucial for anyone seeking comprehensive car loan help credit score strategies, as it reveals precisely where to focus your efforts for improvement. The two major scoring models, FICO and VantageScore, weigh these factors slightly differently, but the underlying principles remain consistent.

Here are the key factors that shape your credit score, explained in detail:

1. Payment History (Approximately 35% of FICO Score)

This is by far the most significant factor. Your payment history details whether you’ve made your credit payments on time. Every late payment, missed payment, or default is recorded and can severely damage your score. Lenders view a consistent history of on-time payments as the strongest indicator of future financial responsibility.

A single 30-day late payment can cause a significant drop in your score, and its impact can linger for years. Conversely, a long history of paying all your bills on time demonstrates reliability and will bolster your score significantly. It’s the cornerstone of a healthy credit profile.

2. Amounts Owed / Credit Utilization (Approximately 30% of FICO Score)

This factor examines how much of your available credit you are currently using. It’s often referred to as your credit utilization ratio. For example, if you have a credit card with a $10,000 limit and a $3,000 balance, your utilization is 30%. A lower utilization ratio is generally better for your credit score.

Experts recommend keeping your overall credit utilization below 30% across all your credit accounts. High utilization can signal to lenders that you are over-reliant on credit or potentially in financial distress, even if you make your payments on time. Reducing your balances can quickly provide a boost to your score.

3. Length of Credit History (Approximately 15% of FICO Score)

This factor considers how long your credit accounts have been open, including the age of your oldest account, the age of your newest account, and the average age of all your accounts. A longer credit history, especially one with a good payment record, indicates more experience managing credit. Lenders prefer to see a seasoned credit profile rather than a very new one.

Individuals with limited credit history, such as young adults, may find it harder to secure favorable loan terms simply because there isn’t enough data to assess their risk. Patience and responsible credit use over time are key here.

4. New Credit (Approximately 10% of FICO Score)

This factor looks at how many new credit accounts you’ve recently opened and how many hard inquiries have been made on your credit report. Each time you apply for new credit (a credit card, a loan, a mortgage), a "hard inquiry" is typically placed on your report. Too many hard inquiries in a short period can suggest you are a higher risk, potentially desperate for credit, and can slightly lower your score.

However, it’s important to note that rate shopping for a car loan (or mortgage) within a concentrated period (usually 14-45 days, depending on the scoring model) will typically be treated as a single inquiry, minimizing the impact. This allows you to compare offers without undue penalty.

5. Credit Mix (Approximately 10% of FICO Score)

This factor assesses the different types of credit you have, such as revolving credit (credit cards) and installment credit (car loans, mortgages, student loans). A healthy mix demonstrates your ability to manage various forms of debt responsibly. It shows versatility in your financial management skills.

While not as heavily weighted as payment history or amounts owed, a diverse credit portfolio can positively contribute to your overall score. It’s not about having more credit, but rather different types of credit managed well.

Pro tips from us: Regularly checking your credit report from all three major bureaus (Experian, Equifax, and TransUnion) is absolutely essential. You’re entitled to a free report from each once a year via AnnualCreditReport.com. Reviewing these reports allows you to spot errors, identity theft, or outdated information that could be unfairly dragging down your score. Disputing inaccuracies can be a quick way to improve your credit profile.

Strategies for Boosting Your Credit Score Before Applying for a Car Loan

Improving your credit score is one of the most effective forms of car loan help credit score strategy you can undertake. While it takes time and consistent effort, the financial rewards of a higher score—lower interest rates and better terms—are well worth the investment. Here are actionable steps you can take to elevate your credit profile before walking into a dealership.

1. Pay All Bills On Time, Every Time

This cannot be stressed enough. As discussed, payment history is the most critical component of your credit score. Make sure all your financial obligations—credit cards, student loans, mortgage, utility bills, and even rent if reported—are paid by their due dates. Set up automatic payments or calendar reminders to avoid missing deadlines. Even a single 30-day late payment can cause a significant score drop. Consistency here is key to building a robust credit foundation.

2. Reduce Your Credit Card Balances

Your credit utilization ratio (the amount of credit you’re using versus your total available credit) significantly impacts your score. Aim to keep your balances below 30% of your credit limit on each card, and ideally even lower, closer to 10-20%. Paying down high balances demonstrates responsible credit management and can provide a relatively quick boost to your score. Consider focusing on the card with the highest utilization first.

3. Avoid Opening New Credit Accounts

In the months leading up to a car loan application, resist the temptation to open new credit cards or take out other loans. Each new application results in a "hard inquiry" on your credit report, which can temporarily lower your score. Furthermore, opening new accounts reduces the average age of your credit history, another factor that negatively impacts your score. Maintain stability in your credit profile during this crucial period.

4. Review Your Credit Report for Errors

Common mistakes to avoid are neglecting to regularly check your credit reports. Errors can occur, such as incorrect late payments, accounts that aren’t yours, or inaccurate balances. These errors can unfairly depress your score. Obtain your free annual credit reports from AnnualCreditReport.com and meticulously review them. If you find any inaccuracies, dispute them immediately with the credit bureau. Correcting errors can sometimes lead to a quick and significant score improvement.

5. Become an Authorized User (with caution)

If you have limited credit history, becoming an authorized user on a trusted family member’s credit card can help. The primary cardholder’s positive payment history and low utilization will often be reflected on your credit report, helping to build your own. However, this strategy requires trust and careful consideration. Ensure the primary user has excellent credit habits, as their missteps could also negatively affect your report.

6. Consider a Secured Credit Card or Credit-Builder Loan

For individuals with poor or very limited credit, these tools can be invaluable. A secured credit card requires a cash deposit that acts as your credit limit. By using it responsibly and making on-time payments, you demonstrate creditworthiness. A credit-builder loan is designed specifically to help you establish or improve credit. You make payments into a savings account, and once the loan is paid off, you receive the funds, having built a positive payment history.

Pro tips from us: Patience is a virtue when improving your credit score. While some actions, like paying down balances, can have a relatively quick impact, building a strong, long-term credit history takes time. Start these strategies well in advance of your car loan application, ideally 6-12 months before you plan to buy. For more detailed steps on repairing and building your credit, you might find our article on "Essential Credit Repair Tips for a Stronger Financial Future" particularly helpful. (This is an example of an internal link).

Navigating Car Loans with Different Credit Score Ranges

Your credit score acts as a financial compass, guiding you through the landscape of car loan options. Depending on where your score falls, your journey will look quite different. Understanding these variations is vital for anyone seeking effective car loan help credit score advice.

1. Excellent/Good Credit (670-850)

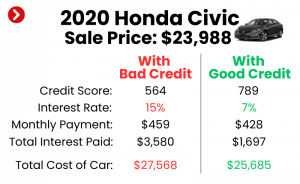

Congratulations! If your credit score falls into this range, you’re in an enviable position. Lenders view you as a highly reliable borrower, which means you’ll typically qualify for the lowest available interest rates, often advertised as "prime" rates. You’ll also likely have more flexibility in loan terms, such as longer repayment periods or lower down payment requirements.

-

Benefits:

- Lowest Interest Rates: Significantly reduced borrowing costs over the life of the loan.

- Easier Approval: Quick and straightforward loan approval process.

- Negotiating Power: You’re a desirable customer, giving you leverage to negotiate not just the car price but also loan terms.

- Flexible Terms: Access to a wider range of loan products and conditions.

-

Strategy: Don’t just take the first offer. Shop around aggressively among banks, credit unions, and even dealership financing departments. Get pre-approved by a few lenders to compare rates and use those offers as leverage.

2. Fair/Average Credit (580-669)

This is a common credit range, and while it’s not ideal, it doesn’t mean you’re out of luck. Borrowers in this category will likely face slightly higher interest rates compared to those with excellent credit, reflecting a slightly elevated risk perception by lenders. However, many options are still available.

-

Challenges:

- Higher Interest Rates: Expect to pay more in interest over the loan term.

- Potentially Stricter Terms: Lenders might require a larger down payment or a shorter loan term to mitigate their risk.

-

Strategy:

- Increase Your Down Payment: A larger down payment reduces the loan amount and shows the lender you have skin in the game, making you a less risky borrower.

- Consider a Co-signer: If you have a trusted friend or family member with excellent credit, their co-signature can help you qualify for better rates. Be aware that the co-signer is equally responsible for the debt.

- Clean Up Your Credit: Focus on the credit-boosting strategies mentioned earlier, even if you can only make minor improvements before applying.

- Shop Around: Compare offers from multiple lenders, including credit unions, which often have more flexible lending criteria.

3. Bad/Poor Credit (300-579)

Securing a car loan with a low credit score can be challenging, but it’s often not impossible. Lenders view borrowers in this range as high-risk, leading to significantly higher interest rates to compensate for that perceived risk. This means your monthly payments and the total cost of the car will be substantially higher.

-

Options Available (but with caution):

- Subprime Lenders: These lenders specialize in working with high-risk borrowers. While they offer loans, their interest rates are typically very high.

- "Buy Here, Pay Here" Dealerships: These dealerships offer in-house financing, often without a credit check. However, they are known for extremely high interest rates and unfavorable terms. Pro tips from us: Approach these with extreme caution; they should be a last resort.

- Secured Loans: Some lenders might offer a secured car loan where the car itself acts as collateral, but again, rates can be high.

-

Strategy for Improvement:

- Focus on Rebuilding Credit First: If possible, dedicate time to improving your credit score before buying a car. Even a small bump can make a big difference in interest rates.

- Substantial Down Payment: A large down payment is critical. It reduces the amount you need to borrow and demonstrates your commitment, making you a more attractive borrower.

- Budget for Higher Costs: Be realistic about the higher interest rates and total cost of the loan.

- Consider a Less Expensive Vehicle: Start with a more affordable car to keep the loan amount manageable.

- Co-signer: This can be particularly beneficial for bad credit borrowers, but again, ensure the co-signer understands their full responsibility.

Pro tips from us: Regardless of your credit score, getting pre-approved for a car loan is a smart move. Pre-approval gives you a clear understanding of the interest rate and loan amount you qualify for before you step onto a dealership lot. This separates the financing negotiation from the car price negotiation, giving you more leverage and preventing you from being swayed by dealer-provided financing that might not be in your best interest. For more information on understanding your credit and its impact, consider visiting the Consumer Financial Protection Bureau (CFPB) website for valuable resources. (This is an example of an external link).

The Car Loan Application Process and Your Credit Score

Understanding the nuances of the car loan application process, particularly how it interacts with your credit score, is crucial for a smooth and successful purchase. This knowledge provides practical car loan help credit score insights, enabling you to navigate the experience confidently.

1. Gathering Your Documents

Before applying, ensure you have all necessary documents ready. This typically includes:

- Proof of identity (driver’s license, passport).

- Proof of income (pay stubs, tax returns, bank statements).

- Proof of residence (utility bill, lease agreement).

- Social Security Number (for credit check).

- Information about the vehicle you wish to purchase (if you’ve chosen one).

Having these prepared streamlines the process and shows lenders you are organized and serious.

2. Understanding Different Loan Types

You have several avenues for car financing, each with its own characteristics:

- Bank Financing: Traditional banks offer competitive rates, especially for borrowers with good to excellent credit. They often have transparent processes.

- Credit Unions: Known for member-friendly rates and terms, credit unions can be an excellent option, particularly for those with fair or average credit. They may be more flexible than large banks.

- Dealership Financing: Dealers act as intermediaries, working with a network of lenders. While convenient, their rates might not always be the best. They often mark up interest rates to profit from the loan.

- Online Lenders: A growing number of online platforms offer quick applications and competitive rates. They are worth exploring for pre-approval.

Your credit score will heavily influence the offers you receive from each of these sources.

3. The Impact of Multiple Inquiries (Rate Shopping)

A common concern is that applying for multiple loans will hurt your credit score. While each application results in a "hard inquiry" (a temporary small dip), credit scoring models are smart. They recognize that when you’re shopping for a car loan, you’re likely comparing rates from several lenders.

From my professional experience, if you submit multiple car loan applications within a concentrated period (typically 14 to 45 days, depending on the scoring model), they are generally grouped together and treated as a single inquiry for scoring purposes. This means you can confidently shop around for the best rates without fear of significant credit score damage. The key is to do all your rate shopping within that short window.

4. Negotiating the Best Terms

Once you have a few pre-approval offers in hand, you gain significant negotiating power.

- Compare Rates: Use the lowest pre-approved rate you’ve received to negotiate with the dealership’s finance department. They may be able to beat or match it.

- Focus on the Total Cost: Don’t just look at the monthly payment. Understand the total interest you’ll pay over the life of the loan.

- Beware of Add-ons: Dealers might try to sell you extended warranties, GAP insurance, or other add-ons. Research these thoroughly and only purchase what you genuinely need. Some can be rolled into the loan, increasing your overall interest burden.

A solid credit score, combined with diligent preparation and negotiation, is your strongest tool in securing favorable car loan terms.

Post-Approval: Maintaining and Improving Your Credit

Getting approved for a car loan is a significant achievement, but the journey doesn’t end there. Your new auto loan presents a prime opportunity to further strengthen your credit score, which is a powerful piece of ongoing car loan help credit score advice. Responsible management of your car loan can pave the way for even better financial opportunities in the future.

1. Making Timely Payments on Your New Car Loan

This is the most straightforward and effective way to continue building positive credit history. Your car loan is an installment loan, and consistent, on-time payments will be reported to the credit bureaus. Each payment you make on time reinforces your creditworthiness, steadily boosting your score over the loan term.

Set up automatic payments if possible, or create reminders to ensure you never miss a due date. Even a single late payment can counteract months of good behavior, so vigilance is key. This consistent positive action will demonstrate your reliability to all future lenders.

2. Refinancing Opportunities

As you make on-time payments and your credit score improves over time, you might become eligible for better interest rates than you initially received. This is where refinancing comes in. Refinancing means taking out a new loan to pay off your existing car loan, ideally with a lower interest rate or more favorable terms.

Pro tips from us: If your credit score has significantly improved since you first bought your car, or if interest rates have dropped, research refinancing options. Even a percentage point or two lower interest rate can save you hundreds, or even thousands, of dollars over the remaining life of the loan. Our article on "When and How to Refinance Your Car Loan for Maximum Savings" provides an in-depth look at this valuable strategy. (This is an example of an internal link).

3. Monitoring Your Credit

Even after securing your car loan, regularly monitor your credit report and score. This ongoing vigilance helps you:

- Track Progress: See how your on-time car loan payments are positively impacting your score.

- Spot Errors: Identify and dispute any new inaccuracies that may appear.

- Prevent Fraud: Detect suspicious activity or accounts opened in your name without your knowledge.

Many credit card companies and financial institutions now offer free credit score tracking, making it easier than ever to keep an eye on your financial health.

By actively managing your new car loan responsibly and continuing to practice good credit habits, you’re not just paying for your vehicle; you’re actively investing in a stronger financial future.

Conclusion: Your Roadmap to Car Loan Success with a Strong Credit Score

Navigating the world of car loans can seem daunting, but armed with a thorough understanding of your credit score and how it functions, you transform from a passive applicant into an empowered consumer. This comprehensive guide has provided essential car loan help credit score strategies, demonstrating that your credit score is not merely a barrier but a powerful tool that, when understood and managed correctly, can unlock significant financial advantages.

From dissecting the components of your FICO or VantageScore to implementing proactive strategies for improvement, every piece of advice in this article aims to put you in the driver’s seat of your financial future. Whether you’re aiming for the lowest possible interest rate with excellent credit, or diligently working to rebuild a tarnished score, consistent effort and informed decisions are your most valuable assets. Remember to pay your bills on time, keep your credit utilization low, and regularly review your credit reports for accuracy.

The ultimate goal is not just to get approved for a car loan, but to secure one with terms that genuinely benefit you and align with your financial well-being. By mastering the intricate relationship between your credit score and car financing, you ensure that your journey to owning your dream car is as smooth and affordable as possible. Start today, and drive towards a smarter financial future.