Navigating the Road to Your Dream Ride: A Comprehensive Guide to Car Loans in Oregon

Navigating the Road to Your Dream Ride: A Comprehensive Guide to Car Loans in Oregon Carloan.Guidemechanic.com

For many Oregonians, a reliable vehicle isn’t just a convenience—it’s a necessity. From commuting through Portland’s bustling streets to exploring the breathtaking coast or the vast high desert, personal transportation offers unparalleled freedom and practicality. But acquiring that perfect car often involves securing a car loan, a financial journey that can seem daunting without the right guidance.

As an expert blogger and SEO content writer with years of experience in the automotive finance industry, I understand the nuances of vehicle financing. My mission today is to demystify the process of Car Loans Oregon, providing you with a super comprehensive, in-depth guide that will empower you to make informed decisions and drive away with confidence. This isn’t just about getting a loan; it’s about securing the right loan for your unique circumstances in the Beaver State.

Navigating the Road to Your Dream Ride: A Comprehensive Guide to Car Loans in Oregon

Understanding the Basics of Car Loans in Oregon

Before we dive into the specifics, let’s establish a foundational understanding of what a car loan entails. Simply put, a car loan is a sum of money borrowed from a financial institution to purchase a vehicle, which you then repay over a set period, typically with interest. In Oregon, like elsewhere, this process is governed by various factors that influence the terms you receive.

What Exactly is a Car Loan?

At its core, a car loan is a secured loan. This means the vehicle you purchase acts as collateral. Should you fail to make your payments, the lender has the right to repossess the car to recover their losses. This collateral aspect is why car loans often come with more favorable interest rates compared to unsecured personal loans.

Understanding this fundamental principle is crucial. It highlights the importance of making timely payments, not only to maintain possession of your vehicle but also to build a positive credit history.

Key Terms You Need to Know

When discussing Oregon auto loans, you’ll encounter several important terms that directly impact your financial commitment. Grasping these concepts will make the application process much clearer.

- Principal: This is the original amount of money you borrow to purchase the car. It’s the sticker price of the vehicle minus any down payment or trade-in value.

- Interest Rate (APR): The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a percentage of the principal. It includes the interest rate plus any additional fees charged by the lender. A lower APR means lower total costs over the life of the loan.

- Loan Term: This refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). A longer term usually means lower monthly payments but can result in paying more interest overall.

- Down Payment: This is the initial sum of money you pay upfront towards the purchase of the car. A larger down payment reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest accrued.

New vs. Used Car Loans Oregon

The type of vehicle you choose—new or used—will significantly impact your loan options and terms. While the fundamental process remains similar, there are key differences in new car loans Oregon and used car loans Oregon.

New cars typically qualify for lower interest rates and longer loan terms due to their higher value and perceived reliability. Lenders often see less risk in financing a brand-new vehicle. However, new cars depreciate rapidly, meaning their value decreases significantly the moment they leave the lot.

Used cars, on the other hand, might come with slightly higher interest rates or shorter loan terms, depending on the vehicle’s age and mileage. Yet, they offer the advantage of having already undergone significant depreciation, often making them a more budget-friendly option upfront. The key is to find a balance that suits your financial situation and vehicle needs.

The Car Loan Application Process in Oregon: Your Step-by-Step Guide

Securing an auto loan doesn’t have to be a confusing ordeal. Based on my experience, a structured approach can make the process smooth and stress-free. Here’s a breakdown of the typical application journey for Oregon vehicle financing.

Step 1: Assess Your Financial Health

Before you even start looking at cars, take an honest look at your finances. This involves reviewing your credit score, understanding your monthly budget, and determining how much you can realistically afford for a car payment. This preliminary step is often overlooked but is absolutely critical.

Knowing your financial standing upfront will help you set realistic expectations and avoid applying for loans that are beyond your reach.

Step 2: Get Your Credit Score in Order

Your credit score is arguably the most influential factor in determining your car loan rates Oregon. Lenders use this three-digit number to assess your creditworthiness and the risk associated with lending you money.

Scores generally range from 300 to 850, with higher scores indicating a lower risk. Take time to check your credit report for any inaccuracies and understand what factors are influencing your score. Even a small improvement can translate into substantial savings over the life of your loan.

Step 3: Gather Required Documents

Lenders will require specific documentation to verify your identity, income, and residency. Being prepared with these documents can significantly speed up the approval process.

Commonly requested items include:

- Government-issued photo identification (e.g., Oregon driver’s license)

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of residency (utility bill, lease agreement)

- Social Security Number

- Information about the vehicle you intend to purchase (if you’ve already chosen one)

Step 4: Explore Your Lender Options

One of the most important pro tips from us is to shop around for the best Oregon auto loan rates. Don’t just settle for the first offer you receive, especially if it’s from a dealership. Several types of lenders offer car loans:

- Banks: Traditional banks often provide competitive rates, especially if you’re an existing customer.

- Credit Unions: These member-owned institutions are known for offering some of the lowest interest rates and personalized service. If you qualify for membership, definitely explore this avenue for best car loans Oregon.

- Dealerships: While convenient, dealership financing (often through their network of lenders) may not always offer the most competitive rates. However, they can sometimes work wonders for specific situations, like those needing bad credit car loans Oregon.

- Online Lenders: A growing number of online platforms specialize in car loans, offering quick applications and competitive rates.

Step 5: Get Pre-Approved

Securing pre-approval before stepping onto the car lot is a game-changer. Pre-approval means a lender has conditionally agreed to lend you a certain amount of money at a specific interest rate, based on a preliminary review of your credit and finances.

Based on my experience, having a pre-approval letter in hand gives you significant negotiating power. It shows the dealership you’re a serious buyer with financing already secured, allowing you to focus on the car price rather than getting bogged down in financing details.

Factors Influencing Your Car Loan in Oregon

Several interconnected factors play a pivotal role in shaping the terms and conditions of your car loans Oregon. Understanding these can help you optimize your application and secure a more favorable deal.

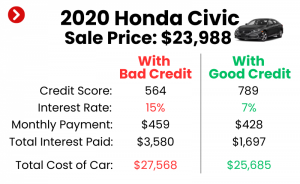

The Indispensable Role of Your Credit Score

As mentioned, your credit score is paramount. Lenders categorize borrowers into different tiers based on their FICO score, and each tier corresponds to a range of interest rates.

- Excellent Credit (780-850): You’ll qualify for the lowest interest rates available.

- Good Credit (670-779): Still eligible for very competitive rates.

- Fair Credit (580-669): Rates will be higher, but loans are generally accessible.

- Poor Credit (300-579): Securing a loan can be challenging, and rates will be significantly higher. This is where options for bad credit car loans Oregon come into play, often requiring a co-signer or larger down payment.

Pro tips from us: Regularly monitor your credit report. Even a small error can negatively impact your score. Dispute any inaccuracies promptly to ensure your credit profile is as strong as possible.

Interest Rates: The Cost of Borrowing

The interest rate, or APR, is the true cost of your loan. It’s not just about the monthly payment; it’s about the total amount you’ll pay over the loan’s lifetime.

Interest rates are influenced by your credit score, the loan term, the economy, and the specific lender. Fixed-rate loans, where the interest rate remains constant throughout the loan term, are most common for car loans. Variable-rate loans, while less common for vehicles, have rates that can fluctuate with market conditions.

When comparing offers, always look at the APR, not just the quoted interest rate, as it provides a more complete picture of the total cost.

Loan Term: Balancing Payments and Total Cost

The loan term, or repayment period, is a crucial consideration. Longer terms mean lower monthly payments, which can make a more expensive car seem affordable.

However, a longer term also means you’ll pay more in total interest over the life of the loan. For example, a 72-month loan will almost certainly cost you more in interest than a 36-month loan for the same principal amount, even if the interest rate is identical.

Common mistakes to avoid are extending the loan term purely to reduce monthly payments without considering the increased total cost. Always strive for the shortest term you can comfortably afford.

The Power of a Down Payment

A substantial down payment is one of your strongest allies in securing favorable Oregon auto loans. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay.

Furthermore, a larger down payment can make you a less risky borrower in the eyes of lenders, potentially qualifying you for a lower interest rate, especially for used car loans Oregon. Aim for at least 10-20% of the vehicle’s purchase price if possible.

Vehicle Choice: New vs. Used and Loan Amount

The type and price of the vehicle you choose directly impact your loan amount. A more expensive car requires a larger loan, leading to higher monthly payments and potentially more interest paid.

Consider your needs versus your wants. While a brand-new luxury SUV might be appealing, a reliable used sedan could be a more financially sound choice, especially if you’re trying to keep your monthly payments manageable. Remember that new cars depreciate quickly, so buying a slightly used car can save you a significant amount on the purchase price and subsequent loan.

Navigating Car Loans with Less-Than-Perfect Credit in Oregon

Don’t despair if your credit score isn’t pristine. While challenging, securing bad credit car loans Oregon is absolutely possible. Many individuals have successfully navigated this path, and it can even be an opportunity to rebuild your credit history.

Options for Borrowers with Challenged Credit

From my observations, many individuals in Oregon with challenged credit have successfully secured auto loans by focusing on a few key strategies:

- Subprime Lenders: These lenders specialize in working with borrowers who have lower credit scores. While their interest rates are typically higher, they offer a viable path to vehicle ownership.

- Co-Signers: A creditworthy co-signer with a good credit score can significantly improve your chances of approval and potentially secure a lower interest rate. The co-signer essentially guarantees the loan, taking on responsibility if you default.

- Larger Down Payment: As discussed, a substantial down payment reduces the lender’s risk and can make your application more attractive, even with a lower credit score.

- Secured Auto Loans: Some lenders offer secured loans where you might put up another asset as collateral, though this is less common for typical car loans.

Avoiding Predatory Lending Practices

When seeking bad credit car loans Oregon, it’s crucial to be vigilant against predatory lenders. These lenders often target vulnerable borrowers with extremely high interest rates, hidden fees, and unfavorable terms.

Always read the fine print, understand all charges, and never feel pressured to sign anything you don’t fully comprehend. If an offer seems too good to be true, or if a lender guarantees approval without checking your credit, proceed with extreme caution. Research the lender’s reputation before committing.

Rebuilding Credit Through a Car Loan

Successfully managing a car loan can be an excellent way to rebuild your credit. By making consistent, on-time payments, you demonstrate financial responsibility, which is reported to credit bureaus.

Over time, this positive payment history will contribute to an improved credit score, opening doors to better financial opportunities in the future. It’s a journey, but a well-managed car loan can be a powerful step forward.

Refinancing Your Car Loan in Oregon

Even after you’ve secured a loan, your financial journey doesn’t have to end there. Refinancing your car loan is a strategy many Oregonians use to improve their loan terms.

Why Consider Refinancing?

Refinance car loan Oregon options allow you to replace your existing car loan with a new one, often with more favorable terms. Common reasons to refinance include:

- Lower Interest Rate: If your credit score has improved since you first took out the loan, or if market rates have dropped, you might qualify for a significantly lower interest rate.

- Lower Monthly Payments: A lower interest rate or an extended loan term (though be cautious with this) can reduce your monthly payment, freeing up cash flow.

- Change Loan Term: You might want to shorten your loan term to pay it off faster and save on interest, or extend it to reduce payments during a financial crunch.

- Remove a Co-Signer: If your credit has improved, you might be able to refinance and remove a co-signer from the original loan, relieving them of their obligation.

For a deeper dive into the specifics of refinancing, you might find our detailed article on particularly helpful.

When is a Good Time to Refinance?

Consider refinancing if:

- Your credit score has improved significantly since your original loan.

- Current interest rates are lower than what you’re currently paying.

- You’re struggling with your current monthly payments and need a more manageable option.

- You initially accepted a high-interest loan due to bad credit and now qualify for better terms.

The process for refinancing is similar to applying for an initial loan, involving an application, credit check, and vehicle information. Shop around for the best rates, just as you would for a new loan.

Oregon Specific Considerations for Car Loans

While many aspects of car loans are universal, there are specific factors unique to the Beaver State that borrowers should be aware of.

No Sales Tax, But Other Fees Apply

One significant advantage for car buyers in Oregon is the absence of a statewide sales tax. This means you won’t pay an additional percentage on the purchase price of your vehicle, which can lead to substantial savings compared to neighboring states.

However, don’t confuse this with a complete absence of fees. You’ll still be responsible for various Oregon Department of Motor Vehicles (DMV) fees, including:

- Title Fees: To transfer ownership of the vehicle into your name.

- Registration Fees: Annual fees to legally operate your vehicle on Oregon roads. These vary based on vehicle type and age.

- License Plate Fees: For new plates or renewals.

These fees are often rolled into your loan amount or paid upfront, so factor them into your overall budget.

Mandatory Auto Insurance Requirements in Oregon

Before you can register and drive your new (or used) vehicle in Oregon, you must have valid auto insurance. Oregon law mandates specific minimum coverage levels:

- Bodily Injury Liability: $25,000 per person / $50,000 per accident

- Property Damage Liability: $20,000 per accident

- Personal Injury Protection (PIP): $15,000 per person

- Uninsured Motorist Coverage: $25,000 per person / $50,000 per accident

Lenders will require proof of insurance before finalizing your loan, as it protects their collateral (the vehicle) in case of an accident. Be sure to factor insurance costs into your monthly budget when considering how to get a car loan in Oregon.

Oregon Lemon Laws

While not directly related to the loan itself, Oregon’s "Lemon Law" provides consumer protection for buyers of new vehicles. If your new car has significant, unfixable defects that substantially impair its use, value, or safety, you may be entitled to a refund or replacement vehicle.

This law offers peace of mind, knowing that if you encounter a truly problematic new vehicle, you have legal recourse. You can find more detailed information on consumer protection and vehicle laws on the official Oregon Department of Justice website.

Pro Tips for Securing the Best Car Loan in Oregon

Armed with this knowledge, you’re well-equipped to navigate the world of Car Loans Oregon. To ensure you secure the absolute best deal, keep these expert tips in mind:

- Shop Around, Always: Never take the first loan offer. Compare rates from multiple banks, credit unions, and online lenders before visiting a dealership. This competitive shopping can save you hundreds, if not thousands, over the loan term.

- Get Pre-Approved: As emphasized, pre-approval strengthens your negotiating position at the dealership and helps you set a realistic budget for the car itself.

- Understand the Full Cost (APR): Focus on the APR, not just the monthly payment. A lower monthly payment over a longer term can still mean paying more overall.

- Read the Fine Print: Carefully review all loan documents before signing. Understand all terms, conditions, fees, and penalties. If something isn’t clear, ask for clarification.

- Negotiate the Car Price First: Separate the car negotiation from the loan negotiation. Aim to get the best possible price on the vehicle before discussing financing options.

- Don’t Stretch the Loan Term Too Long: While longer terms mean lower monthly payments, they also mean more interest paid and a longer period of negative equity (where the car is worth less than what you owe).

- Consider Your Budget Realistically: Beyond the monthly car payment, factor in insurance, fuel, maintenance, and potential repair costs. A comprehensive budget will prevent you from being "car poor." For more budgeting advice, check out our article on .

Conclusion: Drive Away with Confidence

Securing a car loan in Oregon doesn’t have to be a confusing or intimidating experience. By understanding the fundamentals, preparing thoroughly, exploring your options, and applying these expert tips, you can confidently navigate the process. Whether you’re seeking new car loans Oregon or need guidance on bad credit car loans Oregon, the key is to be an informed consumer.

Remember, your goal isn’t just to get a car loan; it’s to get the right car loan that aligns with your financial goals and allows you to enjoy the unparalleled freedom of the open road in beautiful Oregon. Take your time, do your homework, and you’ll be well on your way to driving away with the perfect vehicle and a financing plan you’re comfortable with. Start your journey today, and make your dream of car ownership a well-informed reality.