Navigating the Road to Your Dream Ride: A Comprehensive Guide to the Best Car Loans For Used Cars

Navigating the Road to Your Dream Ride: A Comprehensive Guide to the Best Car Loans For Used Cars Carloan.Guidemechanic.com

Buying a used car is often a smart financial decision, offering excellent value and a wider range of options compared to new vehicles. However, securing the right financing – specifically, the best car loans for used cars – can feel like navigating a complex maze. It’s not just about finding a loan; it’s about finding the right loan that fits your budget, credit profile, and long-term financial goals.

As an expert blogger and professional SEO content writer with years of experience in the automotive and finance sectors, I’ve seen firsthand how a well-chosen used car loan can save you thousands, while a poor one can lead to unnecessary stress and expense. This comprehensive guide will equip you with the knowledge and strategies needed to confidently secure the best possible financing for your pre-owned vehicle. Let’s embark on this journey together.

Navigating the Road to Your Dream Ride: A Comprehensive Guide to the Best Car Loans For Used Cars

Why Your Used Car Loan Choice Truly Matters

Many people view a car loan as a simple necessity, a hurdle to jump before getting the keys. However, the specific terms of your used car loan will dictate a significant portion of your financial life for the next several years. It impacts not just your monthly budget, but also the total cost of your vehicle and your ability to pursue other financial goals.

The interest rate, loan term, and associated fees all play a critical role in determining how much you ultimately pay for your used car. A slight difference in the Annual Percentage Rate (APR) can translate into hundreds or even thousands of dollars over the life of the loan. Understanding these nuances is the first step towards making an informed decision.

Demystifying Used Car Loans: The Essential Terminology

Before diving into where to find the best car loans for used cars, it’s crucial to understand the fundamental terms you’ll encounter. Based on my experience, a clear grasp of this vocabulary empowers you to ask the right questions and evaluate offers effectively.

- Annual Percentage Rate (APR): This is arguably the most important number. The APR represents the true annual cost of borrowing money, including both the interest rate and any additional fees the lender charges. Always compare APRs, not just interest rates, when evaluating loan offers.

- Principal: This is the initial amount of money you borrow to purchase the car. It’s the purchase price of the vehicle minus any down payment or trade-in value.

- Interest Rate: The percentage charged by the lender for borrowing the principal. It’s a component of the APR, but not the whole picture.

- Loan Term: This refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter term usually means higher monthly payments but less total interest paid. Conversely, a longer term offers lower monthly payments but accrues more interest over time.

- Down Payment: This is the upfront cash amount you pay towards the purchase of the car. A larger down payment reduces the principal you need to borrow, often resulting in lower monthly payments and less interest paid over the life of the loan.

- Collateral: In the case of a car loan, the vehicle itself serves as collateral. This means if you fail to make your payments, the lender has the right to repossess the car.

Understanding these terms will allow you to critically assess any loan offer and determine if it aligns with your financial capacity.

Key Factors That Influence Your Used Car Loan Approval and Rates

Lenders evaluate several factors to assess your creditworthiness and determine the interest rate they’re willing to offer for a used car loan. Knowing these elements can help you prepare and even improve your chances of securing favorable terms.

Your Credit Score: The Cornerstone of Your Loan Application

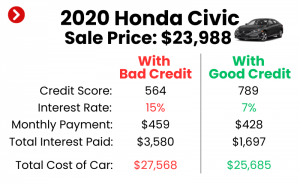

Your credit score is a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. It is, without a doubt, the most significant factor influencing the interest rate you’ll receive on a used car loan.

- Excellent Credit (780-850): Borrowers in this range typically qualify for the lowest interest rates and the most flexible terms. Lenders view them as very low risk.

- Good Credit (670-779): Most consumers fall into this category. You’ll still likely receive competitive rates, though perhaps not the absolute lowest.

- Fair Credit (580-669): Securing a used car loan with fair credit is possible, but you should expect higher interest rates. Lenders see a moderate risk here.

- Poor Credit (300-579): For those with poor credit, obtaining a used car loan can be challenging, and the interest rates will be substantially higher. Lenders may also require a larger down payment or a co-signer.

Pro tips from us: Before even looking at cars, pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) and check for errors. Dispute any inaccuracies, as this could unfairly impact your score. We have a detailed guide on (internal link placeholder) that can help you further.

Your Down Payment: Showing Financial Commitment

A substantial down payment signals to lenders that you are serious about your purchase and reduces their risk. It also lowers the amount you need to borrow, which directly translates to lower monthly payments and less interest over the loan term.

Common mistakes to avoid are underestimating the power of a down payment. Even an extra 5-10% down can significantly impact your loan terms. Aim for at least 10-20% of the vehicle’s purchase price, if possible.

The Loan Term: Balancing Monthly Payments and Total Cost

As mentioned, the loan term dictates how long you’ll be making payments. While a longer term might offer attractive low monthly payments, it invariably leads to paying more interest over the life of the loan.

Based on my experience, many borrowers get fixated on the lowest possible monthly payment, neglecting the total cost. A 72-month loan might seem appealing, but often a 48 or 60-month loan offers a better balance between affordability and overall cost.

Your Debt-to-Income Ratio (DTI): Can You Afford It?

Lenders assess your DTI to determine if you have enough disposable income to comfortably make your car loan payments. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates less risk for the lender.

Generally, a DTI below 36% is considered ideal, though some lenders may approve loans for ratios up to 43% or even higher for specific programs.

Vehicle Age and Mileage: The Lender’s Perspective

Used cars carry more inherent risk for lenders compared to new vehicles. Older cars with high mileage might be seen as less reliable and more prone to needing costly repairs, which could impact your ability to make payments. Some lenders have restrictions on the maximum age or mileage they will finance.

This is why you might find slightly higher interest rates on very old or high-mileage used cars, as the perceived risk of depreciation and breakdown is greater.

Where to Find the Best Car Loans For Used Cars

The landscape of auto lending is diverse, offering multiple avenues to secure financing. Each option has its unique advantages and disadvantages. Shopping around is a critical step to ensure you get the most competitive offer.

1. Banks: The Traditional Route

Major national and regional banks are often the first place people consider for car loans. They offer a variety of loan products and can be a good option, especially if you have an existing banking relationship and good credit.

- Pros: Established institutions, often offer competitive rates for prime borrowers, convenient if you already bank with them.

- Cons: May have stricter lending criteria, can be slower in processing applications, might not be as flexible for those with less-than-perfect credit.

2. Credit Unions: Member-Focused Advantages

Credit unions are non-profit financial cooperatives that often offer some of the most competitive interest rates on auto loans, including those for used cars. Their "member-first" philosophy often translates to better deals.

- Pros: Generally lower interest rates, more flexible lending terms, personalized service, easier to qualify for members with fair credit.

- Cons: Requires membership (though usually easy to join), branch networks might be smaller than large banks.

Pro tips from us: Don’t overlook credit unions! Even if you’re not a member, many have open membership criteria based on location or affiliation. It’s often worth the small effort to join for potential savings.

3. Online Lenders: Speed and Convenience

The rise of online lenders has revolutionized the car loan application process. Companies like Capital One Auto Finance, LightStream, and others offer quick pre-approvals and a streamlined digital experience.

- Pros: Fast application and approval process, ability to compare multiple offers from various lenders quickly, often cater to a wider range of credit scores.

- Cons: Less personalized service, requires comfort with digital transactions, some may offer less competitive rates for certain credit tiers.

This can be a fantastic way to quickly get multiple quotes and compare the best car loans for used cars from the comfort of your home.

4. Dealership Financing: Convenience at a Cost?

Many dealerships offer in-house financing or work with a network of lenders. This option provides a "one-stop shop" experience, allowing you to buy the car and secure financing all in one place.

- Pros: Extreme convenience, potential for special promotions, can sometimes work with challenging credit situations.

- Cons: Dealers often mark up the interest rate to profit from the loan, may not present you with the absolute best rate available, less transparency in comparing offers.

Common mistakes to avoid are accepting the first financing offer from a dealership without having pre-approval from an outside lender. Always get pre-approved elsewhere first; it gives you a benchmark and negotiation leverage.

Applying for a Used Car Loan: A Step-by-Step Guide

The application process doesn’t have to be daunting. Following these steps will help ensure a smooth and successful experience.

Step 1: Get Pre-Approved Before You Shop

This is arguably the most crucial step. Getting pre-approved means a lender has reviewed your credit and income and committed to lending you a specific amount at a particular interest rate, before you even pick out a car.

Based on my experience, pre-approval transforms you into a cash buyer at the dealership. You’ll know your budget, your rate, and you can focus solely on negotiating the car’s price, rather than getting caught up in financing negotiations.

Step 2: Gather Your Essential Documents

Lenders will require several documents to verify your identity, income, and residence. Having these ready will expedite the application process.

- Proof of Identity: Driver’s license, state ID, passport.

- Proof of Income: Recent pay stubs (1-2 months), W-2 forms, tax returns (for self-employed).

- Proof of Residence: Utility bill, lease agreement, mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information: Once you’ve chosen a car, you’ll need its VIN, make, model, and mileage.

Step 3: Fill Out the Application Accurately

Whether online or in person, take your time to complete the application fully and accurately. Any discrepancies could cause delays or even rejection. Be honest about your financial situation.

Step 4: Understand and Compare Loan Offers

Once you receive loan offers, don’t just look at the monthly payment. Scrutinize the APR, the total interest paid over the loan term, and any fees.

Pro tips from us: Create a simple spreadsheet to compare offers side-by-side. Focus on the APR and total cost, not just the monthly payment. This helps you truly identify the best car loans for used cars.

Step 5: Finalize the Deal and Read the Fine Print

Before signing anything, read all loan documents carefully. Ensure that the terms and conditions match what you were offered. Don’t hesitate to ask questions about anything you don’t understand.

Strategies to Secure the Best Used Car Loan Rates

Even if your credit isn’t perfect, there are proactive steps you can take to improve your chances of getting a great rate on your used car loan.

- Boost Your Credit Score: Pay all your bills on time, reduce existing debt, and avoid opening new credit accounts in the months leading up to your car loan application. Every point counts!

- Save for a Larger Down Payment: As discussed, a larger down payment reduces the loan amount and signals financial stability to lenders.

- Shorten Your Loan Term: While it means higher monthly payments, a shorter loan term almost always results in less total interest paid and often a slightly lower interest rate, as the lender’s risk is reduced.

- Shop Around Aggressively: This cannot be stressed enough. Get pre-approvals from at least 3-4 different lenders (banks, credit unions, online lenders) within a short window (14-45 days) to minimize the impact on your credit score. This allows you to truly compare and select the best car loans for used cars.

- Consider a Co-signer: If your credit score is on the lower side, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. However, understand that the co-signer is equally responsible for the debt.

Common Mistakes to Avoid When Getting a Used Car Loan

Based on my extensive experience, certain pitfalls commonly trip up used car buyers. Steering clear of these can save you money and stress.

- Not Getting Pre-Approved: This leaves you vulnerable to dealership markups and reduces your negotiating power.

- Focusing Only on Monthly Payments: This can lead to longer loan terms and significantly higher total interest paid. Always consider the total cost of the loan.

- Ignoring the APR: The interest rate alone doesn’t tell the full story. The APR is the true cost of borrowing.

- Skipping a Pre-Purchase Vehicle Inspection: Before you finance a used car, always have an independent mechanic inspect it. You don’t want to take out a loan for a car that needs thousands in repairs. We have a helpful article on (internal link placeholder) that elaborates on this.

- Accepting the First Offer: Always compare multiple loan offers. Competition among lenders benefits you.

- Not Budgeting for Additional Costs: Remember to factor in insurance, registration, maintenance, and potential repair costs when budgeting for your used car and its loan.

Special Considerations for Used Car Loans

Bad Credit Used Car Loans

If your credit score is less than ideal, don’t despair. Securing a used car loan is still possible, though the terms will likely be less favorable.

- Look for specialized lenders: Some online lenders and credit unions specialize in bad credit auto loans.

- Expect higher interest rates: Lenders compensate for higher risk with higher APRs.

- Prepare for a larger down payment: This reduces the lender’s risk.

- Consider a co-signer: As mentioned, a co-signer can greatly improve your chances.

- Focus on improving your credit: Use this loan as an opportunity to rebuild your credit by making consistent, on-time payments.

Refinancing Your Used Car Loan

Did you get a used car loan with a higher interest rate than you’d like? Perhaps your credit score has improved significantly since then, or interest rates have dropped. Refinancing your used car loan can be a smart move.

- When to consider it: If your credit score has improved, current interest rates are lower, or you want to change your loan term (e.g., shorten it to save interest or lengthen it for lower payments).

- How it works: You apply for a new loan to pay off your existing one, ideally with better terms.

For more detailed information on consumer financial products, including auto loans, you can refer to trusted external sources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.

Pro Tips From Us: Your Expert Edge

- Always Negotiate: The sticker price on a car is rarely the final price. The same goes for loan offers, especially if you have competing pre-approvals.

- Understand the Total Cost: Beyond the monthly payment, calculate the total amount you’ll pay over the life of the loan (principal + total interest). This gives you the clearest financial picture.

- Read All Documents Carefully: Don’t rush through the paperwork. Ask for explanations for anything unclear before you sign.

- Don’t Rush the Process: Take your time to research, compare, and make an informed decision. A car loan is a significant financial commitment.

Conclusion: Drive Away with Confidence

Finding the best car loans for used cars doesn’t have to be a stressful ordeal. By understanding the key terminology, knowing where to look, diligently preparing your application, and employing smart strategies, you can secure financing that truly works for you. Remember, the goal isn’t just to get approved, but to get approved for terms that save you money and align with your financial well-being.

Empower yourself with knowledge, shop around with confidence, and you’ll be well on your way to driving off in your perfect used car, knowing you made the best financial decision possible. Happy car hunting!