Navigating the Road to Your Dream Ride: The Best Used Car Loan Companies for Smart Buyers

Navigating the Road to Your Dream Ride: The Best Used Car Loan Companies for Smart Buyers Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car can be exhilarating. The thrill of finding the perfect vehicle at an attractive price often comes with a crucial next step: securing the right financing. For many, a used car loan is the key to unlocking ownership, but the sheer number of lenders can feel overwhelming. How do you choose the best used car loan companies that truly fit your needs and budget?

As an expert blogger and professional SEO content writer who has navigated the complexities of auto financing for years, I understand the importance of making an informed decision. This comprehensive guide is designed to cut through the noise, offering you a deep dive into the world of used car loans. We’ll explore various lender types, highlight top contenders, and equip you with the knowledge to secure the most favorable terms. Our ultimate goal is to empower you to drive away with confidence, knowing you’ve made a smart financial choice.

Navigating the Road to Your Dream Ride: The Best Used Car Loan Companies for Smart Buyers

Why Opt for a Used Car Loan? Understanding the Value Proposition

Before we delve into specific lenders, let’s briefly consider why a used car loan is often a sensible choice for many buyers. While some prefer the allure of a brand-new vehicle, used cars offer significant advantages, especially when financed appropriately.

Firstly, used cars typically come with a lower purchase price compared to their brand-new counterparts. This directly translates to a smaller loan amount, which can mean lower monthly payments and less interest paid over the life of the loan. It’s a pragmatic approach to vehicle ownership, allowing you to stretch your budget further.

Secondly, new cars experience rapid depreciation the moment they leave the dealership lot. By opting for a used car, you avoid this initial, steep drop in value. Your financing is based on an already depreciated asset, offering better value retention over time. This financial stability is a compelling reason for many savvy car buyers.

Finally, the used car market offers an incredible diversity of makes, models, and features that might be out of reach in the new car segment. A used car loan can make a premium, well-maintained vehicle accessible, allowing you to enjoy higher-end features or better performance without the new car price tag. It’s about maximizing your investment and getting more for your money.

Essential Factors to Consider When Choosing a Used Car Loan Lender

Selecting the right used car loan company isn’t just about finding the lowest interest rate. Based on my experience and extensive research, several critical factors play a pivotal role in determining the overall quality and suitability of a loan offer. Ignoring these can lead to unexpected costs or long-term financial strain.

Interest Rates: The Cost of Borrowing

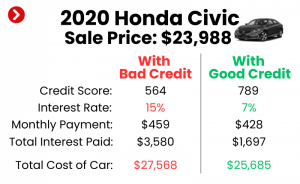

The interest rate is arguably the most significant factor, as it directly impacts the total amount you’ll pay over the loan’s term. A lower interest rate means less money spent on borrowing and more money available for other expenses. Even a difference of one or two percentage points can save you hundreds, if not thousands, of dollars over several years.

Interest rates are primarily influenced by your credit score, the loan term, the down payment amount, and the overall economic environment. Lenders assess your creditworthiness to determine the risk involved in lending to you. A higher credit score signals lower risk, typically resulting in more attractive interest rate offers.

Loan Terms and Repayment Periods

The loan term refers to the length of time you have to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72 months). While longer terms often lead to lower monthly payments, they also mean you’ll pay more in total interest over time. It’s a delicate balance between affordability and the overall cost of the loan.

Pro tip from us: Aim for the shortest loan term you can comfortably afford. This minimizes the total interest paid and helps you build equity in your vehicle faster. While a 72-month loan might seem appealing for its low monthly payment, carefully calculate the total cost before committing.

Fees and Additional Charges

Beyond the interest rate, some lenders may impose various fees that can add to the total cost of your loan. These might include origination fees, application fees, prepayment penalties, or late payment fees. It’s crucial to thoroughly review the loan agreement for any hidden charges.

Common mistakes to avoid are overlooking these fees during the comparison phase. Always ask for a clear breakdown of all potential costs associated with the loan. A loan with a slightly higher interest rate but no fees might sometimes be more economical than one with a lower rate burdened by hefty upfront charges.

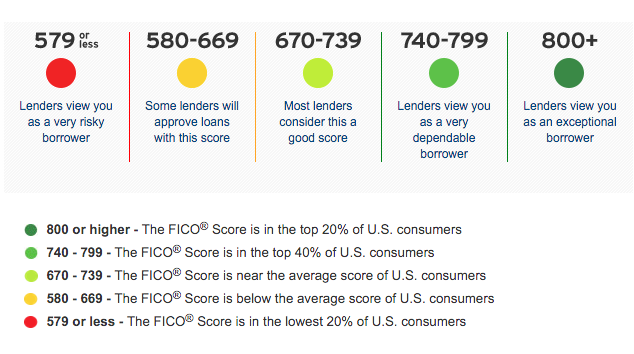

Your Credit Score: The Ultimate Game Changer

Your credit score is the most powerful tool in your arsenal when applying for a used car loan. Lenders use it as a primary indicator of your financial responsibility and ability to repay debt. A strong credit score (generally 700+) opens the door to the most competitive rates and favorable terms.

If your credit score isn’t where you’d like it to be, don’t despair. There are still options available, but understanding how your score impacts your loan offers is vital. We’ll discuss lenders catering to various credit profiles later in this article. Improving your credit score, even slightly, before applying can significantly enhance your borrowing power.

Diving Deep: Categories of Used Car Loan Companies

The landscape of auto lenders is diverse, with different types of institutions offering distinct advantages and disadvantages. Understanding these categories is the first step in narrowing down your search for the best used car loan company.

1. Traditional Banks: Reliability and Established Presence

Traditional banks like Chase, Bank of America, and Wells Fargo are often the first stop for many borrowers. They are well-established financial institutions with extensive resources and a reputation for stability. Their auto loan departments typically offer a range of products, from new to used car loans, often with competitive rates for borrowers with excellent credit.

Pros:

- Competitive Rates: Especially for borrowers with strong credit histories.

- Established Reputation: Offers a sense of security and reliability.

- Convenience: If you already bank with them, it can simplify the application process and loan management.

Cons:

- Strict Eligibility: Often have stringent credit score requirements, making them less accessible for those with fair or poor credit.

- Less Flexibility: Loan terms and conditions might be less flexible compared to other lender types.

- Slower Approval Process: Can sometimes take longer to approve loans compared to online lenders.

Who they are good for: Borrowers with good to excellent credit who value the stability and comprehensive services of a major financial institution.

2. Credit Unions: Member-Focused and Often More Flexible

Credit unions are non-profit financial cooperatives owned by their members. This structure often translates to a member-first approach, leading to potentially lower interest rates and more personalized service compared to traditional banks. Examples include PenFed Credit Union, Alliant Credit Union, and local community credit unions.

Pros:

- Lower Rates and Fees: Often offer some of the most competitive interest rates and fewer fees.

- Personalized Service: Known for a more human-centered approach to lending.

- Flexibility: May be more willing to work with borrowers who have less-than-perfect credit, especially if they are long-standing members.

Cons:

- Membership Requirements: You must meet specific eligibility criteria to join a credit union (e.g., live in a certain area, work for a particular employer, or join an associated organization).

- Limited Branch Network: May not have as many physical locations as large banks.

- Slightly Slower Technology Adoption: Some credit unions may not have the same level of digital convenience as large online lenders, though this is rapidly changing.

Who they are good for: Borrowers seeking competitive rates and personalized service, especially those who can meet membership requirements or have fair credit and a good relationship with a local credit union.

3. Online Lenders: Speed, Convenience, and Wide Accessibility

The rise of online lenders has revolutionized the auto loan market, offering unparalleled speed and convenience. Companies like LightStream (a division of Truist Bank), Capital One Auto Finance, and Upstart provide quick online applications, rapid approval decisions, and often direct funding. They leverage technology to streamline the borrowing process.

Pros:

- Speed and Convenience: Apply and get approved from anywhere, often within minutes.

- Competitive Rates: Many online lenders offer very attractive rates, especially for well-qualified borrowers.

- Wider Range of Credit Profiles: Some online lenders specialize in catering to borrowers across the credit spectrum, including those with fair or even bad credit.

Cons:

- Less Personal Interaction: The entirely online nature means less face-to-face assistance.

- Scam Risk: It’s crucial to verify the legitimacy of online lenders to avoid predatory practices. Stick to well-known and reputable platforms.

- May Require Strong Digital Literacy: The process is primarily self-service through online portals.

Who they are good for: Tech-savvy borrowers seeking a fast, convenient, and often competitive loan experience, regardless of their credit score (though rates will vary).

4. Dealership Financing: One-Stop Shopping Convenience

Many car dealerships offer in-house financing or work with a network of lenders to provide loan options directly at the point of sale. This "one-stop shop" approach can be incredibly convenient, allowing you to choose and finance your car all in one visit.

Pros:

- Convenience: Streamlined process; you can often drive off the lot with your new-to-you car the same day.

- Special Offers: Dealerships sometimes have special financing incentives or rebates that can lower the overall cost.

- Negotiation Power: You might be able to bundle the financing with the car price negotiation.

Cons:

- Potentially Higher Rates: Dealerships may mark up interest rates to earn a profit, meaning you might not get the best rate available.

- Limited Options: You are typically limited to the lenders the dealership partners with, which might not be the full market.

- Pressure Sales: There can be pressure to make a quick decision, potentially leading to less favorable terms.

Who they are good for: Buyers prioritizing convenience, especially those who prefer to handle everything in one place. However, always compare dealership offers with pre-approved loans from other sources.

Spotlight on Top Used Car Loan Companies by Credit Profile

Finding the best used car loan companies often depends on your individual credit situation. Let’s break down some highly regarded lenders across different credit tiers.

For Excellent Credit (720+ FICO Score)

If you boast an excellent credit score, you’re in the prime position to secure the lowest interest rates and most favorable terms. These lenders are often the best starting points.

LightStream

Overview: LightStream, a division of Truist Bank, is renowned for its low rates and streamlined online application process. They offer unsecured loans, meaning the car itself isn’t used as collateral, which can be advantageous.

Why they stand out: They pride themselves on offering "best rate guarantee" and require excellent credit for their most competitive offers. The application is entirely online, and funding can be incredibly fast. Based on my experience, their efficiency is hard to beat for well-qualified applicants.

PenFed Credit Union

Overview: PenFed (Pentagon Federal Credit Union) consistently ranks among the top for auto loans due to its competitive rates and flexible terms. While it’s a credit union, membership is relatively easy to obtain.

Why they stand out: For excellent credit, PenFed’s rates are often among the lowest available. They offer various loan terms and allow for pre-approval, which is a significant advantage when car shopping. Their member-centric approach means excellent customer service.

Chase Auto

Overview: As one of the largest banks in the U.S., Chase offers a robust auto loan program for used cars. They provide competitive rates and a straightforward application process, especially for existing Chase customers.

Why they stand out: Chase offers both direct-to-consumer loans and financing through dealerships. Their strong reputation and extensive branch network provide convenience. For those with excellent credit, their rates can be very attractive, and their online tools are user-friendly.

For Good Credit (660-719 FICO Score)

With good credit, you still have access to very competitive rates, though they might be slightly higher than those for excellent credit. Focus on lenders that reward responsible borrowing.

Capital One Auto Finance

Overview: Capital One is a popular choice for auto loans, known for its user-friendly pre-qualification process that doesn’t impact your credit score. They work with a vast network of dealerships, making it easy to find a car and financing in one place.

Why they stand out: Capital One offers a broad range of loan options for various credit profiles. Their online pre-qualification tool is a pro tip from us – it allows you to see potential rates without a hard inquiry, empowering you to shop confidently. They also offer direct financing.

Local Credit Unions

Overview: While specific names vary by region, local credit unions are often hidden gems for borrowers with good credit. They are known for their community focus and willingness to work with members.

Why they stand out: Local credit unions often provide more personalized service and may be more understanding of unique financial situations than larger banks. Their rates are consistently competitive, and they frequently offer attractive terms for used car loans. It’s always worth checking with your local options.

For Fair/Average Credit (600-659 FICO Score)

Having fair credit means you might see higher interest rates, but securing a used car loan is definitely achievable. Focus on lenders that specialize in or are accustomed to working with this credit tier.

Upstart

Overview: Upstart uses an AI-powered lending model that considers more than just your credit score, including education and job history. This broader assessment can be beneficial for those with limited credit history or fair scores.

Why they stand out: Their innovative approach means they might approve applicants who traditional lenders would overlook. While they primarily offer personal loans, these can be used for car purchases, offering flexibility. They often provide quick decisions and funding.

Auto Credit Express

Overview: Auto Credit Express is not a direct lender but a network that connects borrowers with bad or fair credit to dealerships and lenders who specialize in subprime auto loans.

Why they stand out: They specialize in helping individuals with challenging credit find financing. While rates will be higher, they can be a lifeline for those struggling to get approved elsewhere. Common mistakes to avoid here are accepting the first offer; always compare the multiple offers they might present.

For Bad Credit (Below 600 FICO Score)

Securing a used car loan with bad credit can be challenging, and interest rates will be significantly higher. However, it’s not impossible. The key is to manage expectations and work with lenders who understand your situation.

Carvana

Overview: Carvana is an online used car retailer that also offers its own financing. They are known for their simplified online buying and financing process.

Why they stand out: Carvana provides an end-to-end solution, from choosing a car to securing a loan, all online. They cater to a broad range of credit scores, including those with less-than-perfect credit. While their rates might be higher for bad credit, the convenience and transparency of the process are appealing.

Specialized Subprime Lenders (e.g., Ally Clearlane, local Buy Here Pay Here dealerships)

Overview: These lenders specifically cater to individuals with bad credit. They understand the risks involved and structure loans accordingly, often with higher interest rates and sometimes requiring collateral or specific down payment amounts.

Why they stand out: They are often the only option for those with very low credit scores. While interest rates can be high, securing a loan and making timely payments can be a crucial step towards rebuilding your credit. For more details on credit rebuilding, consider reading our article on . Always exercise caution and thoroughly review terms with these lenders.

The Used Car Loan Application Process: A Step-by-Step Guide

Navigating the application process can seem daunting, but breaking it down into manageable steps makes it much simpler. Following this guide will help you stay organized and increase your chances of approval.

Step 1: Check Your Credit Score and Report

Before you even think about applying, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and check your FICO score. You can do this annually for free at AnnualCreditReport.com. This gives you a clear picture of your creditworthiness and allows you to dispute any errors. Knowing your score helps you target appropriate lenders.

Step 2: Determine Your Budget

Realistically assess how much you can afford for a monthly car payment, including insurance, fuel, and maintenance. Don’t just focus on the car’s price; consider the total cost of ownership. A smart budget ensures you don’t overextend yourself financially.

Step 3: Get Pre-Approved (Crucial Step!)

This is perhaps the most important pro tip from us. Getting pre-approved by several lenders before stepping foot on a dealership lot gives you immense power. It provides you with a concrete loan offer (interest rate, loan term, maximum loan amount) and lets you know exactly what you can afford. This separates the financing negotiation from the car price negotiation, giving you a stronger hand.

Step 4: Gather Your Documents

Once you have a pre-approval, or if you’re applying directly, have all necessary documents ready. This typically includes:

- Proof of identity (driver’s license)

- Proof of income (pay stubs, tax returns)

- Proof of residence (utility bill)

- Bank statements

- Social Security number

Having these prepared streamlines the application and approval process, preventing delays.

Step 5: Compare Loan Offers

Do not settle for the first offer you receive. Compare interest rates, loan terms, fees, and any other conditions from multiple lenders. Use your pre-approval offers as leverage when negotiating with a dealership or other lenders. This comparison is where significant savings can be made.

Step 6: Finalize Your Loan and Purchase

Once you’ve chosen the best offer, review the loan agreement meticulously. Understand every clause, especially regarding interest rates, fees, and repayment schedules. Don’t hesitate to ask questions. Once satisfied, sign the documents and proceed with your used car purchase.

Common Mistakes to Avoid When Getting a Used Car Loan

Even the savviest buyers can make missteps if they’re not careful. Based on my experience, avoiding these common pitfalls can save you money and stress.

1. Not Comparing Loan Offers

This is perhaps the biggest mistake. Many buyers only get one loan offer, often from the dealership, and assume it’s the best they can get. Always shop around with at least 3-5 lenders. The slight effort can lead to substantial savings over the loan’s term.

2. Focusing Only on Monthly Payments

While a low monthly payment is appealing, it can often hide a longer loan term and a higher total cost of interest. Always consider the total amount you’ll pay back, not just the monthly installment. A lower monthly payment over a very long term might end up costing you more in the long run.

3. Extending the Loan Term Too Long

As mentioned, longer loan terms (e.g., 72 or 84 months) result in lower monthly payments but significantly increase the total interest paid. They also mean you’re "upside down" (owe more than the car is worth) for a longer period, which can be problematic if you need to sell or trade in the car early.

4. Ignoring the Fine Print

Loan agreements are legally binding documents. Common mistakes to avoid include skimming or completely overlooking crucial details like prepayment penalties, late fees, or clauses about default. Always read the entire document carefully before signing.

5. Letting Dealerships Run Excessive Credit Checks

Each time a lender performs a "hard inquiry" on your credit, it can slightly ding your score. While shopping for an auto loan within a short window (typically 14-45 days, depending on the scoring model) is often grouped as one inquiry, too many scattered inquiries can harm your score. Get pre-approved and limit hard inquiries to serious offers.

Pro Tips for Securing the Best Used Car Loan

Beyond avoiding mistakes, there are proactive steps you can take to put yourself in the strongest negotiating position.

1. Improve Your Credit Score Before Applying

If time permits, dedicating a few months to boosting your credit score can dramatically impact your loan offers. Pay bills on time, reduce credit card debt, and check for errors on your credit report. A higher score translates directly to lower interest rates.

2. Make a Significant Down Payment

A larger down payment reduces the amount you need to borrow, which means less interest paid overall. It also signals to lenders that you are a lower risk, potentially earning you a better interest rate. Plus, it helps prevent you from going upside down on your loan.

3. Consider a Co-Signer (If Applicable)

If you have fair or bad credit, a co-signer with excellent credit can help you qualify for better rates. The co-signer essentially guarantees the loan, reducing the lender’s risk. However, ensure both parties understand the responsibilities, as the co-signer is equally liable for the debt.

4. Negotiate!

Everything is negotiable, from the car price to the loan terms. Don’t be afraid to ask for a lower interest rate or fewer fees. Your pre-approval offers are your best negotiating tool. If you want to learn more about how interest rates work, check out our guide on .

5. Shop for the Car and the Loan Separately

This reiterates the importance of pre-approval. When you separate the two processes, you can focus on getting the best deal on the car without feeling pressured by financing, and vice-versa. It empowers you to make two distinct, advantageous decisions.

Conclusion: Drive Away with Confidence

Choosing the best used car loan company is a critical component of a smart car purchase. By understanding the different types of lenders, assessing your own credit profile, diligently comparing offers, and avoiding common pitfalls, you can secure financing that aligns with your financial goals. Remember, the goal isn’t just to get a loan, but to get the right loan.

Armed with the knowledge from this comprehensive guide, you are now well-equipped to navigate the used car loan market with confidence. Take your time, do your research, and don’t settle for anything less than the best terms available to you. Your journey to a great used car experience starts with making an informed and empowered financing decision. For more insights into responsible borrowing, consider visiting the Consumer Financial Protection Bureau’s resources on auto loans: External Link: CFPB Auto Loan Resources. Happy driving!