Navigating the Road to Your New Ride: A Comprehensive Guide to Getting A Car Loan From A Bank

Navigating the Road to Your New Ride: A Comprehensive Guide to Getting A Car Loan From A Bank Carloan.Guidemechanic.com

The dream of a new car often comes with the practical reality of financing. For many, this means getting a car loan from a bank. While dealerships offer convenience, banks often provide competitive rates, transparent terms, and the peace of mind that comes with a trusted financial institution. But how exactly do you navigate this process to secure the best possible deal and ensure a smooth approval?

This article serves as your ultimate guide, meticulously breaking down every aspect of getting a car loan from a bank. From understanding what lenders look for to mastering the application process, we’ll equip you with the knowledge and strategies to drive away with confidence. Our goal is to make this complex journey straightforward, ensuring you secure the financing that best suits your needs.

Navigating the Road to Your New Ride: A Comprehensive Guide to Getting A Car Loan From A Bank

Why Banks Are a Smart Choice for Your Auto Loan

When considering how to finance your next vehicle, you’ll encounter various options. Dealerships, credit unions, and online lenders all present avenues for auto financing. However, banks often stand out as a premier choice for several compelling reasons. They bring a level of stability, transparency, and competitive offerings that can be incredibly beneficial to the borrower.

One primary advantage is the potential for lower interest rates. Banks, especially larger ones, have vast resources and a broad customer base, allowing them to offer highly competitive Annual Percentage Rates (APRs). This can translate into significant savings over the life of your loan compared to what might be offered at a dealership, where rates can sometimes include hidden fees or markups.

Furthermore, banks provide an opportunity to consolidate your financial life. If you already have a checking, savings, or mortgage account with a particular bank, securing your car loan approval there can strengthen your relationship with the institution. This can potentially lead to better terms on future financial products or personalized customer service. Based on my experience, existing bank customers often receive preferential treatment, including slight rate discounts or expedited application processes.

Understanding the Anatomy of a Car Loan

Before diving into the application process, it’s crucial to grasp the fundamental components of a car loan. Knowing these terms will empower you to make informed decisions and confidently negotiate terms. It’s not just about the monthly payment; it’s about the entire financial commitment.

The Annual Percentage Rate (APR) is perhaps the most critical number to understand. It represents the true annual cost of borrowing money, including the interest rate and any additional fees charged by the lender. A lower APR means you’ll pay less interest over the loan term. Always compare APRs, not just interest rates, when shopping for bank car loans.

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term generally means higher monthly payments but less interest paid overall. Conversely, a longer term reduces your monthly payments but increases the total interest expense. It’s a delicate balance between affordability and total cost.

The principal is the initial amount of money borrowed for the car. As you make payments, a portion goes towards the principal and a portion to the interest. Building equity in your car means reducing the principal amount owed faster than its depreciation.

The Pillars of Car Loan Approval: What Banks Truly Look For

Banks are in the business of lending money responsibly, which means they carefully assess your ability to repay a loan. When you’re getting a car loan from a bank, they evaluate several key financial indicators to determine your creditworthiness and the terms they’re willing to offer. Understanding these pillars is your first step towards successful car loan approval.

Your Credit Score: The Ultimate Financial Report Card

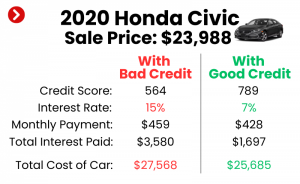

Your credit score for car loan applications is paramount. This three-digit number, primarily FICO or VantageScore, provides lenders with a snapshot of your financial history and your reliability as a borrower. A higher score indicates a lower risk, making you eligible for better interest rates and terms.

Typically, scores range from 300 to 850. A score of 700 and above is generally considered good, while 750+ is excellent. Lenders look for a history of timely payments, responsible use of credit, and a manageable amount of debt. Based on my experience, even a few points can make a difference in your APR, so knowing your score beforehand is crucial. You can obtain a free credit report annually from each of the three major credit bureaus (Experian, Equifax, TransUnion).

- Pro Tip: Check your credit report for inaccuracies before applying. Disputing errors can quickly boost your score. If your score is lower than desired, focus on paying bills on time, reducing credit card balances, and avoiding new credit applications for a few months.

Debt-to-Income Ratio (DTI): A Measure of Your Capacity

Your debt-to-income ratio (DTI) is another critical factor. It’s a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to handle additional debt, like a car loan, without becoming financially strained.

To calculate your DTI, sum up all your monthly debt payments (mortgage/rent, student loans, credit card minimums, etc.) and divide that by your gross monthly income (before taxes and deductions). For instance, if your debts are $1,000 and your income is $3,000, your DTI is 33%. Banks typically prefer a DTI of 36% or lower, though some might go higher depending on other factors. A lower DTI signifies more disposable income, making you a more attractive borrower for securing a car loan.

Income Stability and Employment History: Proof of Steady Repayment

Banks want assurance that you have a consistent and reliable source of income to make your monthly payments. They will typically ask for proof of employment, such as recent pay stubs, W-2 forms, or tax returns if you’re self-employed. A stable employment history, often two or more years at the same company or in the same industry, signals financial stability.

Frequent job changes, especially within a short period, can raise red flags for lenders. If you’re new to your job, be prepared to provide a detailed employment history and explain any gaps or transitions. This is a key component in demonstrating your long-term capacity for financing a car.

The Power of a Down Payment for Car Loan

Making a down payment for car loan is one of the most effective ways to improve your chances of approval and secure better loan terms. A down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan’s life.

From the bank’s perspective, a significant down payment reduces their risk. It shows your commitment to the purchase and ensures you have immediate equity in the vehicle. While there’s no fixed rule, a 10-20% down payment is often recommended, especially for new cars. For used cars, a larger down payment can be even more beneficial due to faster depreciation.

- Common mistake to avoid: Skipping the down payment entirely. While 0% down loans exist, they often come with higher interest rates and leave you "upside down" (owing more than the car is worth) very quickly.

Vehicle Information: The Collateral’s Value

Since most car loans are secured loans, the vehicle itself acts as collateral. Banks will assess the car’s value, age, and mileage to determine its worth and how quickly it might depreciate. This is particularly important for used vehicles. Lenders often use valuation guides like Kelley Blue Book (KBB) or NADAguides to ascertain the car’s fair market value.

The bank needs to be confident that if you default on the loan, they can recoup their losses by repossessing and selling the car. Therefore, very old or high-mileage vehicles might be harder to finance through a traditional bank, or they might come with stricter terms.

Your Step-by-Step Guide to Getting a Car Loan From a Bank

Now that you understand what banks are looking for, let’s walk through the practical steps to get a car loan from a bank. This structured approach will streamline your journey and increase your likelihood of success.

Step 1: Assess Your Financial Health and Set a Realistic Budget

Before even looking at cars, take an honest look at your finances. This involves more than just checking your credit score. Evaluate your monthly income, essential expenses, and existing debt obligations. Determine how much you can comfortably afford for a monthly car payment, including insurance, fuel, maintenance, and potential registration fees.

- Pro Tip from us: Use a budgeting app or spreadsheet to track your spending for a month or two. This will give you a clear picture of your disposable income. Don’t forget to factor in potential increases in insurance premiums for a new vehicle. We have an excellent guide on Budgeting for Your First Car: What You Need to Know that can help you with this crucial first step.

Step 2: Get Pre-Approved for a Car Loan

This is arguably the most powerful step you can take. Getting pre-approval car loan means a bank has provisionally agreed to lend you a specific amount of money at a certain interest rate, pending a final vehicle choice. It transforms you into a cash buyer at the dealership, giving you significant negotiation power.

To get pre-approved, you’ll typically provide your personal and financial information, including income, employment history, and authorization for a credit check. The bank will then give you a pre-approval letter outlining the loan amount, estimated interest rate, and loan term. This process usually involves a "hard inquiry" on your credit report, which can slightly lower your score temporarily.

- Common mistake to avoid: Waiting until you’re at the dealership to think about financing. Without pre-approval, you’re at the mercy of the dealer’s finance department, which might not offer you the best terms.

Step 3: Shop Around for the Best Car Loan Rates

Don’t settle for the first offer you receive. Just as you’d shop for the best car, shop for the best car loan rates. Apply for pre-approval at 2-3 different banks. This allows you to compare offers and leverage them against each other.

Because multiple credit inquiries for the same type of loan within a short period (typically 14-45 days) are often counted as a single inquiry by credit scoring models, you can shop around without significantly harming your credit score. This is your opportunity to secure the most favorable APR for your auto loan application.

Step 4: Choose Your Car Wisely

With pre-approval in hand, you know your budget. Now, it’s time to find the right vehicle. Remember that the car’s value and age can impact your final loan terms. Stick to your budget and consider the total cost of ownership, not just the purchase price.

- Pro Tip from us: If you’re pre-approved for a specific amount, don’t feel obligated to spend it all. Buying a less expensive car means lower payments and more financial flexibility.

Step 5: Gather All Necessary Documents

Once you’ve found your car and are ready to finalize the loan, you’ll need to provide several documents for car loan processing. Being prepared with these items will significantly speed up the approval process.

Commonly required documents include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (2-3 months), W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Bank Statements: Recent statements to show financial stability.

- Vehicle Information: Bill of sale, VIN (Vehicle Identification Number), and possibly title information for a used car.

- Insurance Information: Proof of auto insurance is usually required before driving off the lot.

Step 6: Submit Your Final Application

With your chosen car and all documents in hand, you’ll submit your formal auto loan application to the bank offering the best terms. This step confirms all the details from your pre-approval and finalizes the loan amount based on the actual vehicle purchase price. The bank will conduct a final review of your credit and documentation.

Step 7: Review and Sign the Loan Agreement

This is a critical moment. Before signing anything, thoroughly read the entire loan agreement. Pay close attention to:

-

The final APR: Ensure it matches what was discussed.

-

Loan term: Confirm the number of months.

-

Total loan amount: Verify it aligns with the car’s price minus your down payment.

-

Monthly payment amount: Make sure it’s what you expected.

-

Any additional fees: Look for origination fees, late payment penalties, or early payoff penalties.

-

Prepayment penalties: Ensure there are none if you plan to pay off the loan early.

-

Pro Tip: Don’t hesitate to ask questions if anything is unclear. A reputable bank will be happy to explain every clause. Once signed, you are legally bound by the terms.

Common Mistakes to Avoid When Getting a Car Loan

Even with the best intentions, applicants can fall into common traps. Being aware of these pitfalls can save you time, money, and stress during your quest for car loan approval.

- Not checking your credit score: As mentioned, this is foundational. Surprises on your credit report can derail your application or lead to higher rates.

- Focusing only on the monthly payment: While important, a low monthly payment achieved through an excessively long loan term can mean paying significantly more interest overall. Always consider the total cost of the loan.

- Applying to too many lenders at once (without proper timing): While shopping around is good, spreading out applications over months can lead to multiple hard inquiries, negatively impacting your score. Bundle your applications within a short timeframe (e.g., two weeks) to minimize the impact.

- Ignoring the fine print: Loan agreements are legal documents. Skipping over the terms and conditions can lead to unexpected fees or unfavorable clauses.

- Underestimating additional costs: Remember, the car’s purchase price isn’t your only expense. Factor in insurance, registration, maintenance, and fuel.

- Not getting pre-approved: Going into a dealership without your own financing puts you at a disadvantage.

What If Your Credit Isn’t Perfect? Strategies for Getting a Car Loan

Having a less-than-perfect credit score doesn’t necessarily mean you can’t get a car loan. It just means the process might require a bit more strategy and patience. Getting a car loan from a bank with bad credit is possible, but you’ll likely face higher interest rates.

Here are some strategies:

- Make a Larger Down Payment: This significantly reduces the bank’s risk and shows your commitment, making you a more attractive borrower. It can also help offset a lower credit score.

- Find a Co-signer: A co-signer with good credit can vouch for your loan, making the bank more confident in lending to you. Just ensure both parties understand the full responsibility involved, as the co-signer is equally liable for the debt.

- Improve Your Credit First: If your need for a car isn’t immediate, take time to improve your credit score. Pay down existing debts, make all payments on time, and avoid new credit applications. Our blog post on Understanding Your Credit Score: A Comprehensive Guide offers in-depth advice on this.

- Consider a Less Expensive Vehicle: A lower loan amount is less risky for the bank, potentially making approval easier even with imperfect credit.

- Explore Credit Unions: While this article focuses on banks, credit unions are member-owned and sometimes more flexible with loan qualifications, especially for members with a history.

- Be Realistic: Understand that with a lower credit score, you might not get the best rates. Focus on securing a loan you can afford and then work to refinance it later once your credit improves.

The Post-Approval Phase: What Happens Next?

Once your bank car loan is approved and signed, you’re ready to drive off! But the journey doesn’t end there. Understanding the post-approval phase is just as important as the application itself.

The bank will typically disburse the funds directly to the dealership or seller. You will then receive your official loan documents, including your payment schedule. It’s crucial to understand your due dates and payment methods to avoid late fees and maintain a good payment history. Many banks offer automatic payment options, which can be a convenient way to ensure you never miss a payment.

Over time, as you make consistent, on-time payments, your credit score will likely improve. This opens up opportunities for refinancing your car loan. If interest rates drop or your credit score significantly improves, you might be able to refinance for a lower APR, reducing your monthly payments or the total interest paid over the life of the loan. This is a smart move to continuously optimize your financial situation.

Pro Tips for a Smooth Car Loan Journey

- Build a Relationship with Your Bank: If you have an existing relationship with a bank, start your loan inquiry there. They might offer better rates or more personalized service due to your established history.

- Negotiate, Negotiate, Negotiate: Whether it’s the car price or the loan terms, don’t be afraid to negotiate. Your pre-approval gives you leverage.

- Consider the Total Cost: Always look at the total amount you’ll pay over the life of the loan, not just the monthly payment. A slightly higher monthly payment for a shorter term can save you thousands in interest.

- Protect Your Investment: Don’t forget about comprehensive auto insurance. Many banks require specific coverage levels for the duration of the loan to protect their collateral.

- Future Financial Goals: Think about how this car loan fits into your broader financial picture. Will it impact your ability to save for a house, retirement, or other significant goals?

Conclusion: Drive Away with Confidence

Getting a car loan from a bank can seem like a daunting task, but with the right knowledge and preparation, it can be a smooth and rewarding experience. By understanding what banks look for, meticulously preparing your finances, and following our step-by-step guide, you significantly increase your chances of car loan approval and securing favorable terms.

Remember, the key lies in being informed, proactive, and patient. Don’t rush the process, shop around for the best car loan rates, and always read the fine print. Armed with this comprehensive guide, you are well-equipped to navigate the world of auto financing and confidently drive away in your new vehicle, knowing you’ve made a smart financial decision. Your journey to owning a car starts with smart financing, and a bank loan can be the perfect starting line.

External Resource: For more detailed information on auto loans and consumer protection, visit the Consumer Financial Protection Bureau (CFPB) at www.consumerfinance.gov.