Navigating the Road to Your New Ride: Getting a Car Loan Through Your Bank (The Ultimate Guide)

Navigating the Road to Your New Ride: Getting a Car Loan Through Your Bank (The Ultimate Guide) Carloan.Guidemechanic.com

The dream of a new car often comes with the practical reality of securing financing. For many, the most trusted and familiar path leads right back to their own bank. Getting a car loan through your bank can offer a unique blend of convenience, potential savings, and peace of mind.

This comprehensive guide will demystify the entire process, from preparing your finances to driving off the lot. We’ll explore why your bank might be your best option, what to expect, and how to maximize your chances of approval. Our goal is to equip you with the knowledge to secure the best possible terms for your next vehicle.

Navigating the Road to Your New Ride: Getting a Car Loan Through Your Bank (The Ultimate Guide)

Why Your Bank Could Be Your Best Bet for a Car Loan

When considering an auto loan, your existing banking relationship offers several compelling advantages. It’s not just about convenience; it’s about leveraging a history of trust and potentially unlocking better deals. This familiarity can streamline the application process significantly.

Your bank already has a detailed understanding of your financial history, including your income, spending habits, and existing accounts. This established relationship can often lead to a more personalized and efficient loan experience. Many banks prioritize their existing customers, sometimes offering exclusive rates or more flexible terms.

Moreover, dealing with an institution you already trust can alleviate much of the stress associated with large financial commitments. You’re likely familiar with their customer service and online platforms, making the entire journey feel more secure. It’s a comfortable choice for a significant financial decision.

Understanding the Landscape of Bank Car Loans

Before diving into the application, it’s crucial to grasp the fundamental concepts of car loans offered by banks. This knowledge empowers you to make informed decisions and compare offers effectively. Not all car loans are created equal, and understanding the jargon is key.

Most bank car loans are secured loans, meaning the car itself acts as collateral. If you default on the loan, the bank has the right to repossess the vehicle. This security typically allows banks to offer lower interest rates compared to unsecured personal loans.

Key terms you’ll encounter include the Annual Percentage Rate (APR), which represents the true annual cost of your loan, including interest and fees. The loan term is the duration over which you’ll repay the loan, usually measured in months. Understanding these figures is paramount to calculating your total financial commitment.

Pro tips from us: Don’t just focus on the monthly payment. A lower monthly payment might sound appealing, but it often comes with a longer loan term and a higher total interest paid over the life of the loan. Always consider the total cost of the loan.

Your Step-by-Step Guide to Getting a Car Loan Through Your Bank

Securing a car loan through your bank is a structured process that, when followed diligently, significantly improves your chances of approval and favorable terms. Let’s break down each crucial step to ensure you’re well-prepared.

Step 1: Financial Self-Assessment & Budgeting

Before you even glance at a car dealership, take a deep dive into your own finances. This initial step is perhaps the most critical for responsible car ownership. You need a clear picture of what you can realistically afford without stretching your budget too thin.

Start by calculating your disposable income – what’s left after all essential monthly expenses. Then, consider a comfortable monthly car payment that won’t jeopardize your other financial goals. Remember to factor in not just the loan payment, but also insurance, fuel, maintenance, and potential registration fees. These often overlooked costs can quickly add up.

Based on my experience, many people overlook these additional costs, leading to financial strain down the road. A general rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) shouldn’t exceed 10-15% of your net income. Determine a realistic down payment you can comfortably afford, as a larger down payment reduces the amount you need to borrow and can lead to better loan terms.

Step 2: Check Your Credit Score and Report

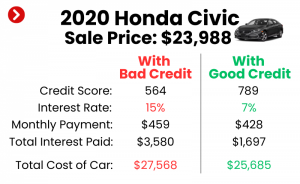

Your credit score is a major determinant in whether your bank approves your loan and what interest rate you receive. It’s essentially a financial report card that tells lenders how reliably you’ve managed debt in the past. A higher score signals less risk to the bank.

Before applying, obtain a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) annually. You can do this through AnnualCreditReport.com. Review these reports thoroughly for any errors or inaccuracies that could negatively impact your score. Disputing and correcting errors can take time, so start this process early.

Common mistakes to avoid are not checking your credit score beforehand. Knowing your score allows you to anticipate the kind of rates you might qualify for and gives you time to address any issues. If your score isn’t where you’d like it to be, focus on paying bills on time, reducing existing debt, and avoiding new credit applications in the months leading up to your car loan application.

Step 3: Gather Necessary Documentation

Banks require specific documents to verify your identity, income, and financial stability. Having these ready in advance will significantly expedite your application process. Being organized demonstrates responsibility and efficiency.

Typically, you’ll need proof of identity (driver’s license, passport), proof of income (pay stubs, tax returns, employment verification letters), and proof of residence (utility bill, lease agreement). Banks may also request bank statements to confirm your financial habits and existing debt statements to assess your debt-to-income ratio.

Pro tips from us: Create a dedicated folder, either physical or digital, for all your loan documents. This ensures nothing is missed and makes it easy to submit your application promptly. Being prepared minimizes back-and-forth with the bank and speeds up approval.

Step 4: Get Pre-Approval from Your Bank

One of the most powerful steps you can take is to get pre-approval for a car loan from your bank. Pre-approval means your bank has conditionally agreed to lend you a specific amount of money at a certain interest rate, pending final verification. It’s a game-changer in the car buying process.

Pre-approval provides you with immense negotiating power at the dealership. You walk in knowing exactly how much you can spend and what your interest rate will be, effectively making you a cash buyer. This allows you to focus solely on negotiating the car’s price, rather than getting entangled in financing discussions that might inflate costs. It also streamlines the dealership experience, as you already have your financing in place.

To apply for pre-approval, you’ll submit many of the documents gathered in Step 3. Your bank will perform a "hard inquiry" on your credit, which might slightly lower your score temporarily, but the benefits far outweigh this minor impact. The pre-approval letter will typically state the loan amount, estimated interest rate, and the term of the loan.

From a professional perspective, pre-approval is your strongest weapon in the car buying journey. It sets a clear budget and eliminates the stress of securing financing while under pressure at the dealership. It empowers you to make a calm, informed decision.

Step 5: Compare Offers and Understand Terms

Even if you have a strong relationship with your primary bank, it’s always wise to compare their pre-approval offer with those from other banks or credit unions. Competition among lenders can often lead to better rates and terms. Don’t assume your bank automatically has the best deal.

When comparing offers, look beyond just the interest rate. Scrutinize the APR, which includes all fees, giving you a truer cost. Compare the loan term and how it impacts your total interest paid. Also, look for any hidden fees, prepayment penalties, or late payment charges. Some lenders may offer incentives like no application fees or lower rates for specific vehicle types.

Common mistakes to avoid are rushing into the first offer you receive or only focusing on the monthly payment. A lower monthly payment often means a longer loan term, which can result in paying significantly more interest over time. Read the fine print carefully and ask questions about anything you don’t understand. Ensure you are comfortable with every aspect of the loan agreement before committing.

Step 6: Finalize Your Loan and Purchase Your Car

Once you’ve chosen the best loan offer, the final steps involve formalizing the agreement and purchasing your vehicle. This is where your pre-approval really pays off, as much of the heavy lifting is already done.

If you’re buying from a dealership, present your pre-approval letter. This tells them you’re serious and have financing secured. The dealership might try to offer their own financing, but with your bank’s pre-approval in hand, you have a benchmark. Only consider their offer if it genuinely beats your bank’s terms. Ensure that all the paperwork from the dealership matches the details of your loan agreement.

If buying from a private seller, your bank will guide you through the process of transferring funds and titling the vehicle. They will typically provide a check or direct deposit the loan amount. Make sure all title and registration documents are correctly processed to reflect the new ownership and lien holder. This step ensures a smooth transition to car ownership.

Pro tips from us: Don’t feel pressured at the dealership to accept add-ons or services you don’t need. Stick to your budget and your pre-approved loan terms. Take your time to review all final documents before signing.

Step 7: What to Do If Your Loan is Denied

A loan denial can be disheartening, but it’s not the end of your car-buying journey. It’s an opportunity to understand what went wrong and improve your financial standing. Banks are legally required to provide you with the reason for denial.

Common reasons for denial include a low credit score, high debt-to-income ratio, insufficient income, or errors on your credit report. Request the specific reasons from your bank. This feedback is invaluable for future applications.

Based on my expertise, a denial isn’t the end of the road. If denied, focus on addressing the issues identified. Work on improving your credit score, reducing existing debt, or saving for a larger down payment. Consider applying with a co-signer who has good credit, or explore alternative lenders like credit unions that might have more flexible criteria. Sometimes, simply waiting a few months and improving your financial health can make all the difference.

Advantages of Bank Car Loans vs. Other Lenders

While various lenders offer car loans, choosing your bank often comes with distinct advantages that can lead to a smoother, more beneficial experience. It’s about more than just interest rates; it’s about the overall relationship and transparency.

Banks typically offer competitive interest rates, especially for customers with a good credit history and an existing relationship. This established trust can sometimes unlock rates that independent lenders or dealerships might not match. The convenience of managing your car loan alongside your checking, savings, and other accounts is also a significant plus, simplifying your financial life.

Moreover, banks are highly regulated institutions, which generally means greater transparency and consumer protection. You’re less likely to encounter hidden fees or predatory lending practices compared to some less reputable lenders. Their customer service departments are usually well-established and accessible, providing a reliable point of contact for any questions or issues throughout your loan term. This provides a level of comfort and security often unmatched by other lending avenues.

Common Pitfalls and How to Avoid Them

Even with the best intentions, car loan applicants can fall into common traps. Being aware of these pitfalls allows you to navigate the process more effectively and secure the most favorable terms. Vigilance is key to a successful loan experience.

One significant pitfall is not reading the fine print. Loan agreements can be complex, and overlooking clauses related to fees, penalties, or early repayment terms can lead to unexpected costs. Always take the time to understand every section of the document before signing.

Another common mistake is only focusing on the monthly payments. While a low monthly payment seems attractive, it often means a longer loan term and ultimately, paying significantly more in interest over the life of the loan. Prioritize the total cost of the loan, including interest and fees, rather than just the immediate monthly outflow.

Ignoring additional fees is also a trap. These can include origination fees, application fees, or documentation fees. While some are unavoidable, others can be negotiated or avoided by choosing a different lender. Finally, applying for too many loans at once can negatively impact your credit score, as multiple hard inquiries signal higher risk to lenders. Be strategic and targeted with your applications, especially after securing a pre-approval.

Conclusion: Driving Towards Your Dream Car with Confidence

Getting a car loan through your bank offers a well-trodden path to vehicle ownership, characterized by familiarity, potential savings, and robust support. By taking a methodical approach – from assessing your finances and checking your credit to securing pre-approval and comparing offers – you empower yourself to make the best financial decision.

Remember, the goal isn’t just to get a loan, but to get the right loan that fits your budget and financial goals. Leveraging your existing banking relationship can provide a significant advantage, offering competitive rates, clear terms, and the peace of mind that comes with a trusted institution. You are now equipped with the knowledge and strategies to navigate this process with confidence.

Don’t let the excitement of a new car overshadow the importance of smart financial planning. By following the steps outlined in this guide, you can secure favorable financing and drive away in your new vehicle knowing you’ve made a well-informed decision. Start your journey today and experience the benefits of getting a car loan through your bank!