Navigating the Road to Your Next Ride: Everything You Need to Know About a $15,000 Car Loan

Navigating the Road to Your Next Ride: Everything You Need to Know About a $15,000 Car Loan Carloan.Guidemechanic.com

Securing a car loan can feel like a complex journey, especially when you’re aiming for a specific amount like $15,000. This isn’t just a number; it represents the gateway to a reliable vehicle, personal freedom, and a significant financial commitment. For many, a $15,000 car loan hits a sweet spot, providing enough capital for a good quality used car or a basic new model without overwhelming monthly payments.

In this comprehensive guide, we’ll strip away the jargon and provide you with an in-depth roadmap to successfully acquiring and managing a $15,000 car loan. We aim to equip you with the knowledge and confidence to make informed decisions, ensuring you drive away with a deal that truly benefits you. Our goal is to make this process as clear and straightforward as possible, from initial planning to final repayment.

Navigating the Road to Your Next Ride: Everything You Need to Know About a $15,000 Car Loan

Why a $15,000 Car Loan is a Popular Choice

A $15,000 car loan often represents an accessible entry point into vehicle ownership for many individuals. This amount is frequently sufficient to purchase a dependable used car, perhaps just a few years old, that still offers modern features and good reliability. It strikes a balance between affordability and quality, making it a highly sought-after loan value.

Furthermore, for those seeking a brand-new vehicle, $15,000 can cover the cost of certain entry-level models or serve as a substantial down payment on a more expensive car. This flexibility makes it an attractive option for a wide range of buyers with varying needs and budgets. It’s a sweet spot that allows for significant purchasing power without the burden of an excessively large debt.

Understanding the Fundamentals of Any Car Loan

Before diving into the specifics of a $15,000 car loan, it’s crucial to grasp the basic components that define any auto financing agreement. These core elements will dictate the overall cost and manageability of your loan, regardless of the principal amount. Familiarizing yourself with these terms will empower you to analyze loan offers critically.

The principal amount is simply the total sum of money you borrow, in this case, $15,000. This is the base figure upon which all interest calculations are made. Understanding this initial sum is the first step in comprehending your overall financial obligation.

Interest is the cost of borrowing money, expressed as a percentage of the principal. This percentage is typically presented as an Annual Percentage Rate (APR), which includes the interest rate plus any additional fees charged by the lender. A lower APR directly translates to less money paid over the life of the loan.

The loan term refers to the duration over which you agree to repay the loan, usually expressed in months. Common terms range from 36 to 72 months, or even longer. While a longer term can lead to lower monthly payments, it often results in paying more interest over time, increasing the total cost of the loan.

Key Factors Influencing Your $15,000 Car Loan Approval and Terms

Securing favorable terms for your $15,000 car loan hinges on several critical financial factors. Lenders assess these elements to determine your creditworthiness and the level of risk involved in lending to you. Understanding and optimizing these factors before you apply can significantly improve your chances of approval and secure a better deal.

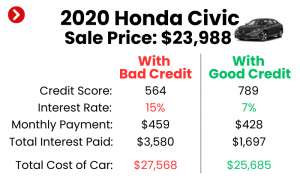

Your credit score is arguably the most influential factor. It’s a three-digit number that summarizes your credit history, reflecting your ability to manage debt responsibly. A higher credit score (typically 700+) indicates a lower risk to lenders, often qualifying you for the best interest rates and loan terms.

Lenders also closely examine your income and employment stability. They want to ensure you have a consistent and sufficient income stream to comfortably afford your monthly loan payments. A stable work history, ideally with the same employer for several years, reassures lenders of your financial reliability.

Your debt-to-income (DTI) ratio is another crucial metric. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover new loan payments, making you a more attractive borrower. Lenders typically prefer a DTI below 36% to 43%.

A down payment demonstrates your financial commitment to the purchase and reduces the amount you need to borrow. Even a small down payment on a $15,000 car loan can lower your monthly payments and potentially secure a better interest rate. It also provides an immediate equity cushion, reducing the risk of being "upside down" on your loan.

The type of vehicle you intend to purchase also plays a role. Lenders consider the car’s age, mileage, and market value. Newer, more reliable vehicles often qualify for better loan terms compared to older cars, which might be perceived as higher risk due to potential maintenance issues or faster depreciation.

Different Avenues for Your $15,000 Car Loan

When seeking a $15,000 car loan, you have several options for lenders, each with its own advantages and disadvantages. Exploring these different avenues can help you find the most suitable and competitive financing for your needs. It’s wise to compare offers from multiple sources before making a commitment.

Dealership Financing is often the most convenient route, as you can arrange the loan at the same place you buy the car. Dealerships work with various lenders and can sometimes offer competitive rates, especially through manufacturer-backed programs. However, convenience can sometimes come at the cost of the absolute best rates, as their primary goal is to sell you a car.

Banks and Credit Unions are traditional sources of auto loans. Banks typically offer a wide range of loan products and competitive rates, especially if you have a strong credit history. Credit unions, being non-profit organizations, are known for offering some of the most favorable interest rates to their members, often beating what traditional banks can provide.

Online Lenders have grown significantly in popularity. They offer a streamlined application process, often with quick approval decisions. Many online lenders specialize in specific credit profiles, including those with less-than-perfect credit, making them a good option for a wider range of borrowers. Their competitive nature can also lead to attractive rates.

Based on my experience coaching clients through car purchases, exploring all three avenues is a pro tip. You might find that a credit union offers the best rate, but an online lender provides unparalleled convenience, or a dealership has a special promotional APR. Always get multiple quotes.

Preparing for Your $15,000 Car Loan Application

Preparation is key to a smooth and successful car loan application process. By taking proactive steps before you even set foot in a dealership or click "apply" online, you can significantly increase your chances of approval and secure more favorable terms for your $15,000 car loan. This groundwork will save you time, stress, and potentially money.

First, establish a realistic budget. Beyond the monthly loan payment, consider the total cost of car ownership, including insurance, fuel, maintenance, and registration fees. A common mistake is focusing solely on the monthly payment without factoring in these additional, crucial expenses. Based on my experience, many people get caught off guard by these hidden costs.

Next, check your credit report and score. You are entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year. Review your report for any errors or inaccuracies that could negatively impact your score. Correcting these can boost your score and improve your loan prospects.

Gather all necessary documentation in advance. This typically includes proof of identity (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bill), and banking information. Having these documents ready streamlines the application process and prevents delays.

Finally, consider getting pre-approved for your $15,000 car loan. Pre-approval involves a preliminary check by a lender that gives you a clear idea of how much you can borrow, at what interest rate, and for what term. This provides significant bargaining power at the dealership, allowing you to focus on the car price rather than getting swayed by financing offers.

The Application Process for Your $15,000 Car Loan: Step-by-Step

Once you’ve done your homework, the application process for a $15,000 car loan becomes much more manageable. While the exact steps might vary slightly depending on the lender, a general framework applies. Understanding this sequence will help you navigate each stage with confidence.

The first step is to submit your application, either online, in person at a bank or credit union, or through a dealership. This form will request personal information, employment details, income figures, and your desired loan amount. Be sure to fill out all sections accurately and completely to avoid any processing delays.

After submission, the lender will perform a credit check. This involves pulling your credit report from one or more credit bureaus to assess your creditworthiness. This is typically a "hard inquiry," which may temporarily lower your credit score by a few points, but the impact is usually minimal and short-lived.

Next, the lender will review your financial information, including your income, debt-to-income ratio, and employment history. They are looking to confirm that you have the capacity to repay the $15,000 loan comfortably. This thorough review ensures they are making a responsible lending decision.

Finally, you will receive a decision. If approved, the lender will present you with a loan offer outlining the principal amount, interest rate (APR), loan term, and monthly payment. This is your opportunity to review all the terms carefully and ensure they align with your financial goals.

Decoding Your $15,000 Car Loan Offer

Receiving a loan offer is an exciting step, but it’s crucial to understand every detail before signing on the dotted line. Don’t let excitement overshadow critical financial scrutiny. For a $15,000 car loan, paying attention to the fine print can save you hundreds, if not thousands, of dollars over the loan’s life.

The Annual Percentage Rate (APR) is arguably the most important number to focus on. It represents the true annual cost of borrowing money, including the interest rate and any associated fees. Comparing APRs from different lenders is the most accurate way to find the cheapest loan. A lower APR directly reduces your total repayment amount.

Your total cost of the loan extends beyond the $15,000 principal. It includes all the interest you will pay over the loan term, plus any origination fees or other charges. Always ask the lender for the total amount you will repay over the life of the loan. This comprehensive figure provides a complete picture of your financial commitment.

Naturally, the monthly payment is a critical figure for budgeting. Ensure this amount fits comfortably within your monthly financial plan. Remember, while a lower monthly payment from a longer loan term might seem appealing, it often means paying significantly more in interest over time. Balance affordability with the overall cost.

Pro tips from us: Never rush this step. Take the loan offer home, read it carefully, and don’t hesitate to ask questions about anything you don’t understand. If a lender pressures you to sign immediately, that’s a red flag.

Smart Strategies for Negotiating Your $15,000 Car Loan

Many people believe car loan terms are set in stone, but that’s a common misconception. There’s often room for negotiation, especially if you come prepared. Approaching the negotiation process for your $15,000 car loan with confidence and knowledge can lead to significantly better terms.

The most powerful negotiation tool you have is pre-approval. When you walk into a dealership with a pre-approved loan offer from a bank or credit union, you’re essentially telling them you already have financing. This forces the dealership to compete with that offer, giving you leverage to negotiate a lower APR or better terms.

Always negotiate the car price and the loan terms separately. A common mistake is to lump them together, which can make it harder to see where you might be overpaying. First, agree on the car’s purchase price, and only then discuss financing options. This clear separation ensures you get the best deal on both fronts.

Don’t be afraid to walk away if the terms aren’t favorable. There are always other lenders and other vehicles. Showing that you’re willing to explore other options gives you significant power. This willingness to disengage can often prompt a lender or dealer to sweeten their offer.

Consider making a larger down payment if possible. Even an extra few hundred dollars can reduce the principal, lower your monthly payments, and potentially qualify you for a better interest rate. A larger down payment reduces the lender’s risk, which they might reward with more attractive terms.

Common Mistakes to Avoid When Getting a $15,000 Car Loan

While the path to a $15,000 car loan can be straightforward, certain missteps can turn it into a financial headache. Being aware of these common pitfalls can help you steer clear of expensive mistakes and ensure a more positive borrowing experience. Learning from others’ errors is a smart strategy.

One of the biggest mistakes is failing to shop around for multiple loan offers. Settling for the first offer you receive, especially from a dealership, can mean missing out on significantly lower interest rates available elsewhere. Always compare at least three to four offers before making a decision.

Another frequent error is focusing solely on the monthly payment without considering the total cost of the loan. A longer loan term might reduce your monthly outflow, but it almost always increases the total interest paid over the life of the loan. Prioritize the overall cost, not just the monthly figure.

Getting swayed by add-ons and extended warranties at the dealership is another common trap. While some might offer value, many are overpriced and can significantly inflate your $15,000 loan amount, leading to more interest and higher payments. Carefully evaluate each add-on’s necessity and cost.

Failing to read the fine print of your loan agreement is a critical mistake. Every clause, fee, and condition matters. Understand prepayment penalties, late payment fees, and any other terms that could impact you. Based on my experience, assumptions about loan terms are a leading cause of future regret.

Lastly, borrowing more than you can truly afford, even if approved, sets you up for financial strain. Just because a lender approves you for $15,000 doesn’t mean that’s the ideal amount for your budget. Always stick to your carefully planned budget, prioritizing affordability over aspiration.

Pro Tips for a Smooth $15,000 Car Loan Experience

Beyond avoiding mistakes, there are proactive steps you can take to make your $15,000 car loan journey exceptionally smooth and beneficial. These insights, drawn from years of financial guidance, aim to optimize your experience from start to finish. Implementing these tips can lead to significant savings and peace of mind.

A critical pro tip is to improve your credit score before applying. Even a modest improvement can shift you into a better rate tier, saving you hundreds of dollars in interest. Pay down existing debts, dispute errors on your credit report, and avoid applying for new credit in the months leading up to your car loan application.

Consider making a larger down payment than initially planned. Even an additional $500 or $1,000 can significantly reduce the amount you finance, lowering your monthly payments and the total interest paid. It also shows lenders you are a serious and responsible borrower.

Choose the shortest loan term you can comfortably afford. While longer terms offer lower monthly payments, they dramatically increase the total interest you pay. Opting for a 36- or 48-month term over 60 or 72 months, if your budget allows, will save you considerable money in the long run.

Don’t forget to factor in the cost of car insurance when budgeting. Your insurance premium can vary significantly based on the car you choose, your driving history, and your location. Get insurance quotes for specific vehicles before finalizing your purchase to ensure the total cost of ownership remains affordable.

– This article can help you budget for and select the right insurance policy for your new car.

Responsibly Managing Your $15,000 Car Loan

Securing your $15,000 car loan is just the beginning; responsible management is key to a positive financial outcome. A well-managed loan can improve your credit score and save you money, while poor management can lead to financial distress. These strategies will help you stay on track.

Always make your loan payments on time, every single month. Late payments can result in fees, negatively impact your credit score, and accrue additional interest. Setting up automatic payments from your bank account is an excellent way to ensure you never miss a due date.

Keep an eye on interest rates. If rates drop significantly after you’ve secured your loan, or if your credit score has substantially improved, consider refinancing your $15,000 car loan. Refinancing could secure you a lower interest rate, reducing your monthly payment or the total cost of the loan.

– Explore if refinancing is the right move for your current financial situation.

Consider making extra payments whenever possible. Even small additional payments can help reduce the principal faster, thereby cutting down on the total interest you pay over the loan’s life. Some borrowers aim to pay an extra half-payment every two weeks, effectively making an extra full payment each year.

Understand your loan’s early payoff terms. While most car loans don’t have prepayment penalties, it’s always wise to confirm this in your loan agreement. Knowing you can pay off your $15,000 loan early without penalty gives you more financial flexibility.

What If Your $15,000 Car Loan Application Is Denied?

A loan denial can be disheartening, but it’s not the end of the road. Understanding why your $15,000 car loan application was rejected is the first step toward improving your chances for future approval. Lenders are legally required to provide you with a reason for denial.

The most common reasons for denial include a low credit score, insufficient income, a high debt-to-income ratio, or an unstable employment history. Sometimes, it could also be due to errors on your credit report that you weren’t aware of. Addressing these specific issues is crucial.

If denied, request the exact reason from the lender. They must provide you with an Adverse Action Notice. Use this information to identify areas for improvement. Based on my experience, this feedback is invaluable for future applications.

Take proactive steps to improve your creditworthiness. This could involve paying down existing debts, especially those with high interest rates, or disputing any inaccuracies on your credit report. Building a stronger credit profile takes time, but it’s an investment in your financial future.

Consider alternative financing options. If a traditional loan isn’t feasible, explore options like a co-signer with good credit, who can strengthen your application. Some lenders also specialize in loans for individuals with less-than-perfect credit, though these typically come with higher interest rates.

You can also consider revising your car choice to a less expensive model, which would require a smaller loan. A lower loan amount reduces the perceived risk for lenders and might make approval easier. Start smaller and build your credit for a larger loan in the future.

Conclusion: Driving Forward with Confidence

Embarking on the journey to secure a $15,000 car loan requires careful planning, informed decision-making, and a clear understanding of the financial landscape. By grasping the fundamentals of car financing, diligently preparing your application, and wisely managing your loan, you’re not just buying a car; you’re building a stronger financial future.

Remember, the goal is not just to get approved, but to secure terms that are truly beneficial and sustainable for your personal finances. With the comprehensive knowledge and pro tips shared in this guide, you are now well-equipped to navigate the complexities of auto financing with confidence and achieve your goal of owning a reliable vehicle. Drive smart, not just hard.

For more detailed information on consumer financial protection and borrowing responsibly, consider visiting the Consumer Financial Protection Bureau (CFPB) website, a trusted external source for valuable financial literacy resources. External Link: Consumer Financial Protection Bureau – Auto Loans